Solana Validator Business Insights: Top Validator Earns Up to $14 Million, While Over a Thousand Nodes Operate at a Loss

TechFlow Selected TechFlow Selected

Solana Validator Business Insights: Top Validator Earns Up to $14 Million, While Over a Thousand Nodes Operate at a Loss

Minimum cost of $60,000 per year, with potential negative returns.

Author: Frank, PANews

Recently, Solana has taken the lead across various metrics. Earlier, PANews published an article detailing the rapid development and landscape of its liquid staking ecosystem. Beyond these front-facing projects, Solana’s validators have remained relatively mysterious. How much can one actually earn as a validator on Solana, and what level of investment is required? PANews conducted research into this business.

Solana employs a consensus mechanism combining Proof of History (PoH) with Proof of Stake (PoS). Token holders can stake their tokens with validators of their choice. Validators with more staked tokens have a higher proportion of leadership in block production, and participants in staking receive block rewards proportionally.

Typically, validators can set commission rates for stakers between 8% and 10%. However, validators that choose not to charge commissions and maintain stable networks are generally more favored by stakers.

There are two types of nodes on Solana: validator nodes, which participate in voting and accounting, and RPC nodes. RPC nodes provide data access interfaces for developers and applications and have lower configuration requirements. However, RPC nodes do not directly participate in network validation and therefore cannot earn block rewards.

In contrast, validator nodes have high requirements for hardware bandwidth, memory, storage, and other aspects. As such, they are typically deployed in data centers around the world, making it a business largely inaccessible to ordinary users.

Minimum annual cost of $60,000

Specifically, the main costs for validators include the following items.

Hardware:

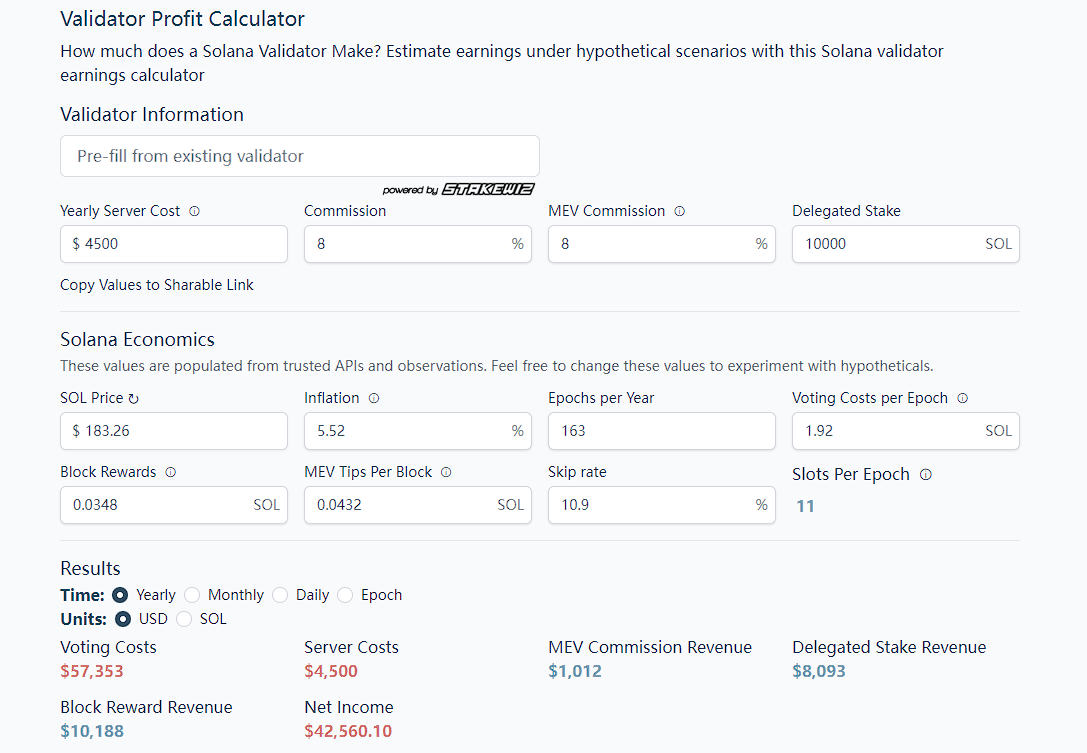

Hardware cost is one of the biggest expenses in becoming a Solana validator. According to Solana's recommended configuration—a 12-core/24-thread CPU, 256GB or 512GB of RAM, and over 1TB of disk space—this setup far exceeds typical consumer-grade computers, especially in terms of memory, where just this component typically costs over 10,000 RMB. Additionally, a stable 1GB bandwidth connection is required. Therefore, most validators opt to rent servers. According to Helius' article, server rental fees range from $370 to $470 per month, amounting to approximately $4,500–$5,600 annually.

Bandwidth costs often depend on the amount staked—the more frequently a validator leads block production, the higher the bandwidth costs.

On-chain voting:

Solana requires on-chain voting to achieve consensus. These voting transactions incur fees similar to other transactions on the network. In each epoch (432,000 slots), validators must vote, with each vote costing 0.000005 SOL (voting is a privilege without associated priority fees). This amounts to total costs of about 2–3 SOL per epoch. Given that an epoch usually spans 2 to 3 days (typically close to 2 days), the annual cost for voting transactions is approximately 300–350 SOL, equivalent to roughly 1 SOL per day. At a price of $182 per SOL, this portion of the cost ranges from $54,600 to $63,700. When SOL prices are higher, this cost often becomes one of the largest expenses.

Overall, the minimum annual cost on Solana is approximately $60,000. This level of financial commitment is substantial for average users and does not even include operational and maintenance labor costs.

Profits could be negative

Although the investment is significant, how profitable is being a validator?

Validator revenue on Solana comes from several sources: inflation rewards, block rewards, and MEV.

Inflation rewards: These are SOL token rewards given to participating validators. The initial inflation rate for SOL was set at 8%, decreasing by 15% annually thereafter. Validator inflation rewards also depend on the network-wide staking ratio—the lower the total staked percentage, the higher the validator’s staking yield. The current combined inflation reward is 5.52%. Assuming a typical validator charges an 8% commission, staking 10,000 SOL would generate approximately $8,000 in annual staking revenue.

Block rewards: Each validator has a chance to become a block leader, with the frequency depending on the amount of staked SOL. For example, with 10,000 SOL staked, a validator might be selected around 11 times per epoch (roughly every 2 days). Annual earnings from this source amount to about 52 SOL (with an average block reward of approximately 0.0332 SOL), or around $9,400.

MEV rewards: "Maximum Extractable Value" refers to profits validators gain by including, excluding, or reordering transactions within the blocks they produce. On Solana, designated leaders have full control over block construction and scheduling. Searchers can send transaction bundles via off-chain auction mechanisms to leaders for inclusion in blocks, along with tips. If a validator runs the Jito-Solana client, they can capture this value—but earnings depend on how often they are elected leader. Currently, the average MEV reward per block is about 0.0427 SOL. With the Jito client, this revenue is typically shared with stakers, and if the validator takes an 8% commission, staking 10,000 SOL yields about $970 annually from MEV.

Based on these figures, with only 10,000 SOL staked, annual costs exceed $60,000 while income is around $18,370, resulting in a loss of $41,630. It appears to be a losing proposition.

However, this loss is primarily due to insufficient staked SOL. If the staked amount increases beyond 32,300 SOL, profitability becomes achievable.

Currently, there are 2,724 validator nodes on Solana, with 857 validators holding more than 32,300 SOL staked. By this calculation, over a thousand remaining validators are operating at a loss. However, the Solana Foundation offers support programs; new validators joining the Delegation Program with less than 100,000 SOL in total stake will receive a 1:1 matching stake from the foundation. Even so, validators still need to secure at least 15,000 SOL in stake. If self-funded, this represents a capital outlay of no less than $2.73 million at current prices.

Top validator earns up to $14 million

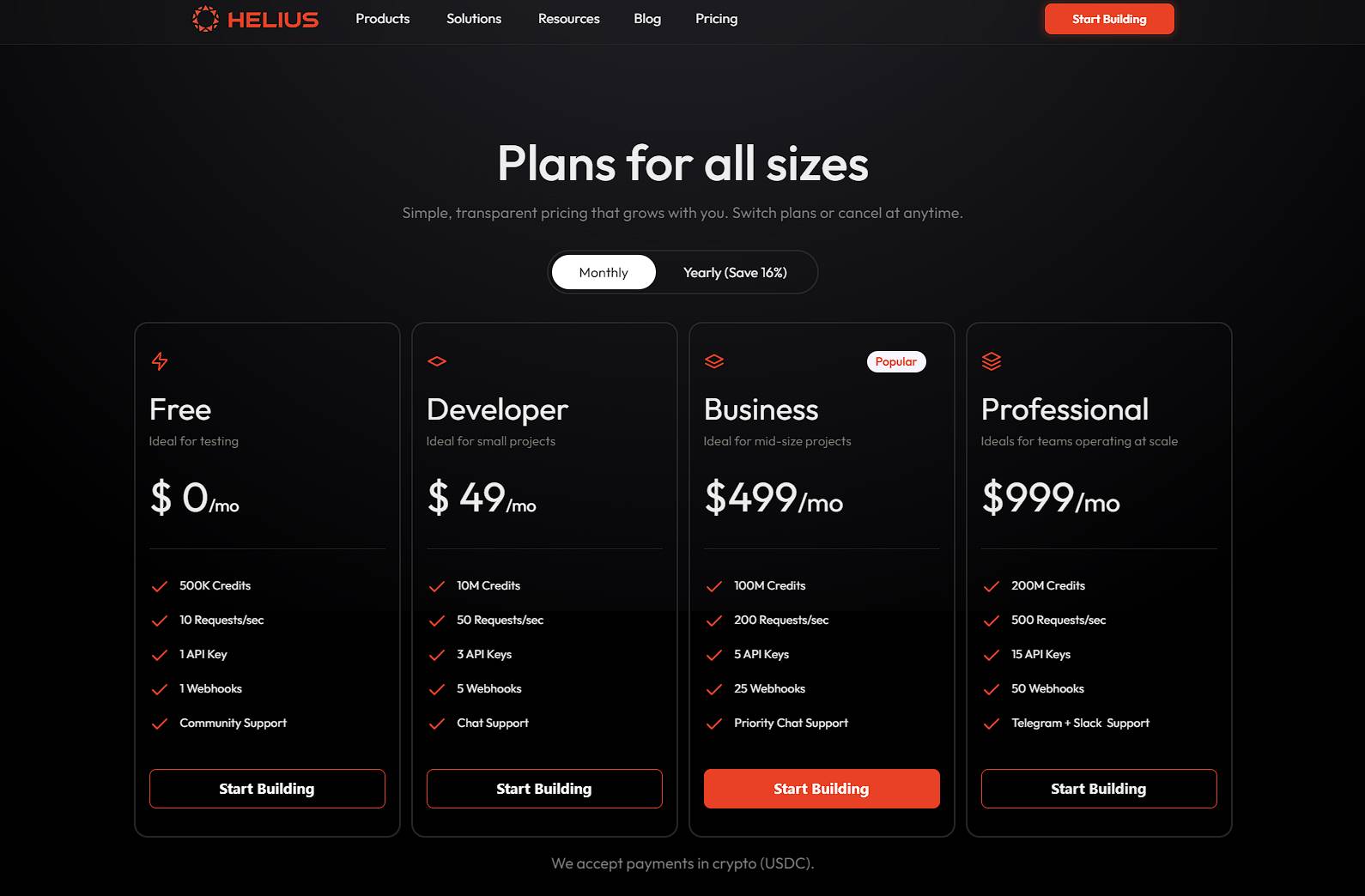

For established validators, validator income can be highly profitable. Take Helius, recently crowned the largest validator, which currently manages 13 million staked SOL. Helius charges zero commission on both inflation and MEV rewards, passing all benefits directly to stakers. Under this model, Helius’ annual block reward reaches $14.05 million. If Helius charged an 8% commission, its income would increase by another $14 million. Yet, perhaps precisely because it forgoes these fees, Helius attracts more stakers to delegate their tokens.

Moreover, large validators like Helius don’t rely solely on block rewards. Helius also generates revenue by providing RPC node services and API access. Its subscription plans range from $49 to $999 per month, making Helius one of Solana’s primary RPC service providers.

Staking alone may not yield profit

For users staking with such validators, typical annual returns range between 6% and 8%. However, these are not guaranteed stable returns. Stakers face risks such as declines in SOL price, penalties for validator downtime, and malicious actors secretly increasing commission rates to 100%. Nonetheless, data shows that approximately 65.7% of SOL tokens are currently staked—one of the highest staking ratios among public blockchains—suggesting that staking has become a collective choice among major SOL holders. Still, this strategy works mainly under expectations of rising SOL prices. If the holding cost of SOL is too high, losses during price drops can quickly erase all gains.

Overall, whether in terms of capital requirements or technical complexity, becoming a Solana validator involves certain barriers to entry. For well-connected and well-capitalized entities within the ecosystem, however, being a validator can offer relatively stable returns. Nevertheless, the high barrier raises concerns about increasing centralization and monopolization by a small group. For ordinary users, relying solely on staking and MEV revenue sharing remains an inadequate hedge against asset volatility.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News