How did the house dump in this round? See which pitfalls you've fallen into?

TechFlow Selected TechFlow Selected

How did the house dump in this round? See which pitfalls you've fallen into?

Staking, repurchase, one-sided pools, contracts...

Author: shushu, BlockBeats

The market has been declining continuously, and many altcoins have even reached a point where they can't fall any further. Many believe that a bear market has arrived. Periods of market correction are often times when risks are concentrated and released, but they also contain opportunities for investors to enhance their understanding and build strength. Reviewing this market cycle, the offloading strategies employed by various market manipulators have been remarkably diverse, with carefully designed distribution tactics worth thorough analysis.

Traditional market manipulation theory suggests that manipulators generally go through four stages: accumulation, markup, washout, and distribution. However, the core principle has always been precise control over the emotions and behaviors of market participants. Through price fluctuations and the passage of time, manipulators subtly influence retail investors' decisions, ultimately maximizing their own profits.

So, in such a complex and ever-changing market environment, how can retail investors effectively identify signs of manipulator distribution? And how can they strengthen their risk awareness to avoid falling into traps? BlockBeats has summarized typical distribution tactics based on community discussions—including one-sided liquidity pools, fake buyback announcements, spot position control combined with futures short liquidation, and high-yield staking schemes—for readers' reference.

One-Sided Liquidity Pools: Empty-Handed Profits

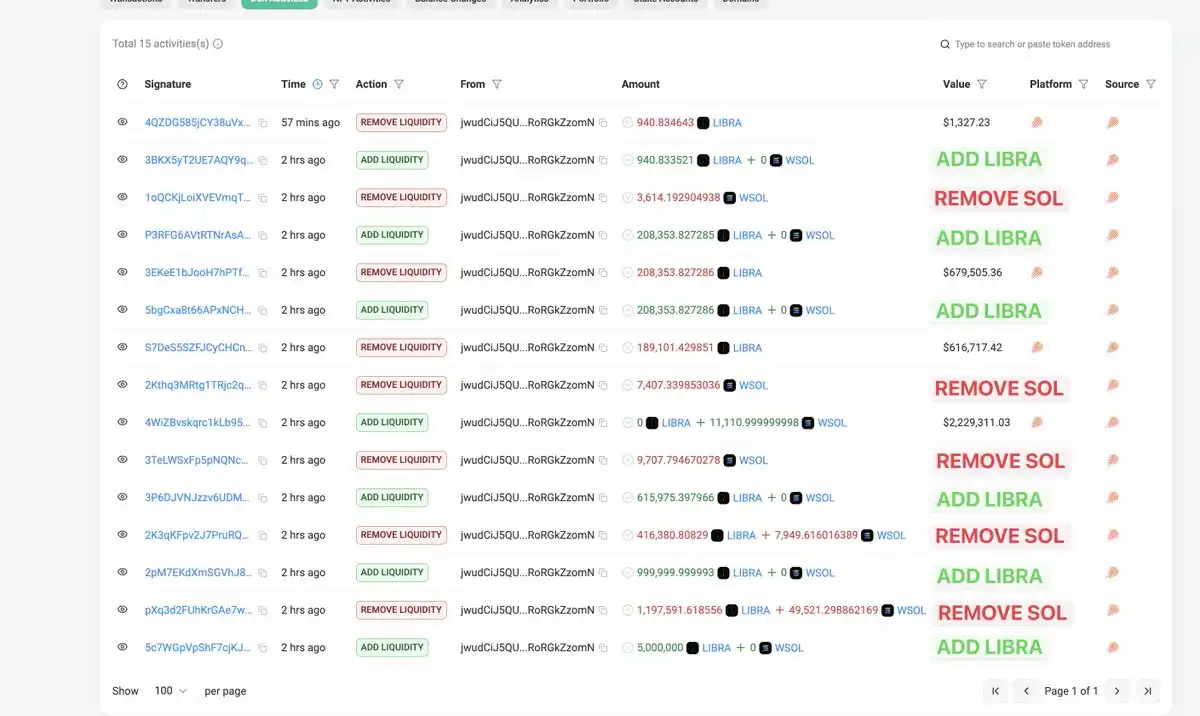

A prime example of this distribution method was the LIBRA token, which recently gained attention after being endorsed by Argentina's president. The LIBRA team set up one-sided liquidity pools for LIBRA-USDC and LIBRA-SOL on the Meteora platform—meaning they only deposited LIBRA tokens into the pools, without adding any counterpart assets like USDC or SOL.

Image source:Bublemaps

The mechanism works as follows: if only SOL is added to a pool, then as SOL’s price rises, it’s equivalent to continuously selling SOL for USDC. Conversely, if only USDC is added, it means continuously buying SOL as its price drops. Applying this logic to LIBRA, since only LIBRA tokens were placed in the pool and no USDC or SOL was provided, any purchase of LIBRA directly pushes up its price due to the absence of sell-side orders, creating an early illusion of "only rising, never falling."

Since the project team controlled the vast majority of circulating LIBRA tokens early on, they didn’t need to provide real stablecoins or ETH as counterparty liquidity, unlike on platforms such as Uniswap. Instead, the team simply posted buy orders for LIBRA at different price levels. With almost no sell orders available in the market, these buy orders kept getting filled, further driving up the price and manufacturing artificial prosperity.

Once this "artificial boom" attracted a large number of investors, pushed prices to high levels, and sufficient capital flowed in, the project team moved to the next step—removing the liquidity. They swiftly transferred the stablecoins or other assets invested by buyers into pre-designated consolidation addresses. Due to the unique nature of one-sided liquidity pools, there were no exchangeable assets left in the pool, making it practically impossible for investors to sell their LIBRA tokens. Any new purchases would only further inflate the unsupported price, allowing the team to complete their distribution.

Besides price manipulation, the LIBRA team also exploited the customizable fee feature of CLMM pools. This allowed them to earn additional fees totaling between ten and twenty million dollars during the process—a tactic similar to the high fees seen with TRUMP at the time.

Additionally, Mindao, founder of DeFi protocol dForce, analyzed that although Uniswap V3 also offers one-sided liquidity functionality, its main purpose is to improve capital efficiency and meet the needs of professional market makers. The key difference with LIBRA lies in its use of complex pool configurations and high customization, indicating that the design of its one-sided liquidity pool was not intended to provide genuine liquidity, but rather to facilitate subsequent price manipulation and liquidity withdrawal.

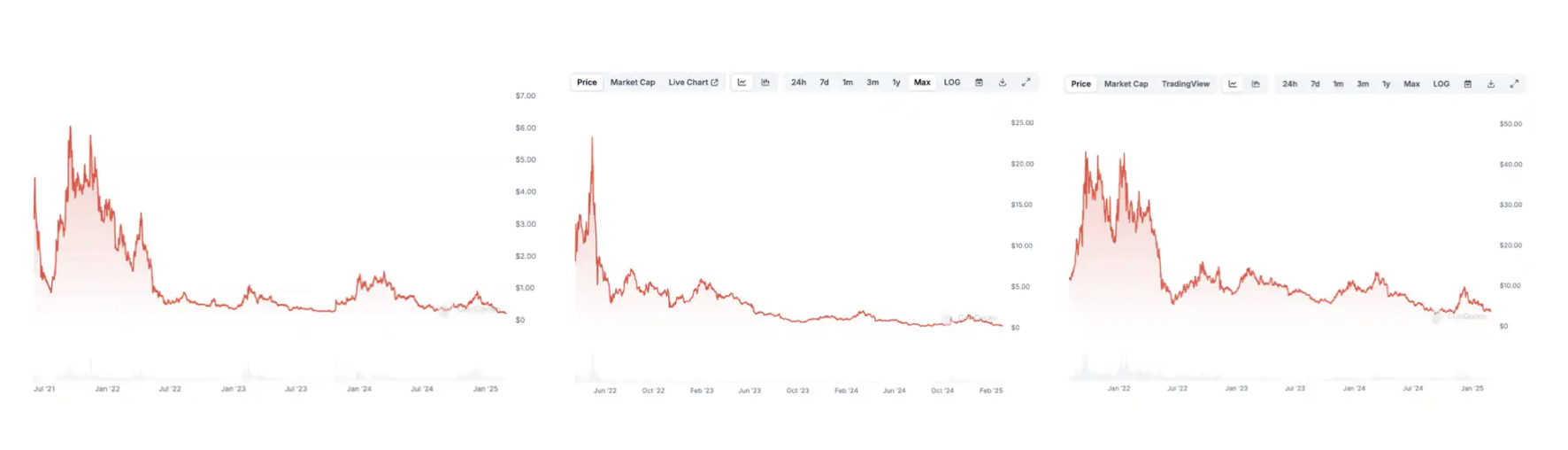

Buybacks Announced But Price Fails to Break Out of Consolidation

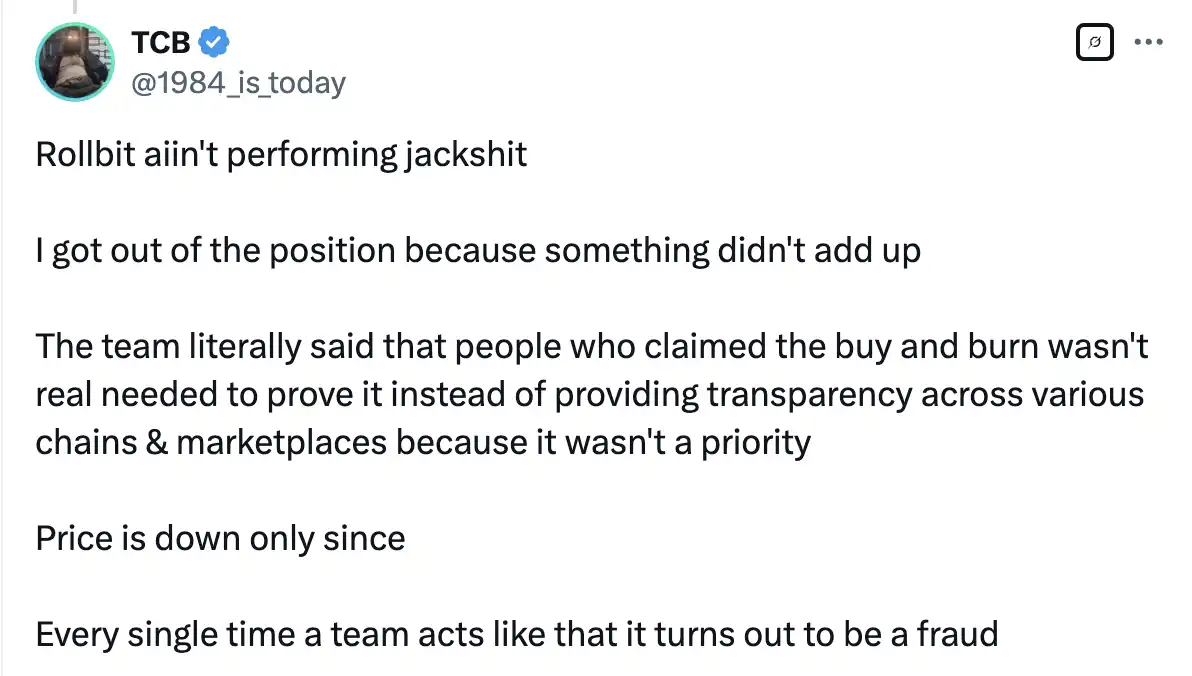

In August 2023, shortly after its TGE, GambleFi platform Rollbit announced changes to its tokenomics: 10% of Casino revenue, 20% of Sportsbook revenue, and 30% of 1000x perpetual contract revenue would be used for daily RLB buybacks and burns. Following this announcement, the token price initially rose. However, within two months, the price began a continuous decline. Community members gradually discovered a hidden "distribution" operation—the Rollbit team was laundering tokens via the Rollbit Hot Wallet before dumping them into the market through algorithmic distribution addresses.

Buybacks are usually seen as a way for project teams to stabilize the market and boost token prices. Normally, buyback funds should come from project earnings or capital appreciation. But if the funds originate from the team’s "hot wallet"—an internal wallet holding large amounts of tokens or funds—then the money isn’t truly flowing in from external sources, but is instead pre-held capital.

If the project uses its own hot wallet to fund buybacks, the money remains under its control. After purchasing tokens from the market, those tokens may not actually be burned or removed—they might simply return to the team’s possession. The repurchased tokens could flow back via the hot wallet into algorithmic distribution addresses controlled by the team and re-enter the market.

Token price keeps falling, with community members questioning Rollbit team's lack of transparency across chains and markets

The model of "selling 30%, buying back 10%" is inherently incapable of genuinely increasing the token price—it's yet another carefully orchestrated distribution scam by the project team.

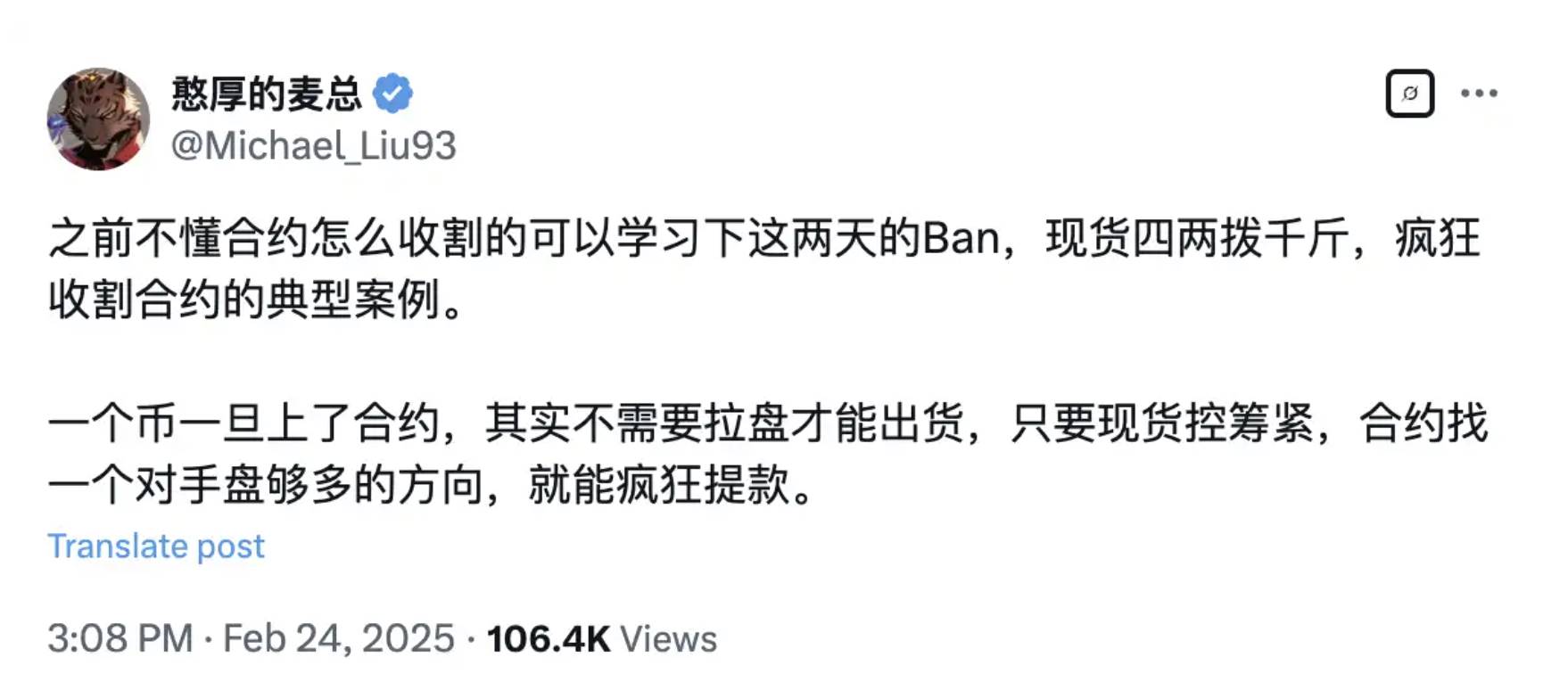

Spot Position Control Combined with Aggressive Futures Short Liquidation

"If you don’t like it, just short it" briefly became the most effective trading strategy this cycle. Although new tokens now often experience full-fee volatility in both directions, since the backlash against "VC coins," most secondary-market assets first undergo several days of decline, followed by a rapid rally, then enter a prolonged downtrend. Unbeknownst to many, this too is a form of distribution—exploiting low liquidity in the futures market and retail traders’ tendency to chase momentum.

The entire process can be broken down into several phases: First, during the initial listing phase, market makers typically refrain from supporting the price, allowing early airdrop recipients to dump. This stage primarily aims to flush out short-term speculators, clearing space for later operations.

Next, market makers begin preparing for the pump and distribution. Prior to this, they try to gain maximum control over spot holdings, reducing circulating supply so that sell-side pressure cannot significantly impact the price. This also limits the ability of short sellers to borrow tokens. With tight control over spot tokens, market makers can use relatively small amounts of capital to drive up prices, potentially triggering a short squeeze. When users follow suit by buying spot or opening long futures positions, they create ample demand, enabling the project/market maker/institutional players to offload their holdings in batches—an act of double harvesting.

Once short positions in the market diminish and the price reaches a certain level, market makers start harvesting liquidity from the futures market. They rapidly push the token price upward, attracting retail FOMO buying and creating an illusion of prosperity. This pump is usually substantial but generally doesn’t exceed the opening price. Subsequently, open interest in futures increases noticeably, while funding rates turn negative—signaling that market makers are establishing short positions.

Finally, operators gradually dump their holdings in the spot market. While profits here are limited, the more important part is that they secure ample exit liquidity through short positions in the futures market. A large number of retail traders, having gone long during the rally, become counterparties to the market makers’ shorts. As market makers increase their short exposure and simultaneously sell in the spot market, the token price begins to fall, causing massive long liquidations—achieving a dual harvest.

Retailers Can’t Play the Staking Game

Previously, launching staking for a token was considered a positive development in a project’s roadmap—intended to incentivize user participation in network maintenance, reduce circulating supply through lockups, and enhance token scarcity. However, many project teams have used this mechanism as cover to distribute and cash out.

Projects lure investors into locking up large amounts of tokens with high-interest staking rewards. On the surface, this appears to be an effort to stabilize the price by reducing circulation. In reality, however, most floating supply becomes trapped in staking contracts and cannot exit promptly. During this period, project teams operate with informational advantages over staking retail investors—allowing them to freely distribute tokens. Even if the team or major holders choose to stake, they earn high staking yields while continuously dumping on the market.

Moreover, another common script unfolds when the staking period ends: panic selling ensues as investors rush to exit, allowing the project team to quietly accumulate cheap tokens. Once market sentiment stabilizes and prices rebound, the team cashes out. At this point, retail investors flood back in, deceived by the appearance of recovery—only to find that the smart money has already exited, leaving behind nothing but retail bagholders at the top.

Reviewing the above distribution methods, their essence lies in precisely manipulating market expectations and investor psychology. To survive in this volatile market, retail investors must adopt the mindset of a manipulator. By "manipulator’s mindset," we do not mean orchestrating market manipulation, but rather cultivating independent thinking, resisting emotional swings, anticipating risks in advance, and developing corresponding defensive strategies.

The market amplifies emotions—only with calmness and rationality can one avoid becoming prey. Next time you hear terms like "buyback," "staking," or "one-sided pool," exercise extra caution. That extra vigilance might just help you avoid the carefully laid trap set by the project team. Feel free to share in the comments what other distribution tactics you’ve encountered.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News