PolyFlow: Building the PayFi Crypto Payment Network

TechFlow Selected TechFlow Selected

PolyFlow: Building the PayFi Crypto Payment Network

PolyFlow is integrating the transformative power brought by cryptocurrency and blockchain technology to build a new decentralized PayFi crypto payment network.

The Bitcoin white paper of 2008 painted a vision of a peer-to-peer electronic cash payment network that requires no trusted third party. Payments were among the earliest promises made by digital currencies and blockchain technology.

To this day, digital-age payment networks still run on outdated rails established two decades ago during the rise of the internet. When faced with emerging digital assets like cryptocurrencies, these legacy systems struggle to meet people’s growing desire for financial freedom and the global free flow of assets.

Blockchain's true potential lies in reshaping financial infrastructure. PolyFlow is harnessing the transformative power of cryptocurrency and blockchain technologies to build a new decentralized PayFi crypto payment network—accelerating the shift toward innovative financial paradigms and unlocking the true value of Web3. Ultimately, PolyFlow aims to turn the grand vision laid out in the Bitcoin white paper into reality.

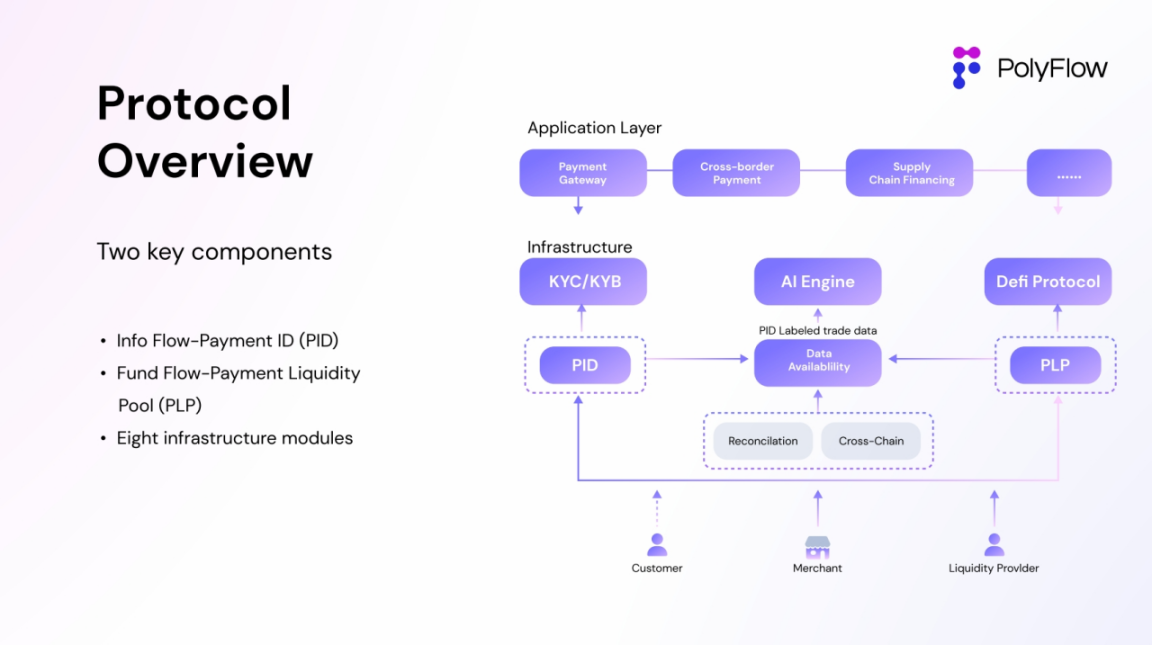

1. Introduction to PolyFlow

PolyFlow—the first decentralized PayFi infrastructure—bridges RWA and DeFi, aiming to further enable efficient and free circulation of value. As an infrastructure layer on the blockchain network, PolyFlow integrates traditional payments, crypto payments, and decentralized finance (DeFi), processing real-world payment scenarios in a decentralized manner to drive the establishment of new financial paradigms and industry standards.

Through modular design, PolyFlow supports the development and deployment of diverse PayFi applications while introducing composability and scalability from the DeFi ecosystem. Overall, it provides PayFi applications with a lightweight, regulatory-compliant architecture free from custody risks and compatible with the DeFi ecosystem, along with a secure and compliant framework for digital asset transfer, custody, and issuance.

PolyFlow introduces two key components—Payment ID (PID) and Payment Liquidity Pool (PLP)—to decouple the information flow from the fund flow within payment transactions:

• PID is linked to the information flow, serving as a powerful tool enabling identity verification and compliance onboarding, privacy protection and data sovereignty, AI-driven data processing, and X-to-earn functionalities;

• PLP is tied to the fund flow, managed by smart contracts that hold funds for payment transactions. It not only provides a secure and compliant framework for digital asset movement, custody, and issuance but also brings composability and scalability from the DeFi ecosystem.

On this foundation, AI can analyze rich streams of everyday payment data, returning data ownership to PID holders—data that was previously monopolized by fintech giants. The revenue generated through the protocol is reflected directly in the PLP, creating for the DeFi ecosystem a risk-free real-world asset (RWA) yield category rooted in actual payment activity.

Looking ahead, as PayFi infrastructure, PolyFlow will enable on-chain credit capabilities—empowering PayFi applications to offer consumer loans, buy-now-pay-later (BNPL), credit cards, and interest-bearing lending features for individual users’ daily spending, as well as corporate lending and supply chain financing for businesses—ultimately delivering the benefit of “Buy Now, Pay Never.” It must be understood that only by integrating with real-life use cases can PayFi truly evolve, marking a critical step toward mass adoption of crypto.

PolyFlow’s robust functionality enables the construction and deployment of various PayFi application scenarios, delivering innovative financial models and user experiences far beyond what traditional finance can offer. It also empowers exchanges, payment service providers, banks, supply chain financiers, and settlement networks to expand and enhance their operations in the digital asset era. Most importantly, it allows all participants in the network to share in the immense benefits of the PayFi crypto payment network, realizing the true value of Web3.0.

2. Current Challenges in Crypto Payments

In today’s crypto payment business models, whether payment solution providers or asset management services, most operate in a centralized fashion. These centralized entities lack transparency, are prone to counterparty risks leading to single points of failure, and suffer from trust issues due to centralized decision-making. These persistent problems complicate transactions and raise concerns among regulators:

• Centralized Custody: Institutions hold users' private keys, exposing user assets to significant custodial risk.

• Regulatory Black Holes: Opaque centralized institutions, combined with incomplete legal frameworks for crypto, pose major challenges for oversight.

• Fiat Settlement: Current crypto payment models remain transitional, requiring reintegration with traditional fiat settlement systems—greatly increasing costs and reducing efficiency.

• Limited Service Capabilities: Crypto payment services offered by single institutions are often narrow in scope, failing to meet diverse user needs.

• Incompatibility with DeFi: Centralized institutions cannot integrate with the DeFi ecosystem, hindering widespread PayFi adoption.

It is well known that these centralized institutions—including banks—have failed before, and they will fail again. Recall the 2008 global financial crisis and the more recent collapses of FTX and Silicon Valley Bank in 2023—these serve as stark market lessons. This is precisely the problem the Bitcoin white paper sought to solve.

Therefore, the crypto payment industry urgently needs an innovative financial infrastructure capable of eliminating centralized custody risks, meeting complex compliance requirements, and seamlessly integrating with the DeFi ecosystem. Likewise, decentralized finance (DeFi) requires a bridge to the real world—one that captures stable, risk-free yield sources and ultimately achieves mass adoption.

3. The PolyFlow PayFi Solution

The convergence of crypto payments and DeFi has given rise to PayFi—a field demanding entirely new infrastructure to support its deployment and address intricate compliance challenges. Since Lily Liu, President of the Solana Foundation, introduced the concept of PayFi at the Hong Kong Web3 Festival, PolyFlow has emerged as one of the pioneering protocols building foundational PayFi financial infrastructure.

PolyFlow’s core idea is to use modular design to decouple transaction information flows and fund flows—previously controlled by centralized institutions—and manage them in a decentralized way. This approach better aligns each stage of the transaction with regulatory compliance, reduces custody risk, and leverages blockchain’s inherent strengths to connect with the DeFi ecosystem, accelerating large-scale PayFi adoption.

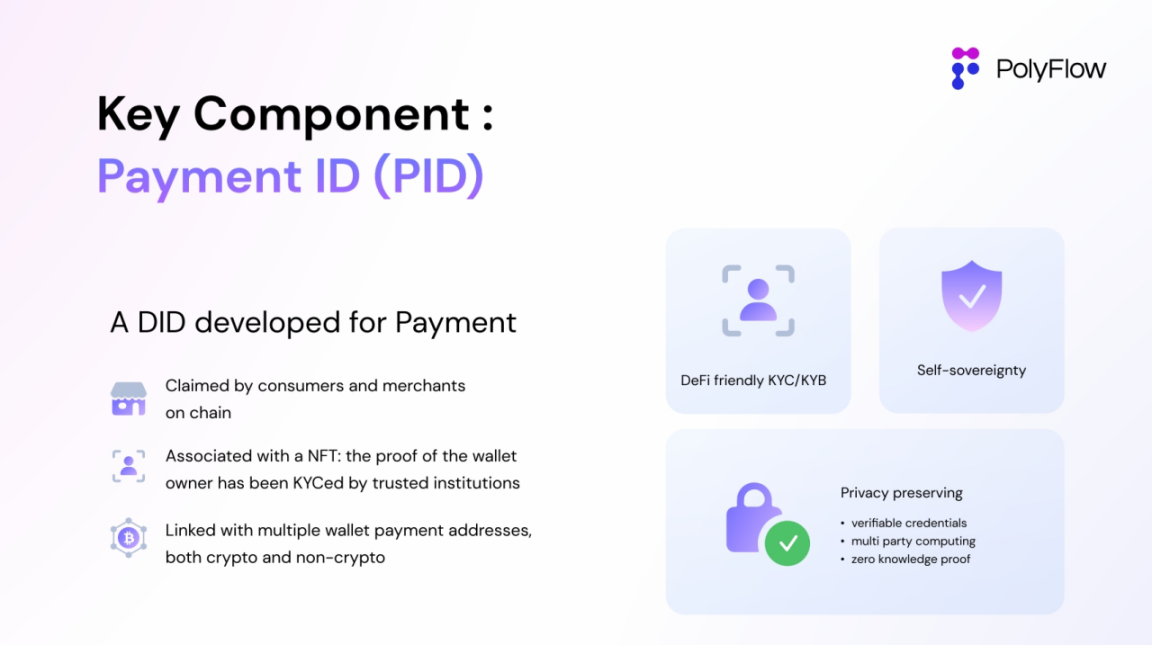

3.1 Payment ID (PID)

PID is a decentralized identifier bound to encrypted, privacy-preserving KYC/KYB attestation data, linking verifiable credentials from multiple platforms where a user has completed KYC/KYB processes. It enables:

• Compliance Onboarding: A PID can aggregate verification data across multiple platforms and be easily shared via QR code. This structured method of identification and transaction management simplifies validation for partners while remaining compatible with the DeFi ecosystem. More importantly, it breaks down the information silos created by centralized institutions, using PIDs to build an open, decentralized identity system that empowers both traditional finance and DeFi ecosystems.

• Privacy Protection: By leveraging zero-knowledge proofs and other advanced technologies, PID enables compliance with anti-money laundering (AML) and counter-terrorism financing (CTF) obligations without exposing sensitive user data. This is a prerequisite for user participation in traditional finance and DeFi.

• Data Sovereignty: As a product of splitting off the transaction information flow, PID ensures that transaction metadata can be reported to regulators to meet compliance needs, while simultaneously returning behavioral data on-chain back to individual users. Users may choose to contribute PID-tagged data to AI analysis in exchange for rewards or token incentives—contrasting sharply with the historical practice of centralized firms profiting from user data without consent. Furthermore, PID plays a pivotal role in establishing on-chain credit systems.

PolyFlow’s innovative introduction of PID delivers transformative advantages to the crypto payment industry—building a vital bridge between traditional finance and the DeFi ecosystem while offering users a flexible and reliable way to manage digital identities, engage in cross-platform transactions, and build on-chain credit.

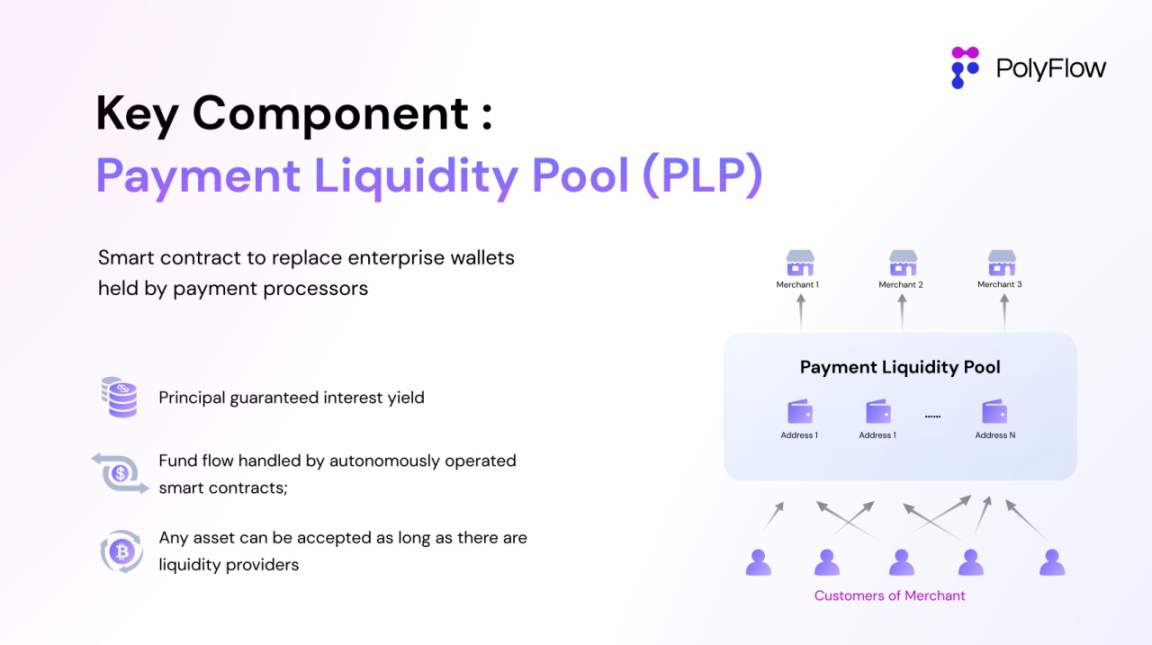

3.2 Payment Liquidity Pool (PLP)

PLP represents the separation of the fund flow in transactions. Its liquidity pool uses smart contract addresses to receive funds, enabling on-chain custody instead of relying on costly enterprise wallets operated by centralized institutions for asset management, fund aggregation, and yield generation. This more decentralized model offers:

• Self-Custody of Funds: Ensures asset security while minimizing reliance on intermediaries, providing public, transparent, and immutable ledgers, and offering PayFi applications a convenient, secure, and compliant custody solution.

• Liquidity Provision: Smart contract addresses aggregate transaction funds, supplying liquidity to meet financing demands in payment transactions.

• DeFi Ecosystem Compatibility: Centralized applications cannot natively integrate with the decentralized DeFi ecosystem. Being built on blockchain, PLP seamlessly connects with DeFi and brings DeFi’s operational logic to PayFi applications.

• Risk-Free RWA Yield Category: Revenue generated by the protocol is directly reflected in the PLP, offering DeFi a stable, risk-free yield stream derived from real-world payment activities.

This PLP architecture eliminates custodial risks associated with intermediaries and flexibly integrates with the DeFi ecosystem, ensuring PayFi applications remain adaptable in the evolving digital asset landscape.

4. Innovation Paving the Way

PolyFlow introduces several groundbreaking innovations:

4.1 Modular Crypto Payments: Decoupling Information Flow and Fund Flow

Traditionally, centralized institutions manage both information and fund flows simultaneously, drawing strict regulatory scrutiny due to fraud risks in the absence of third-party oversight, along with high custody risks. By decoupling these flows, centralized entities handle only information flow and KYC-related compliance, while assets are managed by on-chain protocols—resolving the centralized custody issue. This significantly reduces their compliance burden and facilitates smoother PayFi application development and deployment.

Additionally, AI analytics were previously limited to internal use by centralized firms analyzing their own proprietary data, restricting overall data utility. With decoupled information flows, the resulting data becomes accessible to multiple AI service providers, dramatically improving data utilization efficiency.

4.2 Breaking Down Information Silos and Enabling DeFi Integration

PID leverages DID (Decentralized Identifiers), Verifiable Credentials, and Zero-Knowledge Proofs to deliver privacy-preserving KYC information, aggregated wallet addresses, and AI tagging. It adheres to W3C standards and the Trust-Over-IP stack developed by the Linux Foundation.

PID breaks down the information silos erected by centralized institutions, connecting them into an open, decentralized identity system that empowers the entire traditional finance and DeFi ecosystem. Centralized players—such as centralized exchanges, payment service providers, and KYC vendors—can leverage PID to revitalize their existing infrastructure and build new PayFi use cases.

4.3 Bringing Real-World Asset Yields On-Chain

PLP functions as a risk-free DeFi yield product suitable for on-chain cash flow management. This marks a significant breakthrough, as previous DeFi yield models inherently carried risk—for example, yield products based on decentralized exchanges face impermanent loss, while collateral in lending protocols is vulnerable to extreme price volatility of underlying assets, both common occurrences in DeFi.

In contrast, PLP generates risk-free returns directly from transaction fees in real payment scenarios. For instance, in a payment gateway setup, consumers send payments to the smart contract address within the PLP. When merchants request early settlement, if the smart-contract-based PLP liquidity pool lacks sufficient funds, liquidity providers can step in to settle the transaction in return for payment yield.

Critically, this process is risk-free, with yields determined by the ratio between liquidity providers’ capital and total transaction volume. It can support attractive fixed- or variable-term financial products and enable innovative PayFi applications such as supply chain finance, wallet settlement networks, stablecoins, and insurance.

5. Strong Team Driving Rapid Growth

These innovations did not emerge overnight. They are backed by over two decades of mature operational experience in traditional finance and cross-border payments, coupled with deep expertise in cryptocurrency and blockchain technology.

PolyFlow is the product of an exceptional team whose members come from major cross-border payment firms that provide services to Apple, Amazon, and TikTok; from international standard-setting bodies such as W3C, Linux Foundation, and IEEE; and from investment banks in New York, Hong Kong, Singapore, Dubai, and London—bringing extensive industry knowledge and hands-on experience. Additionally, PolyFlow maintains channel partnerships with bank payment networks across developed nations as well as Latin America, APAC, and Africa, wealth management firms handling over $100 billion in liquid and illiquid assets, and global cross-border commodity trading companies.

PolyFlow’s growth has been accelerated by early investors. Beyond the team’s own accumulated resources from over 20 years in cross-border financial payments, early funding exceeding $5 million was provided by CE Innovation Capital, Hash Global, Stellar Foundation and Community Fund, ZC Capital, and Meters Network. PolyFlow also maintains close collaborations and sponsorship relationships with established Web3 infrastructures such as Solana, Stellar, and Ripple, jointly supporting and building new infrastructure for PayFi and the future of the Web3.0 economy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News