PolyFlow Insight: The Next Step for Stripe & Bridge is PayFi

TechFlow Selected TechFlow Selected

PolyFlow Insight: The Next Step for Stripe & Bridge is PayFi

PolyFlow, as the infrastructure for PayFi, is harnessing the transformative power of cryptocurrency and blockchain technology to build a new PayFi crypto payment network that accelerates the adoption of PayFi applications.

Stripe's $1.1 billion acquisition of Bridge, a stablecoin API infrastructure provider, marks the largest acquisition in cryptocurrency history. What prompts reflection is not the transaction itself, but rather the rapid integration of the entire stablecoin ecosystem into traditional finance.

Both Stripe and PayPal wield vast global influence and have already connected their existing ecosystems to stablecoin-based crypto payment networks through different approaches. By integrating stablecoins, these fintech giants are advancing along the entire payment value chain. Following this integration, merging with DeFi to build new PayFi application scenarios becomes a natural next step.

1. Stripe & Bridge Acquisition

Founded in 2009, Stripe focuses on providing online payment collection services for businesses, offering an all-in-one payment solution. As one of the three major U.S. payment giants, Stripe processed $1 trillion in payment volume in 2023, supporting over 135 currencies and more than 50 payment methods worldwide.

In 2014, Stripe became the first major payment company to offer Bitcoin payments. However, due to long confirmation times, high transaction fees, and price volatility on the Bitcoin network, demand declined, leading to the discontinuation of this feature in 2018.

Despite that, Stripe has continued to monitor and gradually expand its footprint in the crypto space. On October 10, Stripe announced the relaunch of its crypto payment gateway (Pay With Crypto) for U.S. businesses, partnering with MetaMask, Coinbase, Magic Eden, Audius, and others, enabling U.S. merchants to:

-

Accept USDC and USDP via Ethereum, Solana, and Polygon networks from over 150 countries (Crypto Payin);

-

Receive payouts in stablecoins or fiat USD (Crypto/Fiat Payouts);

-

Integrate checkout processing, payment elements, and payment intent APIs, soon extending to subscription services.

Certainly, Stripe aims for even more.

(https://x.com/Stablecoin/status/1848390039975469094)

In its latest announcement, Bridge stated: "Bridge and Stripe will collaborate to accelerate the adoption and utility of tokenized dollars, making it easier for everyone around the world to transfer, store, and spend money. Through numerous real-world use cases, we've demonstrated that stablecoins can serve as core infrastructure for global fund flows, representing an entirely new payment platform—not because consumers or enterprises inherently want 'cryptocurrency,' but because stablecoins solve critical financial problems."

Bridge was founded by entrepreneurs Sean Yu and Zach Abrams. It is a stablecoin API infrastructure providing software tools that help companies accept stablecoin payments. The two previously sold Evenly, a Venmo competitor, to Block in 2013; Abrams also served as a senior executive at Coinbase.

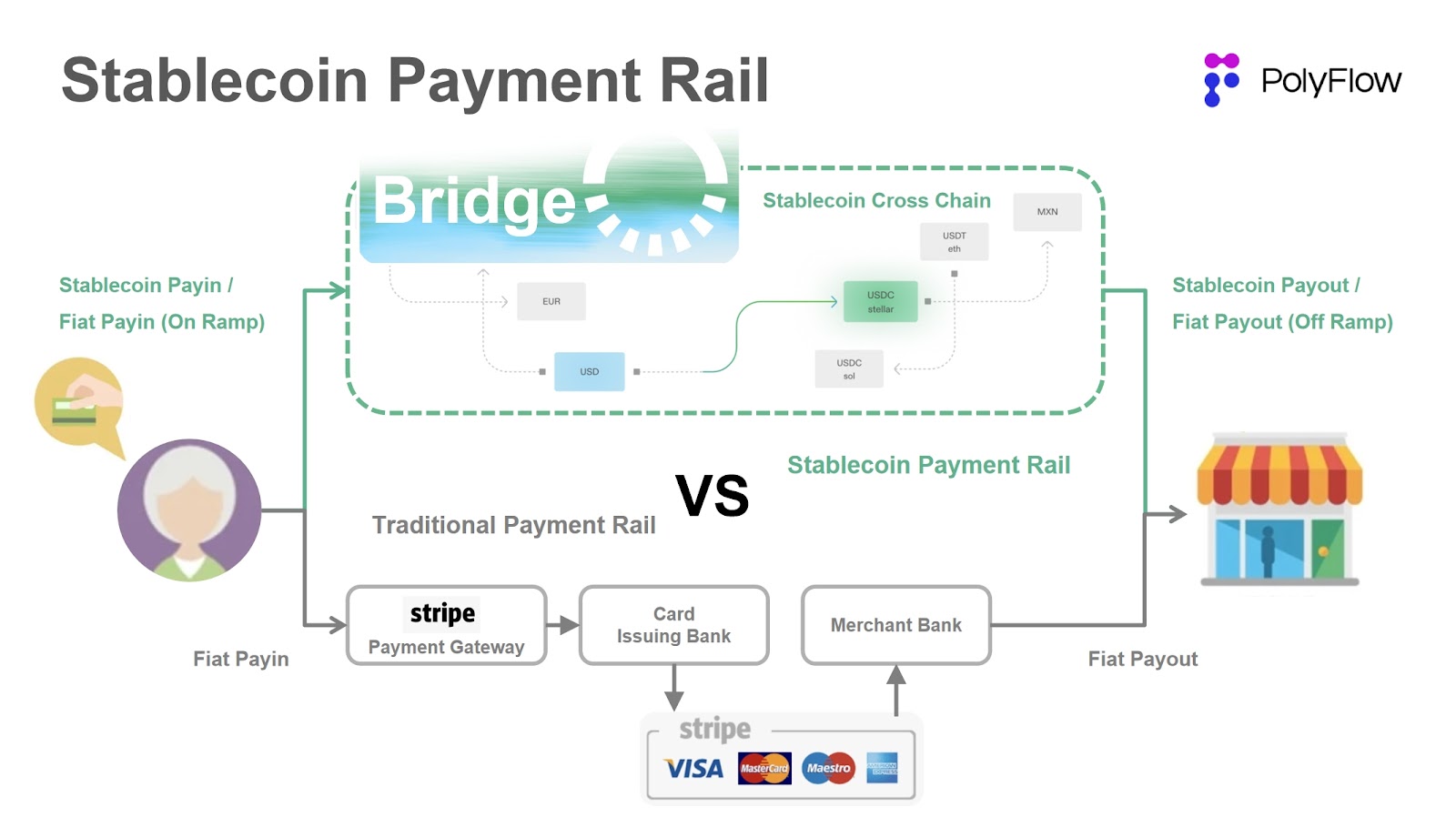

Bridge’s flagship product is the Orchestration API—an API that integrates stablecoin payments into enterprises’ existing operations while handling compliance, regulatory, and technical complexities. Combined with Bridge’s proprietary solutions—1) cross-chain stablecoin transactions, 2) fiat/crypto on/off-ramps, and 3) virtual bank accounts—the Orchestration API enables businesses to seamlessly adopt stablecoin payments with a smooth, frictionless experience.

Bridge claims its API allows funds to be transferred globally within minutes, facilitates seamless stablecoin payments, converts local fiat into stablecoins, and offers dollar and euro accounts for global consumers and businesses, enabling savings and spending in USD and EUR.

If Bridge helps Stripe build a stablecoin-based crypto payment network, broaden its ecosystem, and capture the network effects across the broader stablecoin landscape, then a PayFi network combining crypto payments and decentralized finance could further empower Stripe to deliver global financial services while achieving free value movement.

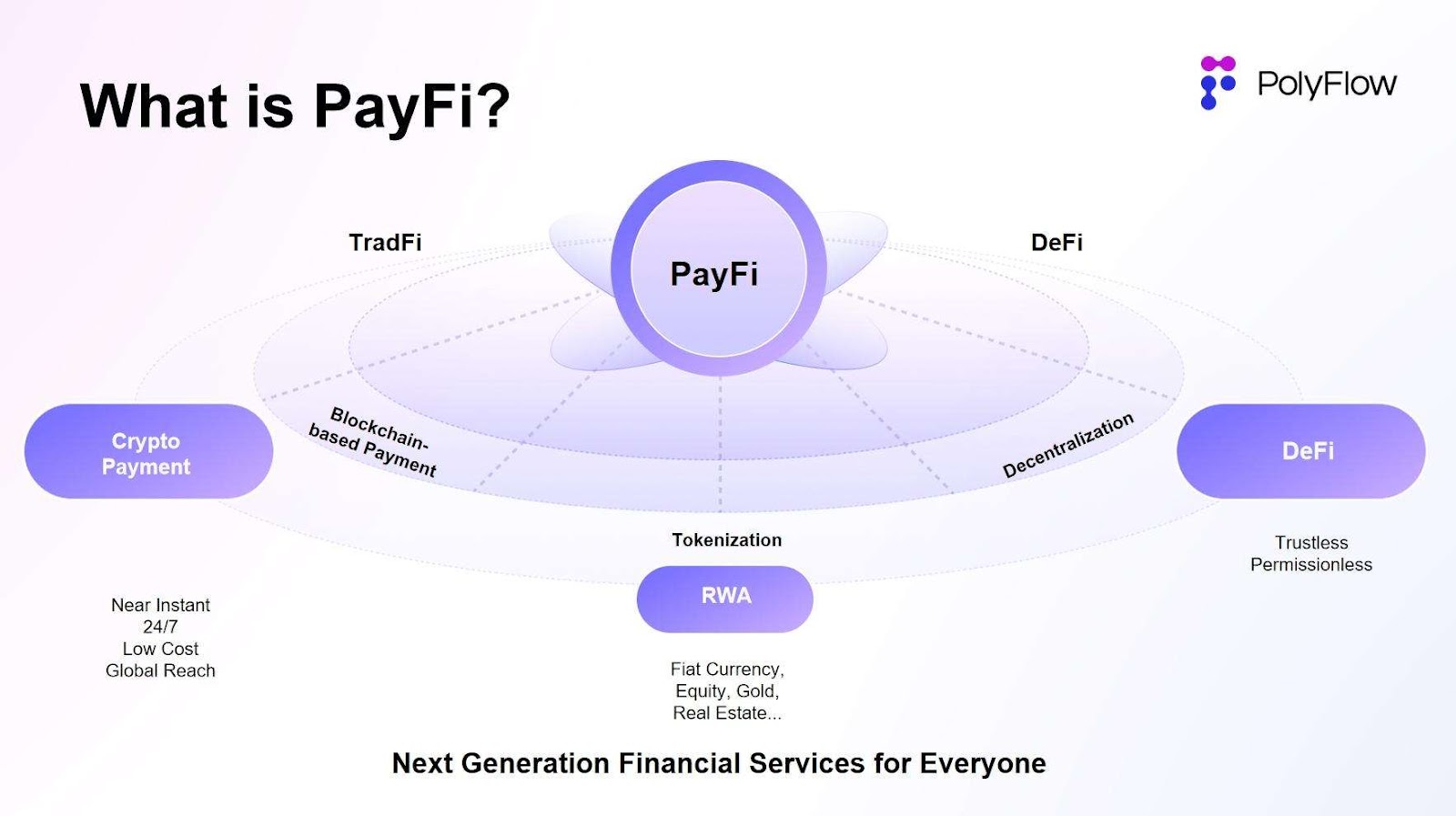

2. What Is PayFi?

PayFi, short for Payment Finance, refers to an innovative application model that combines payment functionality with financial services using blockchain and smart contract technology. At its core, PayFi leverages blockchain as a settlement layer, integrating the advantages of crypto payments and decentralized finance (DeFi) to enable efficient and open value movement.

The goal of PayFi is to realize the vision outlined in the Bitcoin white paper—a peer-to-peer electronic cash system without reliance on trusted third parties—while fully harnessing DeFi capabilities to create a new financial market. This includes delivering novel financial experiences, building complex financial products and use cases, and ultimately forming an entirely new value chain.

PayFi was first introduced as a new narrative by Lily Liu, President of the Solana Foundation, during the 2024 Hong Kong Web3 Festival. In her view, PayFi builds a new financial market centered around the time value of money (TVM)—something difficult or impossible to achieve in traditional finance.

This emerging PayFi financial market not only improves upon traditional finance in terms of efficiency—offering instant settlement, lower costs, transparency, and global reach—but also leverages DeFi to enable decentralization, permissionless access, self-custody of assets, and personal sovereignty across a global network.

(https://x.com/Polyflow_PayFi)

3. Why Stripe & Bridge Are Headed Toward PayFi

PayFi represents the further construction, expansion, and deepening of crypto payment networks. Based on blockchain and smart contracts, and incorporating DeFi, it forms a new financial market that creates globally accessible, payment-related financial derivative services such as lending, wealth management, and investment.

The emergence of Bridge supports the implementation of Stripe’s “Pay With Crypto” strategy. More of Stripe’s existing business will begin settling transactions in stablecoins, reducing internal costs, improving operational efficiency, and enhancing user experience. Meanwhile, Stripe can leverage Bridge to establish a stablecoin payment pathway outside the traditional banking, card networks, and SWIFT systems—extending beyond its current ecosystem while maintaining compatibility with DeFi.

We’ve already seen how Bridge’s Issuance API helps clients issue stablecoins and deploy balances into U.S. Treasuries to improve capital efficiency. It won’t be long before we see Bridge build additional PayFi applications atop its stablecoin payment infrastructure by integrating DeFi.

With Bridge, Stripe’s network effect is no longer confined to its own ecosystem but extends across the entire stablecoin market. Similarly, a PayFi ecosystem built on DeFi can transcend geographical limitations of traditional financial services, enabling free value circulation and greater financial inclusion for users worldwide—precisely the direction PayPal is pursuing after launching its own stablecoin.

4. PolyFlow Enables PayFi Application Adoption

Stripe and PayPal both possess massive global network effects and are connecting their established networks to stablecoin payment systems through different paths. Integrating with DeFi afterward to unlock new PayFi scenarios thus appears inevitable.

If Stripe & Bridge—or stablecoins in general—are seen as games played among Web2 giants, PolyFlow enters the scene as PayFi infrastructure, helping PayFi projects launch and participate in building the global payment network.

PolyFlow’s core philosophy is to modularize processes and use decentralized mechanisms to better meet regulatory compliance standards, eliminate custodial risks, and leverage blockchain features to connect with the DeFi ecosystem, accelerating large-scale adoption of PayFi applications.

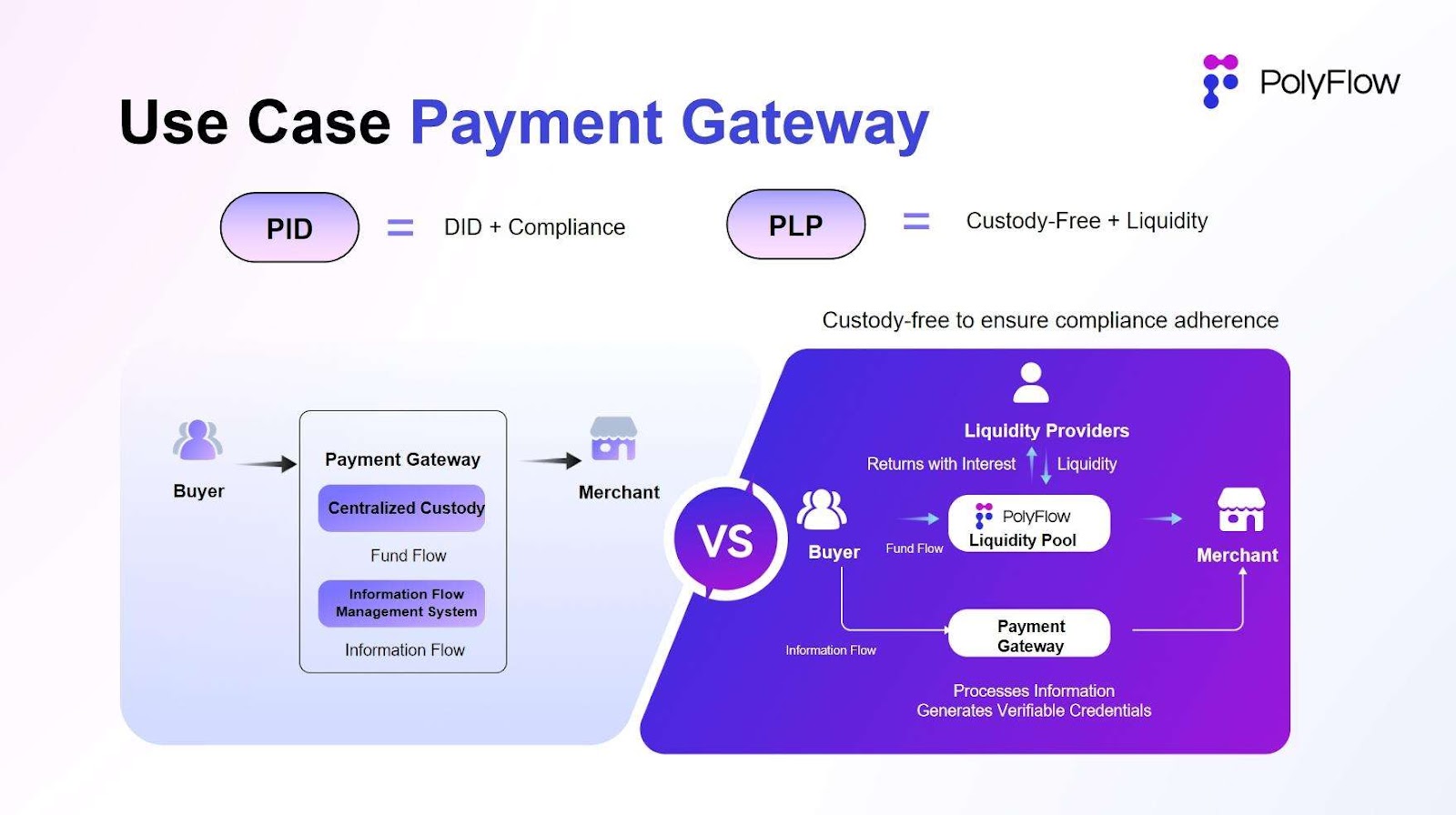

PolyFlow introduces two key components: Payment ID (PID) and Payment Liquidity Pool (PLP):

-

PID links to payment information flows and serves as a powerful tool for user identity verification, compliant onboarding, privacy protection, data sovereignty, AI-driven data processing, and X-to-earn models;

-

PLP connects to payment fund flows and is managed by smart contracts to securely handle transaction funds. It provides a safe and compliant framework for digital asset transfer, custody, and issuance while introducing composability and scalability from the DeFi ecosystem.

Together, PolyFlow establishes a lightweight, regulation-compliant, non-custodial, and DeFi-compatible architecture for PayFi applications, along with a secure and compliant framework for digital asset movement, custody, and issuance.

A crypto payment gateway built on PolyFlow delivers the same advantages achieved by Stripe & Bridge after integrating stablecoin payments:

-

Cost reduction and efficiency gains: Peer-to-peer transactions between buyers and sellers eliminate intermediaries and associated fees from banks and card networks.

-

No custodial risk: Funds are fully held in on-chain smart contracts, transparent and verifiable, removing risks tied to centralized custodians.

-

DeFi compatibility: On-chain Payment Liquidity Pools can integrate with DeFi protocols to enable PayFi use cases such as lending and staking.

-

Global reach: Merchants gain the option to accept crypto payments, opening access to over 600 million global crypto users.

As a foundational PayFi infrastructure, PolyFlow is harnessing the transformative power of cryptocurrencies and blockchain technology to build a new PayFi payment network. It accelerates the deployment of PayFi applications, drives the shift toward innovative financial paradigms, and unlocks the true potential of Web3.

In the end, turning the grand vision of the Bitcoin white paper into reality.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News