Opinion: Why Should We Reject Hype-Driven Speculation and Defend Crypto Fundamentals?

TechFlow Selected TechFlow Selected

Opinion: Why Should We Reject Hype-Driven Speculation and Defend Crypto Fundamentals?

We are still at the beginning of one of the largest cash flow opportunities in the history of capitalism, requiring a paradigm shift toward fundamental perspectives.

Author: Felipe Montealegre (IFS)

Translation: TechFlow

I am confident about the future of our industry, but I don’t expect a bubble like the one four years ago. I believe many high-quality assets will perform well in the coming years, and I’ve allocated all my capital based on this expectation. However, there’s a strange notion in the industry that even fundamentally worthless assets should reach astronomical valuations every four years during market cycles. This happened in 2017 and 2021, leading some to assume it will repeat in 2025. I believe this mindset is flawed and is actually hindering the industry’s progress.

We can divide the industry into two paradigms—the fundamentals paradigm and the cyclical mania paradigm. The fundamentals paradigm means you believe in the long-term vision of the industry but don’t expect token prices to trade far above their intrinsic value. Under this paradigm, investors are incentivized to collaborate with strong teams to build profitable businesses, while builders focus on products, customers, and the fundamental economics of their business.

In contrast, the cyclical mania paradigm assumes that a bubble occurs every four years, so fundamentals become irrelevant. In this case, investors’ natural incentive is to time the market and invest as much as possible in narrative-driven tokens, without regard for whether teams are building for the long term.

I believe many investors still operate under the cyclical mania paradigm, which will likely leave them disappointed in the coming years, as fundamental strategies will outperform while narrative tokens may struggle. There are too many sellers and not enough buyers to recreate the conditions of 2020–2021.

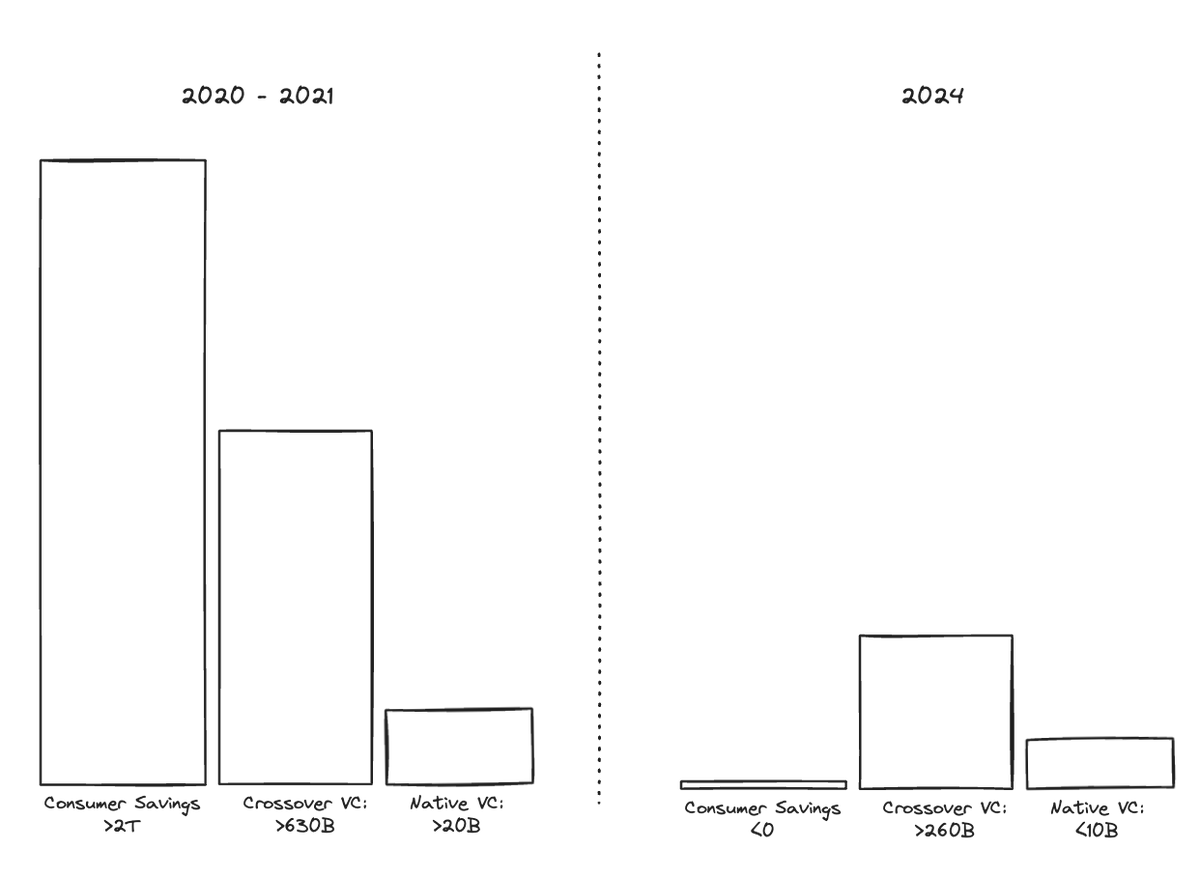

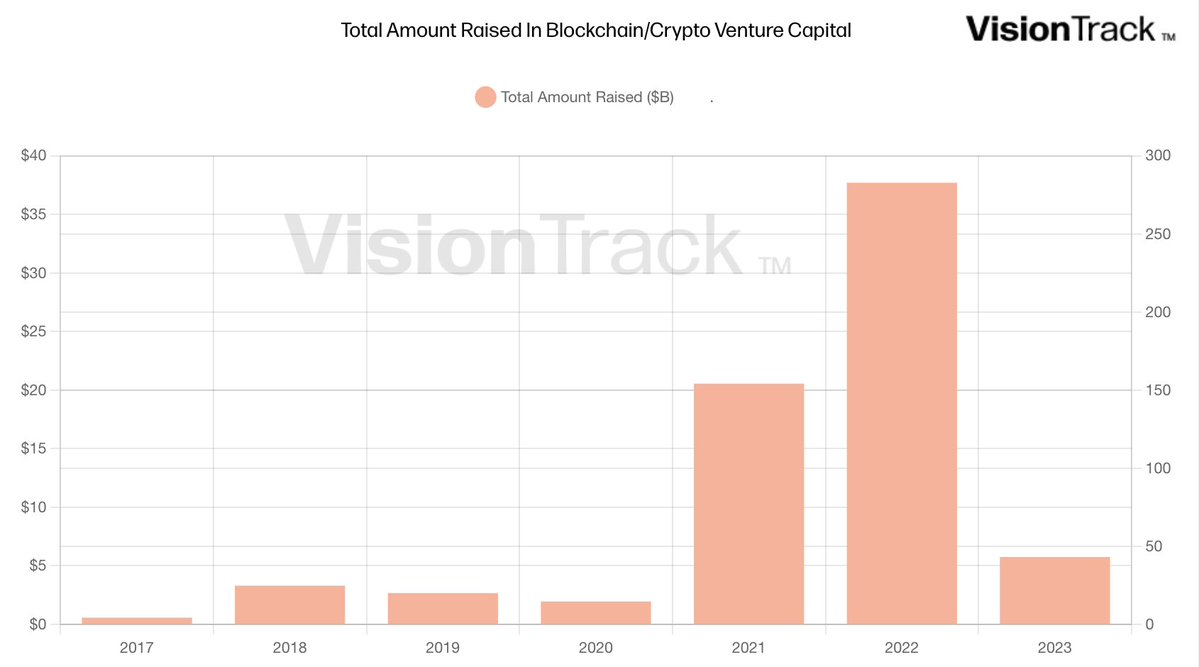

The bubble we experienced in 2021 occurred because multiple inelastic buyers met in a market with almost no supply. At that time, native venture funds raised over $20 billion in 2021 and quickly deployed that capital. Crossover funds raised $630 billion between 2020 and 2021, riding over a decade of strong performance from the tech bull market of 2010–2020, and aggressively invested in crypto.

Mainstream markets were flooded with around $815 billion in stimulus checks, and consumers were confident in the sector. Due to the rapid price appreciation of assets like BTC, ETH, and SOL, whales gained $1.5 trillion in new capital. These investors believed the industry would deliver on its promises—that on-chain finance would disrupt Goldman Sachs within a few years and that by the mid-decade, all businesses would be built on blockchains.

Faced with this demand, there were almost no sellers. Only founders and a small number of early-stage VCs held large amounts of tokens, and they couldn’t sell—partly due to lockups, partly because they believed in the story and had fresh capital to reinvest.

The market cap logic was: If 90 shares are locked up and 10 shares trade at double the previous price, the market cap assumes all shares have doubled in value. Thus, the prior bubble’s market cap surge was primarily driven by too many buyers purchasing too few tokens from a handful of sellers.

Today’s market structure is entirely different. For native funds, raising new capital has become much harder. Fundraising dropped 85% in 2023, with little recovery in 2024 (for example, Paradigm closed its 2024 fund at $800 million, compared to $2.5 billion in 2021). Crossover funds will return slowly, mainstream participation has largely vanished as consumer savings fell from over $2 trillion in 2021 to negative values in 2024. The remaining retail participants prefer investing in meme coins rather than complex infrastructure narratives or embedded venture unlocks. Whales have also shifted preferences—from narrative tokens to yield-generating core assets that made them wealthy (like BTC, ETH, and SOL). While a small amount of liquidity remains willing to buy tokens, it’s tiny relative to the overall market, and we’re unwilling to pay high valuations for low-quality assets.

Who will buy your narrative token?

There’s now a slight forced-seller dynamic in the market. In venture capital, two key performance metrics are Total Value to Paid-In (“TVPI”) and Distributions to Paid-In (“DPI”). TVPI includes both realized gains from sold assets and unrealized gains from appreciated but unsold holdings. DPI measures how much cash has been returned to investors per dollar invested.

VC funds raised before 2019 performed well on both metrics, but most returns remain unrealized. These large funds are now reaching the legal end of their life cycles, meaning they must sell remaining holdings to return capital to limited partners. Funds raised after 2019 still have ample lifespan left, but their DPI returns are minimal (often below 0.10x), and LPs now require DPI returns before allocating to follow-on funds. The industry’s largest single holders appear poised to become net sellers in the coming years.

Funds from 2021 and 2022 have incentives to sell unlocked tokens to demonstrate DPI and raise new capital.

At the end of 2023 and beginning of 2024, many investors tried to position early for another wave of mania, causing narrative token prices to rise. The problem was that most bought assets they didn’t truly believe in, hoping others would buy them at higher prices. That foolish capital never showed up—the market rejected attempts to launch a properbull runfor narrative tokens. Those buyers won’t come, and narrative tokens will continue to underperform in the coming years.

Even with strong momentum, there aren’t enough buyers to sustain a basket of narrative tokens.

We need a paradigm shift toward a fundamentals-based view. Those of us who believe in the foundational vision of an internet-native financial system understand that we’re still at the beginning of one of the largest cash flow opportunities in the history of capitalism. All you need to do is work hard and focus on fundamentals.

I hope our industry evolves post-2001 more like Silicon Valley. Over the past decades, the entire industry flourished—all rooted in hard work, product-market fit, and sound risk assessment. As markets gradually shifted toward valuations based on fundamentals and economic principles, unrealistic metrics like “price-to-clicks” and “price-to-eyeballs” lost credibility. During this process, companies like Amazon, Apple, and Google built some of the most profitable enterprises globally, and nearly everyone who worked hard and focused on fundamentals succeeded.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News