Is the dollar's dominance weakening, with AI rising—will crypto emerge as the winner in global value transfer?

TechFlow Selected TechFlow Selected

Is the dollar's dominance weakening, with AI rising—will crypto emerge as the winner in global value transfer?

The "American exceptionalism" trade may be coming to an end.

Author: Flip Research

Translation: TechFlow

The Retreat of American Exceptionalism

Warren Buffett frequently refers to the concept of a "U.S. tailwind" in his annual letters—a reference to America's long-standing economic advantages on the global stage. His perspective has consistently proven correct, enabling him to achieve extraordinary returns across generations and establishing him as one of history’s greatest investors.

However, I believe this trend is rapidly shifting. As of the end of 2024, I hold only minimal exposure to U.S. equities and cryptocurrencies. In this article, I will elaborate on the logic behind this positioning and explain why I anticipate a decline in the U.S. Dollar Index (DXY) and prolonged underperformance of U.S. stocks—and by extension, cryptocurrencies—in the years ahead.

The Rise of AI: Global Competition and Value Redistribution

In recent years, the emergence of AI has undoubtedly been one of the most significant trends. AI is rapidly transforming how we live, and the pace of this transformation continues to accelerate. This shift is driven by several converging factors:

-

Computing power grows exponentially according to Moore’s Law, with GPUs providing powerful parallel processing capabilities—NVIDIA remains dominant in this space.

-

Breakthroughs in science and technology, such as the development of the Transformer architecture, have laid the foundation for improved AI model performance.

-

Massive investments from both governments and private enterprises. For example, the world’s seven leading tech companies (commonly known as the “Mag 7”) are expected to spend over $300 billion on AI alone in 2025.

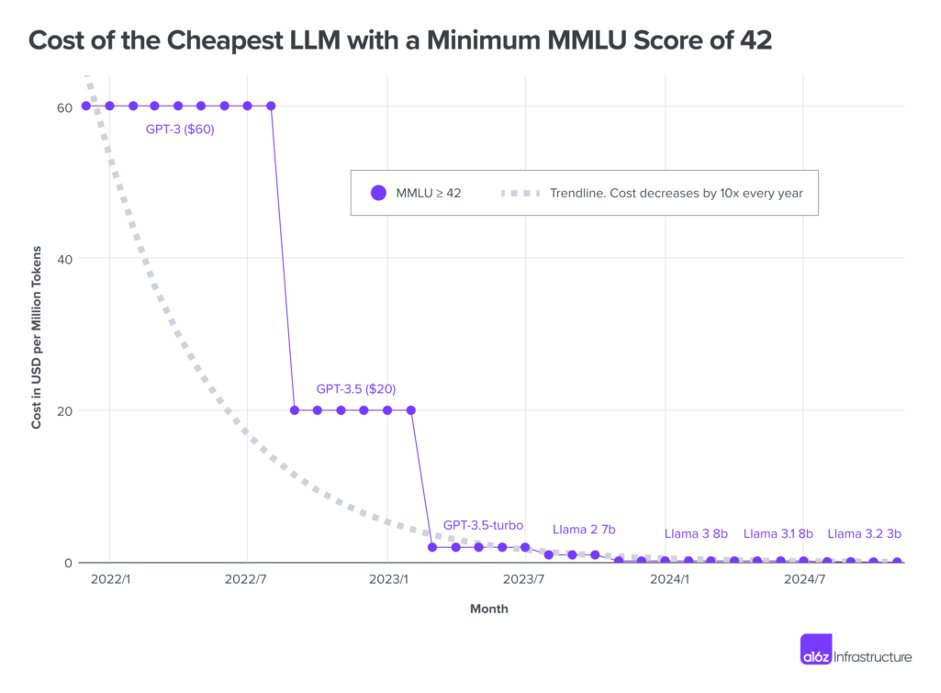

Together, these forces have drastically reduced the cost of inference—the expense associated with using AI models. According to estimates from A16z, this cost has dropped by a factor of 1,000 over the past three years.

The release of DeepSeek r1 has further accelerated this trend. Many refer to it as AI’s “Sputnik moment,” akin to the technological race sparked by the Soviet Union launching the first satellite in 1957. This time, however, the competition centers on building the most powerful large language models (LLMs) globally. Inference costs are now falling rapidly, approaching zero.

So who captures this value? In the short term, value flows down the stack to the application layer—businesses and services built on top of LLMs. However, in the long run, as LLM performance continues to improve, competition among applications intensifies, development becomes easier, and plug-and-play solutions proliferate. Ultimately, this value will flow directly to individual users.

I believe the next two to three years will be a critical period of transformation in AI—one whose impact will far exceed most expectations. This is precisely why I am convinced that AI-driven robotics will gradually emerge as more competitive, given that hardware interfaces present higher barriers to entry than software applications.

From an investment standpoint, there is a clear misalignment. Regardless of where you are in the world, portfolios tend to be heavily concentrated in the S&P 500. The rise of index funds has amplified this trend—many households now allocate spare savings directly into S&P 500 ETFs like VOO, while investment forums commonly advise, “Just put all your money into the S&P 500 and don’t look back.” The traditional 60/40 stock/bond portfolio is nearly obsolete. As a result, the S&P 500 now accounts for over half of global equity market capitalization, totaling around $55 trillion. This concentration risks overlooking new opportunities created by the rise of AI.

Technological Change and Global Value Redistribution

Despite the high concentration of financial capital in U.S. markets, the most transformative technologies of our era are redistributing value across the global population. This may be one of the most powerful equalizers we’ve ever seen—value is gradually being reallocated in line with demographic distribution. What does this mean for the United States? While the U.S. controls over half of the world’s financial capital, its population represents just 4.2% of the global total.

Certainly, some of the above points are simplified for clarity. For instance, the Mag 7 companies are already aware of these emerging risks. Firms like Meta have taken action—by open-sourcing models such as Llama to reduce inference costs, while also investing in robotics and application-layer innovations. Nevertheless, these efforts do not undermine the core argument.

The Trump Effect: Undermining America’s Global Standing

Undoubtedly, Donald Trump is reshaping the global political landscape. The “Make America Great Again” (MAGA) movement marks a sharp departure from traditional political discourse. Yet, while Trump claims his policies will restore American greatness, I argue that his actions are significantly weakening U.S. influence on the world stage and could ultimately lead to a gradual decline in America’s prospects.

To understand this, we must first examine why the U.S. dollar became the world’s reserve currency. On the surface, this can be attributed to the strength of the U.S. economy: the U.S. accounts for approximately 26% of global GDP and possesses a robust, open, and highly liquid capital market.

Yet this alone does not fully explain the dollar’s dominance. If economics were the sole factor, we would expect other currencies’ usage to align more closely with their respective economies’ sizes. In reality, the dollar is involved in nearly 90% of global transactions. What truly underpins the dollar is U.S. political and military power. Whenever a nation grows too strong, the U.S. imposes sanctions and demands allies follow suit. For example, the recent ban on exporting high-performance GPUs to China is a clear illustration. This pattern is not new—the British pound once served as the global reserve currency, backed by the British Empire’s military might, until imperial decline eroded that status.

Trump, however, is rapidly altering America’s traditional political and military posture. His “America First” philosophy prioritizes domestic affairs while de-emphasizing longstanding alliances and global military commitments:

-

Blanket tariff threats: Trump has issued broad tariff threats against all trading partners, including long-time allies. This has fueled anti-American sentiment (e.g., boycotts of U.S. products in Canada) and pushed trade partners to strengthen economic ties elsewhere.

-

Isolationist defense policy: Trump promotes military isolationism, weakens NATO, and demands allies raise defense spending to 5% of GDP. This has already prompted many European nations to compromise—increasing their own defense budgets and reducing reliance on the U.S., thereby undermining Trump’s primary leverage in Europe.

-

European push for independence: This trend is unfolding in real time. Germany’s election winner Friedrich Merz recently stated he would move quickly to unify Europe and “achieve independence from the U.S.” This highlights the diminishing dependence on America under Trump’s policies.

-

Cuts to foreign aid: The Trump administration has drastically reduced U.S. foreign aid, a long-standing tool of global influence. Meanwhile, China has pursued the opposite strategy—especially in Africa, expanding via initiatives like the Belt and Road Initiative to secure vital resources and key supply chains.

-

Alignment with Russia: The Trump administration appears focused on “ending the Ukraine war at any cost,” leading to closer U.S.-Russia relations—even though Russia ranks only 11th globally in GDP. This strategic choice alienates traditional allies and risks weakening America’s global standing.

The Fed’s Dilemma

Current U.S. political and fiscal policies have placed the Federal Reserve in a difficult position. Many of Trump’s isolationist policies lack economic rationale. Economists have long demonstrated that autarkic policies are vastly inferior to global cooperation. The principle of comparative advantage clearly illustrates the benefits of international specialization.

While the U.S. market remains strong overall, signs of weakness are emerging. The labor market is gradually cooling, and corporate investment is declining—largely because businesses are hesitant to make long-term commitments amid policy uncertainty. The 2025 GDP growth forecast stands at 2.2%, a modest level.

At the same time, inflationary pressures persist. January’s Consumer Price Index (CPI) rose 3% year-on-year and has been trending upward over the past six months. This combination of slowing growth and rising inflation places the Fed in a tough spot, forcing it to balance competing priorities. So far, markets widely expect the Fed to cut rates only once or twice this year.

Tracking capital flows remains essential to understanding markets. Last year’s rally was largely driven by expectations of deregulation and increased liquidity. This year, sentiment has shifted sharply, increasingly influenced by tightening policies. That said, the Fed’s Quantitative Tightening (QT) program is set to ease in the first half of the year, injecting additional liquidity into markets.

Conclusion

The “American exceptionalism” trade may be nearing its end, driven by a complex web of factors. But as the saying goes: “The market can stay irrational longer than you can stay solvent.”

Why now? In my view, the Trump administration is the catalyst accelerating this shift. He is reshaping the global political order in ways unseen for decades, forcing traditional allies to reevaluate their positions and inflicting serious damage on America’s international standing.

The current situation is already fragile—only a small spark may be needed to trigger major change. For instance, EU leaders might simply say “no” to Trump’s stance on Ukraine, galvanizing European unity; or allies, facing policy uncertainty, may begin forming new trade blocs. Indeed, we are already seeing early signs of this in Germany’s new leadership.

Meanwhile, the U.S. economic outlook offers little reassurance. At the same time, the impact of the AI transformation is becoming evident. For example, Chinese equities have clearly outperformed U.S. stocks this year, possibly reflecting divergent technological trajectories between the two nations.

As for cryptocurrencies, I believe institutional investors treat them as high-risk assets within the risk spectrum and adjust capital flows accordingly based on the trends outlined above. In crypto circles, institutions often carry a “halo effect,” with many community members—especially in the crypto Twitter (CT) sphere—placing excessive faith in their decisions. Yet in reality, these institutions possess no insider knowledge (and may even know less than the CT community). Thus, when markets undergo sharp corrections, they may suffer losses just like retail investors. Whether MicroStrategy (MSTR) operates a Ponzi scheme is another topic worthy of deeper exploration.

Disclaimer: All views expressed above are my personal opinions and reflect my own portfolio positioning. Content is highly condensed to suit the reading habits of the crypto Twitter (CT) community (which tends to favor brevity). Always do your own research (DYOR) and draw your own conclusions.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News