Meme "Devours" the Market, VC Projects Fall Out of Favor — Where Is the Market Headed Next?

TechFlow Selected TechFlow Selected

Meme "Devours" the Market, VC Projects Fall Out of Favor — Where Is the Market Headed Next?

The "polar extremes" of VC tokens.

Author: Terry

Memecoin or VC Token— which would you choose?

Before 2022, most people would have unhesitatingly chosen high-profile projects backed by well-known venture capital firms—high visibility, high valuation, and seemingly guaranteed success. Yet in just two short years, the tide has turned. Particularly since the emergence of Ordinals in 2023, a small trend quickly evolved into a powerful anti-VC wave across the crypto space.

Since the beginning of this year, Memecoins have consistently outperformed VC Tokens in market performance, rapidly attracting massive attention and capital inflows. The growing public demand for fairness behind these movements is becoming a clear trend. But beneath this phenomenon, are investors truly voting with their money, or is it merely a short-term illusion within the market?

The “Hot-and-Cold” Reality of VC Tokens

The first half of 2024 was essentially a concentrated vesting period for a series of once "legendary" star projects. From Wormhole to Polyhedra Network, from Starknet to LayerZero, and then Zksync to Blast—all were highly anticipated airdrop events long awaited by community members and bounty hunters alike.

However, their post-launch price performances have been disappointing. Especially after airdrops became industrialized, the massive number of community users and farming studios helped these star projects achieve impressive on-chain metrics, driving up valuations, while the ever-inflating FDVs due to VC funding laid the groundwork for significant early liquidity sell-offs.

Take W (Wormhole), ZK, ZRO, STRK—recently launched VC-backed tokens—that can only be described as disastrous: extremely high FDVs coupled with continuously declining prices, nearly closing red every day since listing, leaving almost all retail buyers trapped in deep losses.

Based solely on late June statistics (before recent further declines), PORTAL and SAGA had already dropped about 80% from their opening prices, while W, ZKJ, STRK, OMNI, and ALT had all fallen more than 50%.

Source: @terryroom2014 / X

From a data perspective, for ordinary users, the era where shiny VC Tokens meant “buy and instantly reap high returns” has clearly ended.

At least for recent new tokens, buying on secondary markets may now be cheaper than later-stage private valuations—showing early signs of inverted valuations between primary and secondary markets:

As of July 10’s latest figures:

-

ZRO raised $3 billion cumulatively in funding history; current market cap stands at only $3.8 billion;

-

W raised $2.5 billion cumulatively; current market cap is $2.9 billion;

-

ZK raised $1.25 billion cumulatively; current market cap is $3.1 billion;

-

ZKJ raised $1 billion cumulatively; current market cap is $1.2 billion.

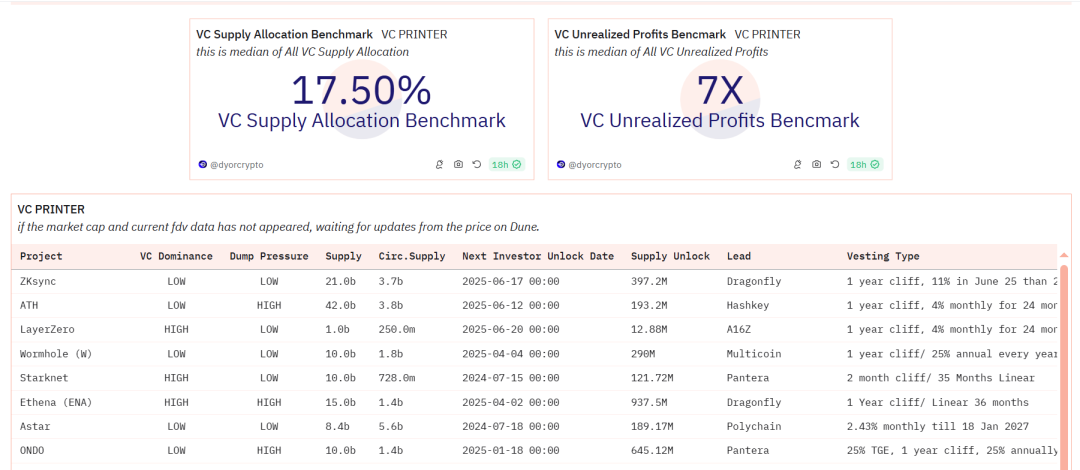

Interestingly, Dune analytics show that despite ongoing market downturns, major VCs still hold paper gains of tens or even nearly a hundred times on these tokens, with overall unrealized profits for VCs remaining as high as 7x.

Source: dune.com

Source: dune.com

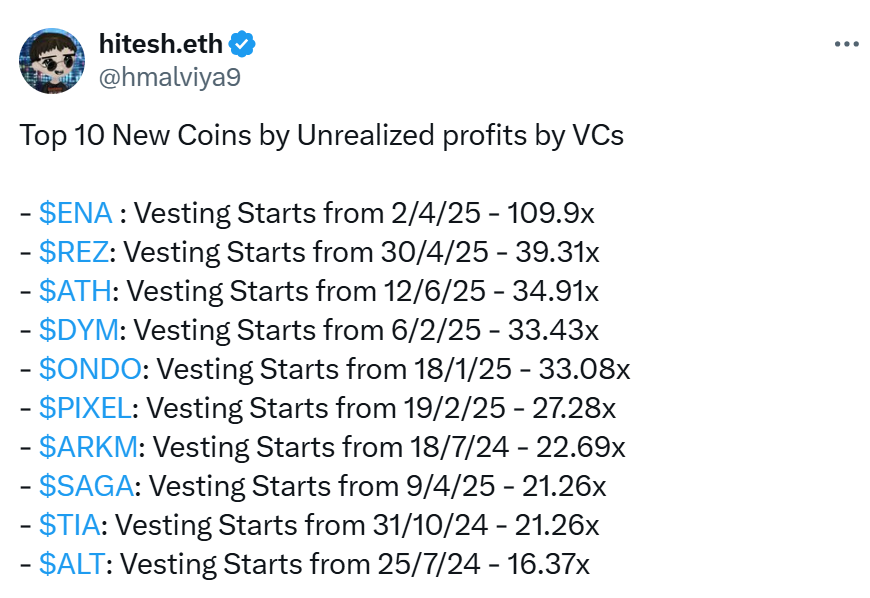

DYOR co-founder hitesh.eth also compiled the top 10 “VC Tokens” by overall VC return rate currently on the market—most of which are exactly the ones leading the downward spiral today, significantly shaking market confidence.

Yet simultaneously, assets like ENA, DYM, and SAGA, while devastating for secondary-market investors, still allow VCs to lock in over 10x profits—ENA reaching nearly 100x returns, and even the lowest, ALT, delivering over 10x. The experience gap between VCs and retail investors could not be more extreme—truly a tale of “fire and ice.”

Memecoins “Devouring” the Market

In contrast to the relentless decline of star VC Tokens listed on exchanges, Memecoins and other on-chain assets have surged ahead in secondary market performance, almost “devouring” the entire market and emerging as the cultural symbol of Web3 at this stage.

Whether it’s rising Memecoin leaders like PEPE and FLOKI, or GME and other new chain-specific Memecoins, multi-fold and even tens-of-fold wealth opportunities keep emerging, briefly evoking memories of the DeFi Summer market environment of 2020.

Especially since April this year, as newly launched star VC Tokens showed reduced volatility, making it harder for traders to profit, FUD around VC Tokens intensified. Meanwhile, Memecoins displayed unique appeal, drawing massive attention and capital through strong community consensus.

In comparison, despite strong institutional backing, VC Tokens have failed to meet investor expectations amid rapid market changes.

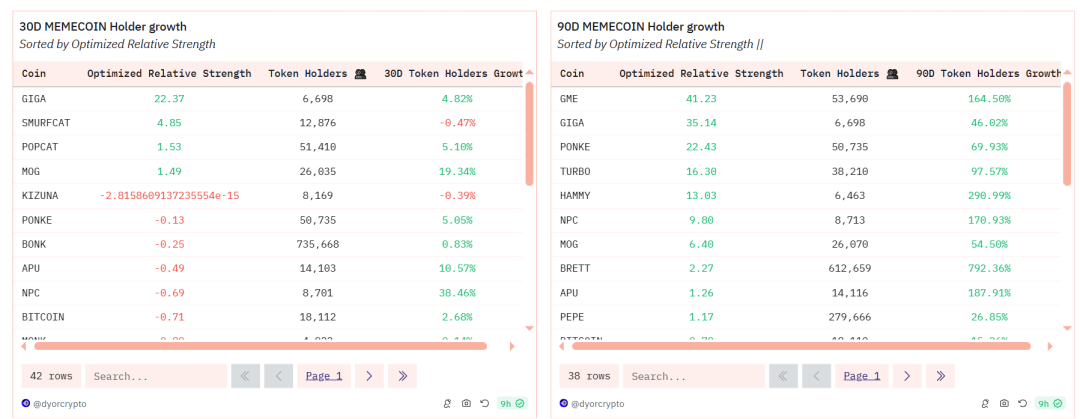

Source: dune.com

More interestingly, Dune data also shows that during this Meme supercycle, the actual number of on-chain holders among the top 46 Memecoins has clearly grown over the past 90 days:

Out of 46 Memecoins, only four showed declining trends (with FLOKI barely down), while the remaining 42 saw widespread double-digit growth—even exceeding 100% increases—in their number of on-chain holders. This data undoubtedly reflects the surging interest and participation in these Memecoins.

Moreover, the buyer-to-seller ratio over the past 30 days has mostly remained above 1, indicating relatively optimistic investor sentiment toward Memecoin price trajectories and willingness to commit more capital for potential returns.

In short, unlike earlier high-barrier crypto projects dominated by large financings and VCs—primarily targeting crypto OGs and whales (wealthy elites)—Memecoins offer broader access to the general public beyond OGs and whales, enabling fair participation and shared benefits.

Thus, when compared directly, debates and skepticism around Memecoins versus VC models inevitably resurface as mainstream discourse. At minimum, Memecoins continue to bring sustained incremental capital and attention via user momentum, whereas recent new projects valued at billions often repack old concepts with grand narratives, naturally earning community disdain.

The Community Rebellion Behind the Meme Wave

If we carefully examine the current market environment, beyond short-term speculation, the public's call for fairness represented by Memecoins is increasingly becoming a trend—capital is voting with its feet.

Put simply, the rise of the Meme wave represents, to some extent, a market and community correction against the traditional “fundraise–exit” model of the past two years: the playbook where star projects gather top-tier VCs, use sophisticated technical narratives to justify high valuations and large funding rounds, then attract communities to generate attractive on-chain metrics via so-called “airdrops”—this model is essentially exhausted.

Especially this year, controversies such as “Sybil attacks” and “insider trading” surrounding highly anticipated projects like ZKsync and LayerZero have signaled that the Web3 world is gradually entering a “post-airdrop era.” When project teams begin treating airdrops as an arrogant exercise of power in resource allocation, airdrops cease to be a mutual win between communities and founders.

Precisely because of this, the rise of Memecoins stems from their freedom from the traditional primary-secondary market handover rules. While this also implies higher risk and more volatile prices, at least it gives ordinary users another choice.

If we delve deeper into the reasons behind the shifting dynamics between Memecoins and VC Tokens, the objective market conditions are plainly visible:

-

First, selling pressure caused by high valuations and low circulating supply. Today’s star projects almost universally launch with high FDVs and low actual circulating supplies, creating inherent instability and prolonged sell-off cycles that place immense pressure on the market;

-

Second, users are becoming desensitized to technical narratives. After experiencing numerous projects—especially star ones—overhyping innovations from L2s to Restaking, users have grown more rational and cautious, no longer easily swayed by complex-sounding but substantively shallow technological claims;

-

Third, the high-frequency capital drain effect cannot be ignored. Similar to IPOs draining capital in traditional stock markets, there has been growing debate in the community about whether the密集 launch of star projects is siphoning off substantial capital, severely impacting overall market liquidity;

-

After all, real capital moving with intent doesn’t lie.

To some degree, the entrenched alliances and利益 consolidation among VCs and projects in the crypto and Web3 space have reached a point that clearly demands disruption. Meanwhile, users’ organic pursuit of real profit opportunities and trending assets is entirely understandable.

In this market full of temptation and opportunity, users naturally gravitate toward opportunities that deliver tangible returns and follow hot trends. When existing projects fail to meet these needs, they express dissatisfaction and resistance in various ways, seeking better investment returns and a healthier market environment.

This serves as a wake-up call for VCs and project teams accustomed to path dependency.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News