Bitcoin: The Ultimate Safe-Haven Solution for Long-Term Thinkers?

TechFlow Selected TechFlow Selected

Bitcoin: The Ultimate Safe-Haven Solution for Long-Term Thinkers?

A contemplation on risk, time, and the future of money.

By: Daii

Hopefully today's topic hasn't shocked you too much. Because reality has slapped the premise of this article right in the face:

Gold briefly surpassed $3,000 per ounce today (March 16), setting a new all-time high.

Bitcoin, after falling from its peak of $102,000, plunged below $77,000 and now hovers around $84,000.

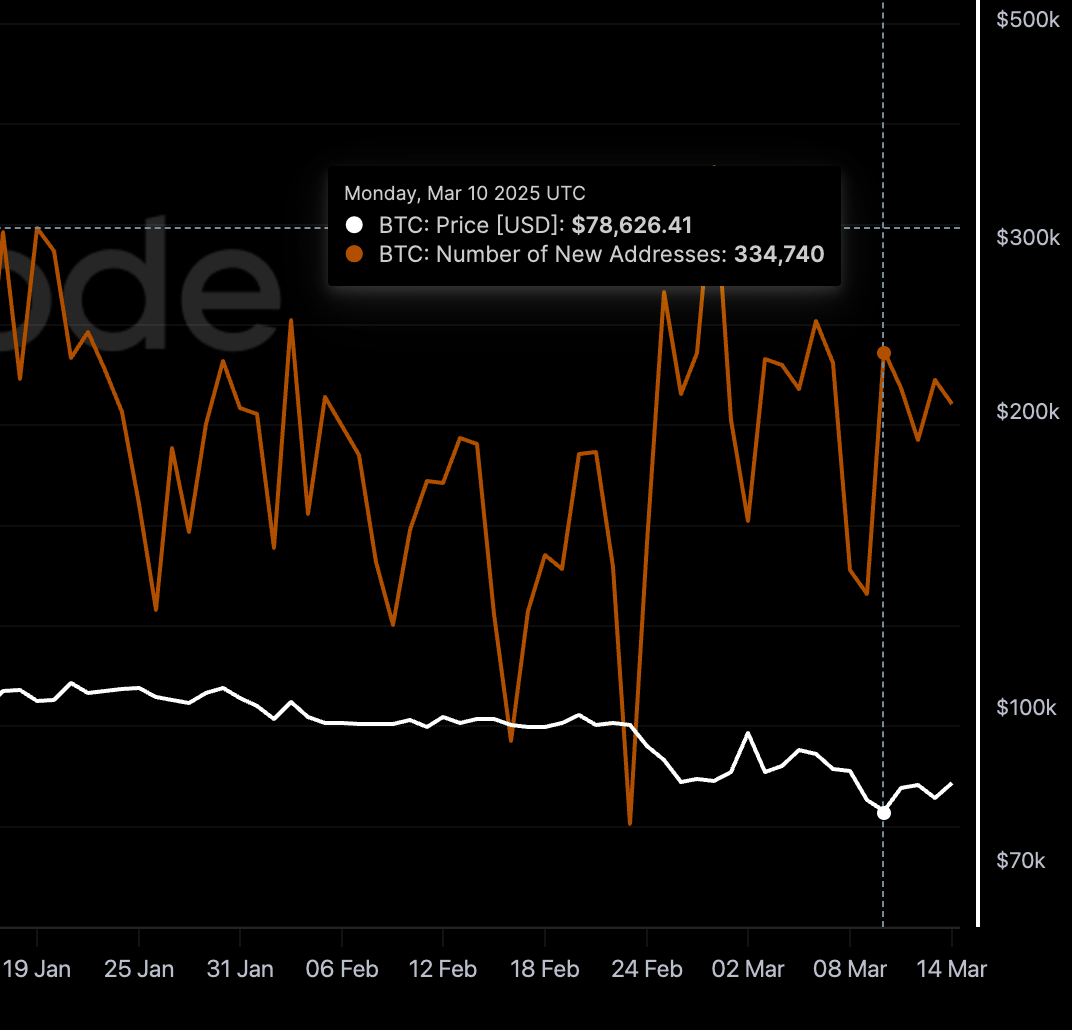

This stark contrast makes it seem obvious that gold is a better safe-haven asset than Bitcoin. So let me ask you—would you sell your Bitcoin now to buy gold? Frankly, I wouldn’t, and I suspect you wouldn’t either. In fact, not only are existing holders unlikely to sell, but more newcomers keep joining steadily. Take a look at the chart below.

The chart shows that even when Bitcoin hit its recent low near $78,000, there were still 330,000 new addresses created that day. Clearly, behind this apparent contradiction lies a hidden truth. Your decision not to sell Bitcoin for gold is correct—and today, I’ll reveal the real reason why. No more suspense—the answer is right in the title, minus the question mark:

Bitcoin: The ultimate safe-haven solution for long-term investors.

Of course, simply stating the answer isn’t enough. I must also explain the reasoning. And as a science communication column, we should practice what we preach. At the end, I’ll provide actionable steps to implement this philosophy. If you identify as a long-term thinker—not someone chasing overnight riches through leverage—then read on.

First, let’s understand: What exactly is a safe-haven asset?

1. What Is a Safe-Haven Asset?

A safe-haven asset, by definition, refers to an asset that maintains or even increases in value during market turmoil, economic uncertainty, or other events that typically cause traditional investments (like stocks or bonds) to decline. These assets are often seen as “safe harbors,” protecting investors’ wealth during times of risk.

Traditionally, safe-haven assets share several core characteristics:

-

Low volatility or negative correlation: Ideal safe-haven assets remain relatively stable during market turbulence and may even move inversely to high-risk assets like equities. When stocks fall, these assets rise, providing effective hedging.

-

Store of value: They must preserve purchasing power over time, resisting erosion from inflation. Investors prioritize stability over short-term gains.

-

Liquidity: The ability to quickly buy or sell at fair prices is crucial. This ensures flexibility when adjusting portfolios under pressure.

-

Historical validation: Assets proven to perform well during past crises gain investor trust and acceptance.

The three traditional pillars of safe-haven assets:

-

Gold: As a millennia-old hard currency, gold’s safe-haven status was cemented by its 70x surge after the collapse of the Bretton Woods system in 1971. Its physical scarcity (approximately 205,000 tons mined globally) and inflation-resistant properties (roughly 7.3% annualized return over the past 50 years) make it a classic crisis hedge.

-

Government bonds: U.S. Treasuries, labeled "risk-free," rely on national credit—but with U.S. debt surpassing $35 trillion in 2024 and real yields negative for 18 consecutive months, they expose an underlying inflation trap.

-

Safe-haven currencies: The U.S. dollar, as the world’s reserve currency, held 59% of foreign reserves during the 2020 pandemic crisis; the Japanese yen benefits from ultra-low rates (-0.1%), while the Swiss franc relies on banking secrecy to maintain its status.

Historically, gold has been viewed as the quintessential safe-haven asset. During stock market downturns or geopolitical tensions, investors flock to gold, driving up its price. Although gold produces no interest or dividends, its scarcity and historical recognition as a store of value make it a key tool for preserving wealth amid uncertainty.

However, financial innovation and evolving investor preferences have broadened the concept of “safe-haven” assets. Newer assets now show potential in certain environments—even if they don’t meet all traditional criteria. That’s precisely why we’re discussing Bitcoin’s role in risk mitigation today.

The most critical point above is “investor risk preference.” Risk perception varies widely among individuals. For instance, I don’t use leverage to get rich quickly, so Bitcoin’s wild price swings aren’t risks—or opportunities—to me.

So, what does risk mean to you?

2. The Relativity of Risk

Let’s expand our view and examine how risk shifts across geography and time.

Imagine living in different countries—you’d experience vastly different risk pressures. In Zimbabwe during hyperinflation, local currency became nearly worthless. Holding ZWD was the biggest risk; residents scrambled to convert savings into stable foreign currencies or physical goods. Contrast this with Switzerland, where economic stability means people focus more on long-term wealth preservation than short-term devaluation fears.

This illustrates the spatial relativity of risk—the same asset carries different risk profiles depending on the economy.

Time also reshapes our understanding of risk. Assets once deemed risky can become mainstream over decades, while traditionally “safe” assets may develop new vulnerabilities.

You might assume such dramatic drawdowns belong to Bitcoin or another crypto—but no, this is gold.

Gold’s safe-haven status isn’t constant. It fluctuates based on economic, political, and monetary factors. While it performs well during some recessions, its track record isn’t flawless.

This panoramic chart clearly shows gold experienced major corrections in the 1970s, 1980s, and 2010s.

Now, resetting our temporal coordinates: What should long-term investors do today?

First, clarify: Long-termists don’t treat wealth accumulation as life’s primary goal. We aim for meaningful pursuits beyond work—I choose blockchain education; you may choose something else. But we share one thing: we don’t want to obsess over money. We seek a set-and-forget investment approach, with modest return expectations and zero appetite for unnecessary risk.

Yet, as long as we live on Earth, one risk is unavoidable.

3. The Risk of Fiat Currency

Fiat money derives its legal tender status solely from government decree and central bank authority. Modern paper currencies like the dollar, euro, and yen are fiat—they’re not backed by physical commodities like gold. Their value rests entirely on public trust in issuing institutions and national economic strength.

3.1 Devaluation

The fatal flaw of fiat is infinite supply. To stimulate growth, manage debt, or combat downturns, governments and central banks routinely increase money supply. While mild inflation can help short-term, sustained inflation erodes purchasing power over time.

The U.S. dollar has lost 98% of its purchasing power since detaching from gold in 1971. In 2024, the Fed’s quantitative easing to address the debt crisis caused M2 money supply to surge 23%, pushing real inflation to 8.5%—far above the 2% target. This “inflation tax” creates a global “time black hole” for cash holders: real returns have been negative for 18 straight months, implying an annual 6.3% loss in buying power.

Worse, a vicious cycle links sovereign debt and fiat credibility: global government debt now stands at 356% of GDP, with U.S. debt exceeding $35 trillion. The myth of “risk-free” Treasuries is crumbling. Japan’s central bank holds over 52% of its own debt, contributing to a 15% plunge in the yen against the dollar. This “debt monetization” mechanism is pushing the entire fiat system toward collapse.

Beyond devaluation, there’s another critical personal sovereignty risk: banks can freeze or restrict your accounts at any time.

3.2 Freezing & Restrictions

Imagine you’ve saved hard-earned money in a bank account. Legally, it’s yours. But in practice, your control isn’t absolute. Banks—as intermediaries—can limit or freeze access due to legal investigations, regulatory compliance, or internal errors.

This indirect control is a latent risk of holding fiat. Your wealth exists digitally, yet ultimate authority lies with states and financial institutions.

2013 Cyprus capital controls: To prevent systemic collapse, Cyprus imposed strict limits: daily withdrawals capped at €300. Shockingly, depositors with over €100,000 faced up to 60% losses—partially converted into bank equity. These controls lasted nearly two years, severely restricting citizens’ access to their own funds.

2011–2015 Argentina FX controls: To curb capital flight, Argentina restricted dollar purchases. A thriving black market emerged, leaving many unable to obtain USD for trade or savings. Grain exporters hoarded hundreds of millions in revenue, waiting for favorable exchange rates—a clear sign of how FX controls distort economic activity.

2008–2017 Iceland capital controls: After its 2008 financial meltdown, Iceland banned large-scale capital outflows for nearly a decade. These measures aimed to stop massive fund withdrawals that could crash the króna. Controls weren’t fully lifted until 2017.

2017 Venezuela withdrawal limits: Amid deepening crisis, Venezuela limited ATM withdrawals to 10,000 bolívares (~$1). Machines often ran dry, forcing people to queue for hours to withdraw just 20,000 bolívares at tellers—insufficient for basic needs.

These real-world cases prove that during crises, governments may restrict or freeze bank accounts to maintain stability. For long-termists seeking financial autonomy, this is a serious concern.

In extreme cases—bank failures or systemic collapses—your deposits could be at risk. Deposit insurance helps, but coverage has limits.

For those valuing full financial sovereignty, this issue demands attention. Now, we can finally answer: Why is Bitcoin a better safe-haven asset for long-term investors?

4. Why Long-Termists Should Choose Bitcoin

First, eliminate fiat—including dollars, yen, and euros—from consideration.

4.1 Fiat vs. Bitcoin

We’ve seen that the U.S. dollar, post-gold standard, has dramatically lost purchasing power. Bitcoin, by contrast, features a fixed maximum supply. The cap of 21 million coins is hardcoded—immutable.

Bitcoin introduces the first mathematically enforced monetary contract in human history: halving every four years, reaching a final supply of 21 million by 2140. This programmed deflation directly opposes fiat’s endless printing. Consider 2024:

-

Dollar: Fed expanded its balance sheet by 23%; M2 exceeded $22 trillion; real inflation hit 8.5%.

-

Bitcoin: Post-fourth halving, annual inflation dropped to 0.9%—lower than gold’s 1.7%.

We also discussed fiat’s freezing risks. Bitcoin’s decentralized nature directly mitigates this. No single entity controls the network. Transaction records are transparent and immutable on the blockchain. Only the private key holder can access funds—no third party can freeze or seize them without consent.

4.2 Bonds vs. Bitcoin

Sovereign bonds, especially U.S. Treasuries, have long been considered “risk-free” assets, backed by national credit. During market stress, capital flows into them for safety.

But for today’s long-termist, this assumption warrants caution—especially given current macroeconomic realities.

As noted, U.S. debt exceeded $35 trillion in 2024. With real yields negative for 18 months, can these “safe” assets truly hedge inflation? Negative real returns mean you’re losing purchasing power—even in supposedly secure instruments. For long-term wealth preservation, this is unacceptable.

Global sovereign debt now equals 356% of global GDP. In Japan, the central bank owns over 52% of national debt—contributing to a sharp drop in the yen. This trend of “debt monetization” undermines the long-term safety of traditional bonds. Allocating significant capital to such assets exposes investors to growing systemic risk.

In contrast, Bitcoin’s value doesn’t depend on any single nation’s solvency. While it carries its own risks, it offers an alternative uncorrelated with legacy finance—an attractive proposition for those wary of sovereign debt collapse.

Yes, bonds offer short-term stability during market shocks. But long-termists focused on decades ahead need more than temporary calm. They need assets that resist inflation and offer genuine long-term appreciation. Despite volatility, Bitcoin’s scarcity, decentralization, and digital-native potential make it a stronger candidate than traditional bonds for enduring wealth protection.

4.3 Gold vs. Bitcoin

Gold delivered ~7.3% annualized returns over the past 50 years—solid performance for a store of value. But Bitcoin’s long-term track record is far more compelling.

According to backtesting data from Curvo.eu (as of March 2025):

-

Past five years: Bitcoin returned ~1,067.5%; gold returned ~88.8%. Bitcoin’s average annual return: 63.5%, vs. gold’s 13.5%.

-

Past ten years: Bitcoin soared 51,259.5%; gold rose ~142.7%. Annualized: Bitcoin ~86.7%, gold ~9.3%.

Nasdaq reported in September 2024 that Bitcoin was the best-performing asset globally over the previous decade, averaging 693% annual returns—versus ~5% for gold.

Post-fourth halving, Bitcoin’s inflation rate is 0.9%—just 53% of gold’s 1.7%. Bitcoin becomes increasingly scarce over time.

Second, portability and storage costs limit gold. Storing large quantities requires physical space, security, and expense. Bitcoin, being digital, incurs almost zero storage cost and can be transferred instantly worldwide—a major advantage in our globalized era.

Bitcoin also wins in divisibility. It can be split down to eight decimal places (satoshis), enabling micro-transactions. Gold’s division and verification are costly and impractical.

Transparency and verifiability are higher with Bitcoin. All transactions are recorded on a public ledger—anyone can audit them, reducing fraud risk. Gold’s purity and authenticity can be difficult to verify.

Market size-wise, gold’s $18.5 trillion valuation still dwarfs Bitcoin’s ~$2 trillion. But Galaxy Research forecasts Bitcoin could reach 20% of gold’s market cap by 2025—indicating strong growth expectations.

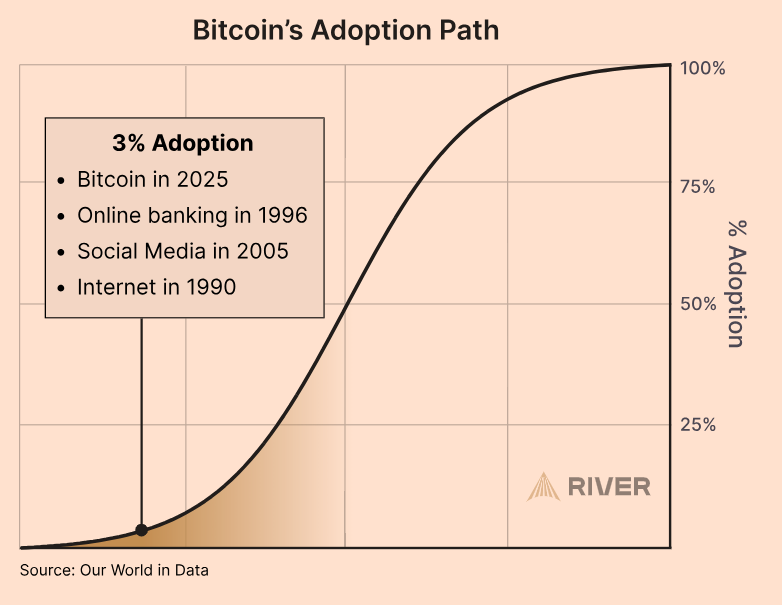

Finally, adoption matters. Gold is mature and widely accepted. Bitcoin, with just 3% adoption, remains early-stage—comparable to the internet in 1990, online banking in 1996, or social media in 2005, as I argued in *“Trends and Cycles: A Cold Look at Bitcoin’s ‘Pullback Moment.’”*

Long-termists choosing Bitcoin aren’t rejecting gold outright. They see Bitcoin as having greater potential to combat fiat debasement, protect personal wealth, and capture upside from the digital economy. We accept volatility today for potentially outsized returns tomorrow.

So how should long-termists invest in Bitcoin?

Keep living expenses aside, and start DCA.

5. Why DCA Is the Long-Termist’s Strategy

DCA stands for Dollar-Cost Averaging—a strategy of investing a fixed amount at regular intervals (e.g., weekly or monthly), regardless of price.

As discussed, Bitcoin is far more volatile than traditional safe-havens like gold or bonds. While we believe in its long-term value, short-term movements are unpredictable. Long-termists don’t chase quick profits—they focus on multi-year or multi-decade horizons. Hence, DCA is ideal.

DCA removes the pressure to “time the bottom.” No one can consistently predict market lows—even professionals fail. Long-termists know this. They care about trends, not timing. DCA lets them invest systematically without guessing entry points.

It also combats behavioral biases. People tend to FOMO-buy during rallies and panic-sell during dips. DCA enforces discipline, helping investors stay rational and committed to their long-term plan.

Data from 2015–2025 shows the power of DCA:

-

$100/month into Bitcoin: Total invested: $12,000; final value: $111,000; annualized return: 25%.

-

Same into S&P 500: Final value: $21,000; annualized return: 9.8%.

This gap stems from Bitcoin’s exponential growth. DCA in crypto is like “temporal arbitrage”—exchanging depreciating fiat for appreciating digital scarcity.

Bitcoin’s price history shows repeated deep drawdowns—but the long-term trend remains upward. An investor using DCA since inception would have achieved extraordinary returns, regardless of interim crashes. Past results don’t guarantee future ones, but DCA’s core benefit is risk diversification—it reduces the impact of poor timing on overall returns.

Long-termists seek simplicity. We don’t want to spend time analyzing charts or predicting markets. DCA fits perfectly. Once set, it runs automatically, freeing us to focus on careers, families, or contributions to society.

Therefore, for those who believe in Bitcoin’s long-term value and want a hands-off approach, DCA is ideal. You might wonder: What about uninvested cash? Simple: convert it to USD-pegged stablecoins. Here’s a beginner’s guide to stablecoins.

In crypto, DCA services are already mature and varied. You can buy Bitcoin on centralized exchanges and transfer to cold wallets. Here are two zero-knowledge guides: one on buying Bitcoin, another on sending it to cold storage.

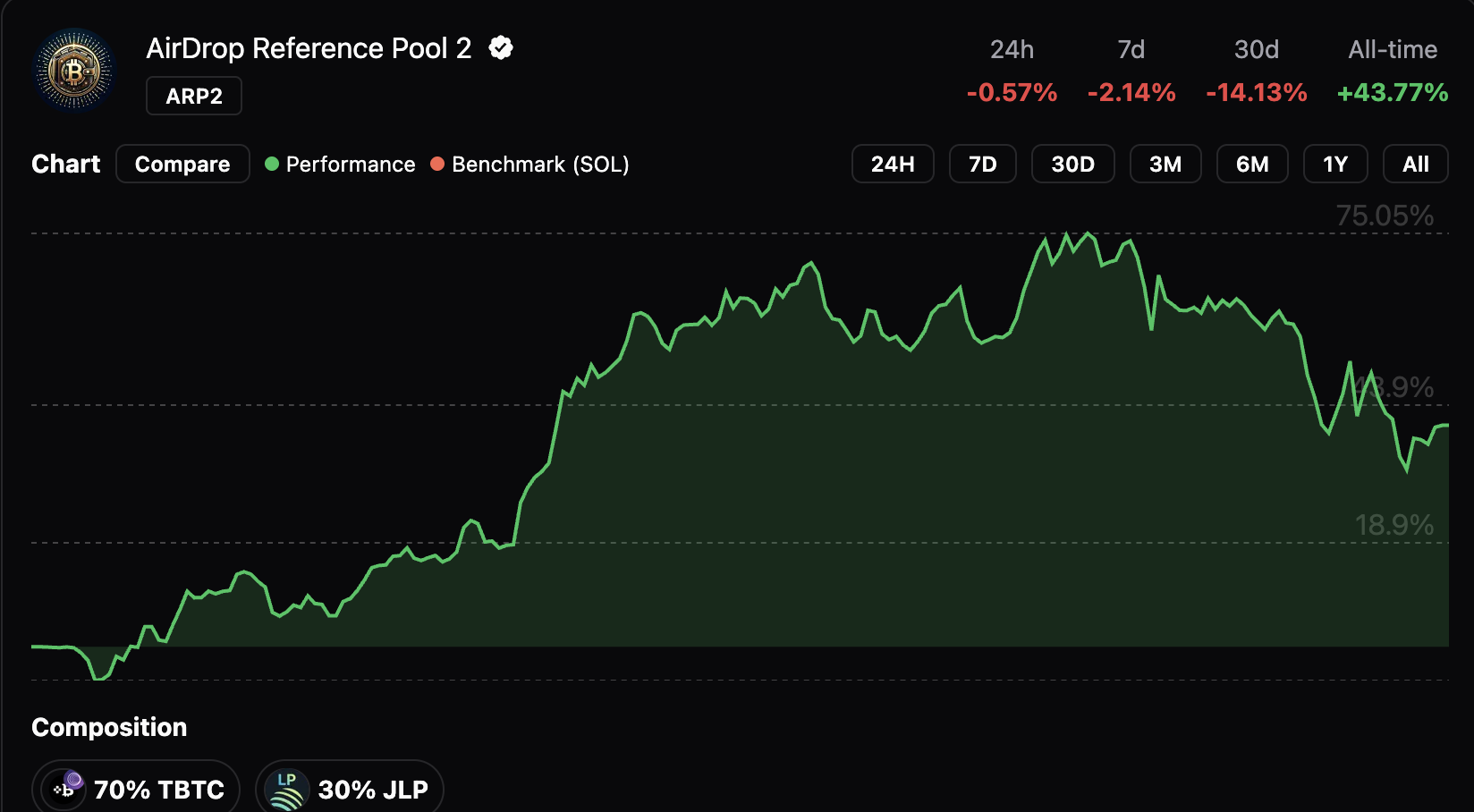

I recommend the ARP2 project by *Airdrop Reference*, because it allows Bitcoin DCA plus automatic rebalancing for extra yield. See detailed instructions here.

Even after Bitcoin’s recent plunge, ARP2 still shows a 43.77% return. Its only drawback: manual execution required for each contribution.

Conclusion: A Timeless Awakening of Value

In the epic of human money, gold spent a millennium building its “temple of value,” fiat wove a “mirage of liquidity” via state credit, and Bitcoin is now constructing a “digital Babel” with math and code. This debate over safe-haven assets is ultimately a contest between human nature and time—gold embodies ancient faith in physical scarcity, while Bitcoin signals a future consensus on digital absoluteness.

The long-termist’s choice is never mere asset substitution—it’s a redefinition of monetary sovereignty. When fiat’s “inflation tax” eats away wealth and gold’s “geopolitical chains” constrain mobility, Bitcoin offers a third path: transparency via “code as law,” and control via “private keys as sovereignty,” empowering individuals against systemic risk.

History proves: true safety isn’t fleeing volatility, but anchoring to the future.

Just as time reveals every bubble’s emptiness, it also illuminates enduring value. Bitcoin—the decentralized network built on mathematics and powered by consensus—is demonstrating, through scarcity, verifiability, and rising adoption, a capacity to outperform traditional safe-havens over time.

Choosing Bitcoin isn’t speculation. It’s a statement of belief in the future. It represents a new philosophy of wealth—one not dependent on centralized authorities, but returning value control to the individual. For long-termists unwilling to waste life chasing fleeting riches, Bitcoin may well be the key that unlocks a freer, safer financial future.

Let patience be our sail, long-termism our rudder, as we navigate toward shores of greater autonomy and enduring prosperity.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News