WOO X Research: Hyperliquid Whales in the Spotlight – A Look at Mechanisms Across Perp DEXs

TechFlow Selected TechFlow Selected

WOO X Research: Hyperliquid Whales in the Spotlight – A Look at Mechanisms Across Perp DEXs

Hyperliquid whale movements draw significant attention.

Recently, address 0xf3f496c9486be5924a93d67e98298733bb47057c opened a 50x leveraged long position on ETH via Hyperliquid, achieving floating profits exceeding $2 million at its peak. Due to the massive size of the position and DeFi's inherent transparency, this whale’s actions have drawn widespread attention across the crypto market. Most expected his next move to be either adding more positions to amplify gains or closing out to secure profits. Unexpectedly, he chose a different strategy: withdrawing margin to extract profits while forcing an upward adjustment of the liquidation price. Ultimately, the whale triggered self-liquidation, securing $1.8 million in profit.

What impact did this action cause? It harmed HLP's liquidity.

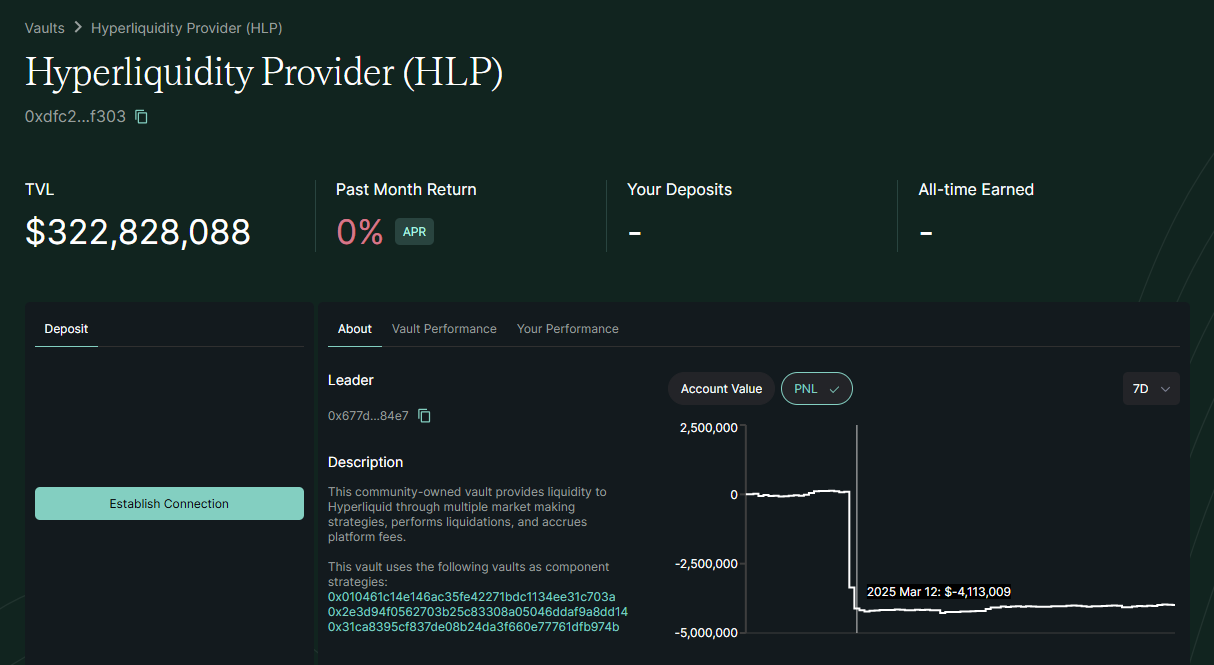

HLP (Hyperliquid Pool) serves as Hyperliquid’s primary market-making mechanism, earning revenue through funding fees and liquidation gains. All users can also contribute liquidity to HLP.

Given the whale’s excessive profits, a standard full position closeout would have caused severe counterparty liquidity shortages. Instead, by intentionally triggering liquidation, the resulting loss was absorbed by the HLP pool, which lost approximately $4 million in just one day on March 12.

This incident highlights serious challenges facing Perpetual DEXs, indicating that liquidity pool mechanisms must evolve. Taking this opportunity, WOO X Research will analyze and compare the core mechanisms of leading Perp DEXs—Hyperliquid, Jupiter Perp, and GMX—and explore how similar attacks can be prevented.

Reference: https://app.hyperliquid.xyz/vaults/0xdfc24b077bc1425ad1dea75bcb6f8158e10df303

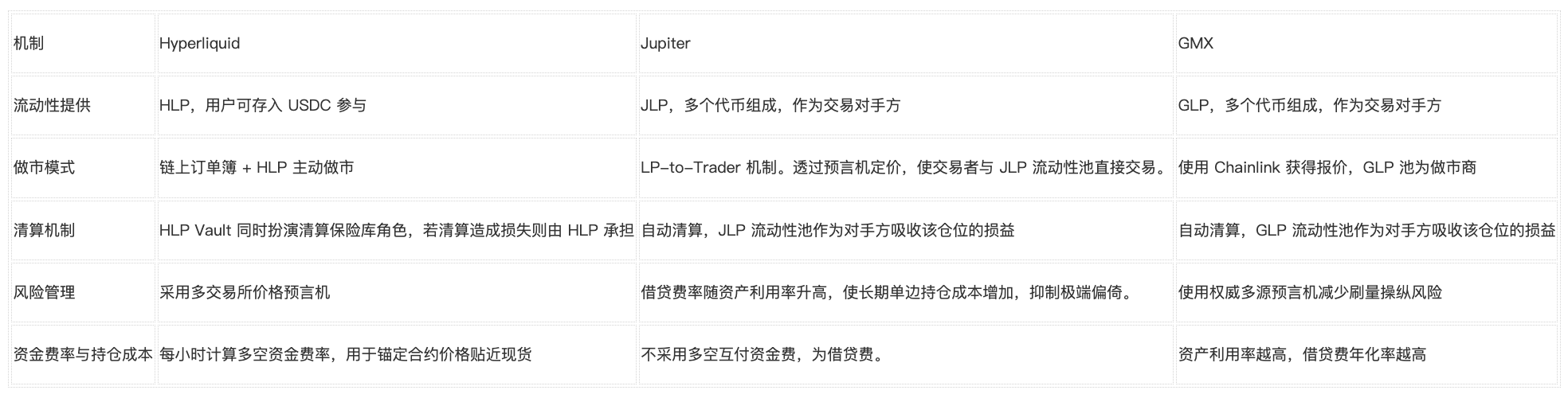

Hyperliquid

-

Liquidity Provision: Funded by the community liquidity pool HLP (Hyperliquid Pool). Users deposit assets such as USDC into the HLP Vault to become platform market makers. Additionally, users may create their own “Vaults” to participate in market-making revenue sharing.

-

Market Making Model: Employs high-performance on-chain order book matching, delivering a centralized exchange-level experience. The HLP vault acts as a market maker, placing orders on the order book to provide depth and handle unmatched portions, reducing slippage. Prices are referenced from external oracles to ensure listing prices closely reflect global markets.

-

Liquidation Mechanism: Liquidations trigger when minimum margin requirements (typically starting at 20%) are breached. Any sufficiently capitalized user can participate in liquidations, taking over undercollateralized positions. The HLP Vault also serves as an insurance fund; if liquidations result in losses, HLP absorbs them (as occurred in this attack).

-

Risk Management: Utilizes multi-exchange price oracles updated every three seconds to prevent manipulation from a single market causing incorrect pricing. In response to extreme whale positions, minimum margin requirements for certain positions have been raised to 20%, reducing the impact of large forced liquidations on the pool. Open participation in liquidations enhances decentralization, though risk is concentrated within individual Vaults. A drawback is that as a relatively new proprietary chain, it hasn’t undergone long-term stress testing, and past incidents involved significant forced liquidation losses.

-

Funding Rates and Holding Costs: Funding rates between longs and shorts are calculated hourly to anchor perpetual contract prices to spot. When longs outweigh shorts, longs pay funding to shorts (and vice versa), preventing prolonged price divergence. For net platform exposures exceeding HLP capacity, Hyperliquid mitigates risk by increasing margin requirements and potentially dynamically adjusting funding rates. Beyond funding fees, there are no additional overnight interest charges, though higher leverage increases funding fee burdens.

Jupiter

-

Liquidity Provision: Liquidity is provided by the multi-asset JLP (Jupiter Liquidity Pool), which includes index assets such as SOL, ETH, WBTC, USDC, and USDT. Users mint JLP by depositing assets, with JLP serving as the counterparty absorbing risks from leveraged trades.

-

Market Making Model: Abandons traditional order books in favor of an innovative LP-to-Trader model. Trades execute against the JLP pool based on oracle pricing, offering near-zero slippage execution. Advanced features like limit orders are supported, but all trades are effectively filled by the pool at oracle-determined prices.

-

Liquidation Mechanism: Fully automated liquidation occurs when a position’s margin ratio falls below maintenance levels (e.g., <6.25%). Smart contracts automatically close positions using oracle prices. The JLP pool absorbs the resulting PnL; in cases of bankruptcy, remaining collateral goes to the pool. Users can adjust collateral during a position to modify liquidation prices, but over-withdrawal brings the liquidation price closer to the current market price, increasing liquidation risk.

-

Risk Management: Oracle-based pricing ensures contract prices track spot closely, preventing internal manipulation. High TPS on Solana reduces settlement lag risks, though network instability could affect trading and liquidations. To deter malicious manipulation, the platform imposes limits on total exposure per asset (e.g., maximum leverage cap). Borrowing rates increase with asset utilization, raising holding costs for prolonged one-sided positions and discouraging extreme imbalances. To date, traders have been net losers, allowing steady growth in JLP funds.

-

Funding Rates and Holding Costs: No traditional funding rate mechanism exists, as Jupiter Perp does not facilitate direct long-short payments. Instead, it uses a borrow fee system, where interest accrues hourly based on borrowed asset utilization within the pool and is deducted from margin. Longer holding periods or higher asset utilization lead to greater accumulated interest, gradually pushing the liquidation price toward the market price. This design constrains long-term unilateral positioning and avoids persistent funding rate imbalances.

GMX

-

Liquidity Provision: Multi-asset index pool GLP (GMX Liquidity Pool) provides liquidity, including BTC, ETH, USDC, DAI, and others. Users deposit assets to mint GLP tokens, making GLP the universal counterparty that bears all trade PnLs.

-

Market Making Model: No traditional order book. Instead, trades are executed against the GLP pool using oracle prices. GMX uses Chainlink decentralized oracles for market pricing, enabling "zero-slippage" execution. The GLP pool functions as a unified market maker, maintaining balance via price impact fees that adjust asset composition within the pool to preserve depth.

-

Liquidation Mechanism: Fully automated. Position values are calculated using Chainlink index prices. When margin ratios fall below maintenance thresholds (approximately 1.25x initial margin), automatic liquidation triggers. Contracts immediately close the position; user collateral first covers pool losses, with any remainder returned or allocated to insurance. As the counterparty, the GLP pool directly incurs losses or gains the bankrupt trader’s remaining margin.

-

Risk Management: Relies on authoritative, multi-source oracles to minimize wash-trading and manipulation risks, avoiding erroneous liquidations due to isolated volatility. Past exploits saw traders manipulate prices externally and arbitrage GMX’s zero-slippage mechanism. In response, GMX imposed maximum position caps on vulnerable assets (e.g., $2 million cap on AVAX). These caps, combined with dynamic fee structures (higher borrowing costs with increased utilization), limit leverage risks. Additionally, 70% of trading fees are rewarded to GLP holders, incentivizing LPs to absorb losses sustainably.

-

Funding Rates and Holding Costs: GMX V1 does not implement mutual long-short funding payments. Instead, it charges a borrow fee (0.01% per hour based on asset usage ratio), paid directly to the GLP pool. Regardless of direction, all holders pay holding interest, incorporated into PnL calculations. As asset utilization rises, annualized borrow rates increase (potentially exceeding 50%), economically penalizing prolonged one-sided congestion. Under this model, perpetual prices remain tightly pegged to spot (zero slippage), eliminating traditional funding rate imbalances—but the pool assumes risk during sharp price movements.

Hyperliquid vs. Jupiter vs. GMX Quick Comparison Table

Conclusion: The Inevitable Path for Decentralized Derivatives Exchanges

Conclusion: The Inevitable Path for Decentralized Derivatives Exchanges

This attack exploited key characteristics of Perp DEXs: transparency and code-enforced rules.

The overall attack strategy was simple: build an extremely large profitable position and exploit weaknesses in the exchange’s liquidity structure.

To prevent future occurrences, platforms must restrict user position sizes—by limiting leverage multiples and increasing margin requirements. Indeed, Hyperliquid has already announced reductions in maximum leverage for BTC and ETH to 40x and 25x respectively, along with a 20% increase in required margin transfer ratios, aiming to prevent excessively large positions.

Beyond these measures, what else could Hyperliquid implement? ADL – Automatic Deleveraging.

When the risk reserve (HLP) cannot absorb further losses from liquidated positions, an Automatic Deleveraging (ADL) mechanism activates to limit additional drawdowns on the reserve. The core idea is that losing positions are offset against opposing profitable or highly leveraged positions (“targeted for deleveraging”), with both positions closed simultaneously. While ADL protects the HLP treasury, profitable positions may be forcibly closed early, capping their upside potential.

However, all these solutions focus on limiting per-account exposure. Determined actors could still circumvent these rules by creating multiple accounts. Platforms could combat this via address clustering analysis to detect and ban coordinated accounts—preventing Sybil attacks (one reason why CEXs require KYC). Yet such measures conflict with a core tenet of DeFi: permissionless access for anyone to use decentralized financial services.

The best solution lies in the natural maturation of Perp DEX protocols—thicker liquidity over time raises the cost of attacks until they become unprofitable. Current vulnerabilities are simply part of the necessary evolution of the sector.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News