Japan's Stablecoin Market Landscape: Regulation First, Growth Awaits

TechFlow Selected TechFlow Selected

Japan's Stablecoin Market Landscape: Regulation First, Growth Awaits

Despite the regulatory framework for stablecoins having been in place for over a year, the Japanese yen's share of the stablecoin market remains small.

Author: Tiger Research Reports

Translation: TechFlow

Key Takeaways:

-

Japan has one of the most advanced stablecoin regulatory frameworks among major countries, thanks to government-led growth initiatives and favorable Web3 policies.

-

However, Japan's stablecoin use cases remain limited. No stablecoin business has yet obtained EPISP registration, and no stablecoins are listed on local exchanges, restricting their retail adoption.

-

Nonetheless, the existence of a clear regulatory framework is significant as it provides greater certainty for businesses. We can expect major Japanese banks and corporations (such as Sony) to enter the stablecoin market.

1. Introduction

Japan’s stablecoin market has stabilized, primarily due to the establishment of a clear regulatory framework. This growth has also been supported by government initiatives and policies from the ruling Liberal Democratic Party aimed at accelerating the Web3 industry. Japan’s proactive openness contrasts sharply with the uncertain or restrictive stances many other countries have taken toward stablecoins. As a result, there is strong optimism about the future of Japan’s Web3 market. This report examines Japan’s stablecoin regulation and explores the potential impact of yen-backed stablecoins.

2. Japan's Stablecoin Market Poised for Rapid Growth Due to Regulatory Progress

In June 2022, Japan prepared amendments to the Payment Services Act (PSA) to establish a regulatory framework for stablecoin issuance and brokerage. These revisions took effect in June 2023. This marked the official start of stablecoin issuance. The revised law provides a detailed definition of stablecoins, specifies eligible issuing entities, and outlines the licenses required for conducting stablecoin transactions.

2.1. Definition of Stablecoins

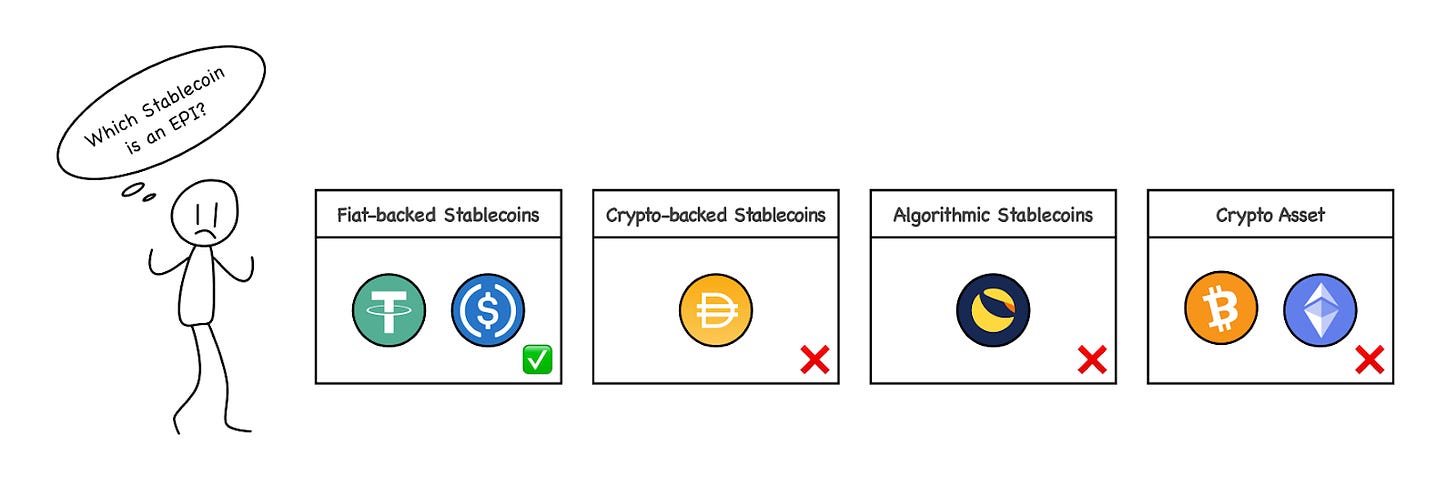

Under Japan’s amended Payment Services Act (PSA), stablecoins are classified as “Electronic Payment Instruments” (EPI), meaning they can be used to pay for goods or services to unspecified multiple recipients.

Source: Tiger Research

However, not all stablecoins qualify under this classification. According to Article 2, Paragraph 5, Item 1 of the amended PSA, only stablecoins whose value is pegged to legal tender are recognized as Electronic Payment Instruments. This means crypto-collateralized stablecoins (such as Bitcoin or Ethereum-backed tokens like MakerDAO’s DAI) are not classified as EPIs under this law. This distinction is a key feature of Japan’s regulatory framework.

2.2. Eligible Stablecoin Issuers

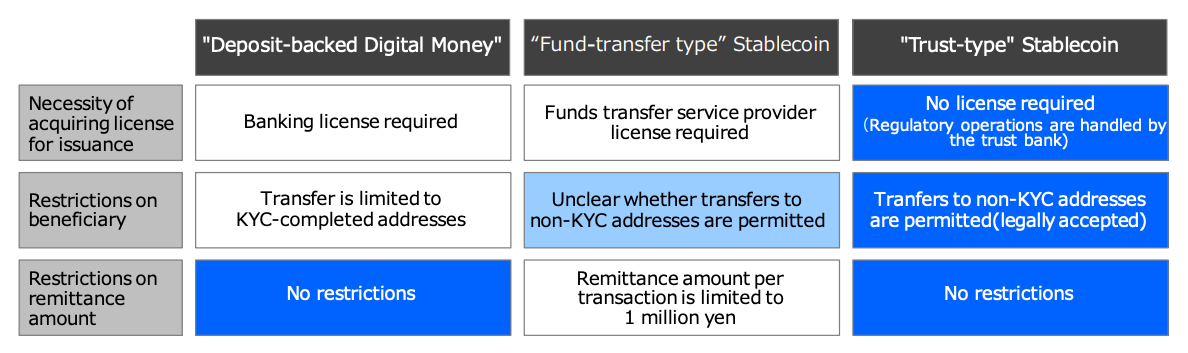

Japan’s amended Payment Services Act (PSA) specifies which entities are permitted to issue stablecoins. Only three types of entities may issue stablecoins: 1) banks, 2) money transfer service providers, and 3) trust companies. Each type can issue stablecoins with different characteristics—for example, differing in maximum transaction amounts or recipient restrictions.

Source: MUFG

Among these issuers, trust company-issued trust-type stablecoins are particularly notable. They are expected to align best with Japan’s current regulatory environment and closely resemble widely-used stablecoins such as USDT and USDC in functionality.

Japanese regulators have indicated that bank-issued stablecoins will face certain restrictions. Banks operate under strict oversight aimed at maintaining financial system stability, and permissionless-based stablecoins may conflict with this responsibility due to their uncontrollable nature. Therefore, regulators emphasize that bank-issued stablecoins require careful consideration and may necessitate further legislation.

Money transfer service providers also face limitations. Each transaction is capped at 1 million JPY, and it remains unclear whether transfers to non-KYC-verified recipients are permitted. As a result, additional regulatory updates may be needed before money transfer providers can issue stablecoins. Given these constraints, the most likely form of stablecoin to emerge in Japan will be those issued by trust companies.

2.3. Licenses for Stablecoin-Related Businesses

In Japan, entities engaging in stablecoin-related activities must register as Electronic Payment Instrument Service Providers (EPISP) to obtain a stablecoin license. This requirement was introduced under the June 2023 amendments to the Payment Services Act (PSA). Stablecoin-related activities include buying, selling, exchanging, brokering, or representing stablecoins. For example, virtual asset exchanges listing and supporting stablecoin trading, or custodial wallet services managing stablecoins on behalf of users, must also register. In addition to registration, these businesses must comply with user protection and anti-money laundering (AML) obligations.

3. Yen-Backed Stablecoins

With Japan establishing a robust stablecoin regulatory framework, various projects are actively researching and experimenting with yen-backed stablecoins. In the following sections, we examine key Japanese stablecoin initiatives to better understand the current state and characteristics of the yen-based stablecoin ecosystem.

3.1. JPYC: Prepaid Payment Instrument

Source: JPYC

JPYC is Japan’s first digital asset issuer linked to the yen, established in January 2021. However, the current “JPYC” token is classified as a prepaid payment instrument rather than an Electronic Payment Instrument under the amended Payment Services Act (PSA), meaning it is not legally recognized as a stablecoin. As such, JPYC functions more like a prepaid voucher, with restricted usage. Specifically, while fiat currency can be converted into JPYC (top-up), converting JPYC back into fiat (withdrawal) is not allowed, limiting its utility.

Notably, JPYC is actively working to issue a stablecoin compliant with the amended PSA. First, it plans to issue a stablecoin by obtaining a money transfer license. Its goal is to expand usability through interoperability with Tochika, a deposit-backed digital currency issued by Hokkoku Bank. Acquiring a money transfer license would enable JPYC to legally conduct fund transfers, enhancing its market competitiveness.

JPYC is also preparing to register as an Electronic Payment Instrument Service Provider (EPISP) to operate stablecoin services. In the long term, the company aims to issue and operate a trust-type stablecoin based on Progmat’s Progmat Coin, enabling support for various commercial activities involving cash or bank deposits. Additionally, integration with Circle’s USDC infrastructure is expected to significantly benefit JPYC’s expansion, especially in cross-border payments.

3.2. Tochika: Deposit-Backed Digital Currency

Source: Hokkoku Bank

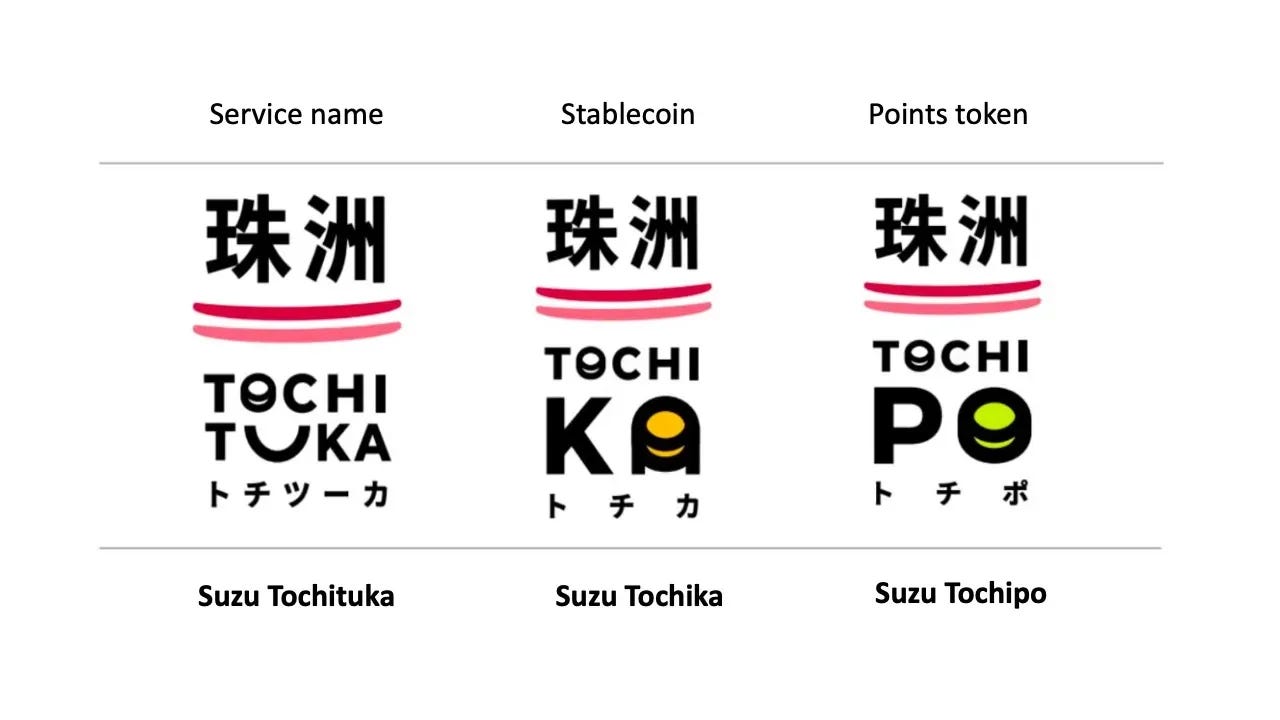

Tochika is Japan’s first deposit-backed digital currency. It was launched in 2024 by Hokkoku Bank, a regional bank located in Ishikawa Prefecture. Backed by bank deposits, Tochika offers digital tokens to account holders as part of a deposit service, enabling easier transaction and fund management.

Users can easily access Tochika via the Tochituka app, jointly developed by Hokkoku Bank and Suzu City. The process is simple: users link their bank accounts within the app, top up their Tochituka balance, and then use it as a payment method at participating merchants across Ishikawa Prefecture. Once topped up, users can conveniently spend and pay.

Tochika stands out for its simplicity and attractive 0.5% commission rate offered to merchants. However, it has limitations. Currently, it is only available within Ishikawa Prefecture, allows only one free withdrawal per month—after which a fee of 110 Tochika (equivalent to 110 JPY) applies—and operates on a private, permissioned blockchain developed by Digital Platformer, restricting its use within a closed ecosystem.

Looking ahead, Tochika plans to enhance and expand its services, including linking with deposit accounts from other financial institutions, expanding geographical coverage, and introducing peer-to-peer remittance features. Despite current limitations, Tochika sets a strong precedent for deposit-backed digital currencies. With ongoing development efforts, Tochika’s future potential is undoubtedly worth watching.

3.3. GYEN: Offshore Stablecoin

Source: GMO Trust

GYEN is a yen-denominated stablecoin issued by GMO Trust, a subsidiary of Japan’s GMO Internet Group based in New York. Regulated by the New York State Department of Financial Services and included in the Greenlist—which authorizes certain cryptocurrencies for issuance in New York—GYEN is the only yen-based stablecoin traded physically on cryptocurrency exchanges and is currently available on Coinbase.

Issued at a 1:1 ratio pegged to the Japanese yen, GYEN is classified as a trust-type stablecoin. However, because GYEN is not issued by a trust company within Japan’s regulatory framework, it cannot be distributed within Japan or to Japanese residents, limiting its domestic use. Nonetheless, Japanese regulators are discussing specific requirements and compliance measures for GYEN, as well as for stablecoins like USDC and USDT. Notably, GYEN may eventually be incorporated into Japan’s regulatory system.

4. Is a Viable Stablecoin Business Possible?

Despite over a year having passed since stablecoin legalization, progress across Japan’s stablecoin projects remains limited. Permissionless stablecoins like USDT or USDC remain scarce in the Japanese market. No company has yet completed the EPISP registration required to operate a stablecoin business.

Additionally, regulatory rules requiring stablecoin issuers to hold all reserves as demand deposits pose significant operational constraints. Demand deposits are typically unprofitable because they can be withdrawn at any time and offer minimal returns. Although the Bank of Japan recently raised interest rates from 0%, short-term rates remain low at 0.25%, still below levels in many other countries. This low yield could undermine the profitability of stablecoin operations. Consequently, demand is growing for more competitive stablecoins backed by other assets, such as Japanese government bonds.

Source: (Left) Circle & Soneium, (Right) DMM Crypto & Progmat

Nevertheless, industry expectations for the future remain high, as major Japanese financial institutions and corporate groups are actively engaging in stablecoin initiatives. These include the three megabanks—Mitsubishi UFJ Bank (MUFG), Mizuho Bank, and Sumitomo Mitsui Banking Corporation (SMBC)—as well as corporations like Sony and DMM Group.

Amid these expectations, calls for regulators to reevaluate their policies are growing louder. While the legal framework has been in place for some time, the lack of tangible outcomes may increase questions and concerns about its effectiveness. Under these circumstances, observing how Japan’s stablecoin market evolves will be particularly interesting.

5. Conclusion

Source: Financial Times, Refinitiv

In recent years, Japan has been grappling with the challenge of yen depreciation and has implemented various strategies to strengthen its currency’s competitiveness. Stablecoins are part of this broader effort to enhance the yen’s scalability and global standing. The adoption of advanced stablecoins is expected to pave the way for a range of global use cases beyond domestic applications, including cross-border payments. This could enable Japan to expand its influence in global financial markets.

Source: rwa.xyz

However, despite the stablecoin regulatory framework being in place for over a year, the yen’s share in the stablecoin market remains small. Stablecoin implementations are still rare, and no company has registered as an EPISP for stablecoin operations. Declining approval ratings for the Kishida administration and the Liberal Democratic Party also make it difficult to push forward strong Web3-related policies. Nevertheless, establishing the regulatory framework is an important step forward. While progress may be slow, the changes it brings are worth anticipating.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News