PolyFlow Payment ID: PayFi's Identity Revolution and the Realization of DID Value

TechFlow Selected TechFlow Selected

PolyFlow Payment ID: PayFi's Identity Revolution and the Realization of DID Value

This article will explore the unique features of Payment PID, its advantages and role within the PolyFlow ecosystem, as well as its value proposition, potential use cases, and future outlook for individual users.

PolyFlow is an innovative PayFi protocol designed to connect real-world assets (RWA) with decentralized finance (DeFi). As the infrastructure layer of the PayFi network, PolyFlow integrates traditional payments, crypto payments, and decentralized finance (DeFi), processing real-world payment scenarios in a decentralized manner. PolyFlow provides the essential infrastructure for building PayFi applications, ensuring compliance, security, and seamless integration of real-world assets to drive the creation of a new financial paradigm and industry standards.

PolyFlow’s two powerful tools—PID (Payment ID) and PLP (PolyFlow Liquidity Pool)—serve as gateways for on-chain compliance access and fund custody, respectively, redefining how decentralized payment systems operate within the Web3 space and expanding innovative use cases for PayFi.

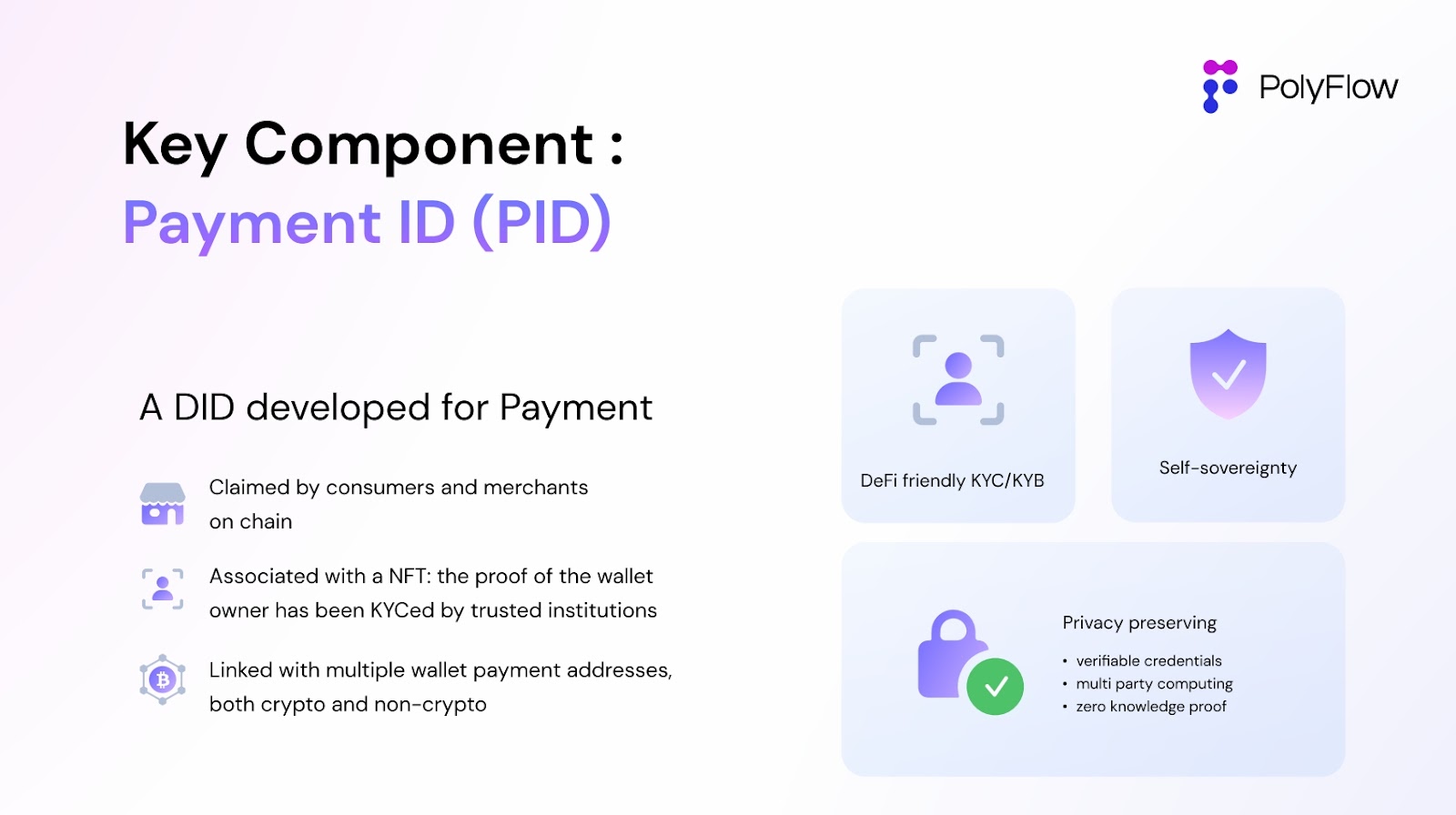

The PID introduced by PolyFlow is a DID designed for payments (a DID developed for Payment), aiming to bridge users’ real-world identities with their on-chain wallets. It enables users to store, verify, and manage various digital credentials while protecting privacy and asserting identity sovereignty, meeting compliance requirements for payments and finance, and leveraging blockchain technology to enable global trust transfer.

This article explores the unique features, advantages, and role of the payment-oriented PID within the PolyFlow ecosystem, along with its value proposition, potential applications, and future outlook for individual users.

1. What is DID?

DID Concept

DID stands for Decentralized Identity, a decentralized identity system. Proposed by W3C (World Wide Web Consortium), DID is a decentralized identifier that does not rely on any centralized entity, authority, or third party for verification. A DID is a self-owned, distributed, verifiable, and persistent identifier applicable to any subject—including individuals, organizations, and objects.

Users first generate a public-private key pair, then package the public key and other identity information into a DID document. This document is stored on a decentralized network (such as a blockchain) and assigned a unique DID. Users can control this DID using their private key—for example, updating or revoking it.

Ideally, during the decentralized identity phase, users have full control over their own information. This is the core of DID, embodying the principle of self-sovereignty.

In relation to PolyFlow's PID system, different cryptocurrency wallets can be linked to this PID. While maintaining asset autonomy, users can bind all personal proof data to this DID and store it on-chain as verifiable credentials (VCs), enabling external verification while preserving user privacy.

Why Do We Need DID?

Compared to traditional user identity systems (IDs), one relies on phone numbers, email addresses, WeChat, Alipay, Google, or Facebook to log into specific websites or systems, while the other involves credentials issued by governmental or authoritative bodies. In both cases, sensitive user identity information is stored within the target system. The system administrators effectively own all user data and possess actual control rights including querying, altering, or deleting it.

Consider some extreme examples: financial institutions can arbitrarily adjust your credit rating, affecting your loans or cash flow; gaming platforms can freeze your account worth thousands overnight; governments can freeze your assets or revoke your qualifications and business licenses at will. You don’t truly own your account identity—you merely hold temporary usage rights. Behind these actions, such entities can exploit your identity and data for profit.

The core idea of DID is transferring control of identity authentication from centralized institutions to individuals. By placing identity data on-chain, each person owns and controls their identity information, requiring explicit authorization before others can access it.

Centralized account systems can be frozen, but decentralized DID systems cannot—no one can freeze your assets.

Not your keys, not your coins. Through blockchain technology, we’ve achieved ownership over our assets. Similarly, our identity and personal data must also be under our own control.

Core Value of PID

Therefore, one of the core principles of Web3 is autonomy—what we call self-sovereignty. This encompasses three aspects:

1. Asset autonomy.

2. Identity autonomy.

3. Data autonomy.

These three points align perfectly with the core functions of PolyFlow’s PID, especially in payment scenarios involving large transaction volumes, strict compliance requirements, and extensive transaction data generation. Thus, the PID launched by PolyFlow is a DID designed specifically for payments—a DID developed for Payment.

As PolyFlow co-founder Raymond stated:

"A PID isn't necessarily just an ID for payments—it should be more like a physical wallet.

Imagine what else is in your physical wallet besides cash? It could be family photos (NFTs), bank cards, driver’s license, and identification documents (protected via ZK technology to safeguard user privacy).

From this perspective, a Wallet shouldn't equate only to a Money Wallet—there's much more that a PID can do."

2. Why Is DID So Important in Payments?

Currently, no DeFi protocols require compliance—anyone can freely participate in swaps on Uniswap or borrow/lend on Aave, achieving true permissionless access on-chain. However, in crypto payment scenarios, whenever fiat currency or real-world transactions are involved, due to anti-money laundering (AML) and other financial compliance regulations, Know Your Customer (KYC) procedures become mandatory. This is one of the fundamental differences between PayFi and DeFi.

We understand PayFi as the combination of Crypto Payments and DeFi, enabling mass crypto adoption. The prerequisite for this is compliant onboarding (including KYC/AML/CTF), which is absolutely critical. This is precisely why PolyFlow, as PayFi infrastructure, has introduced the PID.

The most direct value of PID lies in bridging the real-world identity system (KYC information tied to fiat) and the crypto world identity system (wallet addresses and cryptocurrencies), thereby connecting on-chain DeFi with off-chain real-world payment pathways. Only through this linkage can we use crypto to purchase real-world goods and services.

Returning to PID’s value proposition, compliant onboarding corresponds to DID’s goal of identity autonomy (covering credentials, proofs, qualifications, etc.), while transaction data relates to data autonomy (including on-chain and off-chain transaction behaviors). Otherwise, we remain vulnerable to centralized institutions that control identity data, leak privacy, and monetize user data for profit.

3. How PID Enables Identity Autonomy, Compliance Onboarding, and Privacy Protection

As shown above, the PID introduced by PolyFlow is a payment-focused DID—a DID developed for Payment. We can use PID to carry individual users’ verifiable credentials (Verifiable Credentials) for compliance onboarding, while also providing privacy protection.

Verifiable Credentials

One of blockchain’s core strengths is verifiability. Don’t trust it—verify it.

Verifiable Credentials (VCs) are typically issued by third parties to individuals, who then decide whom to authorize for access. VCs can be verified on-chain via blockchain technology, hence the term “verifiable” credentials.

VCs can represent academic diplomas from educational verification platforms, attendance certificates (NFTs issued by event organizers), or in-game achievements. Most importantly, they can include your KYC identity verification.

All these VCs are carried by DIDs and held directly by users, enabling identity autonomy. Users can authorize DApps to use these VCs or present them to third-party verification agencies—the most straightforward example being academic credential verification.

Currently, to prove your academic qualifications, you must go through official platforms like China’s Student Information Network (Chsi.com.cn), entering and verifying information on their website. The platform holds your proof—not you. This is the Web2 model.

The DID approach allows you to personally own your academic VC. If an internet company wants to use or verify it, you must explicitly authorize them. The company then uses your VC to validate authenticity through the original issuer (e.g., Chsi.com.cn).

Compliance Onboarding

Once users have VCs related to identity verification, the next step is compliance onboarding—one of PID’s most crucial components.

Compliance onboarding involves adherence to global regulatory frameworks, particularly in traditional financial payments. Whether conducting cross-border remittances or e-commerce purchases, users must meet varying levels of KYC/AML/CTF requirements depending on the country.

For instance, in certain countries, transactions under $500 may require only basic KYC—collecting name, age, and ID information. But amounts exceeding $500 necessitate Full KYC, requiring detailed data collection per national regulations. One such requirement is government-issued identity documentation—proving that the user is the legitimate holder of the ID card.

Since different countries/regions have varying KYC demands—some requiring only name and ID number, others adding address proof and other Full KYC details—PID can generate partial-information VCs tailored to specific regional requirements, proving that necessary data has been collected and is valid and verifiable.

One-Stop "Lightweight" Compliance Onboarding

Back to Crypto Payment / PayFi scenarios: because they interface with the real world—whether real-world payments or fiat on/off-ramps—KYC is mandatory. Therefore, PID introduces the concept of “lightweight” compliance: maintaining rigorous KYC identity verification while minimizing procedural complexity and enabling cross-platform compliance onboarding.

Previously, users had to undergo KYC separately on every platform, with no mutual recognition—leading to cumbersome processes. We aim to minimize KYC efforts by leveraging VCs stored within PID for cross-platform validation. For example, if a user completes KYC on Platform A and holds the corresponding VC via PID, they can seamlessly access Platform B without repeating KYC—as long as Platform B accepts the PID VC. Both platforms can even share KYC costs.

This one-stop “lightweight” compliance model greatly simplifies user interactions across platforms—whether on-chain or bridging on/off-chain environments. Projects also save significant costs (given high KYC compliance expenses) and improve operational efficiency. Combined with PID’s full compliance workflow—including AML/sanctions list screening, customer risk classification, and transaction monitoring—it offers a comprehensive solution for compliance onboarding. Projects no longer need to worry about compliance hurdles, accelerating true crypto mass adoption.

Privacy Protection

Another critical aspect of PID in compliance onboarding is privacy protection. PID leverages zero-knowledge proof (ZKP) technology to allow users to complete verifications without exposing private information.

Take the classic example of purchasing alcohol: how can a merchant verify the buyer is over 18? Traditionally, the user must show their entire ID card. With privacy-preserving methods or selective disclosure via PID VC, the user can instead provide a cryptographic proof confirming they are over 18—without revealing any other details from their ID.

This exemplifies how “lightweight compliance” combines with privacy protection.

4. How PID Enables Data Autonomy & Credit System Construction

Through blockchain and public-private key cryptography, we have achieved asset sovereignty. By binding Verifiable Credentials (VCs) to these keys, we further achieve identity sovereignty. But how can PID enable data sovereignty?

Data Sovereignty

Large internet and fintech companies often offer free services to collect vast amounts of user data, monetizing it through sales—an inherently problematic business model. These platforms profit heavily from user data, returning little to users. Moreover, centralized storage exposes user data to significant risks. Data breaches and illegal trading are common occurrences online.

In contrast, beyond carrying VCs, PID can also store users’ extensive on-chain transaction records and off-chain real-world payment data. This transaction data holds immense value and remains directly owned by the PID user—not by traditional tech giants—achieving true data autonomy.

Users can contribute their PID data for AI analysis and model training in exchange for rewards or token incentives—unlike centralized platforms that unilaterally exploit such data. Furthermore, on-chain and off-chain behavioral data linked to PID forms a foundational element for building an on-chain credit system.

Credit System Construction

By integrating identity and data information carried by PID, we can gradually build a decentralized trust network and credit system—an ecosystem based on real payment activities. Many users in the real world lack access to traditional credit scoring systems, yet they possess wallet addresses or can easily use them. PID can include these users, potentially reaching nearly 2 billion people globally—effectively advancing financial inclusion.

Within this ecosystem, we can develop credit-based financial services such as credit lending, buy-now-pay-later (BNPL), and supply chain finance. Only then can Crypto Payment/PayFi reach its full potential.

5. The Future of PayFi

The innovative introduction of PID gives PolyFlow—as PayFi infrastructure—a transformative advantage. It not only bridges traditional finance and DeFi ecosystems but also offers users a flexible and reliable way to manage digital identities, meet compliance requirements, engage in cross-platform transactions, and build on-chain credit.

In this new PayFi financial market, we can achieve efficiency gains over traditional finance: instant settlement, lower costs, transparency, and global accessibility. At the same time, by leveraging decentralized finance (DeFi), we enable decentralization, permissionless access, asset ownership, personal sovereignty, and financial inclusion across the global network.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News