2024 Bitcoin Development Report: Global Regulation Clarified, DeFi and Scaling Drive Dual Growth

TechFlow Selected TechFlow Selected

2024 Bitcoin Development Report: Global Regulation Clarified, DeFi and Scaling Drive Dual Growth

Each region assigns different meanings to Bitcoin based on its own needs.

Authors: Vaish Puri & Joey Campbell

Translated by: TechFlow

When historians look back at 2024, they may see it as a pivotal year for Bitcoin’s move into the mainstream. It was the year Bitcoin hit new all-time highs, became a talking point in the U.S. presidential election, saw 11 Bitcoin ETFs approved, and experienced its halving event—all while the global economy struggled under inflationary pressures.

In 2024, Bitcoin revealed its multifaceted appeal. In countries grappling with economic turmoil—such as Argentina and Turkey—it served as a hedge against hyperinflation. To Wall Street elites, it transformed into an investment vehicle endorsed by financial giants like BlackRock. For cypherpunks and developers, it became a fresh canvas for innovation. And to governments worldwide, it shifted from being a threat to control into an opportunity to harness.

Bitcoin’s technology also continued evolving. The network, once defined by simplicity, began embracing new functionalities. Reactivated opcodes (like OP_CAT) and groundbreaking research such as BitVM introduced new possibilities for programmability and self-custody at Bitcoin’s base layer. Layer 2 networks advanced rapidly, offering scalability solutions, while liquid staking derivatives opened doors for yield generation on Bitcoin.

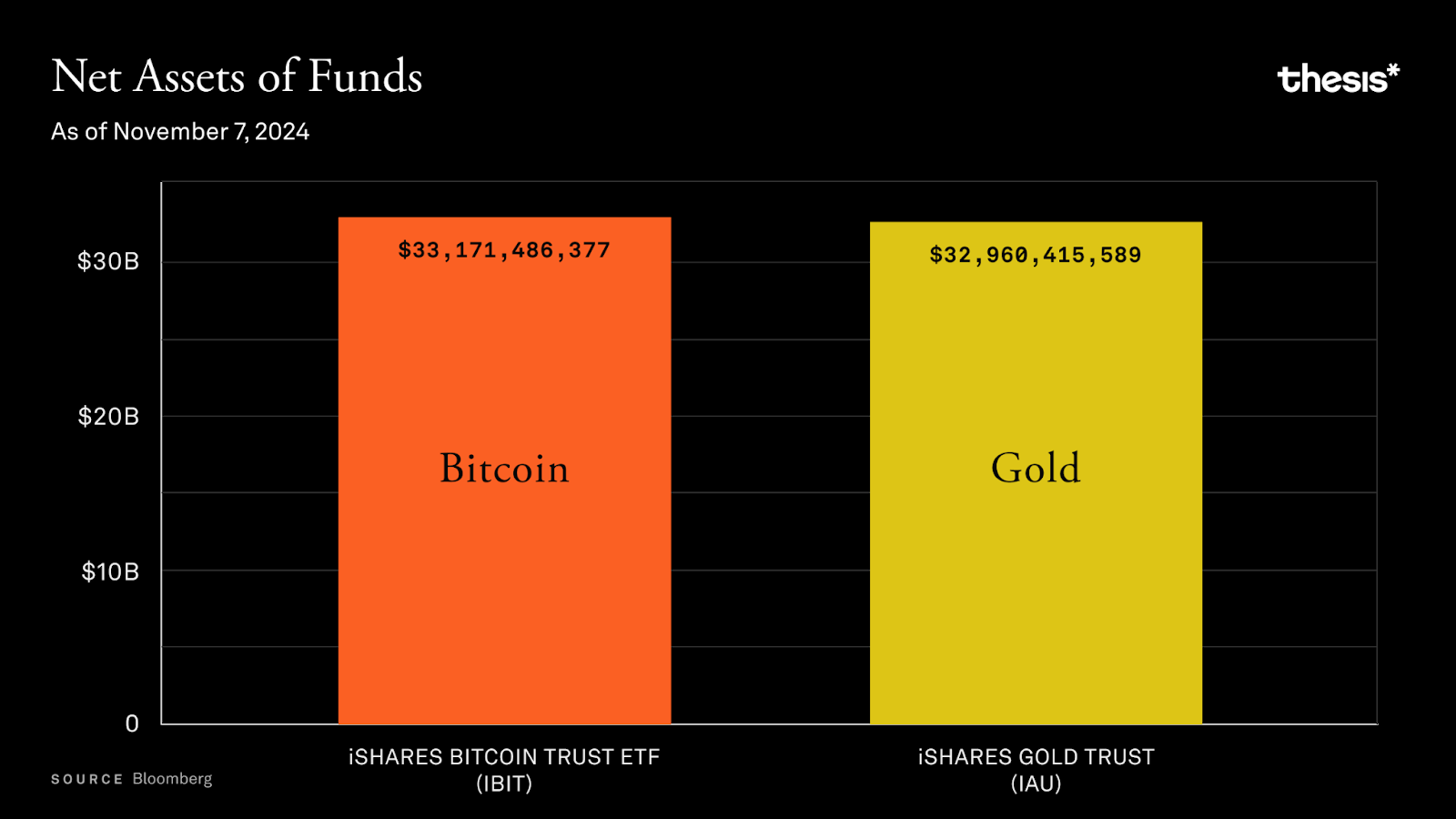

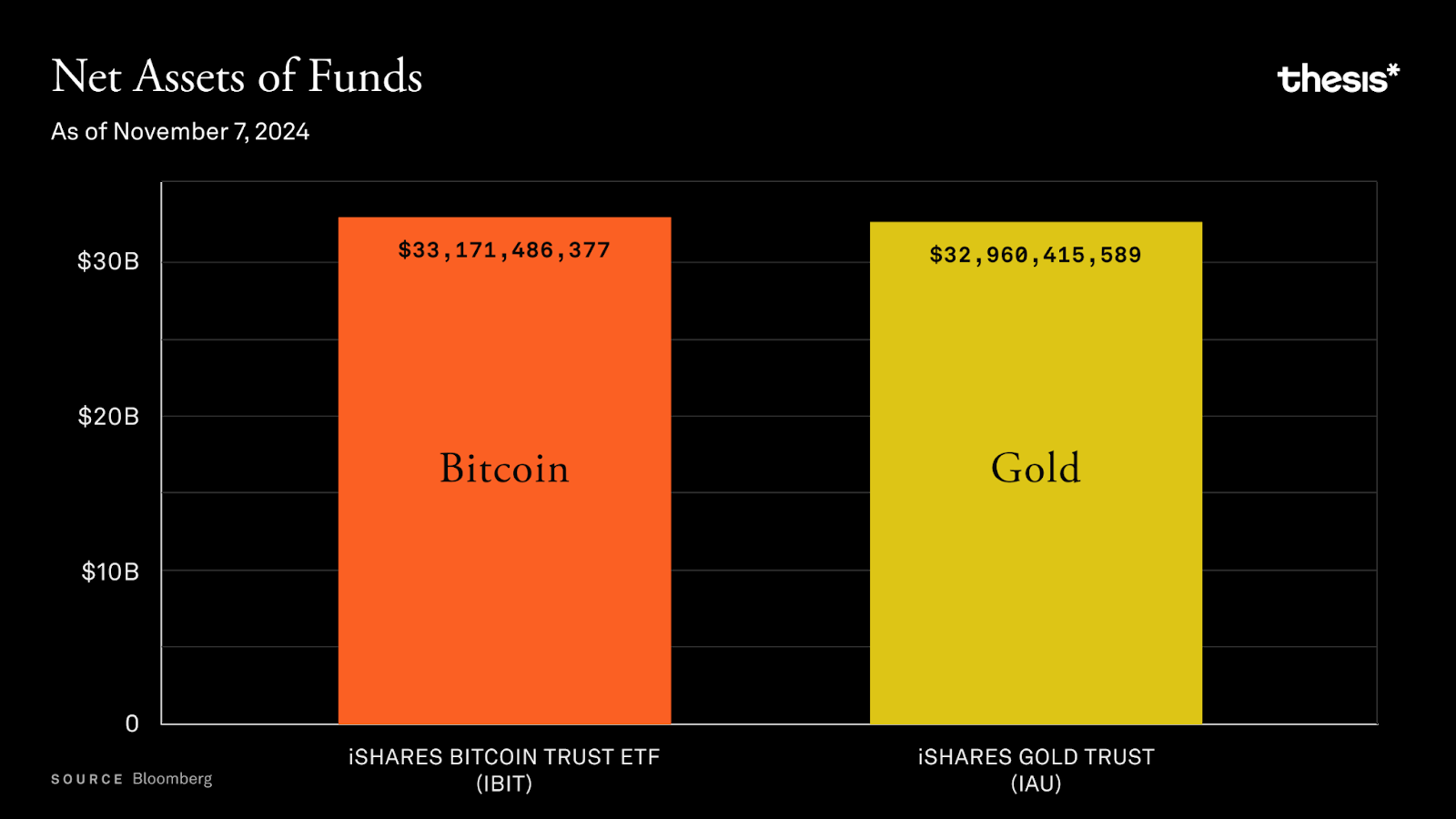

BlackRock’s iShares Bitcoin Trust (IBIT) set records, reaching $10 billion in assets under management (AUM) in just weeks—far outpacing the growth of its gold ETF. As institutional capital flooded in, Bitcoin began entering retirement portfolios. This shift thrilled Wall Street but alarmed Bitcoin purists. ETFs made Bitcoin more accessible than ever—now, 62% of Americans can buy Bitcoin as easily as Apple stock through brokerage accounts. Yet this convenience came at a cost. The core Bitcoin ethos—“not your keys, not your coins”—was increasingly drowned out by the noise of institutional trading.

Yet Bitcoin thrives in contradictions. In the U.S., Trump’s crypto-friendly policies helped legitimize Bitcoin as an institutional asset. In India, despite regulatory headwinds, 75 million users have adopted Bitcoin as a tool for financial empowerment. In Turkey, amid 50% inflation, Bitcoin became a savings vehicle for millions. In Argentina, citizens facing 140% inflation didn’t have time to debate custody models—they used Bitcoin to protect their wealth. Across Latin America and Africa, Bitcoin is not an investment instrument but a means of survival.

This adaptability defined Bitcoin’s journey in 2024. Each region赋予 Bitcoin a unique meaning based on local needs. Rather than diluting Bitcoin’s core purpose, this flexibility demonstrated its resilience. Bitcoin acts like a mirror, reflecting diverse user demands while preserving its fundamental properties.

As 2024 draws to a close, Bitcoin stands at a crossroads. It has gained the legitimacy long sought by early supporters—but perhaps not in the way they envisioned. While ETFs brought transformative change, they also reintroduced risks that Bitcoin was designed to avoid. Meanwhile, scalability challenges are finally being addressed seriously, and the future of 2025 holds promise and possibility.

Are Bitcoin ETFs bridges to mass adoption or gateways to centralization? Can Bitcoin staking enhance network utility without fracturing ideological foundations? With Layer 2 solutions and tokenized Bitcoin emerging, will Bitcoin achieve real scalability—or are we merely repeating past debates? Does Trump’s victory and the end of Gensler’s era signal a new chapter for U.S. crypto policy? From the revival of OP_CAT to record ETF inflows, from MEV on Bitcoin to recursive covenant exploration—the story of Bitcoin in 2024 continues to unfold.

Institutional Adoption: ETFs and MicroStrategy

-

Bitcoin ETFs: Institutional Demand

-

Bitcoin ETFs—such as BlackRock’s IBIT—reached $20 billion in AUM within 137 days, setting a new record. By comparison, the previous fastest-growing ETF (JEPI) took 985 days to reach the same milestone.

-

ETF custodians now hold over 1 million BTC—more than 5% of Bitcoin’s total circulating supply.

-

Hedge funds and financial advisors play key roles among ETF investors, signaling strong institutional interest in Bitcoin.

-

The Decline of Grayscale

-

Grayscale’s GBTC, burdened by a 1.5% management fee and inefficient redemption mechanisms, lost its leading position. Users migrated to lower-cost ETFs, causing GBTC’s AUM to plummet—losing 152,000 BTC in just one month.

-

MicroStrategy’s Strategy

-

Under Michael Saylor’s leadership, MicroStrategy has accumulated 402,100 BTC, valued at approximately $39.8 billion. The company raised capital via convertible bonds and equity offerings to continuously increase its Bitcoin holdings.

-

Though controversial, MicroStrategy remains one of the world’s largest corporate Bitcoin holders and is seen as an indirect investment vehicle. Its stock trades at a premium three times higher than pure Bitcoin exposure.

-

Broad Impacts

With institutional participation, Bitcoin’s price volatility has gradually declined. The launch of ETF options further solidified Bitcoin’s role as a long-term store of value, integrating it into diversified investment portfolios.

While ETFs offer retail investors and advisors convenient access, they face criticism for relying heavily on custodial models—undermining Bitcoin’s foundational principle of self-custody.

BRC-20, Ordinals, and Runes

Taproot and SegWit upgrades enabled innovations like Ordinals and Runes, making NFTs and fungible tokens possible on Bitcoin. These developments boosted network activity but sparked debate. Critics argue they burden the network, while supporters highlight their role in sustaining transaction fees and demonstrating Bitcoin’s permissionless innovation.

-

Trends and Network Impact

The popularity of Ordinals collections drove a surge in Bitcoin transaction activity and elevated network fees. In May 2024, during the peak of the Ordinals craze, transaction fees accounted for over 75% of miner revenue—a historical high.

After mempool size peaked at 350 million bytes in late 2023, it gradually normalized. The introduction of Runes improved UTXO management efficiency.

Throughout the year, Ordinals, Runes, and BRC-20 alternated as primary drivers of transaction volume, with Runes ultimately dominating.

-

Market and Adoption

Platforms like Magic Eden and OKX dominate the marketplace, capturing over 95% of trading volume. Enhanced user experience and cross-chain bridges to Solana significantly increased Bitcoin NFT adoption.

Although Ordinals collections performed strongly early in the year, prices dropped more than 50% from their highs after the halving.

Protocols like Liquidium allow users to use Ordinals and Runes as collateral for loans, expanding Bitcoin-native DeFi use cases. Meanwhile, stablecoins such as USDh (by Hermetica) aim to use Bitcoin as underlying collateral, though technical constraints remain.

-

Cultural and Economic Shifts

Memecoins, digital art, and decentralized markets are redefining how Bitcoin is used. While speculative, these trends reflect Bitcoin’s core values of censorship resistance and permissionless innovation.

Tokenized Bitcoin: BTC on EVM Chains

Using tokenized Bitcoin on EVM chains (Ethereum Virtual Machine chains) remains the most popular way to unlock Bitcoin’s utility—rather than relying on Layer 2 networks. Changes in WBTC’s custodial model reshaped the market landscape for tokenized Bitcoin in 2024.

-

Tokenized Bitcoin and DeFi Applications

Tokenized Bitcoin (e.g., WBTC, tBTC, and emerging cbBTC) accounts for over 25% of total value locked (TVL) in decentralized finance (DeFi).

While Ethereum remains the primary testing ground for DeFi innovation, Bitcoin-centric solutions—such as Bitcoin Layer 2s—are attempting to reduce reliance on custodians and better align with Bitcoin’s decentralized ethos. However, these Layer 2 networks still have a long road ahead before full deployment.

-

Failures and Lessons Learned

Early tokenized Bitcoin projects—such as renBTC, imBTC, and HBTC—failed due to low adoption, hacks, or centralization risks. We refer to these failed attempts as the “Wrapped Bitcoin Graveyard” to analyze their critical vulnerabilities.

Changes in BitGo’s custodial model weakened confidence in WBTC’s dominance. In contrast, Coinbase’s cbBTC rapidly rose, achieving TVL exceeding 20,000 BTC.

-

tBTC and Decentralized Alternatives

tBTC offers a decentralized approach to tokenizing Bitcoin, eliminating custodial risks. With broad integration across protocols like Aave and GMX, tBTC’s supply grew fourfold in 2024—reflecting strong market demand for decentralized solutions.

-

Bitcoin-Backed Stablecoins

Stablecoins backed by Bitcoin (e.g., USDe and crvUSD) are gaining traction, with 30–60% of their collateral consisting of Bitcoin. However, these instruments may introduce risks that Bitcoin users are unwilling to accept.

Fully Bitcoin-backed stablecoins remain a key development goal, as they better align with Bitcoin’s principles of decentralization and openness.

-

EVM Dominance

Despite growing attention to Bitcoin Layer 2s, the EVM ecosystem and its mature applications currently dominate Bitcoin’s use in DeFi.

Bitcoin Layer 2s, while promising, are primarily used for speculative activities like airdrop farming. Meaningful applications will require deeper alignment with Bitcoin’s core protocol.

Bitcoin Staking

In 2024, Bitcoin staking saw rapid growth. Numerous new protocols leveraged Bitcoin—the “hardest money”—to support Proof-of-Stake (PoS) systems. Through native staking, liquid staking derivatives (LSDs), and restaking innovations, platforms unlocked Bitcoin liquidity, with total value locked (TVL) surpassing $10 billion.

-

Native Staking

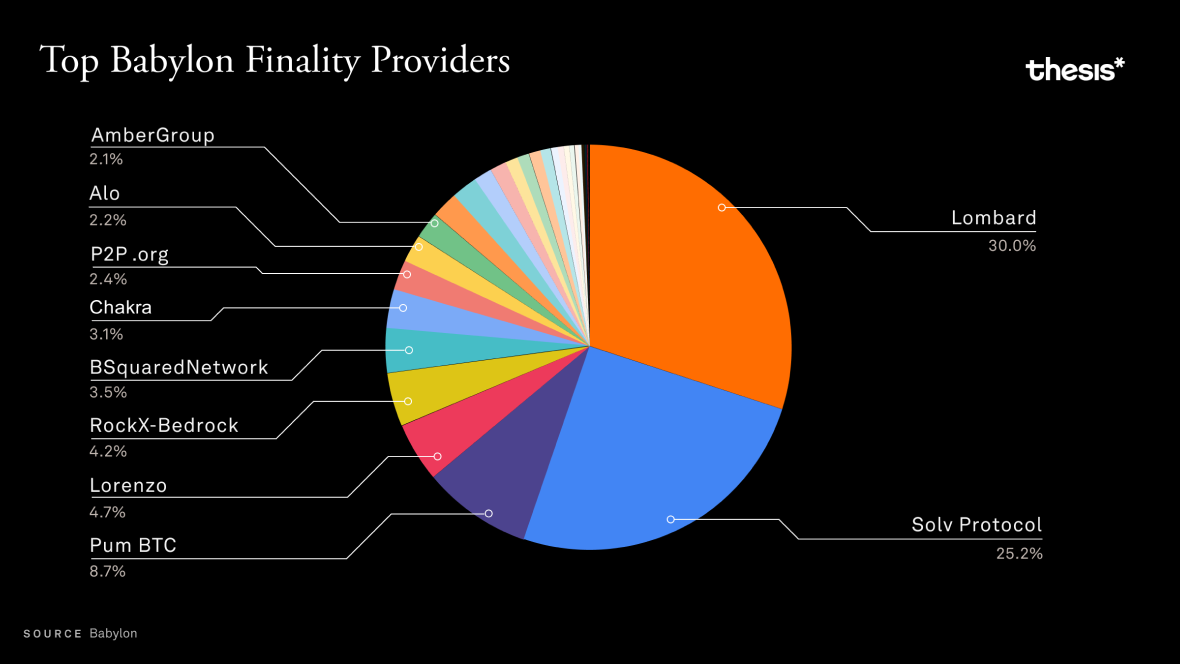

The Babylon protocol allows Bitcoin holders to stake their BTC on PoS chains while retaining custody on the Bitcoin network.

Currently, 34,938 BTC—worth approximately $3.53 billion—are staked, with 82,440 active stakers.

Through covenants and slashing mechanisms, the protocol effectively secures PoS chains.

-

Liquid Staking Derivatives (LSDs)

Lombard: Users receive LBTC after staking Bitcoin, earning Babylon rewards while using LBTC in DeFi (e.g., Curve, Uniswap). The platform’s TVL stands at $1.68 billion.

Solv Protocol: Uses a Staking Abstraction Layer (SAL) to unify Bitcoin staking operations. Its LSDs—such as solvBTC—aggregate Bitcoin liquidity across chains, with TVL exceeding $3 billion.

Examples include solvBTC.BBN (Babylon), solvBTC.CORE (CoreDAO), and solvBTC.ENA (Ethena).

-

Restaking

Platforms like Lombard and Solv enable restaking, where staked Bitcoin generates additional DeFi yields—through liquidity provision and lending. Lombard alone has over $1.04 billion in restaked value.

Bitcoin staking remains in its early stages, largely driven by reward incentives and high yields. Long-term sustainability depends on growing real-world demand. However, dominant players like Lombard and Solv may pose centralization risks. Together, they account for $1.32 billion in TVL on Babylon.

While liquid staking enhances flexibility, it introduces additional trust assumptions. The future trajectory of Bitcoin staking remains to be seen.

Scalability: Sidechains, Rollups, and Layer 2 Networks

-

New Developments

Taproot and opcode revivals: Taproot (launched in 2021) and proposals like OP_CAT enhanced Bitcoin’s programmability, privacy, and covenant capabilities.

BitVM: Introduces Turing-complete contracts off-chain without changing Bitcoin’s consensus, enabling complex computations.

-

Layer 2 Solutions

Sidechains:

Examples include Rootstock (RSK), Liquid Network, and Mezo.

Sidechains bring smart contract functionality and higher throughput to Bitcoin. However, they typically rely on federated security models or merged mining for chain security.

Rollups:

-

ZK-Rollups: Use zero-knowledge proofs for fast transaction finality with strong cryptographic security.

-

Optimistic Rollups: Assume transactions are valid by default, using fraud proofs to detect invalid ones. This boosts scalability but introduces confirmation delays. Example: Citrea uses zk-STARKs and the Clementine bridge to build a trustless Bitcoin bridge.

State Channels (e.g., Lightning Network):

Technologies like the Lightning Network enable near-instant, low-fee payments off-chain.

The Lightning Network’s total capacity reached 5,380 BTC, achieving 11% annual growth.

A trend toward fewer but larger channels has emerged, raising concerns about network centralization.

In developed nations (e.g., the U.S. and Germany), Lightning is mainly used for large payments; in emerging markets, it supports micropayments and small transactions.

-

Build on Bitcoin (BOB):

Though BOB uses Ethereum as its settlement layer, its core mission is to build a Bitcoin-centric economy, leveraging assets like WBTC and tBTC.

In 2024, BOB’s TVL surged from $1.5 million to $238.27 million, driven by deep integrations with Uniswap V3 and Avalon Finance.

-

CoreDAO and Ecosystem Growth

CoreDAO combines Bitcoin’s security with DPoW (Dual Proof of Work) and DPoS (Delegated Proof of Stake) via its Satoshi Plus consensus mechanism.

The ecosystem launched coreBTC—backed by Bitcoin—for use in DeFi, expanding Bitcoin’s utility.

In 2024, CoreDAO achieved remarkable growth: 95% network expansion, 13.3 million new addresses, and daily transaction peaks exceeding 500,000.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News