VC Coin Retreat: Cold Reflections – Who Was Right Doesn't Matter, What Matters Is Who Made Money

TechFlow Selected TechFlow Selected

VC Coin Retreat: Cold Reflections – Who Was Right Doesn't Matter, What Matters Is Who Made Money

A token's decline does not devalue the product developers are building.

Author: R48

Compiled by: TechFlow

If you’ve opened this article, you’re likely interested in tokens invested in by venture capital funds. I hope you don’t take the ideas and views expressed here as investment advice.

All risks associated with buying and selling assets are borne solely by the reader.

Disclaimer: The term “VC tokens” mentioned by the author refers to tokens with low circulating supply in the analysis, which are expected to undergo a series of unlocks that will dilute their valuation.

More precisely, they are characterized by low circulation / high fully diluted valuation (FDV).

Background

Since the beginning of this year, every average inhabitant of the crypto world has recognized its significance, as the growth season particularly incentivized exchanges preparing for 3–4 listings per week. Indeed, everything was going smoothly—until the market began to correct.

I divide the phases of greed and disappointment into two time periods:

-

Greed. November 2023 – March 2024.

-

Disappointment. March 2024 – July 2024 (we are currently in this phase, with similar sentiment).

Greed

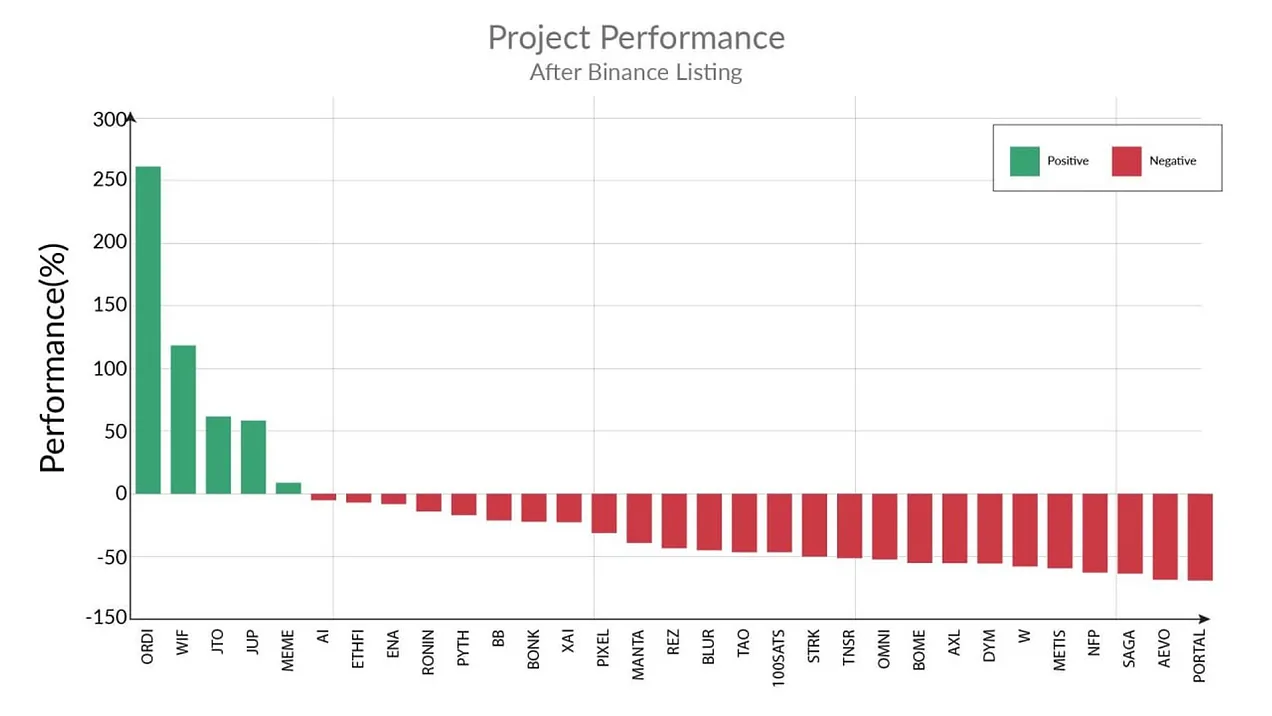

The greedy period is characterized by capital continuously flowing from one category to another, with almost all assets rising. Below are some pump-and-dump examples:

Overall positivity was driven by $BTC, which gained ETF approval in January and surged from 40k to 70k within months. Altcoins were also thriving, with newly issued tokens actively supported by speculators and investors who rushed to buy every token available.

What the market lacked during this period was liquidity. Capital was so limited that when one ecosystem grew, another remained lifeless—and once the first reached its peak, liquidity would shift to the next, creating a cycle.

ETH → Sol → Avax or Sui

In terms of categories, choices were limited:

L2 → AI → BTC-fi (and BRC-20) → Game-fi → Meme

While it can’t be called strictly cyclical, it’s certain that each category showed growth over these six months.

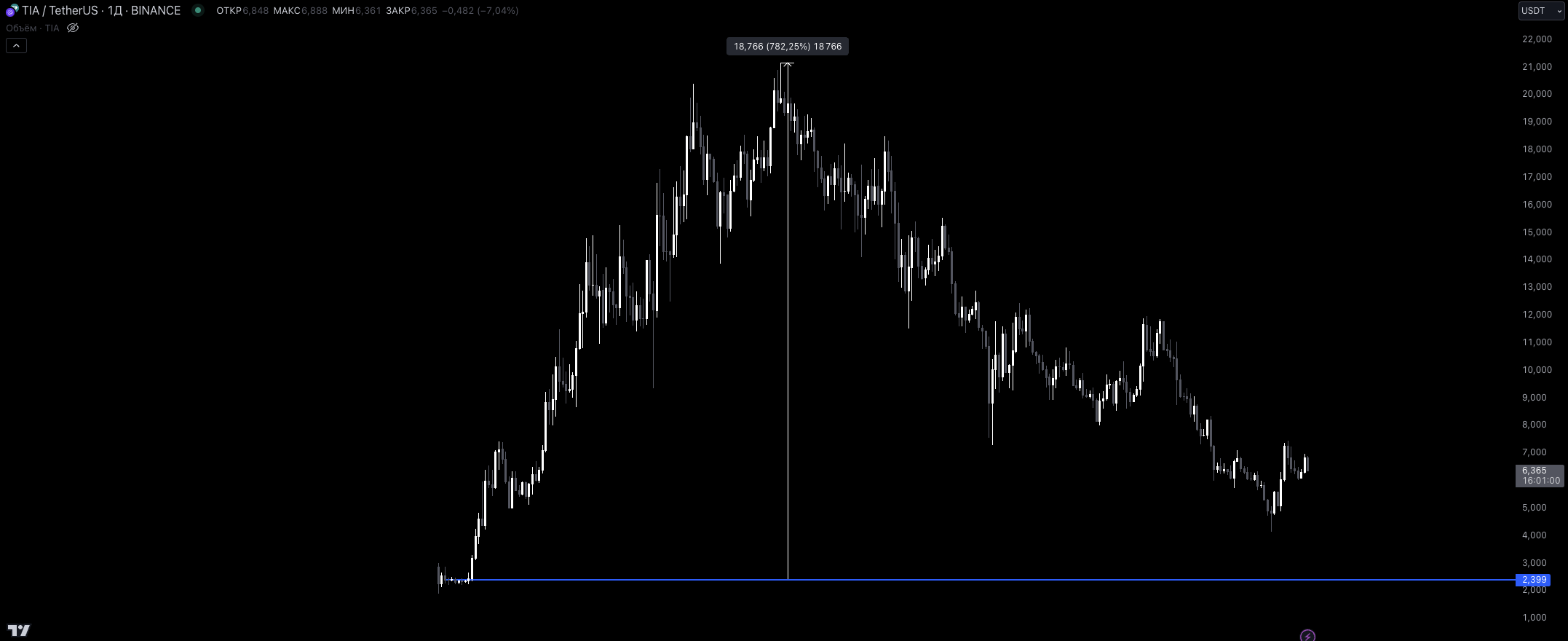

There were no negative tweets about FDV-related metrics—for example, $TIA. It listed on Binance with a market cap of $200 million while having an FDV of $2 billion.

$TIA l 1D l Price performance

Market makers took full advantage of this; selling such charts to communities wasn't hard. So let's summarize:

— Greed

— Low liquidity

— Performance across major categories (the well-known ones)

Disappointment

The disappointment phase gradually began in February with the surge of $PEPE. At the time, the market was experiencing its second meme season, even more intense than the previous one. Although Binance listings were still relatively strong, new token gains dropped from 200%-300% to just 50%-100%. The idea of buying new "cheap" tokens remained viable, but interest in them started to wane.

The first signal of market overheating came with the launch of Starknet ($STRK), an L2 solution, where significant skepticism emerged regarding the prospects of a token ranked among the top 15 in crypto by FDV. This raised a simple question: "Where can it possibly go from here?"

Source: Viktor’s channel

When the market became chaotic, $BTC decided to test the strength of the new wave of altcoins—and the result was... disastrous. Bitcoin dropped around 15%, while high-tech tokens plummeted 30%-40%.

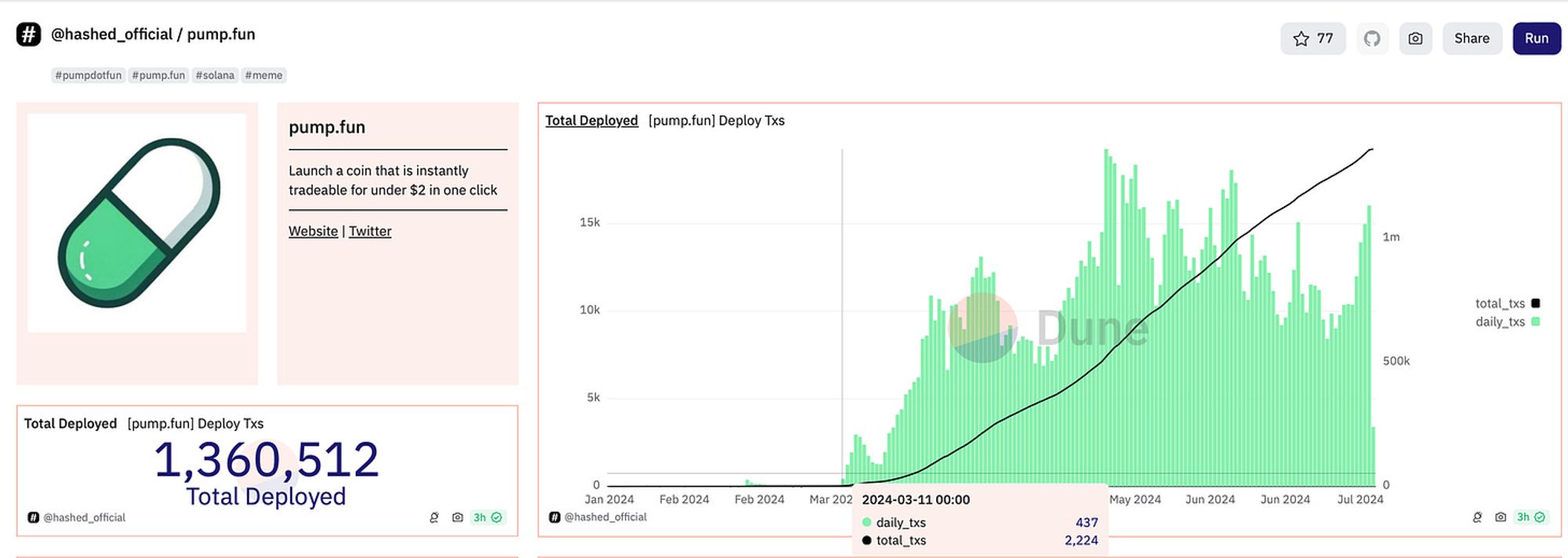

The first sign of weakness in the altcoin market forced users to seek alternatives—and they found them in memes. In my view, the revival of the meme season began on March 11, 2024, when metrics on pump.fun started growing exponentially. The outcome of this growth was the successful launch of new meme categories such as:

WIF, BOME, MEW, MICHI, BRETT, BONK (in no particular order).

Source: Dune

Crypto traders (CTs) clearly observed capital accumulating in memes and holding strong during declines in Bitcoin and Ethereum. This led to a conclusion: “Where attention and money flow, the highest returns follow.”

Moreover, impressive results achieved by speculators provided additional support to memes. Weighing each factor and observing the strong rise of memes in the first half of the year, we now see that every major global event gets memefied on the Solana blockchain.

As for tokens funded by venture capital funds, the situation could be described as outright terrible. Crypto traders arrived at this conclusion for several reasons:

-

Concerning market cap/FDV ratio.

-

Poor tokenomics (small cliffs, high emissions).

-

High profits for VCs (assume a startup raises at a $50M FDV but enters the market at $1B—a 20x pure profit for average secondary exchange projects).

-

Market pressure from airdrop recipients (immediate selling after receiving tokens).

So what do we end up with?

Tokens severely diluted in value, massive multiples for funds, minimal circulating supply (subsequent unlocks will destroy prices), and huge FDVs.

This situation is worsened by the sheer number of such tokens. Each project promotes itself as the ultimate solution to N problems in crypto. Last fall, this worked because:

-

Liquidity wasn’t diluted by memes.

-

Projects weren’t queuing up for launches but waiting for better conditions.

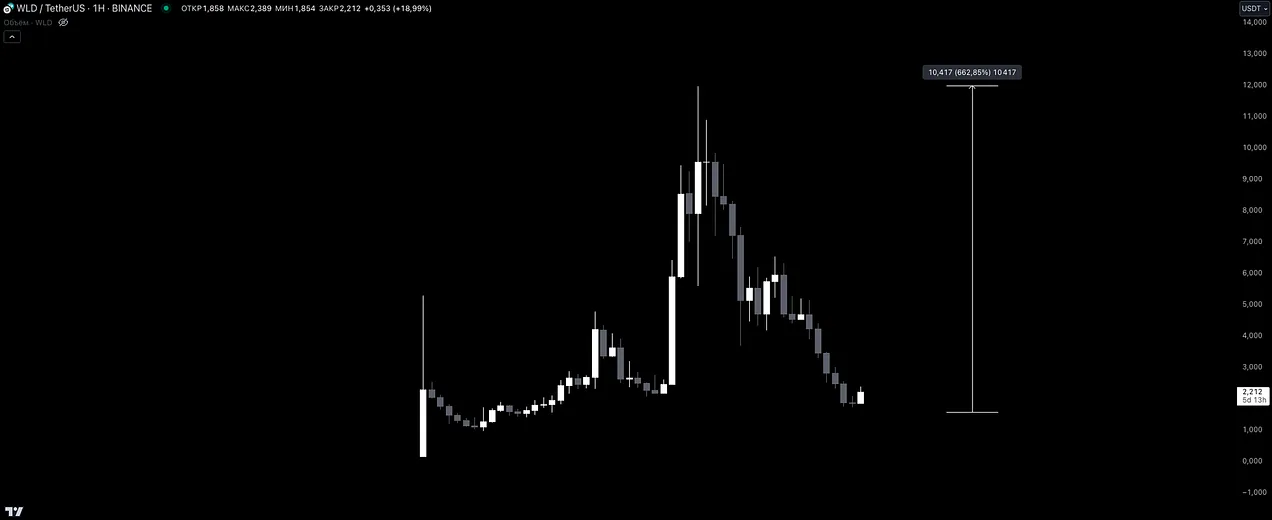

Contempt for “VC tokens” peaked with the rise of Worldcoin ($WLD), which market makers had been accumulating since its listing. Worldcoin is a project led personally by Sam Altman, who heads OpenAI (the company behind ChatGPT). Crypto traders treated $WLD as a proxy bet on OpenAI’s growth, trying to leverage every new update in their trading strategies.

“ChatGPT gets a new update? $WLD takes off.”

Example of fear, uncertainty, and doubt (FUD) around Worldcoin, source

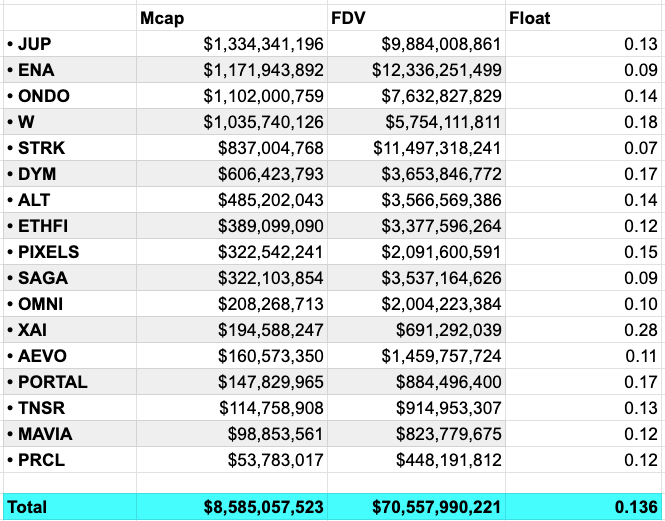

With only 1.14% of tokens in circulation, ideal conditions were created for market manipulation.

Source: Viktor’s TG channel

On paper, $WLD is currently among the top ten crypto assets.

The argument against VC-backed tokens solidified in April when the altcoin market entered a second stage of aggressive sell-off, and a direct clash occurred between developers/Venture Capitals and the forces behind memes. While I can’t say definitively who won, the user influx into pump.fun suggests traders and speculators prefer memes over dull infrastructure. Furthermore, price dynamics for recently listed tokens were dismal, with almost no one willing to buy anything.

Source: X

Summary:

-

Crypto trader (CT) behavior during the Greed phase:

a. FDV doesn’t matter; hype around the project and the initial circulating supply upon launch matter (the lower, the easier to pump).

b. A new token fitting the current narrative (btc-fi, ai, game-fi, social-fi...) is attractive regardless of its tokenomics (consider Shrapnel).

c. Preference for speculation over balanced analysis.

-

Crypto trader (CT) behavior during the Disappointment phase:

a. Listed tokens aren’t profitable; search for alternatives, found in memes because all listed tokens are traded and 100% community-owned coughs conspicuously.

b. Look for catalysts favoring the meme sector (low FDV / low circulation).

c. Disappointment with infrastructure tokens isn’t due to technical complexity but lack of liquidity. Things that fall are hard to sell to the community.

This provides the general backdrop of the past 7–8 months. My main question is: “How strong is the argument that new tokens won’t recover and show performance?”

What happened in the last cycle?

For a robust analysis, I believe we need to look back at history and assess the overall context of altcoin development. The more data I gather, the richer the article becomes.

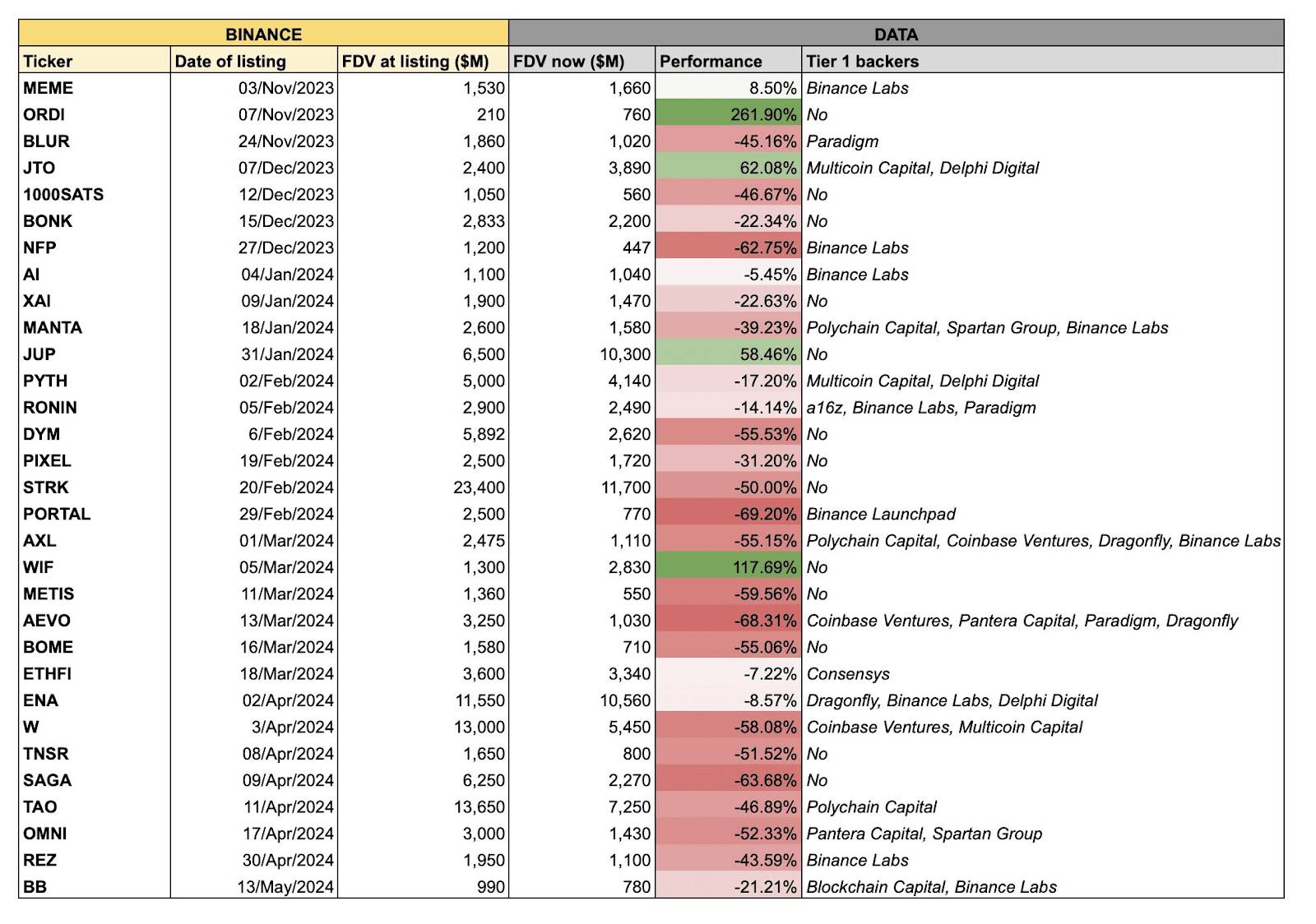

Listings

I often hear the claim: “Binance is listing many projects now, significantly diluting liquidity, which didn’t exist before.”

Initially, I thought this argument made sense and required no further analysis.

However, I decided to independently analyze the number of tokens Binance brought to market—and the result surprised me.

Created by ChatGPT

Preliminary calculations allow for a possible deviation of 2–3 points in either direction, which is acceptable accuracy.

After reflection, I concluded that the above argument stems from authors remembering only 5–10 projects that survived the bear market and performed well.

Yet in reality, numerous projects launched, got hyped, then shriveled. Due to short token lifecycles, memories fade over time—this is known as “survivorship bias”—while those achieving product-market fit (PMF) and sustained demand remain memorable.

Try this: which tokens from 2020–2021 do you remember? For me, SOL, AVAX, FTM, UNI, LDO come to mind. But in fact, there were ten times more tokens; most either failed to achieve PMF or quickly collapsed.

Based on this, we cannot claim the previous cycle consisted of just N successful projects.

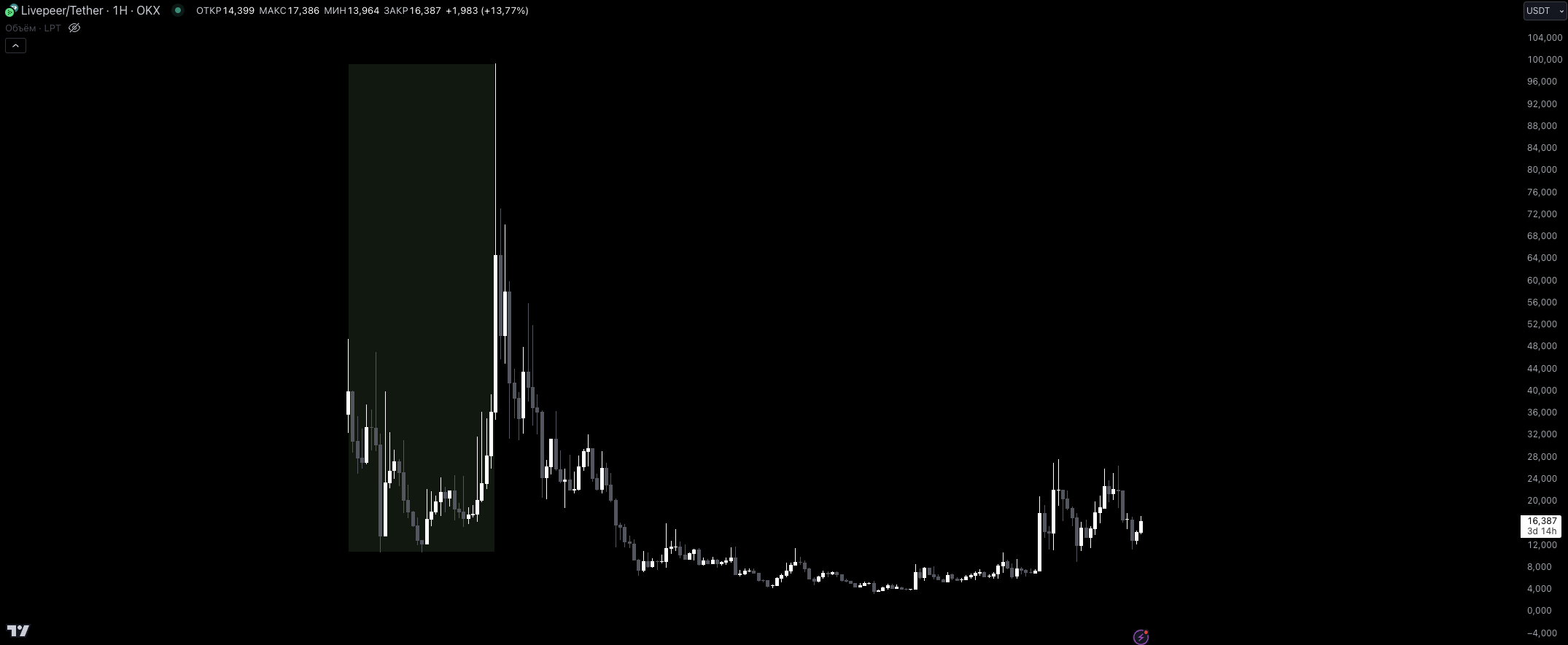

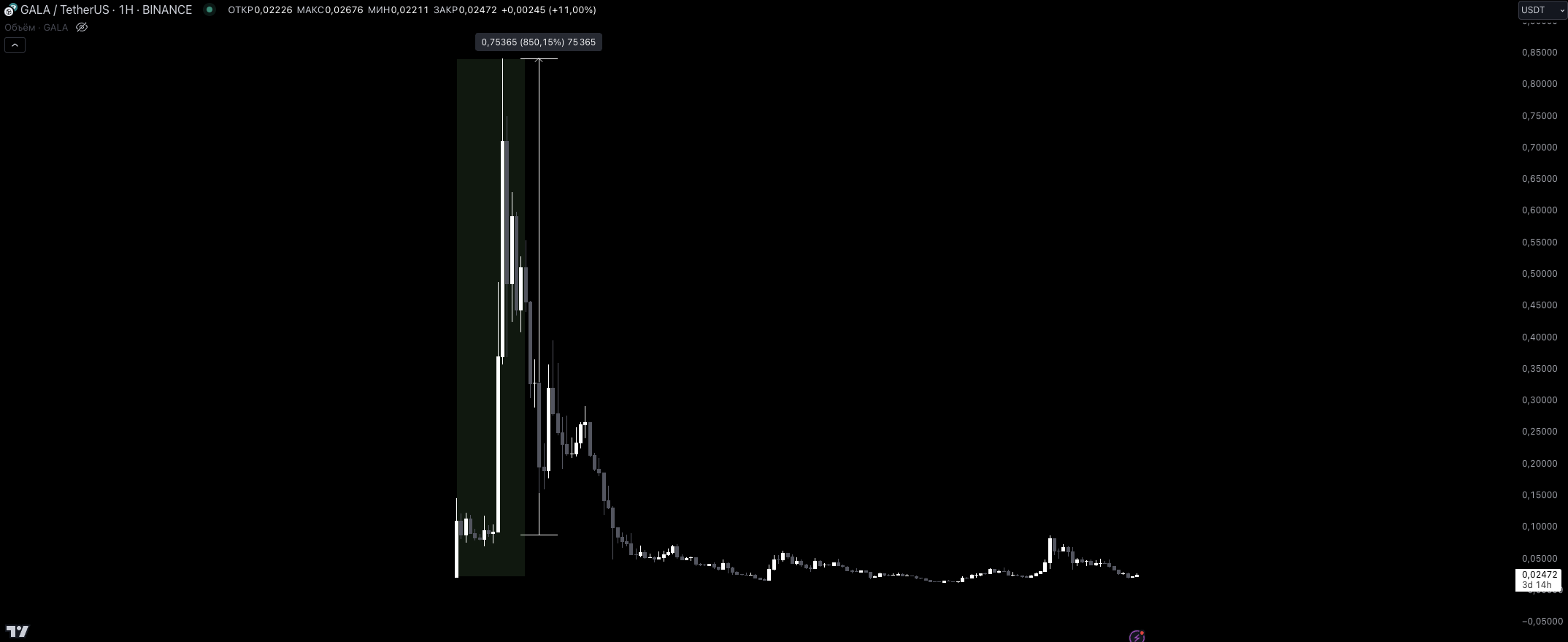

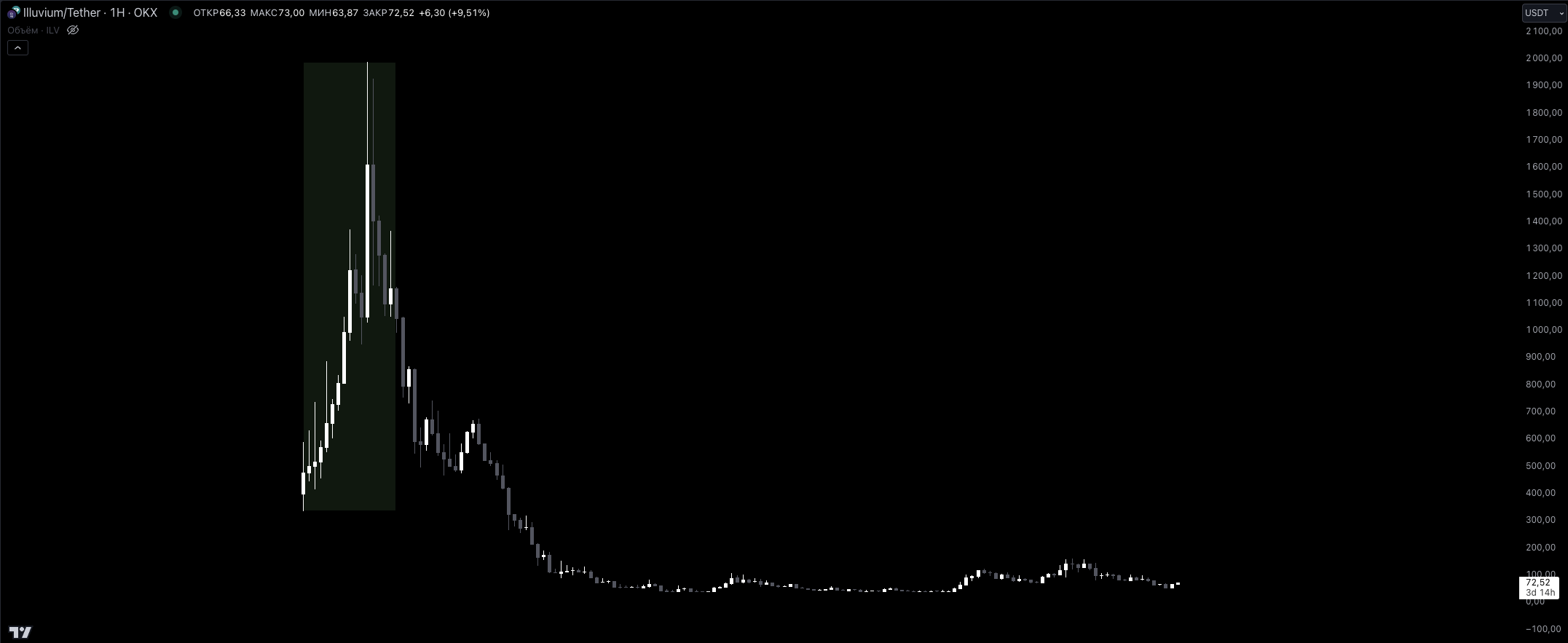

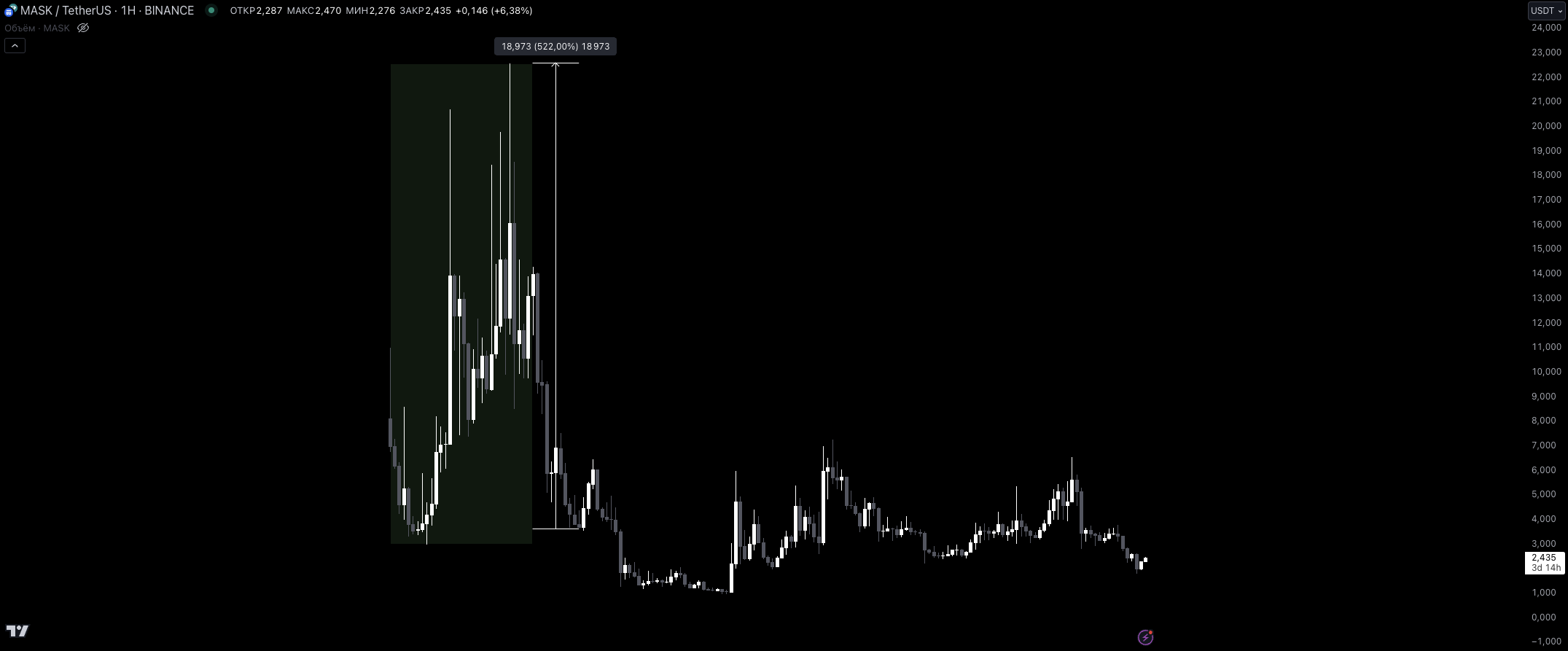

Here are some examples of tokens from the last cycle:

More examples below:

-

$ALICE, $SKL, $ROSE, $AKRO, $AUDIO, $ORN, $ILV, $MASK.

You can check the charts of these projects yourself.

Let me ask you: have you heard of these projects? Are you currently using any of them?

Bear markets tend to eliminate weak products or tokens with poor tokenomics, but every token gets a chance to prove itself during bull runs. Among these projects, some were infrastructure, others applications.

You might wonder—what about the number of tokens in the market?

These projects received strong VC backing, and their low circulation / high FDV was evident at launch. Yet this did not prevent them from showing multiplicative growth as investors and teams unlocked tokens starting from TGE (token generation event).

Conclusion

-

Low circulation / high FDV is part of the lifecycle of any altcoin during its search for product-market fit (PMF). One improvement in today’s market is that most investors face a one-year cliff followed by a two-year vesting period.

-

Survivorship bias of projects is not a valid argument compared to those that failed to reach PMF.

-

Comparing post-listing performances leads to a simple conclusion: Binance has become more cautious with projects (though ineffective from March to July), listing tier-2 projects and, of course, those incubated internally.

Where are we now, and what happens next?

First, I want to emphasize that in the cycle of new tokens, we haven’t deviated from the path by even 1%. Here are some comparisons:

-

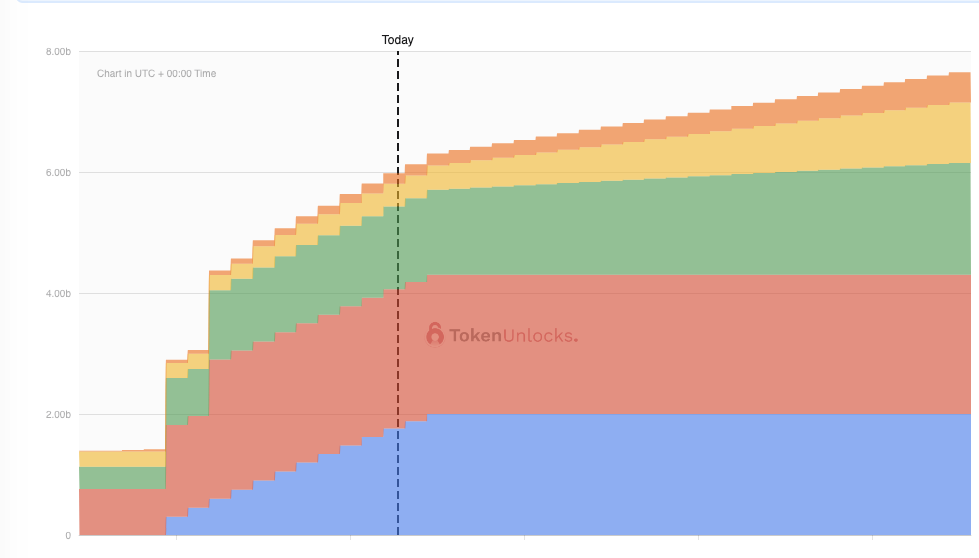

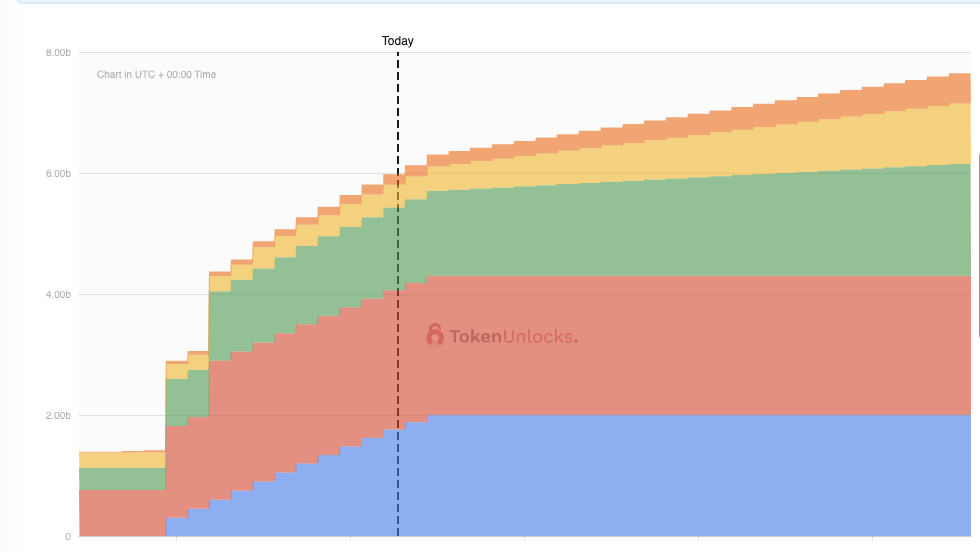

$UNI, -50% and -79%. See TradingView chart.

-

$SOL, -68% and -79%. See TradingView chart.

-

$NEAR, -59%. See TradingView chart.

-

Price performance since TGE.

Based on these charts, was buying $UNI at a ~50% drop a bad idea? Or buying $SOL down ~70%?

Argument: A token’s decline does not devalue the product being built by developers.

In my view, tokens are a necessary tool for attracting attention. Product growth in crypto occurs through several channels:

-

Token price increases. The community begins questioning whether the token’s rise relates to product uniqueness. What narrative drives the token?

-

Potential retroactive reward campaigns.

-

Referrals = product promotion by influencers (important). Again, must include monetization elements.

In weaker market conditions, short-term declines are normal—for both weak and strong projects alike.

About current projects?

I want to clarify that I may be wrong—it’s normal. There will always be projects launched purely to cash out (e.g., $SAGA, without a single line of blockchain code). Therefore, before determining future price movements of new tokens, I’d like to add some filters:

-

Simple, clear product for ordinary (app) users.

-

Broad user base; app doesn’t depend on the token.

-

Strong team, ecosystem, investors.

-

Token aligned with narrative.

I’m not saying every token released in 2023–2024 will perform strongly. Though possible under high market liquidity, I dislike spreading funds across boring and complex protocols (made mistakes before overestimating projects like $NGL, $MASA, and other junk).

Let’s assume a list of tokens and briefly analyze them:

-

ZRO (LayerZero) — Infrastructure for transferring funds between blockchains. Cheap, fast, efficient. Brian earned >$50M in two years of protocol operation—without a token.

-

$ZK (zkSync) — An L2 solution designed to scale the Ethereum ecosystem. zk technology ensures secure and fast transactions. For detailed info on zk, refer here, and see Vitalik’s thoughts. Top-tier team and ecosystem—you can evaluate metrics here.

-

$OP (Optimism) — Also an L2, but using a different transaction processing method (optimistic rollups). Based on OpStack, the Coinbase team launched their own L2 blockchain—Base—which currently ranks among the top three launched rollups.

Some may argue these tokens are useless, lack utility, and nobody needs them. But the 2020–2021 cycle shows none of that matters—until greed gives way to disappointment. Conversely, I’d say we haven’t even reached greed yet. In my humble opinion, the autumn-spring 2023–2024 scenario was merely the beginning.

Let this tweet support my point:

Here are some TA (technical analysis) considerations:

-

German coin shortage

-

Mt. Gox repayments ongoing

-

FTX repaying $16B to crypto users

-

70% probability of pro-crypto president elected

-

VP is a pro-crypto millennial

-

Global liquidity cycle just beginning

-

Inflation cooling rapidly

-

Rate cuts in September nearly certain

-

Stock markets continuing upward

-

AI speculation driving broad economic bull run

-

BTC ETF becoming the most successful ETF ever

-

ETH ETF launching next week

-

Trump speaking at Bitcoin conference next week

-

Solana ETF application pending

-

Larry Fink promoting Bitcoin as “digital gold”

-

Crypto becoming a bipartisan issue

Source: X

I don’t know how much my portfolio—or yours—will grow. The purpose of this article is to conduct a comparative analysis of altcoins in this cycle versus past cycles, and also to analyze meme coin trends.

To me, who is right doesn’t matter—what matters is who made money, and who didn’t.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News