IOSG: We remain cautious about the recent defensive investment trends in the GameFi market.

TechFlow Selected TechFlow Selected

IOSG: We remain cautious about the recent defensive investment trends in the GameFi market.

This article will carefully examine the defensive investment logic behind such investment phenomena, as well as our perspective on this investment rationale.

Author: IOSG Ventures

Looking back from mid-2023 to today, GameFi-related projects (including what is now often categorized as GambleFi) that have secured substantial funding or shown remarkable performance are primarily concentrated in infrastructure such as gaming platforms and Game Layer 3s. The most eye-catching phenomena have been the explosive popularity of pump.fun’s gambling-style frenzy since the beginning of the year, along with viral clicker games like Not and Telegram-based mini-games. This article will dissect the defensive investment logic behind these trends and our perspective on this investment rationale.

1. Overview of GameFi Market Funding

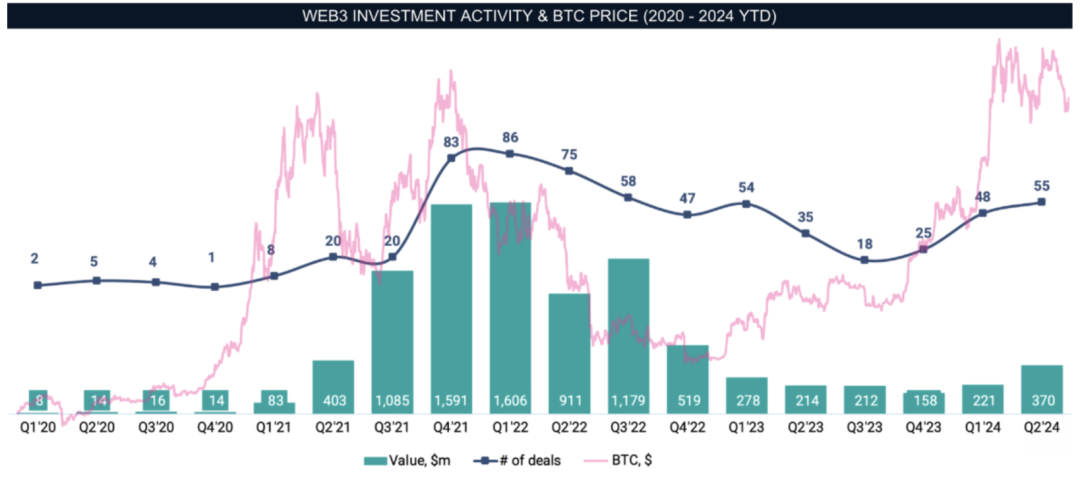

Source: InvestGame Weekly News Digest#35: Web3 Gaming Investments in 2020–2024

Reviewing quarterly investment volume and number of projects in the GameFi space from 2020 to 2024, despite Bitcoin surpassing its 2021 all-time high this year, data over the past year shows relatively weak and conservative activity both in total capital deployed and project count. Compared to Q4 2021—the previous peak period—when there were 83 funded projects totaling $1.591 billion, averaging $19.2 million per project, Q1 2024 saw only 48 projects raise $221 million collectively, averaging just $4.6 million per project—a 76% decline year-on-year. In absolute terms, overall investment behavior reflects a cautious, defensive posture.

2. Analyzing Three Key Market Phenomena Over the Past Year: Underlying Logic, Shifts, and Questions

2.1 Phenomenon One: Gaming Platforms Evolving from Pure Infrastructure into User Acquisition Channels

"Beyond their strong survivability and long life cycles, game infrastructures are increasingly being valued for their role as user acquisition channels—this evolution explains their appeal to VCs."

Among the 34 GameFi-related projects that raised over $10 million between June 2023 and August 2024, nine were gaming platforms and four were game-focused L3s. From BSC to Solana, Base to Polygon—even custom-built Layer 2s and Layer 3s—gaming platforms have proliferated. Even amid a significant drop in total funding volume, 38% of high-value investments still went toward robust, long-lifecycle infrastructure projects. These platforms represent narratives immune to fleeting trends and offer low-risk, defensive bets to remain active in the market.

Source: Pantera

Beyond early-stage funding, major funds like Pantera have also heavily backed top-tier gaming ecosystems such as Ton's ecosystem token, while Ronin remains a preferred secondary-market bet among multiple VCs. The reason for VC enthusiasm toward ecosystems like Ton and Ronin may lie in the evolving function of these platforms. With nearly one billion users on Telegram, lightweight games like Not, Catizen, and Hamster have drawn millions of new users into Web3 (Not: 30M users; Catizen: 20M users, 1M paying; Hamster: 300M users). Additionally, traffic generated within Ton’s ecosystem has translated into inflows of new users onto exchanges after token listings. Since March, Ton has announced over $100 million in ecosystem incentives and multi-phase tournament prize pools. However, chain data suggests Ton’s TVL hasn’t grown significantly alongside the mini-game boom. Most users appear to be directly converted into exchange accounts through pre-funded campaigns. On Telegram, CPC (cost-per-click) can be as low as $0.015, compared to an average cost of $5–$10 to acquire a new account on an exchange—and over $200 per paying user, averaging $350. User acquisition and conversion costs on Ton are far lower than those incurred by exchanges themselves. This helps explain why exchanges are rushing to list various Ton-based mini-game tokens and memecoins.

Ronin’s established user base similarly offers significant user acquisition opportunities for individual games. The migration of quality titles such as Lumiterra and Tatsumeeko onto the Ronin chain underscores how incremental user growth and acquisition capabilities have become key criteria in platform selection. Thus, the ability of gaming platforms to drive user growth appears to have emerged as a new dimension of investor interest.

2.2 Phenomenon Two: Short-Term Projects Dominate Market Favor—but Long-Term Retention Remains Questionable

"In a low-liquidity secondary market, many games’ flywheel mechanics and profit loops are effectively severed. Perpetual gameplay devolves into one-off speculation. While short-term projects align with VCs’ risk-averse, defensive strategies in poor macro conditions, whether they can deliver sustainable user retention commensurate with investor expectations remains uncertain."

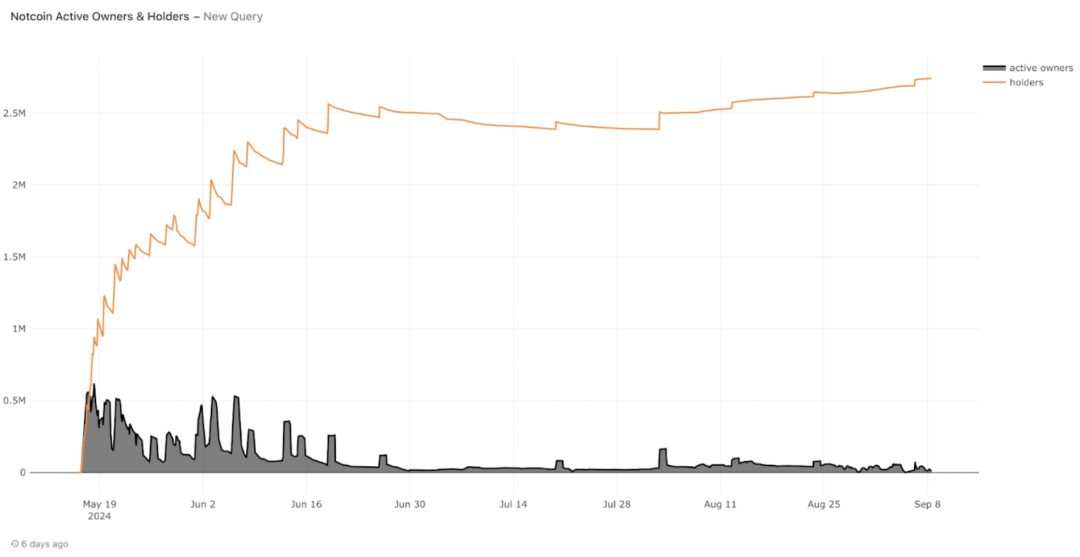

Analyzing Not (a short-term project)'s Economic Model

Source: Pantera

Active users of Not declined sharply after token launch—dropping from 500K at TGE to 200K five days later, eventually stabilizing around 30K. A 94% drop in user base clearly marks Not as a quintessential short-term project. Yet recently listed projects like Dogs, Hamster Kombat, and Catizen—all fully unlocked, short-duration initiatives—have gained strong traction among both markets and VCs. Why?

Source: Starli

From earlier P2E models involving gameplay-for-profit, simple level designs, auto-battlers, pixel farming in games like Pixel, to Not’s “click-to-earn” mechanic, projects under the GameFi label are progressively simplifying—or outright discarding—the “game” layer. When the market enthusiastically embraces these formats, is it due to greater acceptance, or growing impatience and superficiality? If most GameFi is essentially mining via interactive actions instead of running node hardware, why maintain complex game development steps and modeling costs? Why not redirect all those development resources into the initial reward pool of this Ponzi-like mine, creating mutual benefit?

Not’s economic model diverges fundamentally from traditional GameFi flywheels. With full token unlocks upon listing and no upfront investment required, users can exit immediately after claiming airdrops. VCs no longer face the burden of multi-year vesting schedules. Instead of sustained play-to-earn economies, these projects resemble short-lived, fully circulating memecoins. Similar to platform-driven user acquisition, simple monetization mechanics attract Web2 users into Web3, who claim airdrops and cash out via exchanges—bringing valuable traffic to both ecosystems and trading platforms. This flow likely contributes to VC favorability toward such models.

The Essence of Flywheel Dynamics and Why Short-Term Models Fit Current Markets—But Mid-to-Late Stage Returns Are Uncertain

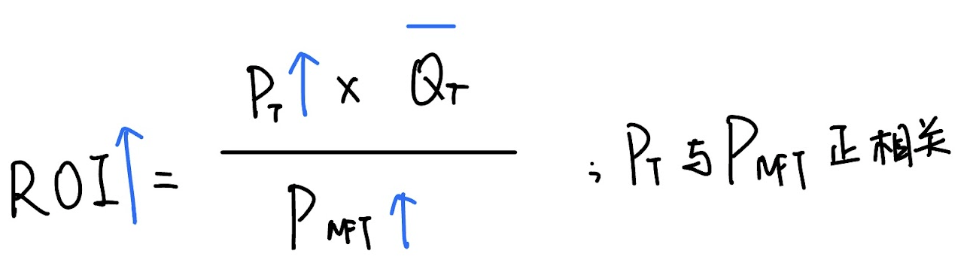

Traditional P2E games relied on self-sustaining economic flywheels. Whether such a loop could spin depended on players calculating an acceptable ROI (Return on Investment):

ROI = Value of Future Rewards / NFT Acquisition Cost

(Where future rewards refer to mined token value, and NFT cost acts as "miner" hardware expense.)

The higher the calculated ROI, the stronger the incentive for participation. How can ROI be maximized? Let's break it down:

Source: Starli, IOSG Ventures

-

Path 1: Increase Value of Future Rewards

Value of Future Rewards = Quantity × Price

V = P × Q

This means increasing either the amount of tokens earned or their market price.

In Web3 economies, token emissions typically follow a decaying curve—similar to Bitcoin halvings—where supply decreases and mining difficulty increases over time. Higher-tier NFTs ("better miners") might yield more rewards, but at increased cost. So without upgrading NFT quality, increasing reward quantity doesn't make sense.

Therefore, the more viable path is increasing the *price* of future rewards—i.e., ensuring the mined token steadily appreciates. This requires strong buy-side pressure in secondary markets, where demand absorbs all selling pressure and drives prices upward—thus increasing the numerator in ROI.

-

Path 2: Reduce NFT Acquisition Cost

Lower denominator → higher ROI. That is, cheaper NFT entry costs ("miner" hardware).

If NFT prices denominated in project tokens fall, it’s either due to reduced demand or oversupply, or depreciation of the underlying token used as medium of exchange. Reduced demand stems from weaker earning potential, prompting players to seek better ROI elsewhere. If priced in ETH, SOL, etc., general crypto market downturns would depress prices across the board. Hence, NFT and token prices tend to move in tandem—meaning numerator and denominator changes are correlated, even mutually reinforcing.

Thus, the only realistic way to increase ROI is when future token prices rise, with NFT prices rising proportionally but less than or equal to token appreciation—keeping ROI stable or slowly growing, sustaining player incentives. In this scenario, incoming speculative capital acts as an amplifier. Only during bull markets—when token prices rise—can P2E flywheels actually spin. When ROI holds steady or grows slightly, players reinvest profits, compounding gains—injection exceeds withdrawal. Axie Infinity was the most successful example of this flywheel effect.

Source: Starli, IOSG Ventures

Source: Starli, IOSG Ventures

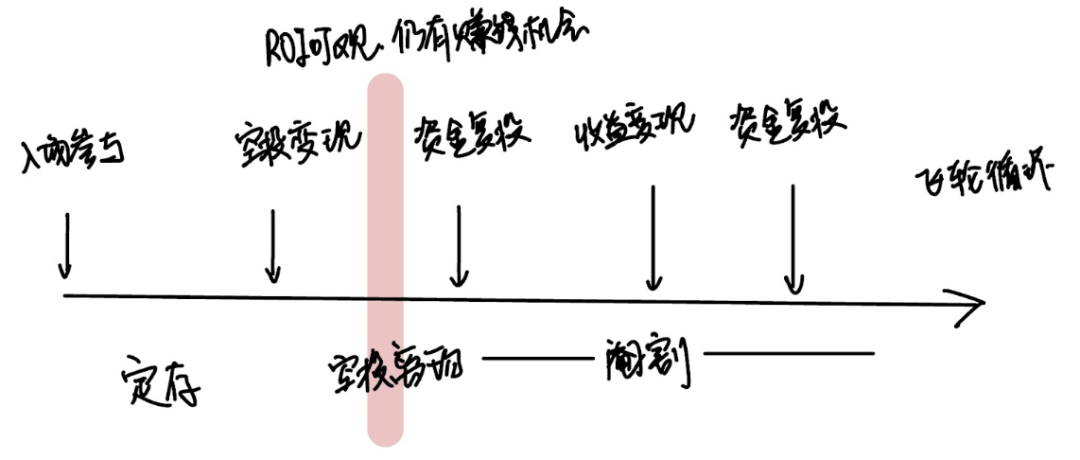

Contrast this with current-cycle games: most experience brief FOMO pre-launch, then crash overnight post-FG. All unlocked tokens turn into instant sell pressure. Players cash out and chase the next opportunity. No ongoing ROI, no reinvestment, no flywheel. Diamond-handed holders bear the entire short-term burden. We hear less about P2E now—P2A (Play-to-Airdrop) has quietly taken over. This is a dangerous concept, branding games as disposable. Farming airdrops becomes purely about dumping them upon listing—not seeking sustained earning opportunities within the ecosystem. Despite similar end behaviors (selling), today’s weak secondary markets—with stagnant altcoins and absent market makers—have forcibly crippled many games’ earning dynamics. Loops collapse into one-offs; perpetual play becomes speculative exits.

Catizen and Hamster’s post-TGE performances confirm they were built on short-term economic models—no need to sustain flywheels or support price pumps. For such projects, mid-to-late stage token funding remains questionable as a return-generating investment.

Flywheel mechanics require refined design and upfront investment. Short-term models only need airdrop expectations—because once listing happens, the mission is complete. Post-listing economics can be entirely discarded. Airdrop expectation, in essence, profits from liquidity spreads between private and public markets. These short-term projects can be seen as fixed deposits: users invest NFT/pass costs and attention as principal, endure time-based illiquidity, then exit with airdrop returns upon listing.

Such projects avoid cross-cycle operational demands and uncertain economic loops. They aren’t fully dependent on market sentiment or FOMO. Their brief, brilliant lifecycles and fully unlocked tokens eliminate VC vesting concerns and enable faster exits. In unfavorable macro environments, these short-term ventures represent classic risk-averse, defensive bets for VCs.

Long-Term User Retention Remains Doubtful

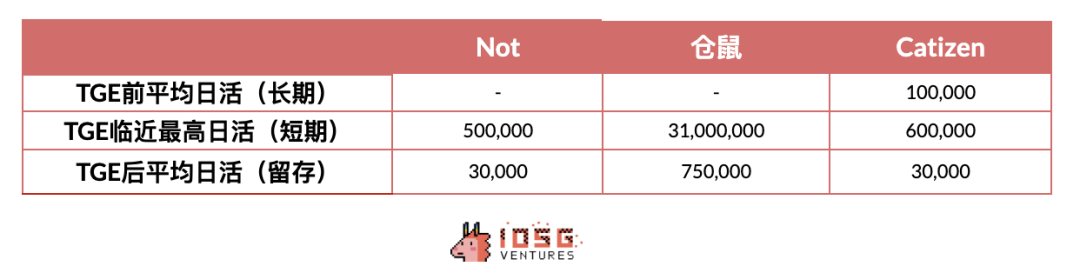

Projects like Not, Catizen, Hamster, and Dogs have driven significant user growth for exchanges like Binance. But how many of these users stay long-term in the ecosystem or on the exchange? Do the retained users justify VC valuations and expectations?

Source: IOSG Ventures

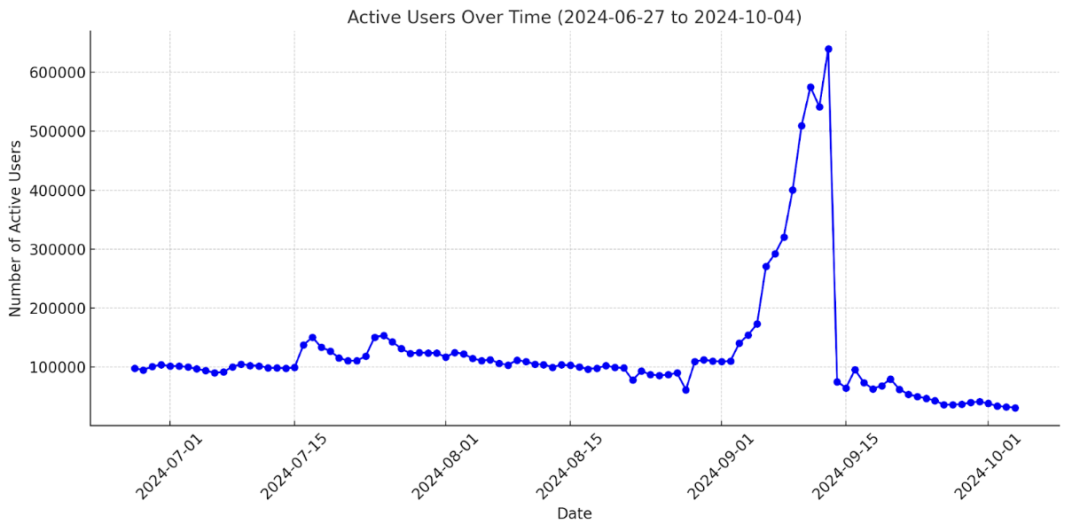

Take Catizen—one of Ton’s hottest mini-games. Active users dropped from 640K pre-token launch to just 70K in one day, with further declines afterward. Even assuming unchanged game content, over 90% of users left immediately once airdrop expectations faded. Only about 30K remained long-term. Does this retention rate meet investor expectations or fulfill acquisition goals? Even if airdrop recipients temporarily boost exchange traffic, will they abandon the exchange just as they abandoned Catizen? When products become viral marketing campaigns designed solely for user acquisition, even if they generate short-term spikes, do the truly retained users satisfy ecosystem or exchange ambitions? Justify the capital invested? We remain skeptical.

2.3 Phenomenon Three: Top-Tier VCs Betting on Casinos for Revenue Share—but Lacking Token Launch Potential and Value Capture

"Infrastructure and secondary trading are tightly tied to macro trends. During strong bull runs, capital prefers staying in-market to ride momentum. But when secondary markets lack strong buying interest, earning revenue share or ‘vig’ from casinos and PvP platforms like pump.fun becomes a safer, more conservative defensive strategy for VCs. Still, questions remain: Where do users come from? And without token issuance prospects, can these platforms truly capture value compared to GameFi investments?"

A growing number of casino projects have emerged, accounting for 15% of high-value GameFi funding in 2024. In today’s fast-paced crypto world, if memes and pump.fun are widely accepted, why should gambling games still hide behind a thin GameFi facade? Now, they stand openly before us.

On February 12, Monkey Tilt—a hybrid sports betting site and online casino—secured funding led by Polychain Capital, with participation from Hack VC and Folius Ventures. On March 24, Myprize announced a $13 million round led by Dragonfly Capital and joined by a16z, going even further: its homepage features live dealers and suggestive imagery.

Source: Myprize

The Revenue Model of Pump.fun and Casino Platforms: Earning Vig and Cash Flow

During periods of market stagnation—amid unresolved elections and delayed U.S. rate cuts—investor fatigue builds. Add to this the dual stimulus of mythical tokens like BOME (Book of MEME) and hundred- or thousand-fold gainers, and speculative appetite surges. More capital flows on-chain and into platforms like pump.fun, chasing the next “golden dog.” Note that pump.fun emerged precisely during Solana’s prolonged consolidation phase after its initial rally.

What is the biggest casino in Web3? Many already know the answer: perpetual futures contracts on top-tier exchanges like Binance and OKX, offering up to 125x leverage, or smaller exchanges with 200x or even 300x. Compare this to traditional stock markets—A-shares capped at ±10% daily moves, ChiNext at ±20%. Tokens, already operating under T+0 with no price limits, combined with 100x leverage, mean less than 1% price movement can wipe out your entire position.

Whether betting on price rises or falls, ultra-short-term contracts are essentially wagers on directional movement over brief intervals, with odds set from 5x to 300x. Exchanges profit handsomely from trading fees, funding rates, and forced liquidations. Similarly, casinos earn via rake or house edge.

While infrastructure and secondary trading thrive in clear bull markets—where capital stays in to capture broad gains—at times of uncertainty, money shifts toward casinos and PvP speculation, using high leverage to chase outsized returns unattainable otherwise. High leverage magnifies both gains and losses. Amid volatile, range-bound markets, revenue from fees and vig may actually exceed that of trending bull phases.

With increased user speculation, capital and attention flow into gambling and PvP arenas. Revenue from casinos and tooling becomes a stable, demand-driven income stream—fitting the defensive investment thesis. Yet challenges persist.

Lack of Token Issuance Expectations and Value Capture

Platform projects like pump.fun may achieve phenomenal scale and transaction volume, yet lack any token issuance roadmap. From a tokenomics standpoint—utility, necessity within the ecosystem—or regulatory angle, avoiding token launches sidesteps SEC scrutiny over securities violations. Most such platforms therefore lack credible token issuance prospects.

Moreover, without token incentives, fee-based revenue models work best during sideways, choppy markets but cannot anticipate or create new trends. These platforms serve as tools fulfilling existing demand rather than generating demand themselves—lacking intrinsic value capture mechanisms.

Pump.fun’s recent large-scale sale of SOL illustrates this (as of September 29, ~$60 million worth of SOL sold—about half its total revenue). While leveraging $SOL’s ecosystem strength, it simultaneously exerts downward pressure on the market. Though pump.fun brings undeniable benefits to Solana—boosted trading activity, new users attracted by meme summer, steady $SOL demand, follow-on buying from price-chasing investors, and some meme traders evolving into long-term $SOL holders and ecosystem supporters—its impact isn’t purely positive.

It takes from the community and sells back to it—collecting $SOL as fees, then dumping them. As sales approach total revenue, pump.fun’s net effect on $SOL price becomes neutral, even potentially negative (only sell-side, no buy-side). During growth phases, its positive impact may compound geometrically. But once mature and plateaued, constant fee-driven sell pressure minus diminishing positive effects could result in net negative influence.

In sum, gambling platforms are likely to underperform truly value-capturing GameFi projects. Furthermore, most VC returns depend on revenue sharing. Without equity exit paths or token issuance logic, VCs must rely on acquisitions or mergers for exit—entailing long, uncertain timelines.

3. Conclusion: Casinos and Platforms May Underperform GameFi; Short-Term Projects Show Poor Retention—Cautious Stance on Past Defensive Bets

Whether drawing existing users to new games or converting mass audiences into new Web3 participants, gaming platforms have evolved into powerful user acquisition channels. However, for projects relying on short-term engagement atop such platforms, long-term user retention remains unproven by data and time. Gambling platforms, lacking token issuance and true value capture, are likely to lag behind GameFi projects with solid product-market fit and sustainable economics during bull markets. We maintain a cautious view toward past defensive investment patterns and remain eager to discover under-the-radar, underfunded products and high-quality games. Such games, driven by superior quality, can convert user interest into higher retention, increased in-game spending, and greater on-chain activity—ultimately translating into stronger token value.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News