Stablecoins in constant expansion: the future of the financial system or just a passing phase?

TechFlow Selected TechFlow Selected

Stablecoins in constant expansion: the future of the financial system or just a passing phase?

Inevitable government pressure in the coming years will create opportunities for truly decentralized and private stablecoins.

Author: DC

Translation: TechFlow

Stablecoins account for two-thirds of on-chain transactions, whether used for exchanges, in DeFi, or simple transfers. Initially, stablecoins gained attention through Tether—the first widely adopted stablecoin—created to address banking restrictions faced by Bitfinex’s crypto users. Bitfinex launched USDTether, backed 1:1 by U.S. dollars. From there, Tether grew in popularity as traders leveraged USDT to more easily exploit arbitrage opportunities across exchanges. Tether transactions settle in just a few blocks (minutes), compared to wire transfers that take days.

Despite this crypto-native origin, stablecoin use has expanded far beyond its initial applications. They are now powerful tools for everyday money transfers and are increasingly used to earn yield and facilitate real-world transactions. Stablecoins represent about 5% of the total cryptocurrency market cap; when including companies managing these stablecoins or blockchains like Tron whose primary value stems from stablecoin usage, stablecoins account for nearly 8% of the entire crypto market cap.

Yet despite this remarkable growth, there remains relatively little discussion on why stablecoins have become so dominant and why tens of millions globally are replacing traditional financial systems with them. Even less is said about the numerous platforms and projects enabling this expansion, or the types of users interacting with them. This article will explain why stablecoins are so prevalent, who the key players are, the main user bases today, and how stablecoins may be shaping the next major evolution of money.

A Brief History of the Dollar

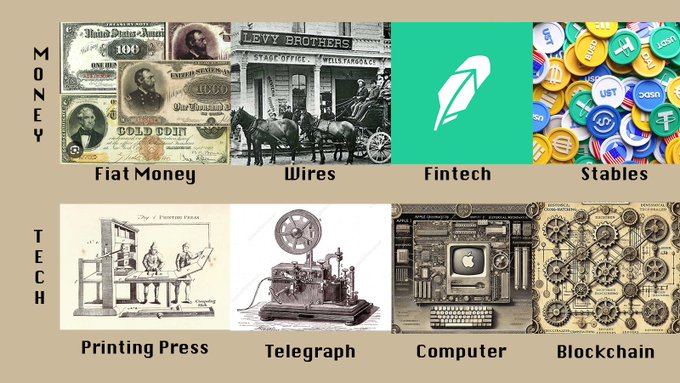

When someone says “money,” what comes to mind? Cash? The dollar? Grocery prices? Taxes? In all these cases, money serves as an agreed-upon unit of measurement to assign value to various, heterogeneous goods. Money began with shells and salt, evolved into copper, silver, gold, and now exists as the dollar/fiat.

Let’s focus on the dollar. The U.S. dollar/modern fiat currency (government-issued money not backed by commodities) has gone through multiple phases. In the U.S., paper notes (paper dollars issued by banks) were initially private. Banks could print their own currencies freely, similar to how Hong Kong’s HKD operates. After problems arose with this model, the government stepped in, legally pegging the dollar to gold.

In 1871, Western Union completed the first telegraphic transfer using the telegraph, enabling funds to move without transporting large volumes of physical cash. This was a massive breakthrough—it removed physical barriers to capital flow, making money—and the entire financial system—more efficient.

Brief timeline:

-

1913: The Federal Reserve System is established.

-

1971: Nixon ends the gold standard, decoupling the dollar from gold and allowing it to float freely.

-

1950: The first credit card is invented.

-

1973: The SWIFT payment network is created, enabling faster, more global dollar transactions.

-

1983: Stanford Federal Credit Union launches the first digital bank account.

-

1999: PayPal enables purely digital payments without requiring a bank account.

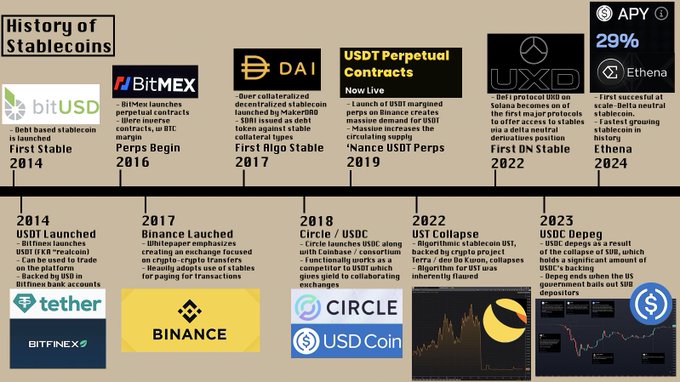

-

2014: Tether launches the first dollar-backed stablecoin, bringing us to where we are today.

The most important takeaway from this short history is that money—what it is and how we use it—is constantly evolving. Today, paying $20 via PayPal, Cash App, Zelle, or bank transfer is equally acceptable, although a standard bank transfer might raise eyebrows. In developing countries—and increasingly in developed ones too—stablecoins are becoming similarly normalized. Personally, I’ve paid salaries in stablecoins, transferred stablecoins to obtain cash, and am increasingly using them in place of bank accounts to save via protocols like @HyperliquidX's HLP, AAVE, Morpho, and of course @StreamDeFi.

We live in a world where existing financial systems disproportionately burden the most vulnerable consumers. Capital controls, monopolistic legacy banks, and high fees are the norm. In such environments, stablecoins are excellent tools for achieving financial freedom. They enable cross-border money transfers and are increasingly used for direct payments for goods. To understand how this happened so quickly, we must first examine why stablecoins outperform traditional financial products.

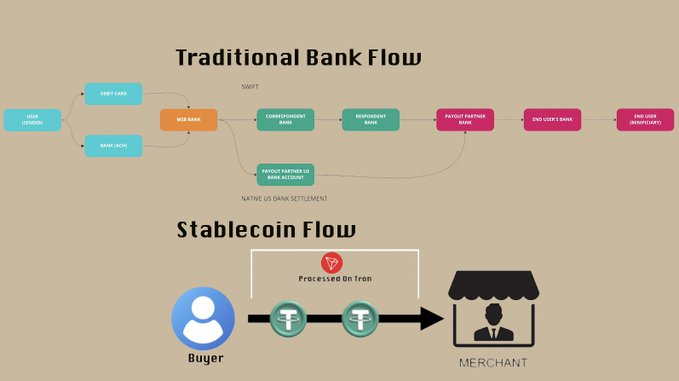

Stablecoins vs. Bank Transfers: A Tale of Two Worlds

At their core, stablecoins are tokens pegged to fiat currencies like the dollar or euro. Many readers of this article likely come from developed regions in North America, Europe, or Asia, where financial systems are relatively fast, smooth, and efficient. The U.S. has PayPal and Zelle, Europe has SEPA, and Asia has numerous fintech firms, especially Alipay and WeChat Pay. People in these regions can confidently deposit money in bank accounts without worrying about balances disappearing overnight or hyperinflation. Small transfers are processed quickly, and while large transfers may take longer, they’re never unmanageable. Most companies mandate local banking systems because they’re perceived as safer and easier than alternatives.

The rest of the world lives under a different reality. In Argentina, bank deposits have been seized multiple times, and the local currency is one of the worst-performing in history. In Nigeria, official and unofficial exchange rates coexist, and moving money in and out of the country can be extremely difficult—a situation ironically mirrored in Argentina. In the Middle East, bank balances can be arbitrarily frozen, leading most non-politically connected individuals to avoid keeping significant liquid assets in banks. Beyond the high risk of holding funds, sending money is often even harder. SWIFT transfers are expensive and cumbersome, and many lack traditional bank accounts due to the issues mentioned above. Alternatives like Western Union typically charge high fees for international transfers (see their fee calculator) and use official government exchange rates, which are worse than actual market rates—resulting in significant hidden costs.

Stablecoins allow people to hold funds outside local financial systems, as they are inherently global and move via blockchain rather than local bank servers. This reflects their origins—crypto exchanges struggled to access bank accounts, dealing with large deposits, withdrawals, and cross-exchange transfers. It’s well known that due to Japan’s overly bureaucratic banking system and capital controls, arbitrage opportunities existed between global and Japanese crypto prices.

In 2017, Binance released a whitepaper stating it would support only stablecoin-crypto trading pairs to ensure faster settlement. As a result, most trading volume shifted to stablecoin pairs. In 2019, Binance launched USDT perpetual derivative contracts, allowing users to post USDT instead of BTC as margin, further cementing this trend. Stablecoins became widely accepted as base assets among global crypto users—and now, this acceptance is beginning to extend beyond pure crypto use cases.

Let’s pause to compare stablecoins with fintech companies: primarily in terms of speed, innovative design, and focus on solving global financial problems. So far, fintech firms have mostly polished or masked the complex, opaque payment infrastructure users face.

Stablecoins represent the first major overhaul of the global financial system in 50 years. Their speed, reliability, and verifiability make them ideal for storing value and sending remittances without paying exorbitant fees (though admittedly at the cost of traditional safeguards offered by existing bureaucratic systems). Stablecoins can be seen as competing with cash and payment processors like Western Union—yet they are more durable and secure than cash. They won’t wash away in floods or get stolen during break-ins, and they’re easily convertible to local currency. Fees (depending on the blockchain) are typically under $2 and fixed—far below the variable fees charged by services like Western Union, which range from 0.65% to over 4%.

Once stablecoins gain broader acceptance and maturity, they inevitably fill gaps left unfilled by traditional providers in the global financial system. With this steady adoption comes an explosion of new services and more sophisticated products. @MountainUSDM brings RWA yields to numerous platforms in Argentina, while @ethena_labs enables users to earn money via delta-neutral strategies without relying on traditional banks or exchange custodians.

Stablecoins are increasingly used not just for payments, holding value, or selling local currency—but also to earn yield and process local payments. As this happens, stablecoins are becoming central to global financial planning and even corporate balance sheets. Many stablecoin users may not even realize they’re using crypto in the background—an indication of the huge strides companies have made recently in building products around stablecoins.

Companies Attracting Stablecoin Users

The main projects tied to stablecoins are the issuing companies themselves: @circle for USDC, @Tether_to for USDT, @SkyEcosystem for DAI/USD, and PYUSD—a product of @PayPal and @Paxos. There are many others I haven’t mentioned, but these are the primary stablecoins used for payments. Most of these companies have bank accounts, receive traditional wire transfers, and convert them into stablecoins for users.

Stablecoin issuers hold transferred funds and charge very low fees (typically 1–10 basis points). Users can now transfer these assets, while issuers earn “float revenue” (or “yield” for DeFi enthusiasts) on the assets held in their bank accounts. Trading firms are increasingly conducting large-scale dollar-stablecoin trades, especially as many exchanges crack down on users who only use them for free deposits and withdrawals. These trading firms often offer better pricing at scale, further enhancing stablecoins’ efficiency and competitive edge in environments where major trading firms openly compete to facilitate these flows. Meanwhile, stablecoin issuers earn interest on user funds, allowing them to profit from float revenue rather than charging users high fees.

It's worth noting that @SkyEcosystem (formerly Maker) is somewhat different. Sky uses multiple collateral types and reserves in other currencies to back its stablecoin USDS. Users deposit these collaterals and borrow SUSDS from the protocol at a set rate. Users can earn yield akin to a “risk-free rate” by depositing into the “Savings Rate Module,” lend out SUSDS on platforms like @MorphoLabs and @aave, or simply hold them in their accounts. This system offers both safer yield options and higher-risk alternatives.

Currently, most major stablecoin issuers are not directly consumer-facing.

Instead, they interact with consumers through various intermediary companies—similar to how MasterCard works with your bank but doesn’t engage with you directly.

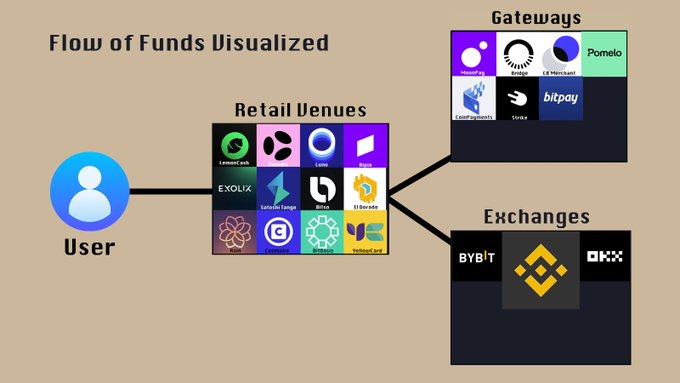

@LemonCash, @Bitso, @buenbit, @Belo, and @Rippio are names rarely seen on Crypto Twitter. Yet, just these Argentine exchanges alone serve over 20 million KYC’d users—half of Coinbase’s user base—despite Argentina’s population being only 1/7 that of the U.S. Last year, Lemon Cash processed around $5 billion in total transaction volume, much of it involving stablecoin-to-stablecoin or Argentine peso-to-stablecoin trades. Platforms like Lemon act as gateways for most non-P2P stablecoin transactions. These platforms also handle substantial crypto trading and stablecoin deposits, though most (except Rippio) don’t maintain order books for 90% of their markets—they operate by routing orders.

This is similar to Robinhood, which isn’t an exchange but routes orders through market makers to manage pricing. I refer to these platforms as “retail venues” because they focus on retail user experience and products, without owning exchange infrastructure. Just as Robinhood wouldn’t let market makers use its app or API (in fact, Robinhood bans users for excessive API requests), BuenBit or Lemon won’t either—because that’s simply not their target audience.

Meanwhile, we have actual blockchains—the places where stablecoins are sent and recorded. These are dominated by @justinsuntron's @trondao, @binance's Binance Smart Chain, @solana, and @0xPolygon. These chains are used for transferring value, not necessarily for interacting with DeFi or earning yield.

Ethereum still leads in TVL (Total Value Locked), but its high costs make it unattractive for most stablecoin transfers. 92% of USDT transactions occur on Tron, and about 96% of Tron transactions involve stablecoins, compared to 70% of value transfers on Ethereum. Additionally, new chains are emerging focused on efficiently and cheaply processing stablecoin transactions—most notably LaChain, a consortium formed by Ripio, Num Finance, SenseiNode, Cedalio, Buenbit, and FoxBit, targeting Latin American users and platforms. This illustrates how complex and refined the stablecoin landscape has become as it continues maturing.

As stablecoins grow in remittance use, they’re increasingly applied to local payments. This is where crypto payment portals and gateways come in—I define these as systems enabling conversion between stablecoins and fiat, or facilitating fiat payments. For example, merchants can “accept” crypto but actually sell it for USD into a bank account, or directly accept stablecoins.

Given that redeeming stablecoins always involves some friction—whether time or cost-related—many companies exist to simplify this process for users and platforms. These products range from relatively simple but highly useful tools like Pomelo (https://www.pomelogroup.com/, enabling crypto debit card transactions) to broader initiatives like @zcabrams' Bridge. Bridge allows seamless transfers between stablecoins, chains, and local currencies, drastically reducing friction for platforms and merchants—so much so that @stripe acquired Bridge to improve the efficiency of its payment system. Systems like Bridge currently exist because merchants don’t directly accept USDC or USDT, so gateways must convert stablecoins on behalf of users and typically provide liquidity in exchange for fees. As stablecoin payments expand—and given that many of these platforms charge lower fees than credit cards and traditional banking—volume in stablecoin-to-stablecoin transactions (between currency and final product) will increase as businesses adopt stablecoins to improve unit economics. This is how stablecoins begin shaping a post-bank-dominated payment world.

An increasing number of companies and projects are focusing on stablecoin applications and enabling current users to save on-chain or through some of the platforms mentioned above.

For instance, Lemon Cash offers an option to deposit funds into @aave to earn yield. @MountainUSDM's USDM earns yield on stablecoins and is integrated across multiple retail venues and exchanges in Latin America. Many retail venues and exchanges view stablecoin yield generation and associated fees as a potential source of stable income, helping smooth out revenue volatility caused by reliance on trading fees and bull-market volume—which plummets dramatically during bear markets (by an order of magnitude).

What’s Next for Stablecoins?

The non-crypto-specific use of stablecoins lies in international transfers and increasingly in payments. However, as stablecoin infrastructure continues improving, they are becoming ubiquitous, and savings may shift toward crypto—especially in developing countries, where this trend has already begun. A few weeks ago, @tarunchitra shared a story: a grocery store owner in Georgia accepts Georgian lari (local currency), converts it to USDT, earns interest, tracks balances in a physical ledger, and takes a cut from the interest. Payments are processed via Trust Wallet QR codes—remarkably, this occurs in a country with a relatively healthy banking system. In a country like Argentina, citizens are estimated to hold over $200 billion in cash outside the traditional financial system, according to the Financial Times. If half of that moved on-chain or into crypto, it would double the size of DeFi and increase stablecoin market cap by roughly 50%—and this is just one relatively small country. Others like China, Indonesia, Nigeria, South Africa, and India have vast informal economies or widespread distrust of banks.

As stablecoin usage grows, additional use cases will likely expand. Currently, stablecoins are only used for fully collateralized lending—one of the least common forms of credit globally. However, with new tools from Coinbase and others, KYC data can be used to extend capital to users, with non-repayment potentially leading to negative credit reporting. Stablecoin issuers are increasingly passing yield to holders—such as USDC’s 4.7% yield and Ethena’s USDe, which typically offers variable yields above 10%. Cross-fiat transaction volume is also rising: starting in one currency, converting to a dollar stablecoin, then into a third. As this continues, it becomes more efficient to use fiat-backed stablecoins pegged directly to underlying currencies to avoid paying fees twice. As more capital flows into stablecoins, an increasing array of products will become available on-chain and in crypto, helping drive mainstream adoption of daily crypto use.

Future Challenges

Finally, I want to highlight some under-discussed aspects in the stablecoin conversation. One is that nearly every stablecoin today relies on bank accounts to some extent—and banking systems aren’t always safe, as we saw in 2023 with USDC depegging and Silicon Valley Bank’s collapse.

Additionally, stablecoins are currently heavily used for money laundering. If you acknowledge that stablecoins help users circumvent capital controls and escape local currencies, you implicitly admit that such use constitutes money laundering in those jurisdictions. This is an open secret with major implications. Currently, neither Circle nor Tether allows “reissuance”—meaning if a user’s stablecoin balance is frozen due to legal action or funds deemed stolen, they cannot reclaim them—even with a court order. This practice is morally questionable at best and unsustainable long-term. Governments will increasingly demand or enforce regulations making stablecoins subject to seizure. This could potentially lead to CBDCs (Central Bank Digital Currencies) replacing stablecoins, though I’ll explore this in a future article.

Mounting government pressure in the coming years will create opportunities for truly decentralized and private stablecoins that can continue operating fully decentralized and immune to government intervention. I may write a deeper follow-up piece exploring this darker side of stablecoins, as it’s a broad and complex topic.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News