Is MicroStrategy's model a scam?

TechFlow Selected TechFlow Selected

Is MicroStrategy's model a scam?

Over 80% of people believe this is a scam...

Author: Crypto_Painter

Little-known fact: During the 2000 internet crisis, Michael Saylor's MicroStrategy was among the companies that suffered the most severe market cap contraction and losses. His personal wealth also experienced a massive drawdown during that bubble burst.

Today, MicroStrategy’s core business is an online AI and data analytics product, with a website interface still resembling that of a traditional internet-to-business (ToB) enterprise.

Aside from its substantial BTC holdings, in my view, there is almost nothing in terms of products or technology to justify MicroStrategy’s current market capitalization of over $20 billion...

Thus, we can roughly understand MicroStrategy’s stock as a corporate “ETF” tied to BTC prices.

Even so, if we calculate the value of its BTC holdings at the current price of $63,000, their total worth amounts to only $15.89 billion—yet the company’s stock market cap exceeds $20 billion.

Moreover, MicroStrategy reportedly still employs around 2,000 people. I wonder, if the company’s value stems entirely from BTC, where does it fund these employee expenses? After all, MicroStrategy’s core operations appear to be unprofitable.

This leads us to a scheme once widely discussed online—the so-called “new type of Ponzi scheme,” known as the “inverse Ponzi scheme.”

Traditional Ponzi schemes rely on inflows from new investors to pay returns to earlier participants, forming a pyramid-like structure.

In contrast, the “inverse Ponzi scheme” involves being both the new and old participant simultaneously—raising external investments or loans to inflate the overall valuation of the capital pool. It resembles a “bootstrapping” method, metaphorically “pulling oneself up by one’s bootstraps,” creating an internal loop that spirals upward.

Now, does MicroStrategy’s behavior fit this model?

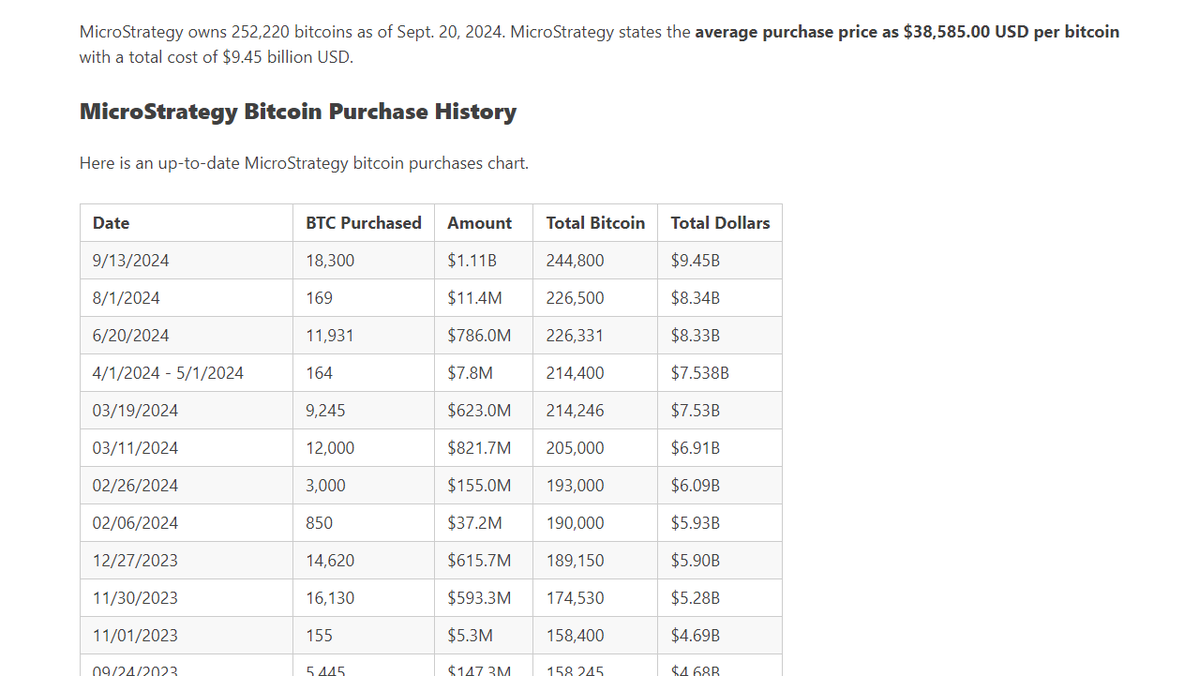

Since 2020, MicroStrategy has been continuously purchasing BTC, with its most recent purchase occurring on September 13. It currently holds 252,220 BTC at an average cost of approximately $38,585 per coin.

The funds for these BTC purchases do not come from company reserves but are raised from the market through instruments such as convertible bonds. Lenders receive MicroStrategy shares at a fixed or negotiated price in exchange.

In simple terms, MicroStrategy sells its own stock, uses the proceeds to buy BTC. Because of these BTC acquisitions, the company’s stock price has become increasingly correlated with BTC since 2020, especially over the past six months, nearly mirroring BTC’s price movements exactly.

From the investor or lender’s perspective, this is effectively equivalent to owning BTC directly. The only risk appears to be BTC’s price volatility—and the entire process is completely legal.

But is that really the case?

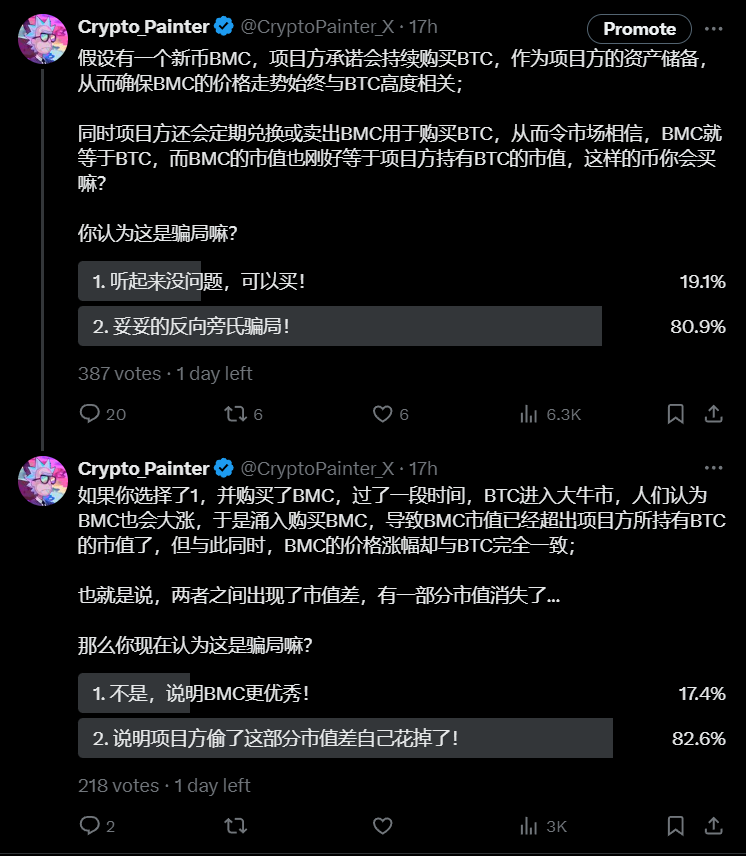

Yesterday, I conducted a poll using an analogy. The results were as follows:

Over 80% of respondents believed this is a scam...

This has led me to ponder: how might this practice of loading massive BTC onto a corporate balance sheet ultimately end?

First issue: The loophole between capital inflow and asset valuation.

Suppose MicroStrategy raises $2 billion from the market to buy BTC. After the purchase, both the company’s stock and BTC prices rise. In effect, MicroStrategy gains double leverage: while holding either BTC or MicroStrategy stock alone would yield a 1:1 return based on price appreciation, MicroStrategy itself benefits from both the rising BTC value and the rising stock price—a 1:2 return.

For investors or lenders, it’s like holding BTC spot exposure and enjoying its upside. But for MicroStrategy, they hold the actual BTC while their equity value rises even faster—their paper wealth grows at twice the rate.

Not to mention, there may be further operational flexibility behind share lending or pledging activities.

Second issue: BTC cannot be inflated, but stocks can...

As long as MicroStrategy keeps buying BTC and maintains market belief that its stock will forever track BTC, any temporary dip below BTC’s implied value will attract arbitrageurs to close the gap. They could short BTC and go long on the stock, then exit when parity is restored (though I believe such trades are difficult in practice).

Still, this helps explain why MicroStrategy’s stock price closely tracks BTC.

But returning to MicroStrategy’s stock: does it have a hard cap on total supply? Can the company split shares or conduct future dilutions?

If the answer is yes, then a clear arbitrage opportunity emerges.

By exchanging seemingly BTC-equivalent assets (shares) for real BTC, even if BTC or the stock crashes later, investors who exit will sell shares—not BTC. MicroStrategy, however, has no obligation to sell its BTC holdings.

If BTC falls below $38,500, could the stock trade at a significant discount to BTC’s value?

In other words, could investors or lenders suffer losses far exceeding those from BTC’s decline alone?

I haven’t fully figured this out, but logically speaking, MicroStrategy’s model may not be a strict scam—it’s more of a mechanism that transfers risk onto lenders and investors.

For Michael Saylor, if BTC continues its bull run, he’ll eventually become one of the richest people in the world. If BTC crashes below $38,500, he remains the largest individual or entity holder of BTC after Satoshi Nakamoto. Either way, he wins.

Unless he chooses to sell BTC to repurchase shares and stabilize the spread when the stock trades at a discount—which could trigger further declines in both BTC and the stock—there’s theoretically no end to how long this model can continue.

Do you think that’s possible?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News