How to Understand the Recent Downward Trend: The First Wave of "Trump Shock" Arrives

TechFlow Selected TechFlow Selected

How to Understand the Recent Downward Trend: The First Wave of "Trump Shock" Arrives

In the coming period, monitoring the policy implementation by the Trump team will clearly take precedence over other factors and requires continuous attention.

Author: @Web3_Mario

Summary: Last week, the cryptocurrency market experienced a significant pullback. The broader market generally attributed this to Federal Reserve Chair Powell's so-called "hawkish rate cut," which triggered concerns in risk markets about inflation and economic recession. However, according to the author’s analysis, this is likely only a secondary factor behind capital market panic. The real catalyst was Trump’s aggressive pressure—jointly with Musk—on Congress regarding the short-term spending bill last Wednesday, including threats to eliminate the debt ceiling rule, which introduced substantial uncertainty and ignited investor risk-off sentiment.

Powell May Be Taking the Blame—Macro Data Isn't Strong Enough to Trigger Monetary Policy Risk Panic

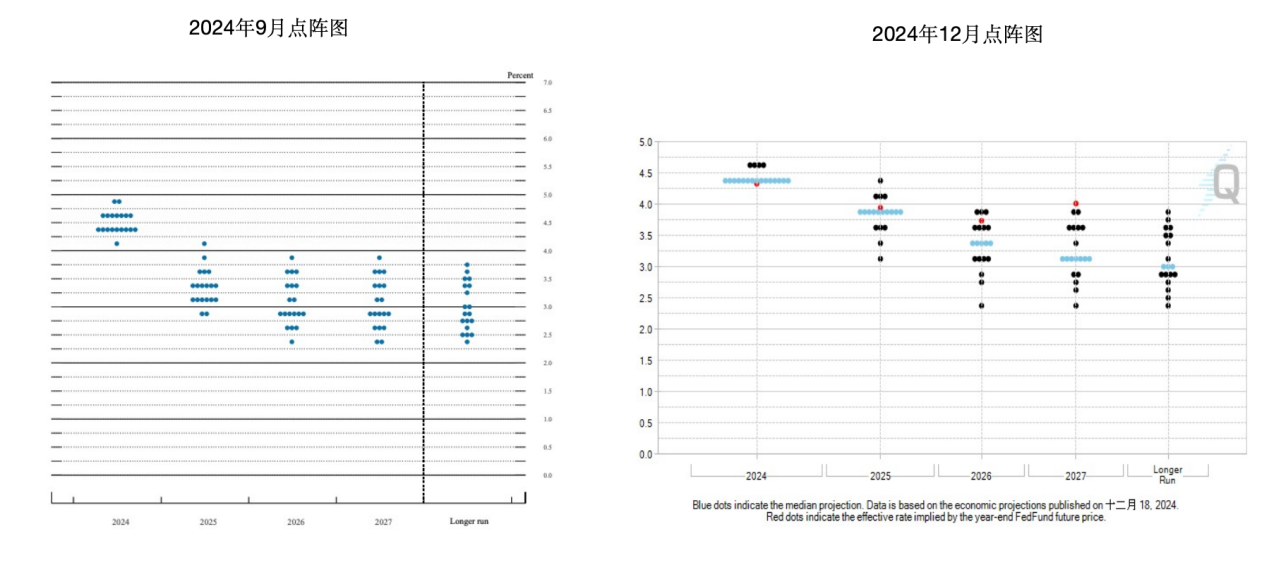

In the early hours of last Thursday, the FOMC interest rate decision met market expectations, concluding with a 25-basis-point cut. Market participants widely attributed the decline in risk assets to two factors. First, the dot plot revealed a lack of consensus among voting members, with Cleveland Fed President Mester favoring a hold on rates. Second, the median projected target rate for 2025 was raised to 3.75%–4.00%, up from the previous September projection of 3.25%–3.5%, reducing the expected number of rate cuts from four to two. For context, the “dot plot” is a chart tool used by the Federal Reserve to illustrate policymakers’ expectations for future interest rate paths. It forms part of the Summary of Economic Projections (SEP) released after each FOMC meeting, typically published four times a year, and serves as a key gauge of internal policy consensus at the Fed.

Additionally, during the subsequent press conference, some of Powell’s remarks were interpreted by markets as hawkish guidance, primarily in two areas: he expressed apparent concern over inflation outlooks for the coming year, and offered no positive response on the idea of establishing a Bitcoin reserve. However, upon closer reading, it appears that Powell’s concerns about inflation risks stem less from shifts in macroeconomic indicators and more from uncertainties surrounding Trump’s policy agenda. At the same time, his overall outlook on the economy still conveyed sufficient confidence.

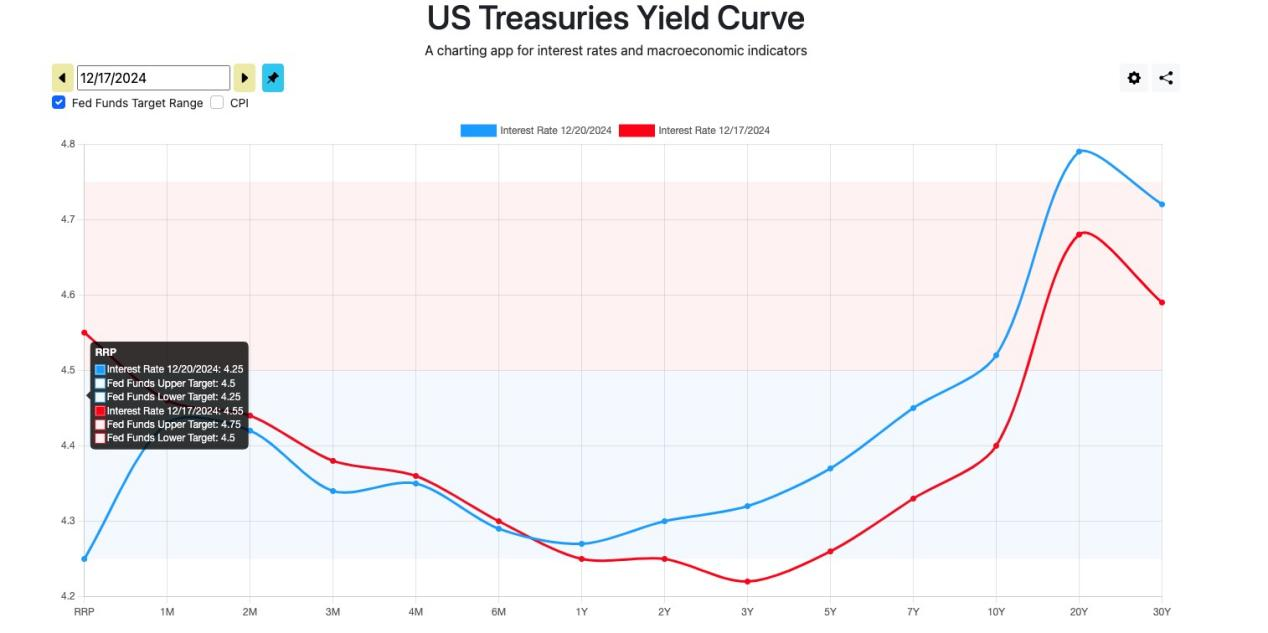

Now let’s examine why this interpretation holds. Consider changes in the U.S. Treasury yield curve before and after the release of the Fed’s decision and related statements. While long-dated yields did rise, the 1-year yield remained largely unchanged—indicating genuine concern about longer-term economic prospects but not suggesting any immediate near-term risks.

Looking at the price of the federal funds futures contract expiring in December 2025, market expectations for two rate cuts had already been priced in since November. Therefore, attributing the recent market correction primarily to anticipated risks around future Fed rate decisions seems analytically weak. As a side note, implied interest rates are calculated as 100 minus the current futures price.

Next, consider several key macroeconomic data points: PCE index, non-farm payrolls and unemployment rate, and GDP growth components. Over recent months, the U.S. PCE index has not shown notable increases—both headline and core PCE YoY remain below 2.5%. The University of Michigan inflation expectations have also stayed stable. Unemployment has not risen significantly, and November’s non-farm payroll data even showed improvement compared to prior months, reflecting strength in the labor market. With Trump’s upcoming tax cuts and relatively steady GDP growth across components—without sharp declines in any particular area—macro data do not support predictions of either renewed inflation or an impending recession within the next year. This further suggests that Powell’s concerns are rooted more in policy uncertainty stemming from Trump’s agenda than in hard economic indicators.

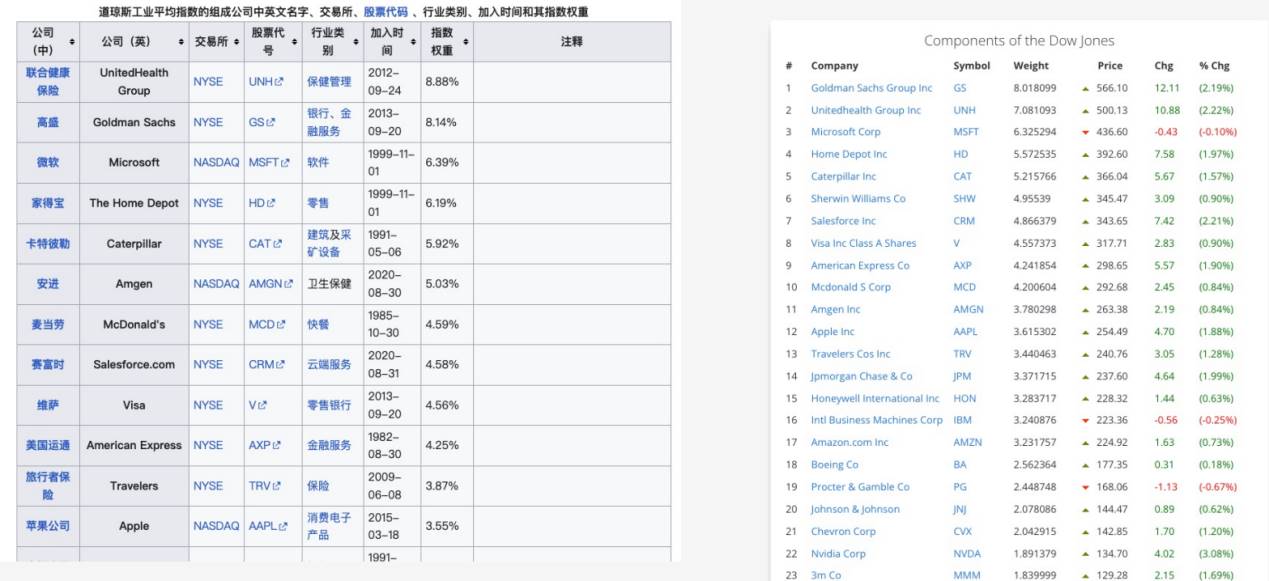

A brief clarification: the Dow Jones Industrial Average has recorded consecutive record drops, leading some to interpret this as bearish sentiment toward America’s industrial future. But digging deeper reveals this is not due to systemic risk, but rather driven mainly by a steep downward revision in UnitedHealth Group (UNH). The Dow Jones Industrial Average (DJIA) is a price-weighted index, meaning each component stock’s impact on the index depends on its absolute share price rather than market capitalization. Consequently, higher-priced stocks carry greater weight. As of November 2, 2024, UNH held the largest weighting in the DJIA at 8.88%. In the latest equity weightings, its share dropped to 7.08%, with its stock falling from $613 on December 4 to around $500—a nearly 18% drop—while other high-weight stocks did not experience similar declines. Thus, the Dow’s fall stems largely from single-stock risk in UNH rather than broad systemic issues.

What happened to UNH? The trigger was the assassination of CEO Brian Thompson outside the Hilton Hotel in Manhattan on December 5. He was fatally shot by Luigi Mangione, who came from a privileged background. During interrogation, Mangione stated his actions were motivated by outrage over UNH’s role in exploiting American citizens through healthcare costs. His stance drew widespread public sympathy, reigniting long-standing tensions over the U.S.’s exorbitant medical expenses—an issue aligned with Trump’s proposed healthcare reforms. This confluence amplified the negative sentiment, causing the stock to plummet (details omitted here).

Regarding the Bitcoin reserve discussion, the author believes Powell’s personal stance is ultimately inconsequential. As Powell himself noted, the authority to advance such a proposal lies with Congress, not the Fed. By analogy, consider how U.S. oil and gold reserves are established and managed—the Department of Energy oversees oil reserves, while the Treasury manages gold reserves. Although agencies like the SEC, CFTC, and the Fed play supporting roles in regulation and policy influence, their functions remain auxiliary in nature.

So why did markets react so strongly? The author argues the primary reason lies in Trump’s coordinated pressure with Musk last Wednesday against the congressional short-term spending bill—and particularly the threat to permanently abolish the debt ceiling rule—which injected profound uncertainty and triggered widespread risk-aversion behavior.

Trump Wields Unprecedented Power to Abolish Debt Ceiling, Casting Shadow Over Dollar Credit System—Markets Shift Into Risk-Off Mode

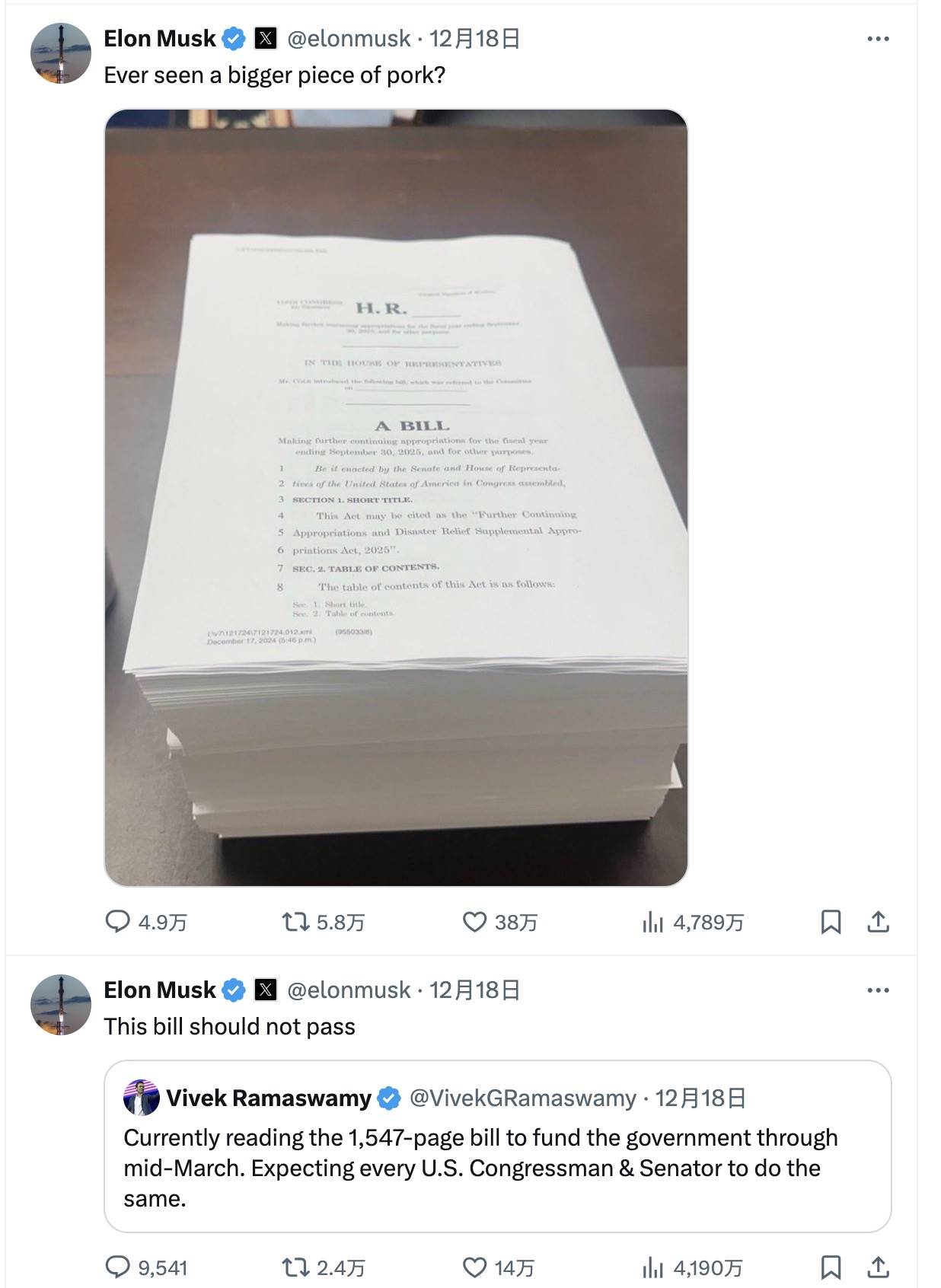

How many readers noticed the political battle in Congress last week over short-term government funding? On Tuesday, December 17, House Speaker Mike Johnson reached a bipartisan agreement with Democrats to extend government financing until March next year, avoiding a shutdown. To secure passage, Johnson made concessions and bundled several bipartisan-supported bills into the package. Yet on December 18, Musk launched a fierce campaign on X, denouncing the bill as deeply harmful to taxpayers, prompting swift rejection of the proposal.

This move received full backing from Trump, who posted on Truth Social demanding Congress repeal the “absurd” debt ceiling rule before his official inauguration on January 20, arguing that the debt crisis was created by Biden and the Democratic administration and should therefore be resolved under his leadership. Subsequently, Republicans revised the spending bill—removing certain compromise expenditures and adding provisions to abolish or suspend the debt ceiling. However, on Thursday, December 19, the bill failed in the House vote with 174 in favor and 235 opposed. This outcome revived fears of a government shutdown. Ultimately, on December 20—just hours before the deadline—the House narrowly passed a new temporary funding bill, though the provision to modify the debt ceiling was removed.

Although the new spending bill passed and prevented partial government shutdowns, the author contends that Trump’s explicit stance on eliminating the debt ceiling clearly unsettled financial markets. Trump now wields unprecedented power among modern U.S. presidents, especially given Republican dominance in the House. New members of Congress will be sworn in on January 3, significantly increasing the likelihood that efforts to abolish the debt ceiling could succeed. Let us now analyze the potential implications.

The U.S. debt ceiling refers to the statutory maximum amount of debt the federal government is authorized to borrow. First introduced in 1917, it is set by Congress to limit the expansion of national debt. While intended to enforce fiscal discipline, the debt ceiling is not an effective tool for controlling actual debt levels—it merely sets a legal borrowing cap. Beyond budgetary control, it has become a powerful political weapon, often wielded by opposition parties to extract concessions by threatening government shutdowns over spending disputes.

The U.S. has suspended the debt ceiling multiple times through legislative action. A suspension allows the government to continue borrowing beyond the statutory limit until a specified date or threshold. Notable examples include:

- 2011–2013: A severe debt ceiling crisis emerged in 2011, with intense negotiations between Congress and President Obama. A deal was eventually struck to temporarily raise the ceiling alongside budget-cutting measures. To prevent default, Congress passed legislation in October 2013 suspending the debt ceiling until February 2014, when debt levels neared the limit.

- 2017–2019: In 2017, Congress passed a bill suspending the debt ceiling until March 2019, tied to broader fiscal agreements, allowing uninterrupted government operations and averting default.

- 2019–2021: In August 2019, Congress enacted a two-year budget deal that increased spending caps and suspended the debt ceiling until July 31, 2021, enabling continued borrowing without constraint.

- 2021: In December 2021, Congress narrowly approved a temporary adjustment, raising the ceiling to $28.9 trillion and permitting borrowing until 2023, avoiding default at the eleventh hour.

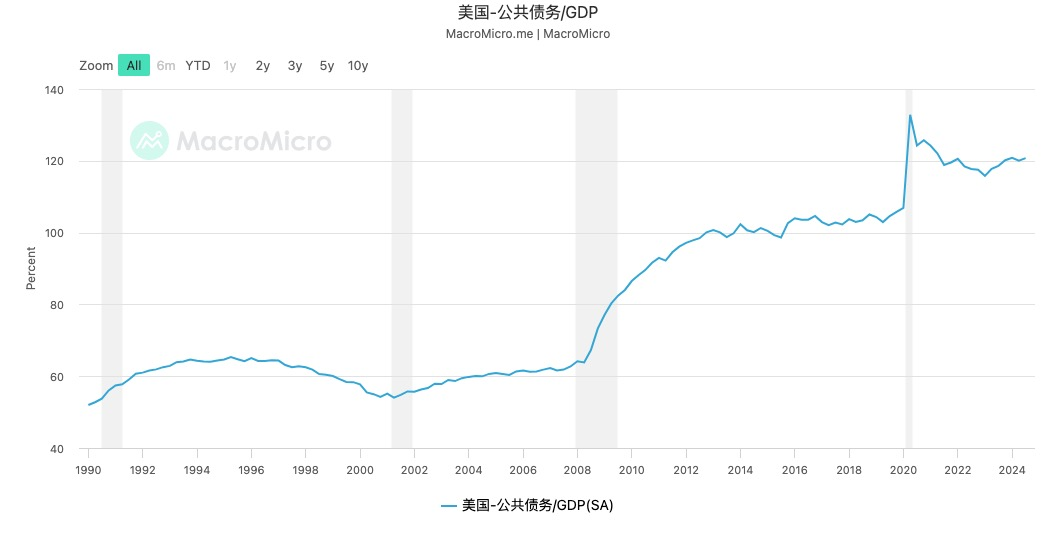

Historically, debt ceiling suspensions occurred during exceptional circumstances—such as the 2008 financial crisis or the 2021 pandemic. So why does talk of abolishing it now cause such alarm? The core issue lies in the current scale of U.S. debt. Public debt relative to GDP has reached an all-time high, exceeding 120%. Eliminating the debt ceiling would mean the U.S. operates without any formal fiscal constraints for the foreseeable future—an outcome whose impact on the credibility of the dollar-based credit system is incalculable.

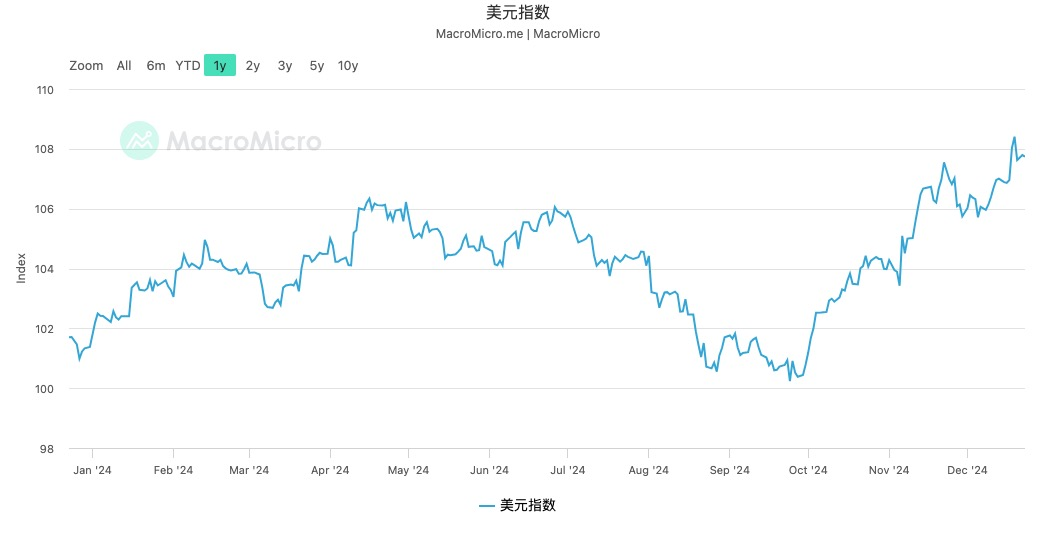

Why would Trump pursue this? The rationale is straightforward: to navigate short-term debt risks. Among Trump’s top policy priorities are tax cuts and reducing public debt. While tax reductions may boost economic activity, they inevitably reduce government revenue in the short run. Though tariff hikes could offset some fiscal shortfalls, manufacturing nations can counteract via currency depreciation. This explains why the dollar index remains strong despite ongoing rate cuts—countries are preemptively hedging against potential trade wars. Meanwhile, spending cuts risk hurting domestic corporate profits and dampening growth momentum. To weather this transitional period, Trump sees eliminating the debt ceiling as a convenient solution—allowing continued deficit financing to bridge the fiscal gap.

Finally, why does this affect cryptocurrencies? The key lies in the erosion of the Bitcoin reserve narrative. One major storyline in recent crypto discourse has been the idea that the U.S. might establish a Bitcoin reserve to address its debt crisis. If Trump simply abolishes the debt ceiling instead, this effectively undermines that entire narrative. As previously analyzed, the crypto market is currently searching for new sources of value support. Profit-taking and risk-off behavior in response to this shift are thus entirely understandable. Going forward, monitoring the policy direction of the Trump team should take precedence over other factors—and warrants close attention.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News