Bitcoin in BlackRock's View: Risk and Return Drivers Are Radically Different from Traditional Assets

TechFlow Selected TechFlow Selected

Bitcoin in BlackRock's View: Risk and Return Drivers Are Radically Different from Traditional Assets

In the long run, the adoption drivers of Bitcoin may differ from, or even be opposite to, the global macro factors influencing most traditional financial assets.

Author: Samara Cohen, Robert Mitchnick, Russell Brownback, Blackrock

Translation: 1912212.eth, Foresight News

Bitcoin has undergone a turbulent journey over its 15-year history—from obscurity to becoming an asset held by an increasing number of individuals and institutions around the world.

We believe that as a global, decentralized, fixed-supply, non-sovereign asset, Bitcoin’s risk and return drivers are fundamentally distinct from traditional asset classes and uncorrelated with them over the long term. We maintain this conviction even when short-term market behavior occasionally (and in some cases, profoundly) diverges from Bitcoin's fundamentals.

On August 5, 2024, Bitcoin experienced a 7% single-day decline at the same time the S&P 500 dropped 3%, amid a sharp global market correction triggered by unwinding of yen carry trades. This event coincided with a series of developments related to long-pending bankruptcies and liquidations (such as Genesis and Mt. Gox) unfolding over the preceding three days. Subsequently, liquidity competition caused by broad global market sell-offs further exacerbated the situation.

Drawing on historical patterns, these occasional periods of sharp short-term negative correlation with equities have typically been followed by price rebounds, with Bitcoin recovering to pre-sell-off levels within three days. We view this pattern as an example of fundamentals ultimately prevailing over short-term leveraged trading reactions. As Warren Buffett said, the stock market is a mechanism for transferring money from impatient investors to patient ones—a principle that has often held true throughout Bitcoin’s history.

Key Takeaways

1. Given Bitcoin’s unique characteristics and history, investors considering exposure to Bitcoin face challenges in comparing it to traditional financial assets using conventional analytical frameworks.

2. Bitcoin is clearly a high-risk asset due to its high volatility. However, the sources of its risks and potential returns are fundamentally different from those of traditional high-risk assets, making it ill-suited for most traditional financial models—including the risk-on/risk-off framework used by many macro commentators.

3. As a scarce, non-sovereign, decentralized global asset, Bitcoin is viewed by some investors as a safe-haven option during market panics and certain geopolitical crises.

4. In the long run, Bitcoin’s adoption trajectory may be driven by growing concerns about global monetary stability, geopolitical tensions, U.S. fiscal sustainability, and U.S. political stability—opposite to how traditional risk assets generally respond to these forces.

Introduction

Is Bitcoin a risk asset or a safe haven? This is one of the most common questions our clients ask when considering investing in Bitcoin for the first time. They want to understand Bitcoin’s long-term correlation with stocks and bonds, and how it reacts to changes in U.S. real interest rates or liquidity conditions.

We believe the answer lies in Bitcoin’s unique nature, which makes it incompatible with most traditional financial frameworks. Bitcoin’s long-term return drivers are fundamentally uncorrelated—and in some cases, even inversely correlated—with those of other portfolio components. While Bitcoin exhibits volatility and has shown temporary correlations with equities—especially during periods of extreme market stress—we aim to explain this dynamic in this paper.

Why Bitcoin Matters

First, we must examine the fundamental reasons why Bitcoin matters. Since its inception in 2009, Bitcoin has become the first internet-native monetary tool to achieve widespread global adoption. Its technological innovation lies in creating a digital-native, globally accessible, scarce, decentralized, and permissionless form of money. These attributes represent significant progress in addressing persistent problems that have plagued other forms of money for centuries:

1) Bitcoin’s supply is capped at 21 million coins, meaning it cannot be easily debased.

2) Its global and digital-native nature allows for near-instantaneous, near-zero-cost transfers across borders, overcoming longstanding frictions inherent in moving value across political boundaries.

3) Its decentralized and permissionless design makes it the world’s first truly open-access monetary system.

Although other crypto assets have emerged since Bitcoin’s original breakthrough—many aiming for broader use cases—Bitcoin stands out as the most prominent asset in the space and has gained global recognition. This gives Bitcoin a unique position among crypto assets as a global monetary alternative and a credible store of value with verifiable scarcity.

The Path to a $1 Trillion Market Cap

Despite significant price appreciation and broad global adoption, uncertainty remains about whether Bitcoin will ultimately evolve into a widely accepted store of value and/or global payment asset. Bitcoin’s fluctuating market value continues to reflect this uncertainty.

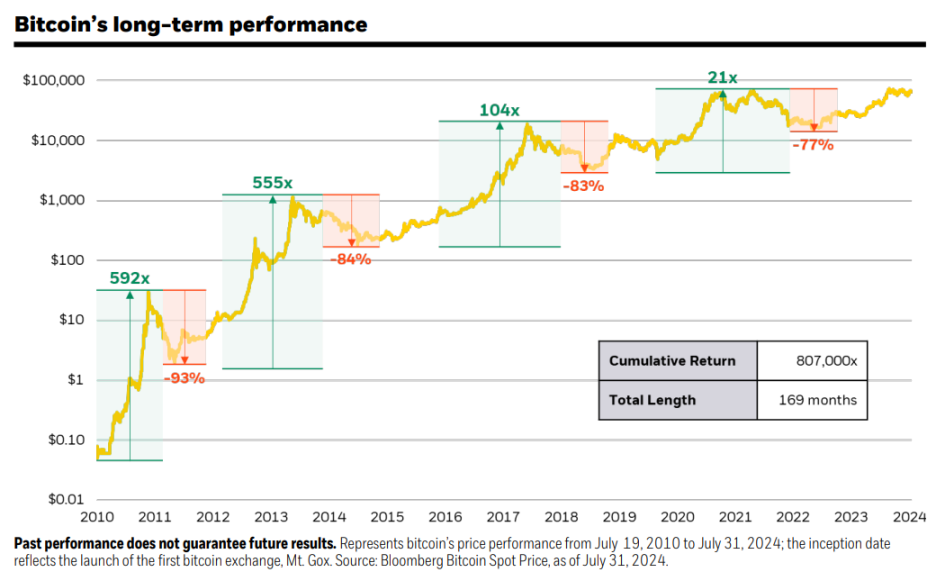

Over the past decade, Bitcoin outperformed all major asset classes in seven of those years, delivering an extraordinary annualized return exceeding 100%. Although it was the worst-performing asset in three of those years and endured four drawdowns exceeding 50%, Bitcoin has consistently demonstrated the ability to recover from corrections and reach new highs—even though bear markets have often lasted for extended periods.

These price fluctuations continue to reflect, to some degree, the evolving prospects of Bitcoin being adopted as a global monetary alternative over time.

“Macro-Variable Uncorrelated” Asset

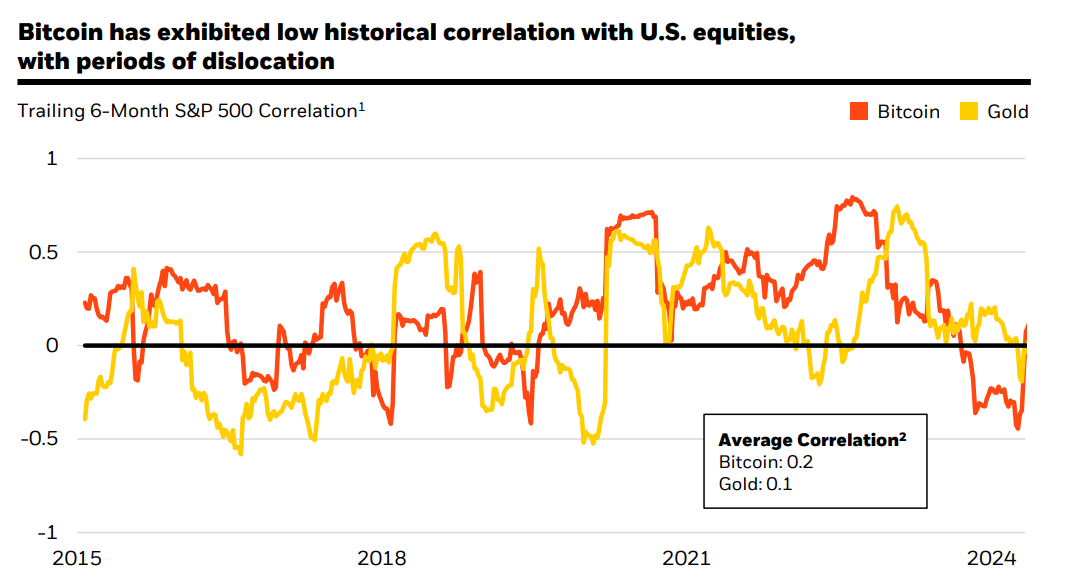

Bitcoin has minimal fundamental linkages to other macro variables, which explains its low long-term average correlation with equities and other risk assets. While Bitcoin’s correlation can spike sharply in the short term—particularly during sudden shifts in U.S. real interest rates or liquidity conditions—these episodes are transient and do not result in statistically significant long-term correlations.

As the first globally adopted decentralized, non-sovereign monetary alternative, Bitcoin carries no traditional counterparty risk, does not rely on any central system, and is not tied to the fate of any single nation. These features fundamentally decouple Bitcoin from key macro risks such as banking crises, sovereign debt crises, currency devaluations, geopolitical turmoil, and country-specific political and economic risks. Over the long term, Bitcoin’s adoption path may instead be influenced by rising or falling concerns about global monetary instability, geopolitical discord, U.S. fiscal sustainability, and U.S. political stability.

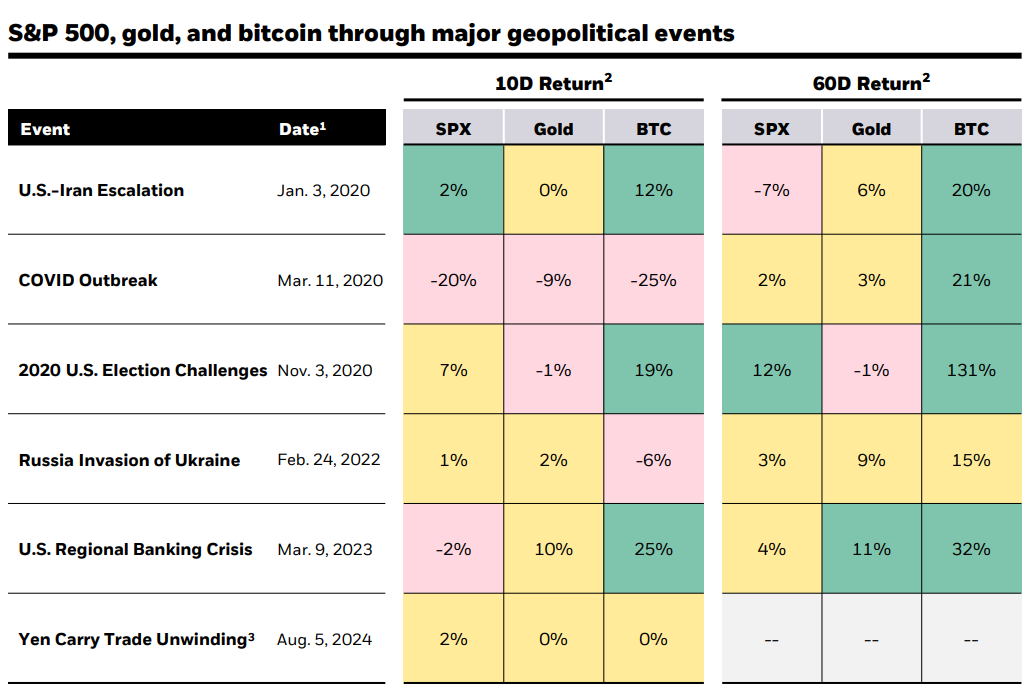

Because of these attributes, Bitcoin has been viewed by some investors as a safe-haven asset during some of the most disruptive global events over the past five years. Notably, Bitcoin sometimes experiences brief negative reactions during these events before rebounding. We attribute these short-term trading moves—which are difficult to explain through fundamentals—to the following factors:

1. Bitcoin trades 24/7 and can be settled into cash almost instantly, making it a highly liquid asset during periods of traditional market illiquidity, especially on weekends.

2. The cryptocurrency market remains immature, and investor understanding of Bitcoin is still limited.

In most cases—including the recent global sell-off on August 5, 2024—Bitcoin recovers to previous levels within days or weeks, often going on to higher prices as the positive implications of these disruptive events for Bitcoin’s fundamentals become more widely recognized.

U.S. Debt Dynamics Back in Focus

Against this backdrop, growing domestic and international concern about the U.S. federal deficit and debt levels has increased the appeal of potential alternative reserve assets as hedges against future events that could affect the dollar. This dynamic appears to be unfolding in other heavily indebted countries as well. Based on our client interactions to date, this explains much of the recent surge in institutional interest in Bitcoin.

Bitcoin Remains a Risk Asset

None of the above analysis negates the fact that Bitcoin itself remains a high-risk asset. It is an emerging technology still in the early stages of adoption on its path to potentially becoming a global payment and store-of-value instrument. Bitcoin has remained volatile and faces risks including regulatory challenges, uncertainty around adoption, and an immature ecosystem.

However, the key point is that these risks are unique to Bitcoin and not shared by traditional investment assets. Therefore, Bitcoin presents a compelling case for why simplistic risk-on/risk-off frameworks lack the nuance needed to be broadly applicable.

From a portfolio perspective, this is why holding a modest allocation to Bitcoin can provide diversification benefits, while larger positions may introduce excessive incremental risk due to Bitcoin’s independent high volatility.

Conclusion

While Bitcoin may move in tandem with equities and other risk assets in the short term, its fundamental drivers are fundamentally different—and in many cases, opposite—to those of most traditional investment assets over the long term.

As the global investment community faces escalating geopolitical tensions, growing concerns about U.S. debt and deficits, and rising political instability worldwide, Bitcoin may increasingly be seen as a distinctive portfolio diversifier against fiscal, monetary, and geopolitical risks investors face.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News