DeFi on the Decline? Leading Projects Returning to Fundamental Value

TechFlow Selected TechFlow Selected

DeFi on the Decline? Leading Projects Returning to Fundamental Value

DeFi is not only far from dead, but also presents an excellent opportunity for strategic positioning.

By Alvis

Are the OG tokens in the DeFi (decentralized finance) space dead?

This was the focal point of discussions during the dramatic crypto market black swan event on August 5. As global markets were gripped by fears of recession, a spectacular plunge followed, triggering severe deleveraging across the cryptocurrency sector. Yet, under this stress test, DeFi—the backbone of liquidity—did not suffer serious dislocations or credit risks. On the contrary, it demonstrated stronger resilience than ever before.

Does this mean that DeFi has finally reached its turning point? Let's reassess this phenomenon.

Token Performance

Data source: CoinGecko

Although Bitcoin hit an all-time high in March, most DeFi tokens have significantly underperformed BTC—and even ETH. The DeFi Pulse Index (DPI) has declined relative to ETH for three consecutive years. During this cycle, ETH itself has also lagged behind BTC. DPI includes DeFi-related tokens such as UNI, MKR, LDO, AAVE, SNX, PENDLE, and others.

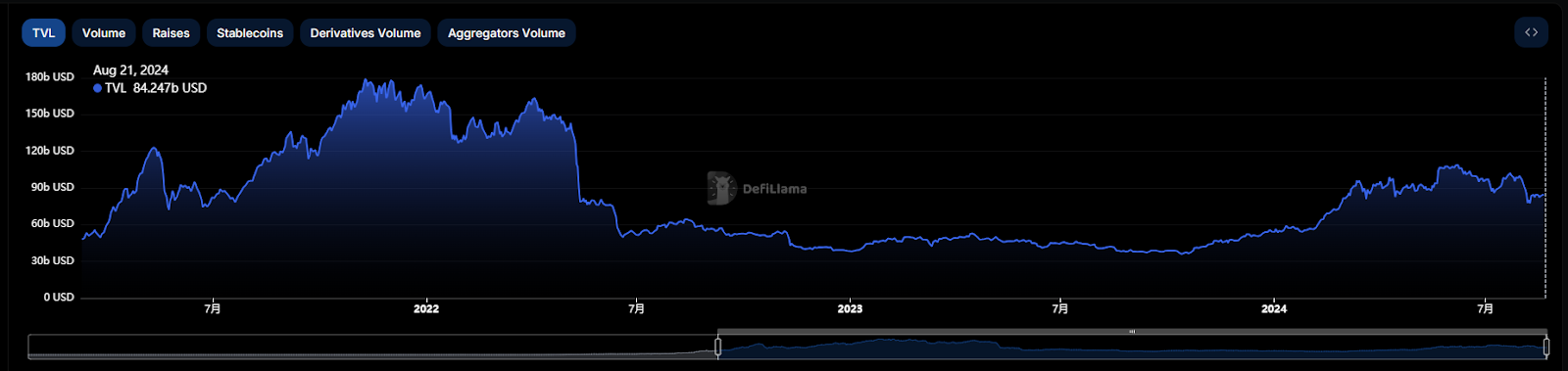

Total Value Locked (TVL)

Data source: DeFiLlama

As of August 21, 2024, multi-chain DeFi TVL has dropped to $8.46 billion. This represents a 54.7% decline from its historical peak of $18.68 billion in December 2021, and is only 61% higher than the level seen after the market turmoil triggered by the Luna collapse. This notable downward trend can be partly attributed to reduced asset wrapping—such as wrapped Ethereum and Bitcoin assets—as well as capital outflows compressing overall liquidity.

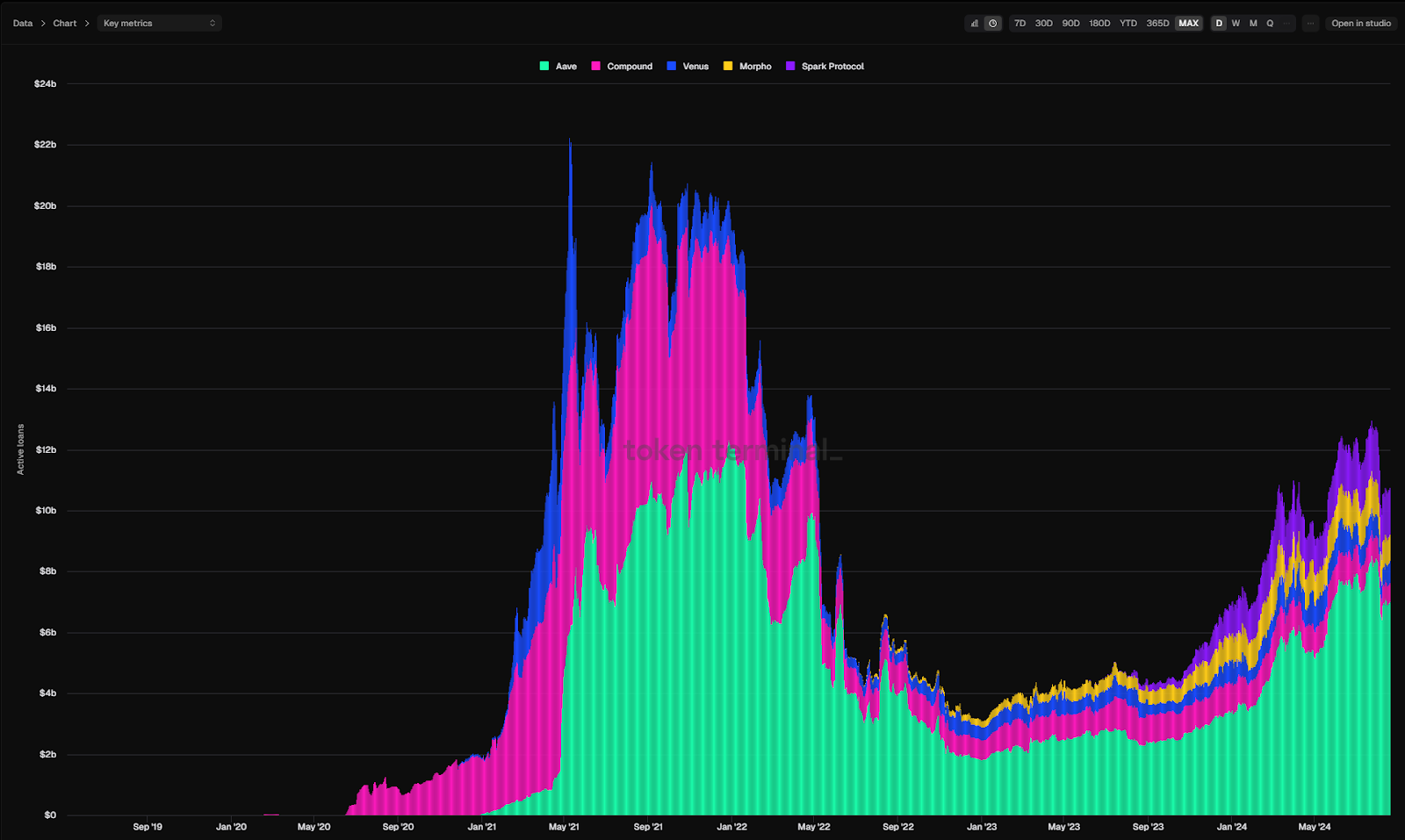

Borrowing Volume

Data source: Token Terminal

Borrowing volume—the value of outstanding debt in lending protocols—is currently at $10.6 billion. This marks a 49.7% drop from its peak of $21.1 billion in December 2021. Declining demand for leveraged loans has directly contributed to weakness in the DeFi ecosystem.

DeFi, one of the oldest sectors in the crypto space, has underwhelmed during this bull market.

If we judged solely based on these three metrics, we would conclude without hesitation that DeFi has fallen far short of expectations in this cycle.

The reasons for the sustained downturn in altcoins—including DeFi tokens—are largely similar, and can be summarized in three points:

First, lackluster growth on the demand side. There is a scarcity of novel and compelling business models, and product-market fit (PMF) remains elusive for many projects.

Second, explosive supply-side growth. As industry infrastructure improves, barriers to entry have lowered, leading to an influx of new projects and token offerings that exceed market absorption capacity.

Third, continuous unlocking of tokens. Projects with low circulating supply and high fully diluted valuations (FDV) are steadily releasing tokens into the market, creating significant selling pressure.

The downward adjustment in altcoin valuations reflects market self-correction—a natural deflation of bubbles and a form of capital redemption through market selection.

Most venture-backed tokens aren’t worthless; they were simply overvalued. The market has ultimately brought them back to reasonable levels.

When mountains and rivers block the path, doubt if there’s a way forward—then suddenly, willows darken and flowers brighten, revealing another village.

DEX Volume

Data source: DeFiLlama

In recent months, DEX trading volume has surged, reaching 80% of the November 21, 2021 peak of $308.6 billion. June 2022 volume is on track to hit $190 billion. Given the strong correlation between trading activity and price appreciation, coupled with liquidity inflows from ETFs, this upward trend may persist through year-end.

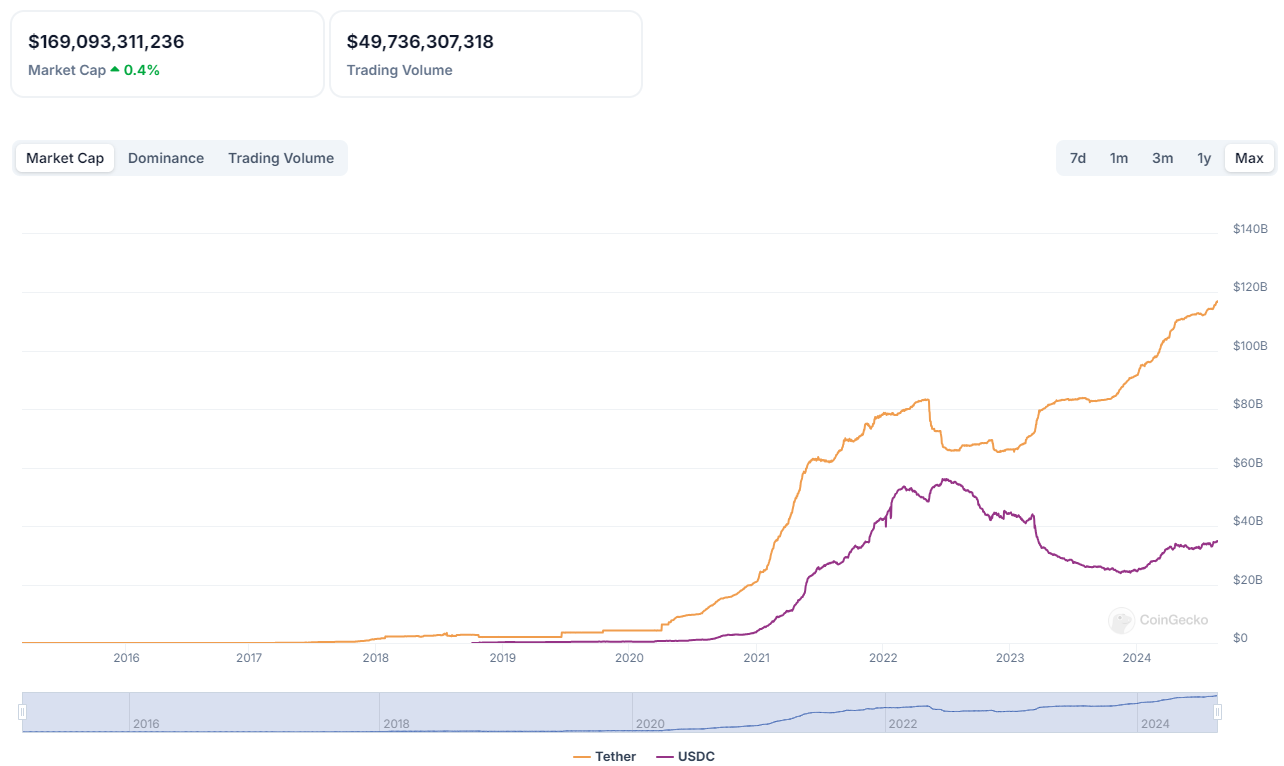

Stablecoin Supply

Data source: CoinGecko

The current stablecoin market cap stands at $169 billion, gaining widespread global adoption and gradually expanding beyond narrow crypto trading use cases to become a key option for global payments.

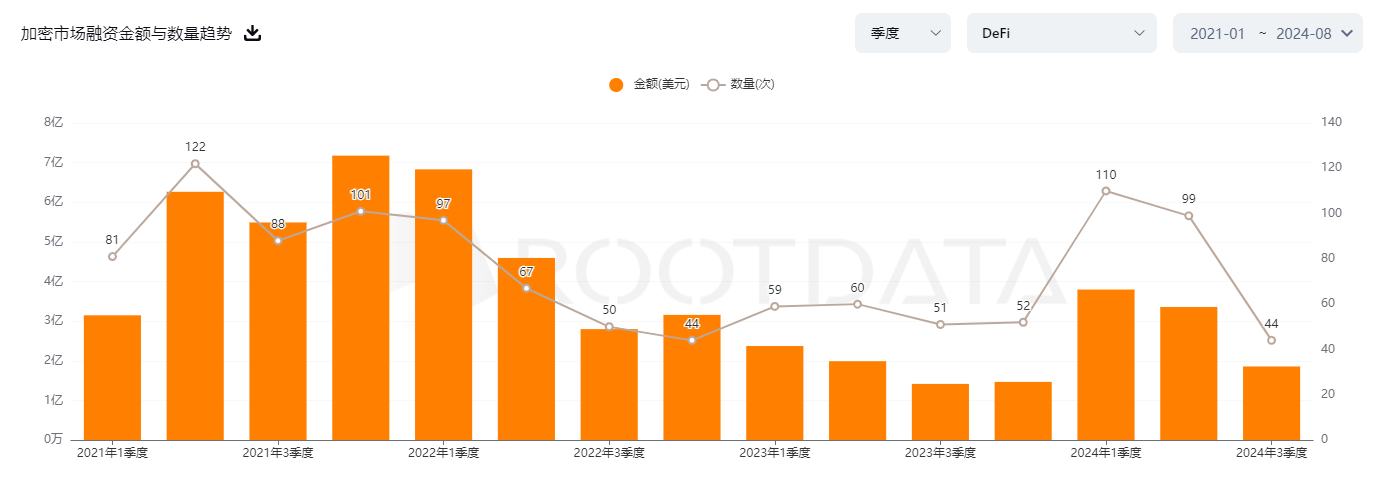

Institutional Funding

DeFi is experiencing a notable revival in venture capital investment. According to the latest data from Rootdata, total investments in DeFi reached $900 million in the first half of 2024. While this figure hasn't yet matched the highs of 2021, it clearly marks a recovery from the lows of 2023, signaling renewed market confidence.

From these three indicators, we see that the current state of DeFi isn't so bleak after all. Is the reality really as negative as most people suggest? Are DeFi value tokens, like Layer2 projects, still in an overvalued zone?

Let’s take a closer look at what some top-tier DeFi projects are doing.

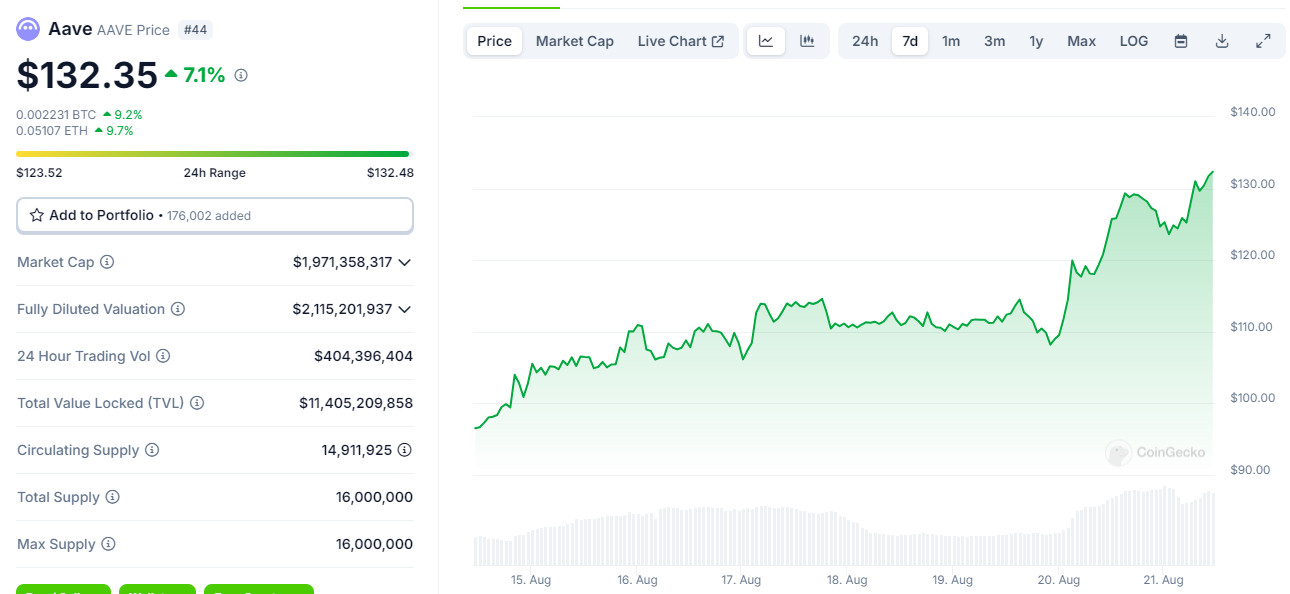

Lending: Aave

Aave is one of the longest-standing DeFi projects. After raising funds in 2017, it transitioned from peer-to-peer lending (when it was known as Lend) to a pool-based model. In the previous bull cycle, it surpassed Compound, its main competitor, and now leads the lending sector in both market share and market cap, with active loans totaling $7.5 billion. Aave’s revenue has already exceeded previous bull market highs, reflecting strong profitability.

Data source: CoinGecko

At the time of writing, the AAVE token price exceeds $132, up more than 50% over the past seven days and matching its March peak. For a deeper analysis of AAVE’s explosive rally, refer to Mars Finance’s earlier report:

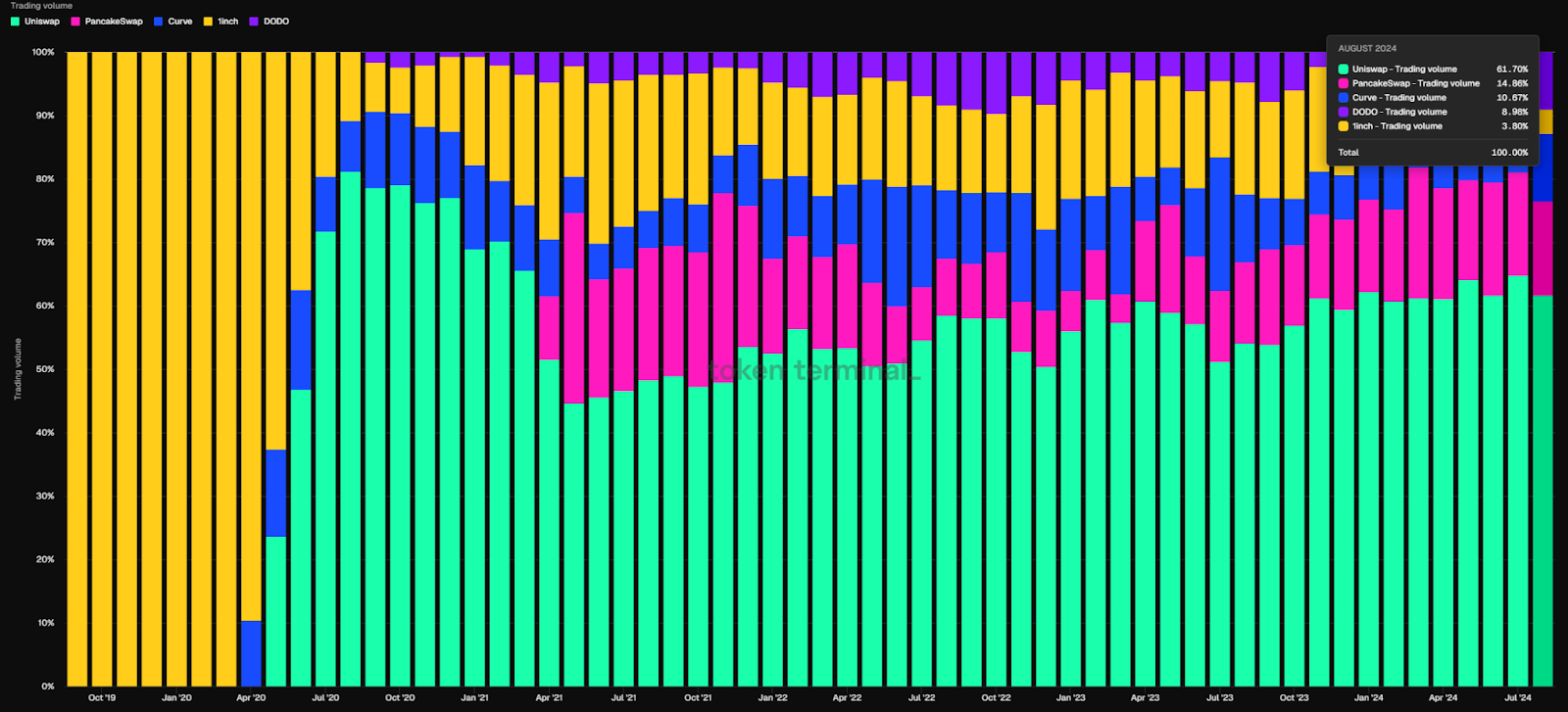

DEX: Uniswap

Data source: Token Terminal

Since the launch of its V2 version in May 2020, Uniswap has experienced a rollercoaster in decentralized exchange market share. It peaked in August 2020 with nearly 78.4% of the market, but fell to a low of 36.8% in November 2021 amid fierce DEX competition. However, like a phoenix rising from the ashes, it has not only regained stability but reclaimed dominance with a 61.7% market share, demonstrating remarkable resilience.

A common flaw with many DeFi tokens is their lack of utility—they serve merely as governance tokens. But this is beginning to change: Uniswap’s proposed fee switch could become a pivotal moment emulated by other DeFi protocols, and the UNI token surged following news of this development.

Additionally, regulatory clarity may accelerate profit-sharing trends. In April 2024, Uniswap received a Wells Notice from the SEC, indicating potential enforcement action. While this introduced uncertainty, it coincided with positive progress on the FIT21 bill, offering a clearer and more predictable regulatory outlook for DeFi projects like Uniswap.

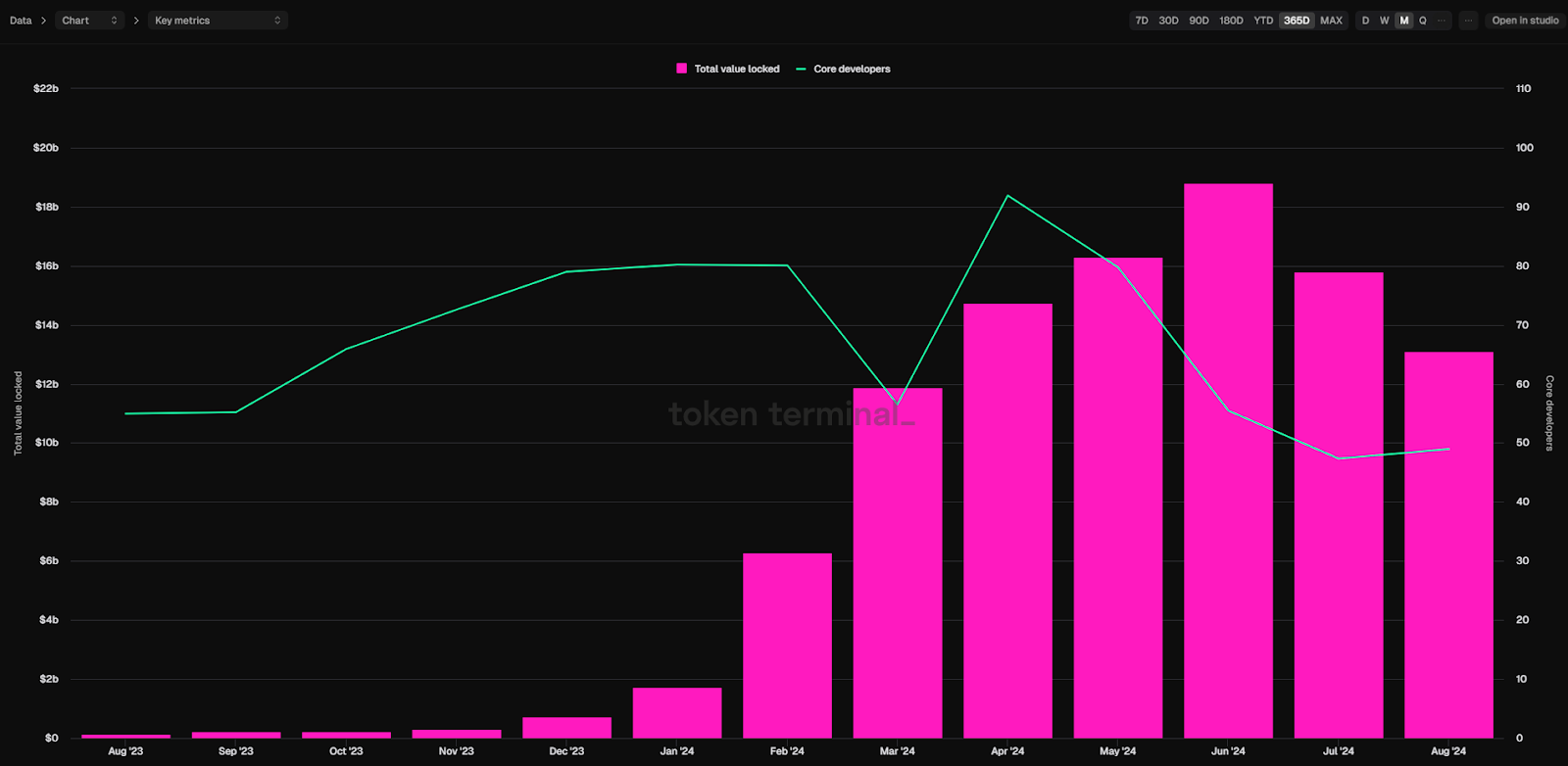

Restaking: EigenLayer

Restaking refers to reusing ETH already staked on the Ethereum mainnet to secure additional protocols. Through this mechanism, users can earn returns not only from their original stake but also from supporting other projects, increasing their potential rewards.

Founded in 2021, EigenLayer pioneered the concept of restaking. It acts as a middleware layer between Ethereum and other applications, deploying smart contracts on the mainnet to allow stakers to re-stake their ETH and liquid staking tokens (LSTs) into EigenLayer.

Data source: Token Terminal

Since launching in June 2023, EigenLayer has grown rapidly, with over $12 billion in total staked value—making it one of the largest blockchain protocols in the market. Its staked value now exceeds that of major DeFi platforms such as Aave, Rocket Pool, and Uniswap.

Thus, rather than being dead, DeFi today presents a prime opportunity for strategic positioning

The DeFi space has matured, developing robust business frameworks and sustainable profit models. Leading projects like Aave, Uniswap, and EigenLayer have built formidable moats.

From a supply perspective, top DeFi projects—having launched early—have mostly passed their peak token issuance phases. With institutional allocations nearing full release, future selling pressure in the market is expected to ease significantly.

Although DeFi has garnered less attention and exhibited weaker price performance compared to emerging narratives like Memes, AI, and DePIN in this bull cycle, its core business metrics—trading volume, lending scale, and profitability—continue to rise. Take Aave, for example: its quarterly net income has not only surpassed the previous cycle’s highs but set a new record. This indicates that the recent price surge in AAVE is well-founded.

Considering traditional financial institutions like BlackRock have increasingly embraced crypto assets—whether through pushing crypto ETFs or issuing U.S. Treasury assets on Ethereum—DeFi is likely to become a key investment focus in the coming years. As these financial giants enter the space, acquisitions may offer them a fast track to market entry. Any sign of M&A activity—even whispers of intent—could trigger a revaluation of leading DeFi projects.

As crypto investing becomes more rational, the bubbles inflated during periods of irrational exuberance have been pricked by tightening liquidity. In this environment, crypto applications backed by solid economic value, high product-market fit, and proven resilience are best positioned to seize new opportunities. Just as Victoria Harbour once symbolized the glory of the British Empire, and Wall Street marked America’s ascent.

In the grand epic of finance, DeFi is setting sail, carrying the torch of transformation toward a new era of financial freedom.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News