Two years, nearly 30 million tokens created—crypto is a massive "token factory"

TechFlow Selected TechFlow Selected

Two years, nearly 30 million tokens created—crypto is a massive "token factory"

Exit or wait for a turnaround? Where should the first shot of transformation be aimed?

Author: flowie, ChainCatcher

Editor: TB, ChainCatcher

If you still have hopes for altcoins, seeing this data might shatter some illusions.

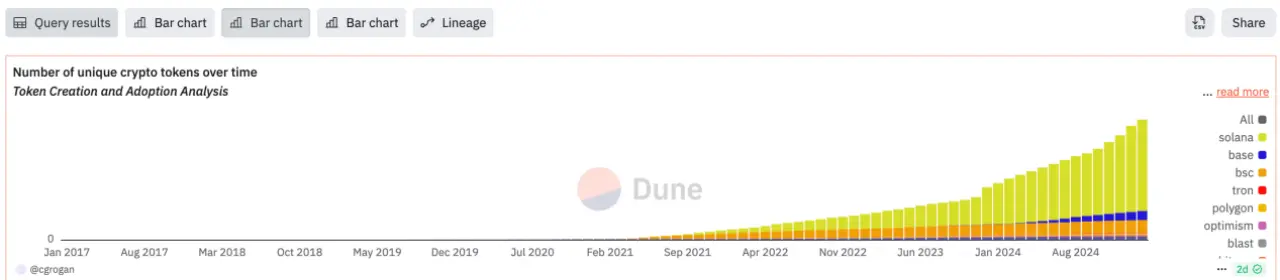

According to statistics from a Dune dashboard created by @cgrogan, the number of crypto tokens has risen from over 3.4 million in 2022 to more than 39 million in 2025. The crypto market generated over 10.09 million and 18.7 million new tokens in 2024 and 2023 respectively.

In stark contrast to this explosive growth of altcoins during the current bull market is the decline in the number of cryptocurrency developers. Electric Capital’s "Crypto Developer Report" shows that the total number of crypto developers dropped by 7% in 2024 and 24% in 2023.

The crypto market has become an unabashed massive “token issuance” factory, where apart from evolving token launch models and casino-like innovations, there is barely any sign of new paradigmatic breakthroughs.

Beneath the surface of fairness and overnight riches lies extremely low cost of malfeasance and a large number of defrauded ordinary users. Through prolonged PvP (player versus player) dynamics, all major participants, including users, have been conditioned to become clever short-termists.

Exit or Wait for a Turnaround?

Yesterday, the Crypto Fear & Greed Index dropped to 10, the lowest level since June 2022. @ZKSgu rebutted calls for externalities in crypto, stating, “People inside are about to lose hope.”

Meanwhile, exchanges and VCs—most criticized participants in this bull run—are now seeking exits or being forced out.

Veteran crypto derivatives exchange BitMEX is exploring a sale. According to sources who spoke to ChainCatcher, Deribit, the largest crypto options exchange, has already completed its sale, with the deal potentially valued as high as $5 billion.

It's not just exchanges—mergers and acquisitions are sweeping across the entire crypto sector. According to RootData, in just the first two months of 2025, over 20 M&A events have occurred in crypto, averaging more than 10 per month.

Many VCs face elimination. YettaS’s biggest takeaway from Consensus HK was widespread VC distress: some VCs couldn’t raise their next fund, others lost half their staff, some shifted to strategic investments instead of independent investing, and some even considered launching memes to raise capital.

Investor @26x14eth has started urging young people not to spend their most precious time chasing quick gains in crypto, but to seek internships in promising fields like AI and robotics. This isn’t the 2017–2021 cycle where everyone could profit—now, time is the most valuable asset.

Yet some are waiting for a turning point. Crypto KOL @cmdefi remains less pessimistic. He feels today’s market resembles 2018–2019, when after the ICO bubble burst, everyone thought the space was hopeless and full of scams.

“But then came DeFi Summer in 2020—speculative capital decreased, and the market began focusing on application innovation. Stay in the game. (Wait for the turnaround).”

Assembly-Line Token Issuance Frantically “Draining Blood”

This bull market is truly hellishly difficult.

There is almost no impressive crypto development to be seen. It took Trump-fueled celebrity coin “rugs,” Pi Coin listings, and recently the Safe hack to wake people up to how absurd and fragile the crypto system really is.

A diagram of the current state of the crypto ecosystem drawn by overseas KOL @sherlock resonated widely, revealing flimsy infrastructure and ubiquitous conspiracy groups.

This time around, making money is harder than ever.

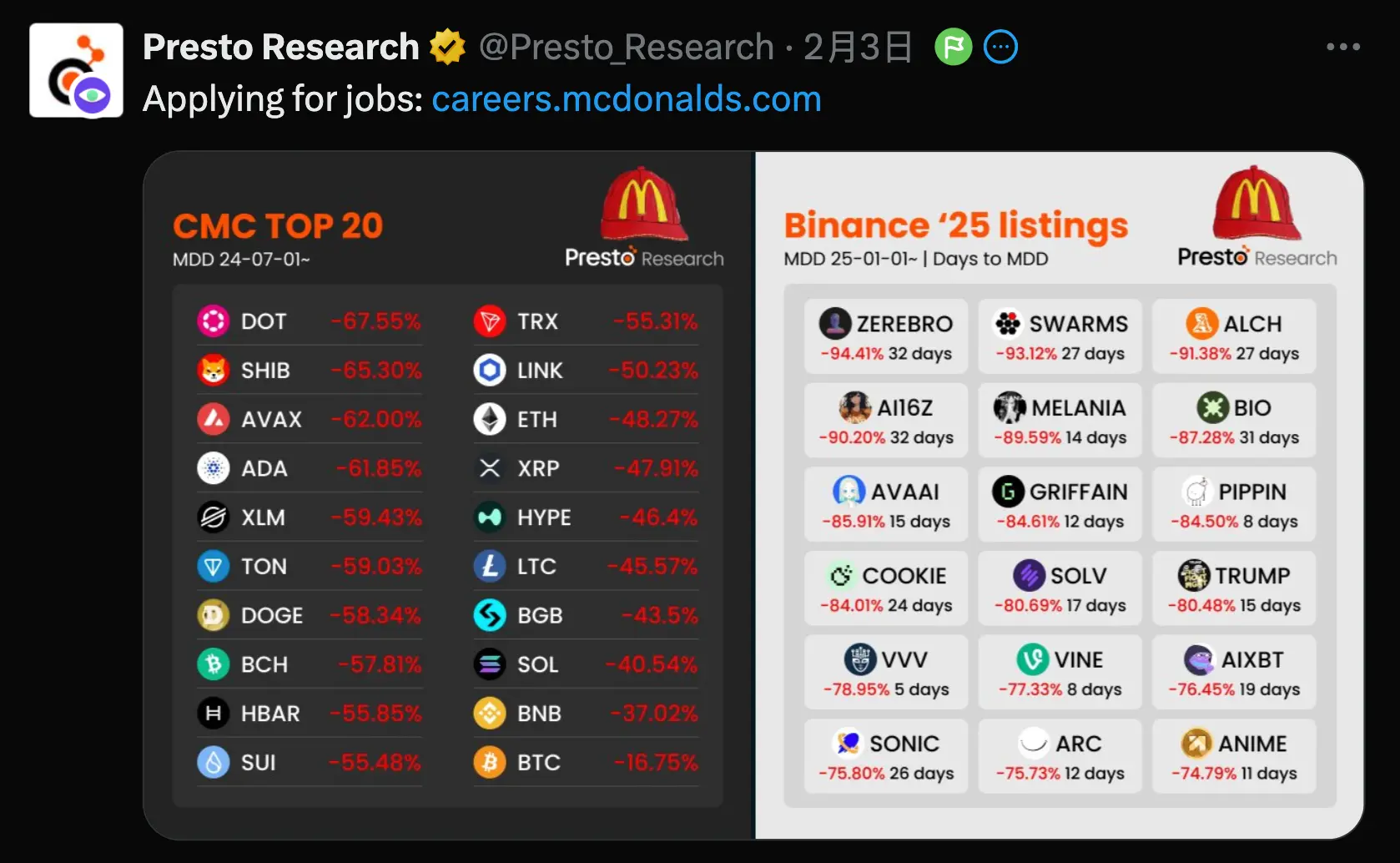

Players who lived through the last bull market may feel particularly pained. Binance, once a wealth-making mythmaker, has turned into a dumping ground for project teams and dog-coin whales. The so-called alpha peaks at listing. Presto Research tracked tokens listed on Binance in January 2025—all of them fell over 70%.

Even diamond-handed holders of top 20 market cap beta assets are no longer rewarded. Since July 2024, top 20 tokens have generally dropped over 60%. Airdrop farmers also lament that despite increasing sophistication and effort, they still end up getting rekt.

Seemingly fair on-chain PvP is nothing but chaos.

As of February 26, Pump.fun has launched over 8.1 million tokens, with only about 32 meme coins exceeding $100 million in market cap and just 154 surpassing $10 million. Now, after scandals involving celebrity coins like Libra, on-chain PvP appears to be ending.

With no real crypto development and most people unable to earn, where did all the money go?

Conflux co-founder Yuanjie may have revealed the truth: aside from a tiny number of lucky geniuses, the vast majority flows to various stakeholders within the “assembly-line token issuance” system.

Yuanjie shared on Twitter: “The ‘token factory’ includes not just VCs, serial entrepreneurs, market makers, OL Agencies, studios, whales, and exchanges—a complete assembly line greedily sucking blood from the industry and retail investors.”

In the crypto market, creating and selling tokens is the biggest business model.

In Yuanjie’s view, under the “token factory” model, a project team’s wealth creation centers on two key steps: token allocation and exchange listing. The assembly-line process goes like this:

-

Secure a founder with backing from inner circles (e.g., Vitalik, A16Z, Binance) or a highly influential meme leader to obtain low-cost tokens

-

Create compelling narratives backed by fabricated data (TVL, on-chain metrics, node count, etc.)

-

Bind incentives with KOL groups to promote via Twitter shilling

-

Target and influence key decision-makers for exchange listing (e.g., He Yi) to finalize the crucial step

-

After listing, use market makers to dump tokens, then repeat the process for the next project

A Web2 and Web3 investor told ChainCatcher that due to lack of R&D investment and minimal staffing needs, as long as projects can list and exit without collapsing, “the market elimination mechanism has completely failed—junk projects and tokens keep multiplying.”

But as ordinary users grow less susceptible to collusive “narratives” from project teams and VCs, a more brutal meme-based token issuance model has emerged—one that simply excludes VCs altogether.

Beneath the façade of barrier-free, fair token launches lies extremely low cost of wrongdoing. Primitive Crypto investment partner @YettaSing believes the meme model is essentially a darker on-chain world than the VC model. Lacking product and technological foundation, “absolute fairness” is often just a cover-up. Scandals like Libra’s celebrity coin ripped off the last veil of decency from meme coins.

Where Should the First Shot of Reform Be Fired?

With wealth effects vanishing everywhere, the industry has begun collective introspection and blame assignment.

Recent discourse has again targeted airdrop farming studios. Crypto KOL @mscryptojiayi argues that altcoins' poor performance traces back to the rise of “bribery systems,” and that the first shot of industry reform should hit these farming studios.

In her view, collusion between studios and project teams created a “false prosperity” that dilutes ordinary users’ expected returns, weakens long-term loyalty, degrades communities from value collectives into transactional markets, and plants landmines for secondary market dumps.

She criticizes that many studios shamelessly collude with fraudulent projects, jointly establishing pump-and-dump schemes and deceiving both exchanges and users.

But airdrop-focused KOL Ice Frog@Ice_Frog666666 pushed back. He argues “false prosperity” is a result—not the cause—of distorted industry development. Studios aren’t the biggest beneficiaries or rule-makers; if reforms don’t target the largest beneficiaries and rule-setters, they’re doomed to fail.

Beyond farming studios, VCs and CEXs—the two other major beneficiaries accused of colluding with projects—are frequent targets in this bull market.

During Hong Kong Consensus, amid rampant junk coins, one crypto VC even claimed, “90% of VCs should shut down.”

VC coins gained traction post-ICO because too many crypto scams existed—projects backed and vetted by VCs gradually earned retail trust.

But this retail leader has now lost credibility. Retail investors believe VCs gain tokens at lower costs and possess information advantages, colluding with projects to dump tokens and rug users.

In this bull run, VC coins typically feature high valuations with low circulating supply, leading to immediate dumps upon listing—fueling community discontent.

He Yi directly admitted in a recent AMA addressing listing controversies: “Some VCs are indeed core reasons behind inflated prices.”

Ordinary retail investors are always the ones hurt.

Exchanges, as the most powerful players in wealth creation, are naturally widely perceived as bearing significant responsibility.

Mainstream platforms like Binance and Coinbase have faced frequent backlash over listing controversies in the past year. Moonrock Capital CEO Simon once viewed exorbitant listing fees on CEXs as the primary reason projects cannot sustain operations and market liquidity drains away.

Although He Yi later denied the existence of such “sky-high listing fees,” CEX listing mechanisms and “inner circle” insider trading remain suspect as among the chief culprits enabling junk projects to list, harvest, and drain value.

Despite He Yi repeatedly emphasizing Binance’s transparent and complex listing procedures, the recent rapid listing and immediate crash of meme TST on BNB Chain led even CZ to question Binance’s listing practices.

Not only exchanges and VCs—but nearly every beneficiary along the “token factory” chain could be revolutionary targets. Crypto KOL @CyberPhilos identifies three major parasites in the crypto world: besides CEXs, there are KOL Agencies and market makers.

A common view is that key participants in this bull market are overly path-dependent, lacking sufficient native innovation. Once new external liquidity stops flowing in, everything collapses. But is this effect or cause? Why can every party in the chain become a “parasite”?

Overseas KOL Murtaza reflected: “Wealth arrived far earlier than utility—not just a minor error that self-corrects over time. It actually poses a fatal threat to the technology realizing its potential.”

Murtaza noted that the global crypto industry’s market cap exceeds $2 trillion. Typically, an industry of this scale forms only after developing something socially useful.

Bill, co-founder of Cypher Capital, and Nothing Research partner @0x_Todd expressed similar views while reflecting on the dilemmas facing VCs and exchanges.

Bill stated that Web3 venture capital follows entirely different logic from Web2 VC—it emphasizes “early fame as key,” and the fast wealth creation model drives founders to chase trends, focus on marketing, and rush to list on exchanges.

In Bill’s view, Web3 actually needs more “patient capital”—VCs adopting Web2-style approaches that support founders in building long-term value in primary markets, allowing teams to focus on product development rather than rushing to cash out.

CEX listing issues may similarly stem from projects cashing out too early. @0x_Todd argues that unlike traditional Web2 IPOs, crypto protocols enjoy the benefits of public listing—investor exits and employee incentives—without bearing any of the obligations.

The lack of crypto regulation is also a critical issue. @0x_Todd stated that tactics like bribery, fraud, volume manipulation, and deception thrive precisely because they carry no consequences.

Crypto fear and panic have reached an extreme. Despite widespread blame and reflection, the industry remains collectively trapped. Whether it can truly undergo “radical surgery” and reach a cleansing moment remains unknown.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News