Opinion: Emerging from the山寨 bear market requires a DeFi revival

TechFlow Selected TechFlow Selected

Opinion: Emerging from the山寨 bear market requires a DeFi revival

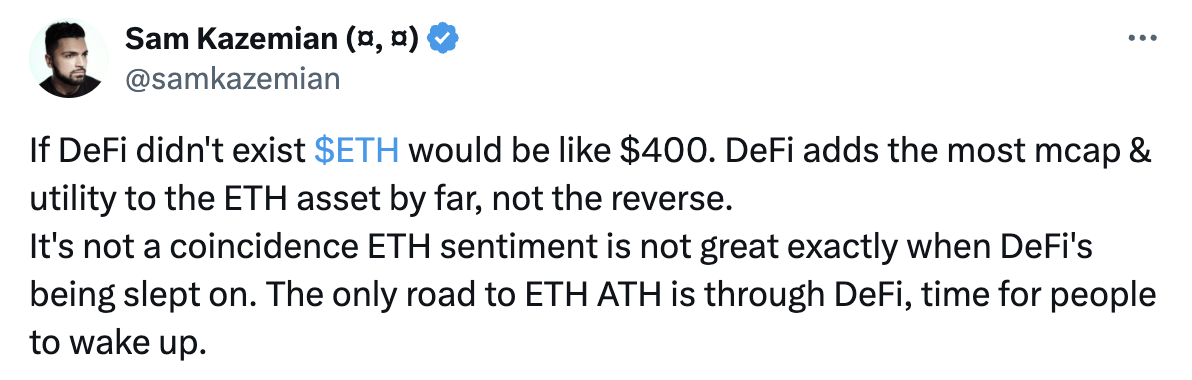

Without DeFi, Ethereum's price might still be at 400.

Author: Alex Liu, Foresight News

If DeFi didn't exist, ETH might be priced at $400. DeFi has added the most market cap and use cases to ETH so far—not the other way around. It's no coincidence that when DeFi is neglected, sentiment in the ETH ecosystem sours. The only path for ETH to reach new highs is through DeFi—everyone needs to realize this. — Sam Kazemian, Founder of Frax Finance

What is the current state of the crypto market?

-

A bear market for altcoins—Even though BTC remains volatile around $60,000, many altcoins have retraced all their gains from this cycle, even hitting new lows. Most new tokens peak immediately upon launch.

-

More gamblers than believers—"Value investing leads nowhere; go all-in on MEMEs and live in a palace." This isn't just a joke—it reflects the real mindset of many in the industry suffering from "wealth anxiety." Chase new launches, not old projects; even if friends are "cannibalizing" each other, they won't play sucker for VCs.

-

Lack of capital inflows—There's no so-called "mass adoption," no retail inflows, just participants trading among themselves. For A to profit, B must lose. There’s no growing the pie together.

How can we break this stalemate? I believe DeFi needs a renaissance.

The Dilemma of DeFi

DeFi has struggled unusually in this cycle. In an era dominated by traffic and narratives, it has lost attention and relevance. How did this happen?

Ninety percent of the crypto market is narrative-driven, and the depressing truth is—most influential shillers and KOLs have no skin in DeFi tokens. It's far more profitable to promote a meme coin they just bought or partner with new protocols that allocate large token supplies to KOLs.

Those who create narratives rarely hold DeFi tokens themselves. KOLs see little value in mentioning OG DeFi projects because maximum benefits go to early insiders: large token allocations held by teams or VCs, most of which are already unlocked.

Thus, promoting DeFi tokens falls primarily to the builders themselves and true DeFi believers.

In short: DeFi’s困境is an inevitable outcome when market sentiment is restless and speculators dominate. But if beyond 90% narrative games, there remains 10% pursuit of real utility—when rationality returns, the market will correct itself.

DeFi, The Future

DeFi Has Intrinsic Value

DeFi tokens have real value—entirely opposite to the low-circulating, high-FDV VC coins and meme tokens people despise.

OG DeFi tokens (AAVE, MKR, COMP, CRV, etc.):

-

Mostly circulating now

-

Increasingly recognized revenue-sharing mechanisms

-

Time-tested PMF (product-market fit) and proven resilience through long-term development

Many DeFi protocols are already profitable, with buyback mechanisms (Maker), ve-token models (protocol revenues and external bribes directed to locked token holders, as in Curve), or planned revenue-sharing schemes (Aave). Holding these tokens equates to owning a continuous stream of cash flow.

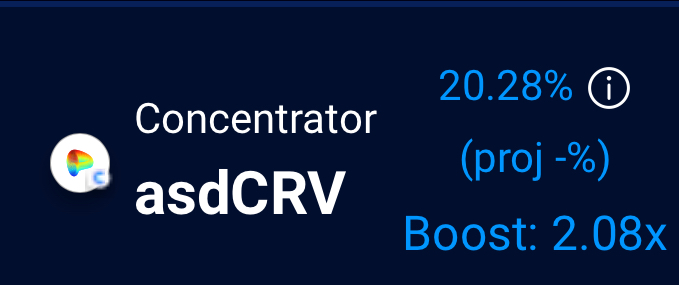

Currently, locking liquidity on Curve yields ~20% annualized return

DeFi Is the Core Use Case

What exactly is blockchain solving? Blockchain addresses mutual distrust by replacing data stored centrally (by banks, companies) with redundant storage across every participant, then achieving consensus on a shared public ledger—essentially, redundant storage.

Redundant storage is costlier and less efficient. Only use cases where users are willing to pay this premium can compete against centralized solutions. Financial activities like trading, transfers, and lending—highly asset-sensitive—can tolerate some inefficiency and higher costs (relative to centralized systems) in exchange for absolute security. Decentralized finance (DeFi) is therefore blockchain’s natural core use case.

DeFi Is the Industry Direction

The current market issues—too many gamblers, lack of capital inflows—are solvable as the industry evolves. But where is the industry headed?

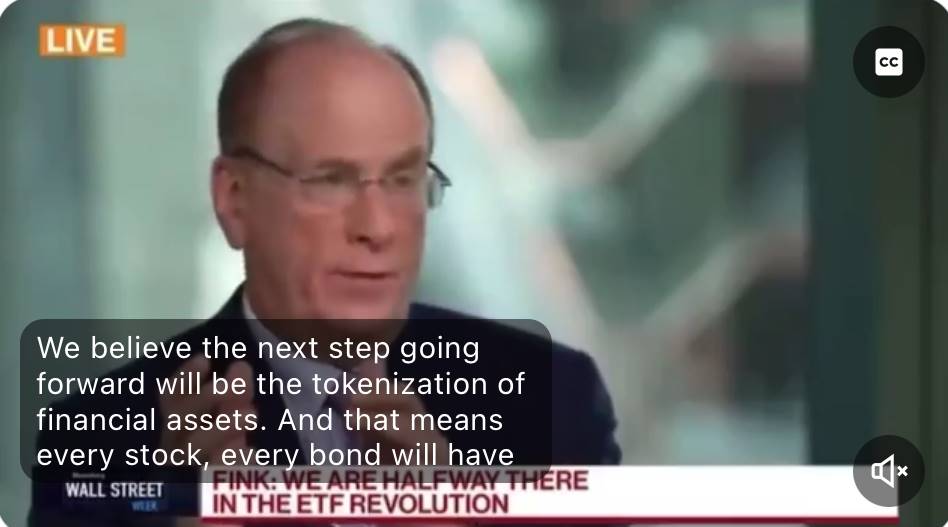

Larry Fink, CEO of BlackRock—the Wall Street giant behind Bitcoin ETF approval and the main catalyst of this cycle—has stated that all stocks, bonds, and financial assets will eventually be tokenized on-chain.

Can financial assets going on-chain bypass existing decentralized financial infrastructure?

For stable asset swaps—like converting on-chain USD to on-chain EUR—would one choose Curve?

Could multi-trillion-dollar-sized interest rate derivatives in traditional markets directly or indirectly leverage Pendle?

For collateralized lending of financial assets, would you ignore battle-tested, code-proven Aave? (If traditional finance resists full decentralization and relinquishing control, couldn’t Aave design a dedicated market for Lido—and likewise customize one for BlackRock?)

Larry Fink in an interview

DeFi is the direction of the industry, with sufficient scale to absorb transformative levels of capital.

DeFi Is Experiencing a Renaissance

DeFi is waking up.

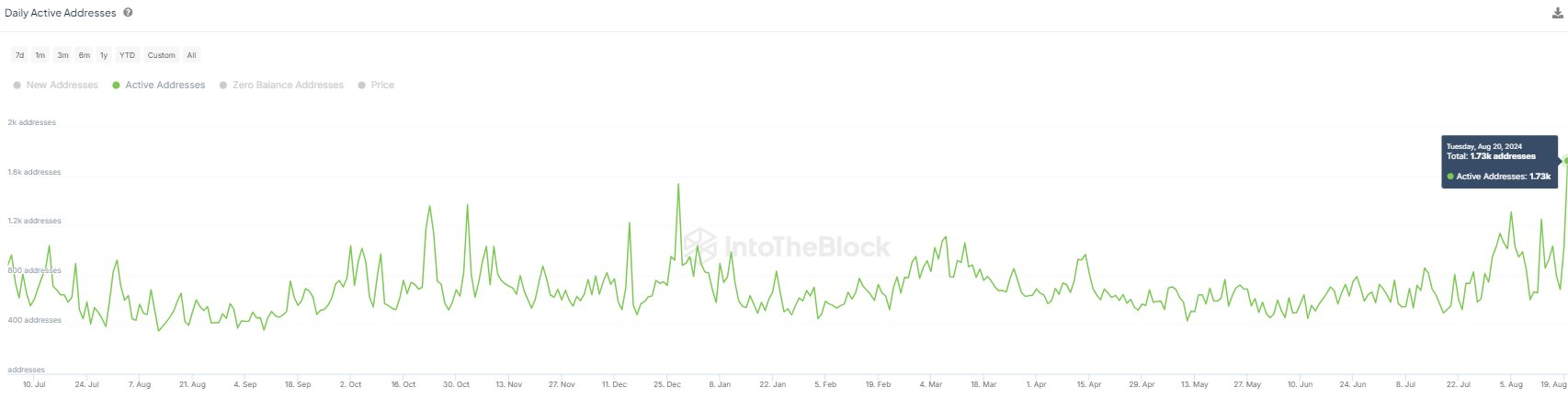

Since Aave announced its revenue-sharing plan, its token price nearly doubled from the bottom. After Curve Finance founder’s borrowing position was finally liquidated, the "bearish" pressure cleared, and CRV rebounded from 0.18 USDT to 0.34 USDT. On-chain metrics across major protocols are also improving:

Aave daily active addresses hit a near-one-year high on August 19

With DeFi reviving, how far off could a raging bull market be?

Some insights sourced from: https://x.com/DefiIgnas/status/1824447367417835559

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News