Ethereum Reclaims $4,000: Are Fundamental Factors in the Ecosystem Driving the Price?

TechFlow Selected TechFlow Selected

Ethereum Reclaims $4,000: Are Fundamental Factors in the Ecosystem Driving the Price?

Ten years have passed, and Ethereum is no longer in its startup phase. For the next decade, Ethereum's future is already clearly visible.

Author: Kaori, BlockBeats

After a recent pullback in the bull market, ETH prices have once again climbed above $3,900. Looking back at Ethereum's development over the past year, there are many complex factors and emotions at play. On one hand, the successful completion of the Cancun upgrade and the formal approval of spot ETFs have given Ethereum a new bullish outlook both technically and fundamentally. On the other hand, while Bitcoin, SOL, and BNB have successively broken new all-time highs, ETH’s price remains stuck near the $4,000 mark.

The chart above shows three main phases in ETH’s price movement this year, with each rally driven by different catalysts. At the beginning of the year, following the approval of Bitcoin spot ETFs, Ethereum’s price rose along with overall market sentiment, briefly surpassing $4,100. However, by late March, it began to decline alongside the broader market. Meanwhile, Solana and its ecosystem surged strongly, leading to significant outflows of liquidity from the Ethereum ecosystem.

In May, the approval of Ethereum spot ETFs led to a short-lived price spike. However, demand was not as strong as seen with Bitcoin. The initial market reaction to the Ethereum ETF launch was negative, as speculative investors who had bought into Grayscale’s Ethereum Trust expecting conversion into an ETF took profits, resulting in $1 billion in outflows and downward pressure on ETH’s price. Additionally, Ethereum’s narrative as a tech innovation product—compared to BTC’s “digital gold” positioning—has been less appealing to traditional markets. Furthermore, the SEC’s restriction prohibiting staking functionality in spot Ethereum ETFs objectively weakened their attractiveness.

Following this, controversies around the Ethereum Foundation, restaking ecosystems, and roadmap disputes followed one after another, marking a dark period for Ethereum.

In November, the U.S. election concluded, and the pro-crypto Republican party and Donald Trump brought renewed confidence and liquidity into the entire crypto ecosystem, triggering Ethereum’s third major rally of the year. This time, however, the surge was different: institutions entered openly, signaling through capital flows what they recognize and support. Ethereum is destined to stay true to its original vision as the “world computer.”

Improved Liquidity Fundamentals

Since December, Ethereum spot ETFs have recorded net inflows exceeding $2.2 billion over 15 consecutive days. Nate Geraci, president of The ETF Store, noted on social media that advisors and institutional investors are only just beginning to pay attention to this space.

In the third quarter of this year, banks such as Morgan Stanley, JPMorgan Chase, and Goldman Sachs significantly increased their holdings in Bitcoin ETFs, nearly doubling their positions quarter-over-quarter. But their investments weren’t limited to Bitcoin alone. According to recent 13F filings, these institutions have also started purchasing Ethereum spot ETFs since then.

Additionally, earlier this year, the Wisconsin State Investment Board and Michigan Retirement Systems purchased Bitcoin spot ETFs. In the third quarter, Michigan further acquired over $13 million worth of Ethereum spot ETFs. This indicates that pension funds—representing low-risk tolerance and long-term investment strategies—not only acknowledge Bitcoin’s role as digital value storage but also recognize Ethereum’s growth potential.

Shortly after the approval of Ethereum spot ETFs, JPMorgan published a report suggesting that demand would be far below that of Bitcoin spot ETFs. However, the report projected up to $3 billion in net inflows for spot Ethereum ETFs by the end of the year, potentially rising to $6 billion if staking were allowed.

Jay Jacobs, head of thematic and active ETFs at BlackRock, said during the "ETFs in Depth" conference: “Our exploration of Bitcoin, and especially Ethereum, is still just the tip of the iceberg. Only a small fraction of our clients currently hold (IBIT and ETHA). Our current focus is on expanding adoption here rather than launching new altcoin ETFs.”

A Blockworks Research survey found that a vast majority (69.2%) of respondents currently hold ETH, with 78.8% being investment firms or asset managers. This suggests institutional willingness to participate in ETH staking has reached a critical mass, driven by yield generation and contributions to network security.

Institutions are actively engaging in ETH staking, though participation levels and methods vary. Regulatory uncertainty has led to divergent attitudes—some institutions proceed cautiously, while others are less concerned. Regardless, institutional participants demonstrate high awareness of operational aspects and risks associated with staking.

Tide Turning

After FTX collapsed, Coinbase, Kraken, Ripple, and others faced severe crackdowns from U.S. regulators like the SEC. Many crypto projects couldn’t even open bank accounts with mainstream U.S. financial institutions. During the previous bull market, traditional financial investors entering via DeFi also suffered massive losses. Large funds such as Thoma Bravo, Silver Lake, Tiger Global, and Coatue didn’t just lose money on FTX—they also invested at high valuations in crypto projects that failed to deliver on grand promises, with capital still unrecovered.

In the second half of 2022, many DeFi projects were forced to relocate outside the United States. As qw, co-founder of Alliance DAO, noted: “Two years ago, about 80% of qualified crypto startups were based in the U.S., but that number has steadily declined and now stands at roughly 20%.”

But on November 6, Trump won the election—the green light the U.S. financial system had been waiting for finally turned on.

Trump Saves Crypto

Trump’s victory undoubtedly cleared away regulatory uncertainties for institutional adoption.

By establishing the Department of Government Efficiency and bringing together Wall Street elites like Elon Musk, Peter Thiel, and Marc Andreessen, and later appointing Paul Atkins as SEC chair and PayPal co-founder David Sacks as “White House Director of AI and Cryptocurrency,” Trump signaled his intent to build a crypto-friendly administration.

JPMorgan analysts suggest that several stalled cryptocurrency bills could swiftly pass under a Trump administration, including the FIT21 Act (Financial Innovation and Technology for the 21st Century), which would clarify regulatory responsibilities between the SEC and CFTC, offering much-needed clarity for the industry. They also expect the SEC’s aggressive enforcement approach to evolve into a more collaborative stance, and that SAB 121—the rule restricting banks from holding digital assets—could be repealed.

High-profile lawsuits against companies like Coinbase may be eased, settled, or even dropped. Regulatory notices sent to firms like Robinhood and Uniswap could be reconsidered, reducing litigation risk across the broader crypto sector.

Beyond departmental and legislative reforms, the Trump team is reportedly considering drastically cutting, merging, or even eliminating key Washington banking regulators. Insiders reveal that Trump advisers have asked potential candidates for banking regulator roles whether entities like the Federal Deposit Insurance Corporation (FDIC) could be abolished. Questions were also raised regarding FDIC and Office of the Comptroller of the Currency nominees. Plans to merge or comprehensively reform the FDIC, OCC, and the Federal Reserve have also been floated.

As policy benefits gradually unfold, large-scale institutional capital from the U.S. market is poised to return to crypto.

DeFi Renaissance Underway

More conservative capital sources—such as family offices, endowments, and pension plans—will not only invest in Ethereum spot ETFs but also re-enter proven DeFi sectors from the last cycle.

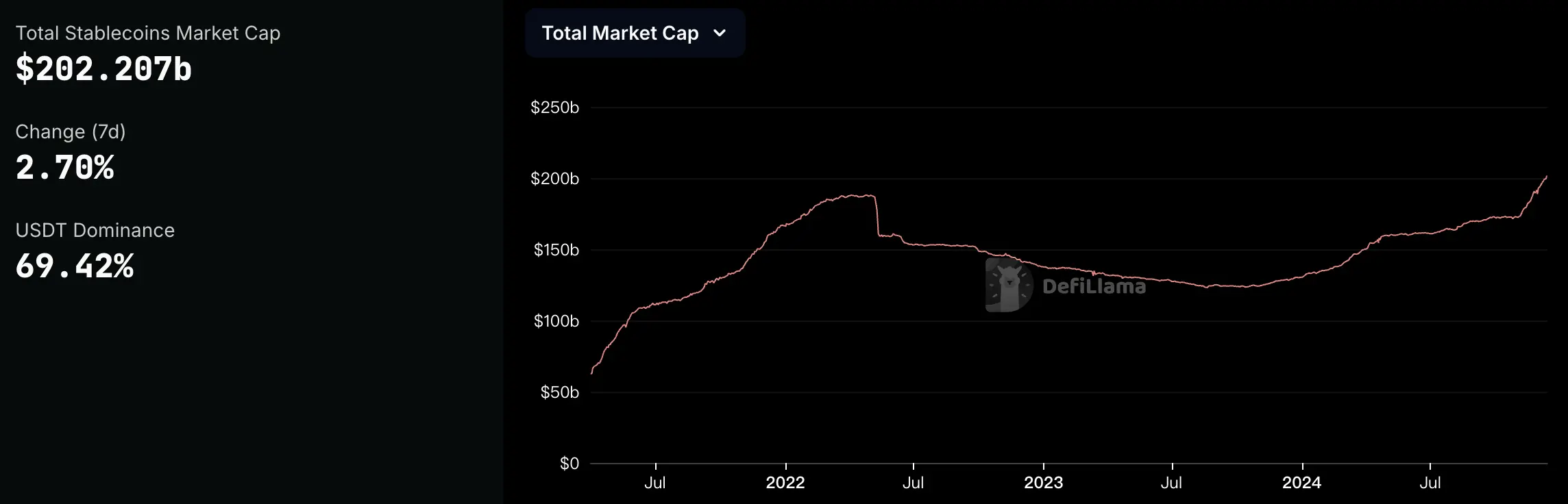

Compared to 2021, stablecoin supply has reached record highs. In the month following Trump’s election, stablecoins saw nearly $25 billion in new issuance, bringing total market cap to $202.2 billion.

Coinbase, the leading publicly traded U.S. crypto firm, made notable strides in DeFi this year beyond political contributions. As the largest crypto ETF custodian, it also launched cbBTC.

Because cbBTC avoids the custody and counterparty risks inherent in most Bitcoin ETFs, some traditional financial institutions may reassess paying fees to hold Bitcoin ETFs and instead opt for near-zero-cost participation in DeFi. This shift could channel capital into battle-tested DeFi protocols, especially when DeFi yields remain more attractive than traditional finance returns.

Another major DeFi segment this cycle is RWA (real-world assets). In March, BlackRock made a high-profile entry into the RWA space by partnering with U.S.-based tokenization platform Securitize to launch BUIDL (BlackRock USD Institutional Digital Liquidity Fund). Capital giants like Apollo and Blackstone, which manage massive pools of capital, are also preparing to enter, promising substantial liquidity injections.

Since Trump’s election, compliant DeFi has become a hot topic, particularly after the Trump family launched their own DeFi project. Established blue-chip Ethereum DeFi projects like Uniswap, Aave, and Lido reacted immediately with price increases post-election, while newer DeFi tokens like COW, ENA, and ONDO hit new highs.

Meanwhile, WLFI, the Trump-affiliated DeFi project, has been frequently trading Ethereum-based tokens. After multiple transactions converting 5 million USDC into 1,325 ETH, its multisig wallet subsequently purchased $10 million worth of ETH, $1 million of LINK, and $1 million of AAVE. Recent whale accumulation of ETH continues to signal that both institutions and large holders are refocusing on the Ethereum ecosystem.

WLFI Multisig Wallet Holdings

The price performance of both legacy and emerging DeFi projects speaks for itself. Currently, DeFi’s TVL sits around $100 billion, while the total value of crypto and related assets is approximately $4 trillion. Active funds in DeFi represent just 2% of the overall market—still very small. This implies immense room for growth as regulatory sentiment improves.

Aave exemplifies the beneficiaries of this “capital return” trend. Its price broke out before Trump’s election, followed by explosive growth in TVL and revenue: TVL surpassed its October 2021 peak, reaching $22 billion; the token price climbed from a yearly low of $80 to exceed the March high of $140 by early September, accelerating further in November; protocol daily revenue exceeded its second-highest level from September 2021, while weekly revenue hit an all-time high.

Although Aave recently upgraded to V4, technological innovation alone may not justify such massive gains. Regulatory shifts and capital inflows clearly dominate the narrative—and these forces may spill over into other sectors favored by institutions in the last cycle, such as NFTs.

Ethereum’s Future

Mid-year, Ethereum faced intense debate and controversy over ecosystem development. With Solana’s rise, new and old competing blockchains began capturing Ethereum’s developers and users, shaking confidence in its ecosystem. It seemed Ethereum had lost sight of its original mission. As the first blockchain to introduce smart contracts, Ethereum leveraged first-mover advantage to attract institutional investment throughout the last cycle. Whether DeFi, gameFi, NFTs, or metaverse projects—all revolved around Ethereum. Its identity as the “world computer” became deeply ingrained.

Despite optimistic improvements in liquidity fundamentals, Ethereum’s core on-chain metrics—daily transaction count, gas fees, active addresses—have not shown significant growth. This means on-chain activity hasn't risen in tandem with price, and blockspace remains underutilized.

Ethereum Gas Fee Levels

Over the past few years, Ethereum focused on building crypto infrastructure, providing abundant cheap blockspace. While this improved Dapp performance and reduced L2 expansion costs, insufficient market liquidity and low transaction demand meant Ethereum’s vast blockspace remained largely unused.

However, this isn’t truly a long-term issue. As previously discussed, institutional capital is gradually returning—even developing bespoke blockchain use cases. For Ethereum, with its superior security and flexible architecture, serving enterprise clients (to B) is where its strength lies. It holds overwhelming advantages in security and supports countless EVM-compatible projects, offering developers an option that’s virtually “impossible to fire.”

Ethereum’s long-term value will depend on the scarcity of its blockspace—that is, the real, sustained global demand for Ethereum’s settlement capacity. As institutions and applications flood in, this scarcity will become increasingly evident, solidifying Ethereum’s foundational value. Ethereum is the institution’s world computer. Starting with DeFi, institutions will ultimately resolve the issues of excess blockspace and roadmap disputes.

In early December, Ethereum researcher Jon Charbonneau wrote a detailed article arguing that Ethereum needs a clearer “North Star” goal. He proposed rallying the ecosystem around the idea of the “world computer,” just as Bitcoin has “digital gold” and Solana has “Nasdaq on chain.”

Ten years on, Ethereum is no longer in startup mode. For the next decade, its future path is becoming clear.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News