Ethereum's "Midlife Crisis": Daily Revenue Drops 99% Over Six Months, Once Fell and Rose Three Times

TechFlow Selected TechFlow Selected

Ethereum's "Midlife Crisis": Daily Revenue Drops 99% Over Six Months, Once Fell and Rose Three Times

Looking back at Ethereum's past ups and downs, what matters is not whether crises exist, but whether Ethereum can continue to solve the problems it encounters during its development.

Author: Arain, ChainCatcher

Editor: Marco, ChainCatcher

Does Ethereum's price matter?

Yes. Even Justin Drake, a member of the Ethereum Foundation, stated in a recent AMA that "ETH appreciation is crucial to Ethereum’s success."

Yet in this market cycle, Ethereum’s price performance has been disappointing. According to Coingecko data, over the past year Bitcoin has risen more than 116% against the U.S. dollar, Ethereum up 44%, while Solana surged over 548%. Within a blue-chip investment portfolio, Ethereum clearly lags behind.

The absence of standout developments, lackluster price action, and the stellar performance of so-called "Ethereum killer" Solana have placed Ethereum under increasing public scrutiny over the past year, with skepticism surfacing periodically. This criticism reached a boiling point during the Bankless episode featuring Multicoin Capital.

In that episode, Bankless highlighted a concerning set of figures: SOL/ETH achieved a 300% annual growth rate over the past year, while ETH/BTC declined by 50% over the past two years, halving Ethereum’s market cap relative to Bitcoin.

This data further amplified perceptions of Ethereum’s underperformance in the current cycle. During the discussion, Multicoin partner Kyle Samani described Ethereum’s current state as a “midlife crisis.”

Interestingly, although the Bankless host claimed Kyle was the ideal guest to discuss Ethereum at this moment, Multicoin has long held a bearish stance on Ethereum and actively invested in “Ethereum killers.” The firm first gained attention for backing EOS during its peak and stubbornly refusing to admit error, and now has Solana in its portfolio—a project potentially capable of rivaling Ethereum.

Now the question arises: does Ethereum’s price stagnation truly indicate an underlying problem? Has Ethereum really entered a “midlife crisis” as Kyle suggests?

Stagnation—What Happened?

The description “Ethereum isn’t going up” is inaccurate, especially when comparing Ethereum to itself. According to Coingecko data, from October 2023 to March 12, 2024, Ethereum was actually in an uptrend—though it underperformed Bitcoin, which not only reclaimed but surpassed its previous cycle high. During this period, Ethereum peaked at $4,070.60 per coin, compared to its all-time high of $4,878.26.

Dense news flow around spot Bitcoin ETFs and spot Ethereum ETFs dominated the market during this time. The SEC ultimately delivered, approving the spot Bitcoin ETF on January 11, 2024, and the spot Ethereum ETF on May 24, 2024.

Perhaps influenced by expectations around ETF approvals, both Bitcoin and Ethereum prices began surging as early as October 2023, suggesting possible front-running of bullish catalysts.

For Ethereum, another key difference was the “Dencun (Cancun) upgrade,” a major network event following the Shanghai upgrade, aimed at improving scalability and reducing network fees. The most visible outcome: gas costs for transactions on Ethereum Layer 2 networks were expected to drop by over 90%—a target met in practice.

The Cancun upgrade completed on March 13, 2024, aligning almost exactly with Ethereum’s prior price rise. It was after this upgrade that Ethereum entered its current phase of stagnation—a trend that persists without reversal to date.

Following the upgrade, the SEC approved spot Ethereum ETFs and ETPs for listing and trading—another layer of positive news on the trading front. After its ETF approval, Bitcoin continued climbing to new highs. But that script did not replay for Ethereum.

According to Sosovalue.xyz, since approval, U.S. spot Bitcoin ETFs have seen approximately $16.9 billion in net inflows, whereas U.S. spot Ethereum ETFs have suffered -$560 million in net inflows. Rather than attracting capital, Ethereum ETFs have accelerated outflows, placing downward pressure on ETH’s price.

Dune data shows that 64.7% of assets under management (AUM) in U.S. spot Ethereum ETFs belong to Grayscale. Their research arm, Grayscale Research, argued in a May report that U.S. spot Ethereum ETFs could boost ETH demand and price. However, due to relatively high valuations at approval, they believed upside potential post-approval would be limited.

Ethereum’s price failed to reflect support from ETF buyers. In an August research report, Grayscale Research identified two reasons for Ethereum’s subsequent sharp decline:

-

First, long positions in perpetual futures: approval of U.S. spot Ethereum ETPs encouraged traders to increase long exposure, but liquidations during the downturn accelerated price declines;

-

Second, actual or anticipated selling by a few large holders—including market maker Jump Crypto, venture firm Paradigm, and Golem Network. Grayscale Research estimated these three entities collectively held around $1.5 billion worth of ETH at the time, all potentially subject to sell-offs.

Given Ethereum’s lack of significant rebound in August, Grayscale Research noted this reflected excessive speculative positioning—particularly long positions on CME futures and perpetual contracts.

"More fundamentally, the Ethereum network is undergoing a major transformation… Ethereum plans to scale by moving more transactions to L2 networks, which will periodically settle back to the L1 mainnet. This strategy is working: Ethereum L2 activity has boomed this year, with major companies like Sony announcing projects on Ethereum. However, this also reduces fee revenue on the mainnet, which may negatively impact ETH’s value," wrote Grayscale Research in a September 3 report, adding: "Ethereum’s scaling strategy is proving effective. Current market pessimism about Ethereum is unfounded—but shifting market consensus may take time."

In other words, the lack of a turnaround reflects that the market hasn’t yet updated its narrative around post-upgrade Ethereum. A key factor is “declining mainnet fee revenue”—the direct result of EIP-4844 in the Cancun upgrade, designed precisely to scale L2 and reduce fees. The Bankless-Multicoin episode directly targets this very point as Ethereum’s core weakness.

So, has L2 pushed Ethereum to the edge of danger?

L2 Under Fire

The Multicoin critique centers squarely on Layer 2. Kyle Samani argues “Layer 2 doesn’t belong to Ethereum because it doesn’t contribute to Ethereum’s value capture.” Specifically, he claims Ethereum L1 outsources all MEV and execution to L2—like handing away its money-making tree to others.

This view essentially dismisses a core pillar of Ethereum’s upgrade efforts.

Layer 2 is not the endgame—it’s a solution born from necessity. Looking back at Ethereum’s performance during past bull markets, network congestion was frequently criticized. Users often found fees prohibitively high or even unusable during peak times, fueling constant calls for “ETH 2.0.”

ETH 2.0 is Ethereum’s long-term upgrade roadmap, of which Layer 2 is a critical component—designed to solve scalability, much like building an elevated expressway to relieve traffic on a congested road.

The Shanghai upgrade, completed April 13, 2023, marked the beginning of the Layer 2 era. Key changes included EVM object format updates, enabling withdrawals from the beacon chain, and Layer 2 fee reductions—all while completing Ethereum’s full transition from PoW to PoS.

After the Shanghai upgrade, massive amounts of staked ETH were withdrawn, while new participants also joined.

Dune data shows approximately 13.96 million ETH in net staking inflows since Shanghai. This demonstrates strong market interest in staking. Yet the upgrade had little impact on secondary markets: Ethereum traded around $1,920 at upgrade completion and dropped to $1,652 before the Holesky testnet launch (precursor to Cancun). This muted reaction may reflect broader market conditions, as Bitcoin showed similar price behavior.

The March 13, 2024 Cancun upgrade was pivotal for Layer 2, most notably slashing gas fees: users now enjoy faster speeds, better performance, and lower costs for the same price. This is driven by EIP-4844—the very feature Kyle Samani harshly criticizes.

Protolambda, researcher at Optimism and former Ethereum Foundation contributor, explained that Layer 1 acts as a data layer, while L2 handles computation. Layer 1 provides security and data availability for Rollups (of which L2 is one form). By introducing a new transaction type carrying “blob data,” the base layer can store L2 data more efficiently without compromising data availability security.

“Blob data” is a new transaction type introduced in EIP-4844 that pays fees. These large data packets are temporarily stored in the consensus layer, thereby reducing costs across the Ethereum network and Rollups.

Data seems to visually support Kyle Samani’s argument:

Token Terminal shows Ethereum L1 revenue hit its yearly high (~$35 million) on March 5, and its lowest point (~$200,000) on September 2—a 99.4% drop in half a year.

Base, Coinbase’s L2 built on Ethereum, generated ~$2.5 million in revenue in August but paid only ~$11,000 to Ethereum.

At first glance, L2 is taking a slice of L1’s pie. While Ethereum succeeded in lowering gas fees, moving “execution state” off L1 to L2 remains problematic in Kyle Samani’s view. Bankless’ Ryan further questions whether, at maturity, L2 might compete with Ethereum L1 and break their cooperation.

Independent researcher @Web3Mario argues that L1 and L2 aren’t in an outsourcing relationship as Kyle describes, but rather a hierarchical one—since L2 does not handle consensus, relying instead on L1 for finality via optimistic or ZK-based mechanisms.

L2 acts as Ethereum’s value-capturing agent across domains, while Ethereum ensures its security—thus enabling L1 to “tax” L2. This view appears closer to the original design intent of Ethereum Foundation researchers.

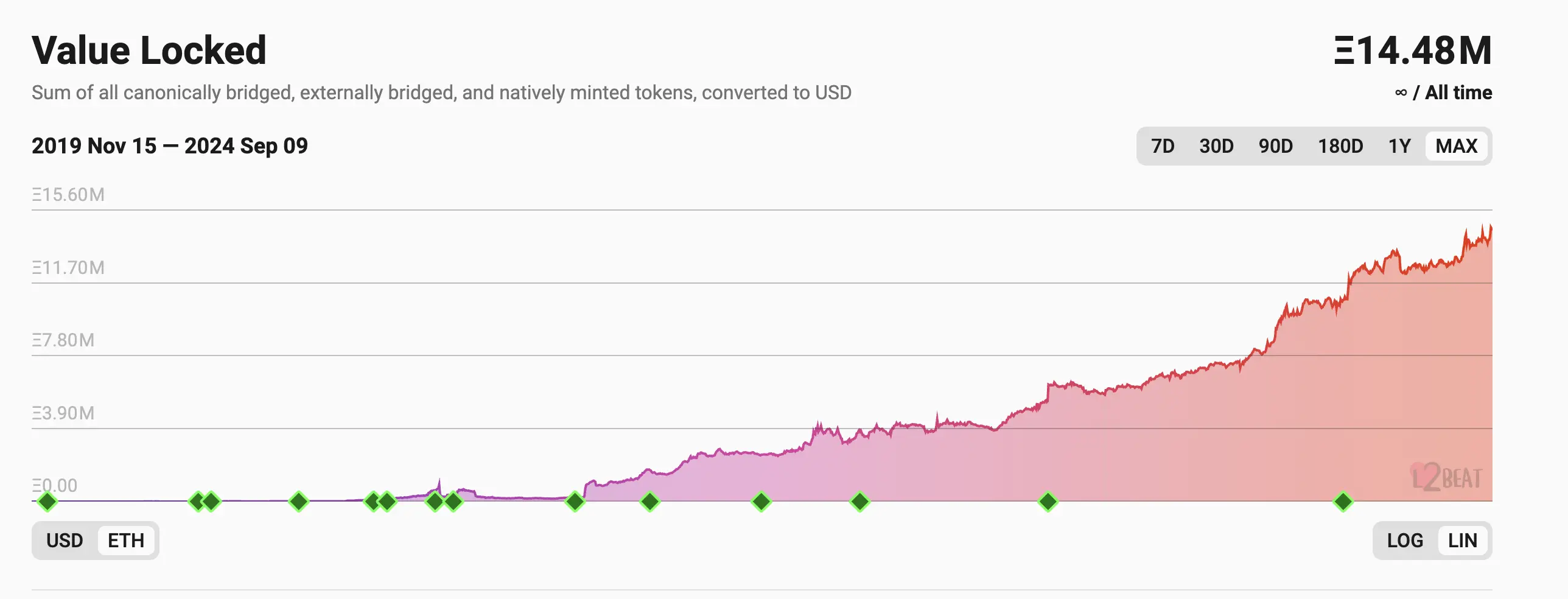

From current data, the L2 space is extremely competitive. Post-Cancun, L2 has not contributed revenue to L1—instead diverting income away. Yet according to l2beat.com, there are now 71 L2 projects, with total TVL spiking rapidly after March 2024, amounting to roughly 14.48 million ETH.

On September 5, the Ethereum Foundation research team hosted its 12th AMA on Reddit, addressing several market concerns.

Dankrad Feist, an Ethereum Foundation researcher, said Ethereum aims to build the most neutral financial platform. L1 serves as an intersection of multiple subdomains. High-value activities will generate fees (assuming sufficient L1 scaling), but alternative value accrual models exist—such as ETH as a primary medium of exchange or collateral—which will drive future ETH price growth.

"Many believe a rollup-centric roadmap weakens Ethereum’s fee revenue and MEV, eventually making rollups parasitic. I disagree. The highest-value transactions will still occur on Ethereum L1, while rollups expand the ecosystem by providing vast transaction capacity. This is symbiotic: Ethereum offers cheap data availability to rollups; rollups make Ethereum L1 the natural hub for high-value transactions," replied Dankrad Feist.

Ethereum Foundation researcher Anders Elowsson believes ETH appreciates when Ethereum enables sustainable economic activity.

Notably, scaling L1 execution remains part of Ethereum’s roadmap, with recent progress. Official statements suggest Ethereum is not, as Kyle Samani claimed, betting everything on a rollup-centric path while abandoning L1 scaling.

Dankrad Feist confirmed that scaling L1 execution is a parallel goal alongside rollup development. L1 itself is expected to scale 10 to 1,000 times beyond current capacity, with rollups handling the rest to achieve global scale. Justin Drake of the Ethereum Foundation said the long-term sustainability plan involves using SNARKs to scale EVM execution on the mainnet. Over recent months, significant progress has been made in SNARKing L1 EVM—lightening the load for users and validators. Validators will verify low-cost SNARKs instead of re-executing every EVM transaction.

A Review of Ethereum’s Past Crises

Regardless of whether Ethereum is facing a real or imagined crisis now, the most important factor is the team’s ability to solve problems.

Looking back at past Ethereum crises:

1. The 2016 “smart contract vulnerability crisis,” epitomized by “The DAO hack,” where a flaw enabled hackers to steal millions of dollars worth of Ether.

Solution: The Ethereum community executed a hard fork (leading to Ethereum Classic), reversing the transaction and restoring funds. This split the network into Ethereum (ETH) and Ethereum Classic (ETC).

2. Ongoing since 2017: network congestion crisis. As DApps (decentralized applications) surged, Ethereum became severely congested, causing transaction fees to spike.

Solution: The community explored scaling solutions, laying the foundation for ETH 2.0, incorporating sharding and Layer 2 scaling techniques like Rollups and State Channels.

3. Since 2018: high energy consumption due to PoW has raised environmental concerns. While not a full-blown crisis, the response significantly shaped Ethereum’s evolution.

Solution: Transition from Proof-of-Work (PoW) to Proof-of-Stake (PoS) to drastically cut energy use.

Each crisis opened doors for so-called “Ethereum killers”—new public chains like BNB Chain, Cardano, Avalanche, Polkadot, EOS, and Solana. Except for Solana, which remains active today, the others once challenged Ethereum in prominence.

Today, Solana is the last remaining vocal “Ethereum killer,” with Multicoin as one of its largest backers.

In this light, Ethereum’s resilience makes it a success story.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News