Stablecoins are essentially banking as a service, and their potential uses have yet to be truly explored.

TechFlow Selected TechFlow Selected

Stablecoins are essentially banking as a service, and their potential uses have yet to be truly explored.

Although the form of stablecoins is unlikely to change significantly, their utility has yet to be fully explored.

Author: Jack Chong

Translation: TechFlow

Stablecoins are an internet-native form of monetary liability — they represent the new generation of Banking as a Service (BaaS).

The form (assets) of stablecoins will not change; we're only beginning to explore their utility. Below are some mental models for predicting the future of stablecoins:

Stablecoins Are the New Generation of Banking as a Service (BaaS)

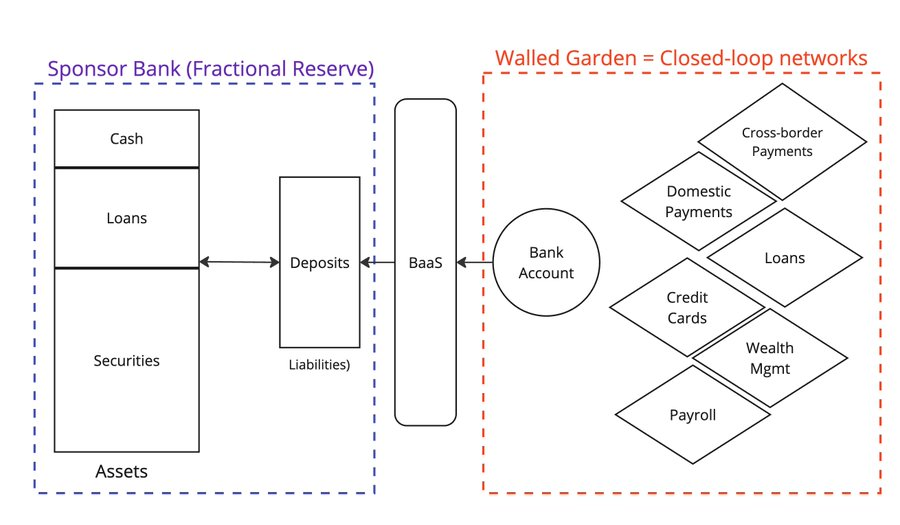

In Web2 fintech, a wave of startups offered Banking as a Service (BaaS), enabling new applications to be built on top of them.

These BaaS companies act as middleware, simplifying the complexity of interacting with traditional banks. Companies like @Venmo, @wise, @CashApp, and @Affirm have all benefited from BaaS, launching new product categories such as peer-to-peer payments, buy-now-pay-later (BNPL), and cross-border payments.

All account holders deposit their funds into fractional-reserve banks, bearing the risk that the bank may fail. But the collapse of Silicon Valley Bank reminds us that nothing is absolutely certain.

Unfortunately, one of the leading players, Synapse, has already gone bankrupt, causing significant disruption to its customers and partners.

And Evolve Bank, one of the major sponsor banks, suffered a massive data breach after being attacked by Russian hackers.

So what's the alternative to Banking as a Service? If BaaS powered Fintech 2.0, stablecoins are now enabling Fintech 3.0.

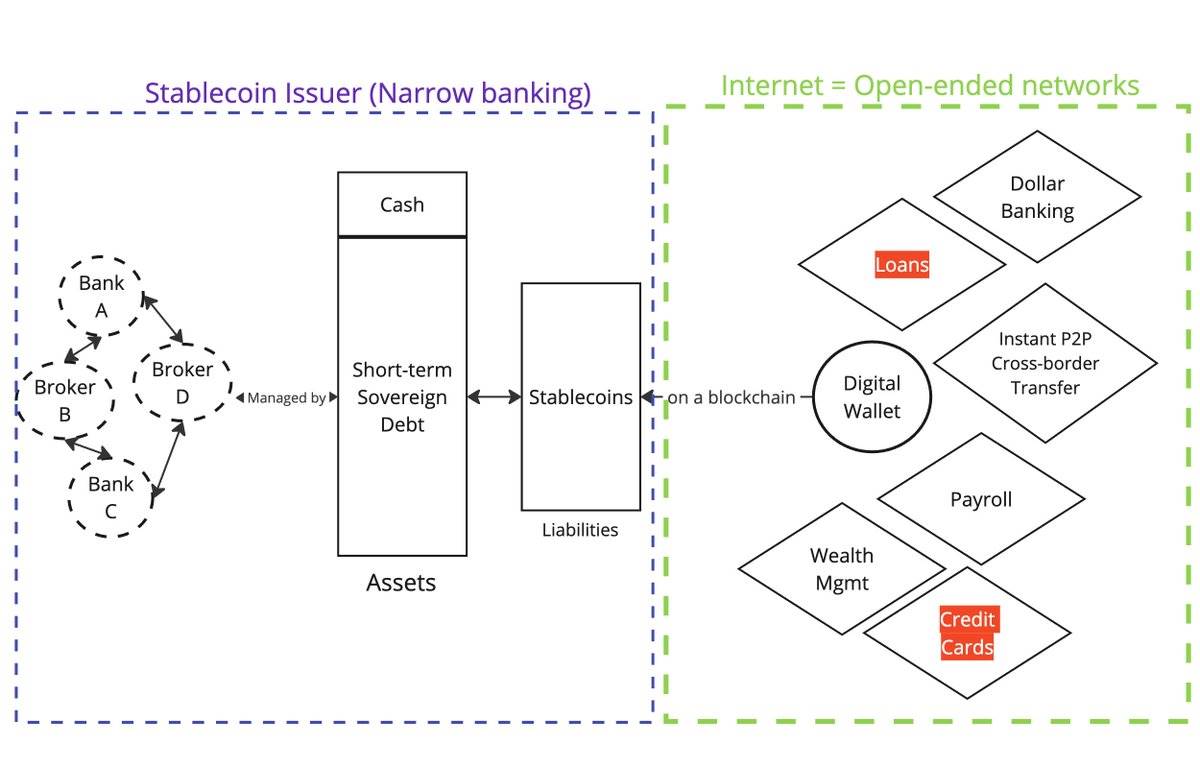

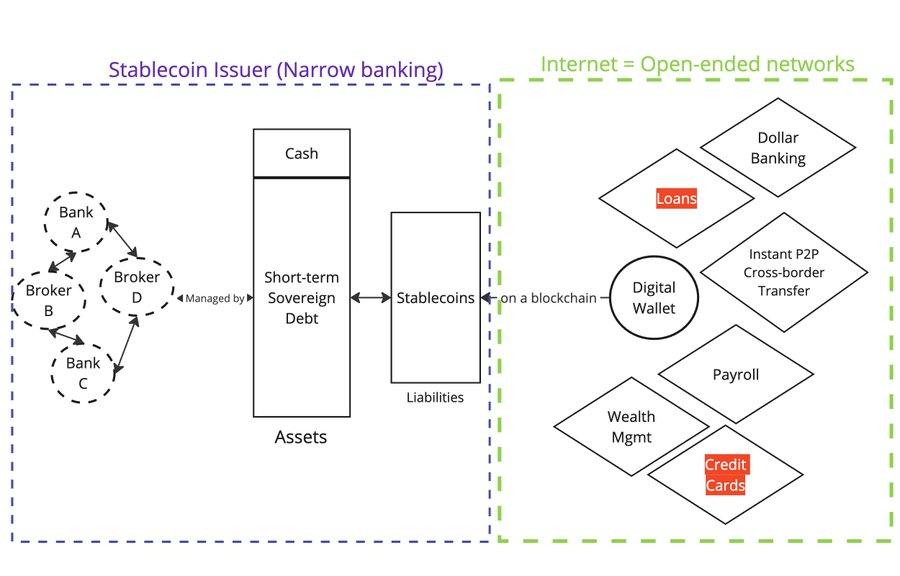

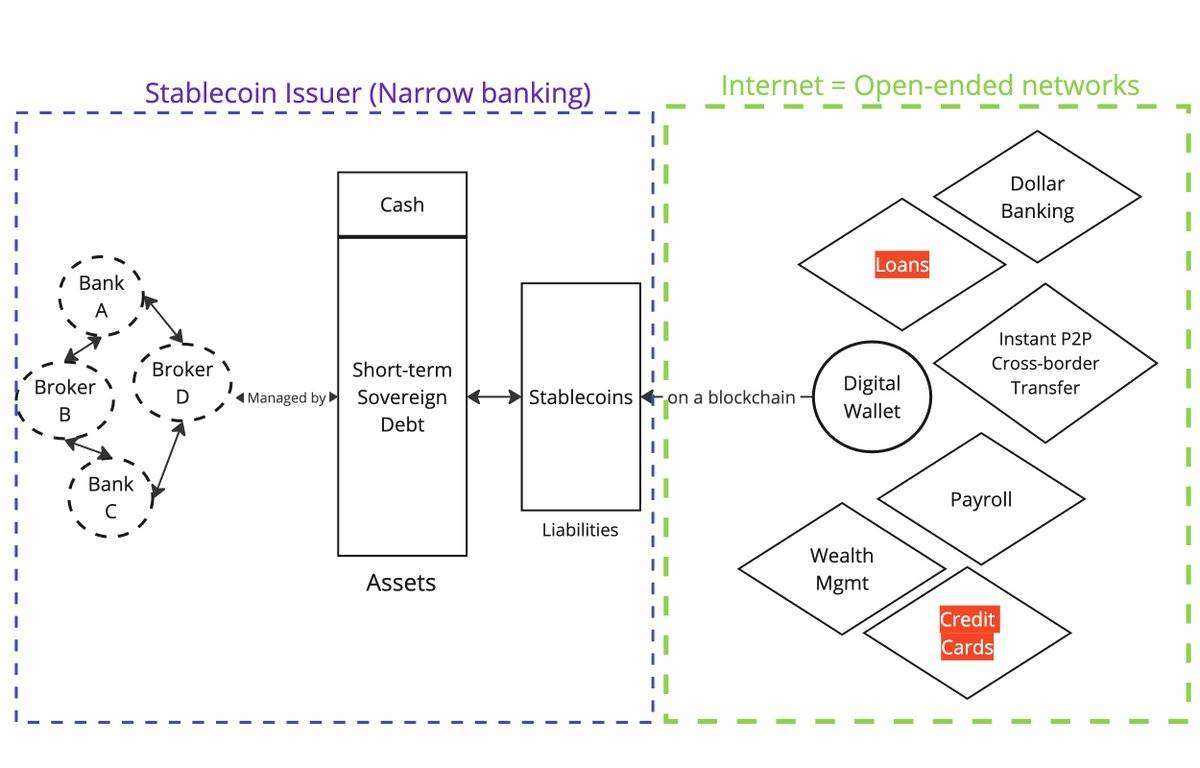

Fiat-backed stablecoins (e.g., @circle, @Tether_to, @Paxos) represent on-chain claims, where these tokens are backed by some form of fiat collateral held off-chain somewhere.

Assets

Issuers do not provide loans; they are narrow banks.

Liabilities

Tokens are now distributed on blockchains. Anyone with a wallet and internet access can purchase and hold these tokens from secondary markets.

Functionally, stablecoins deliver the same services to consumers as Banking as a Service (BaaS).

Holding $USDC as a non-U.S. user is equivalent to having a U.S. dollar account via @Wise.

If you hold $USDC, you bear the risk of Circle as the issuer, BlackRock as the securities custodian, and Circle’s banking partners.

If you hold a U.S. dollar account through @Wise, you bear the risk of Wise’s BaaS partners and the underlying sponsor banks (fractional reserve).

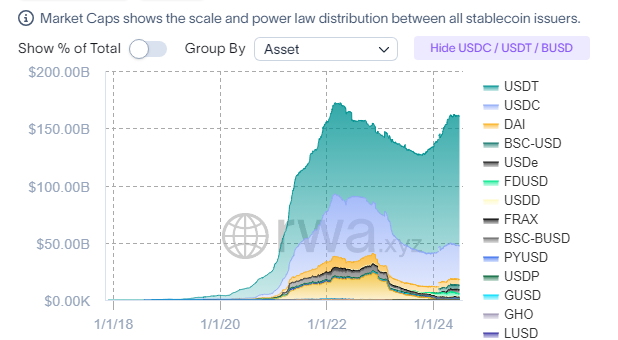

So why have stablecoins grown so rapidly in such a short time?

It all comes down to the distribution of liabilities (deposits in Web2 vs. stablecoins in Web3).

In Web2, deposits are trapped within closed networks (e.g., domestic payment networks and SWIFT).

In Web3, stablecoins are recorded on public blockchains from day one — they are open networks.

This also explains why public blockchains may achieve the Lindy Effect (i.e., the longer something exists, the more likely it is to continue existing), as they become focal points for coordination among all market participants.

(See thread)

This leads me to my next point:

-

The form of stablecoins (i.e., the asset side) will not change in the future

Precisely because stablecoins must focus on distribution (i.e., liabilities), issuers will naturally converge toward similar asset compositions.

On Regulation

Regulators (such as those in the U.S., EU, Hong Kong, etc.) are narrowly focusing stablecoin regulation on the asset side — specifying asset types and how assets should be managed is relatively straightforward.

If you want to protect consumers, regulating the asset side makes sense (see Terra/Luna algorithmic backing).

-

While the form of stablecoins won't change much, the utility of stablecoins (i.e., how liabilities are used) remains vastly unexplored

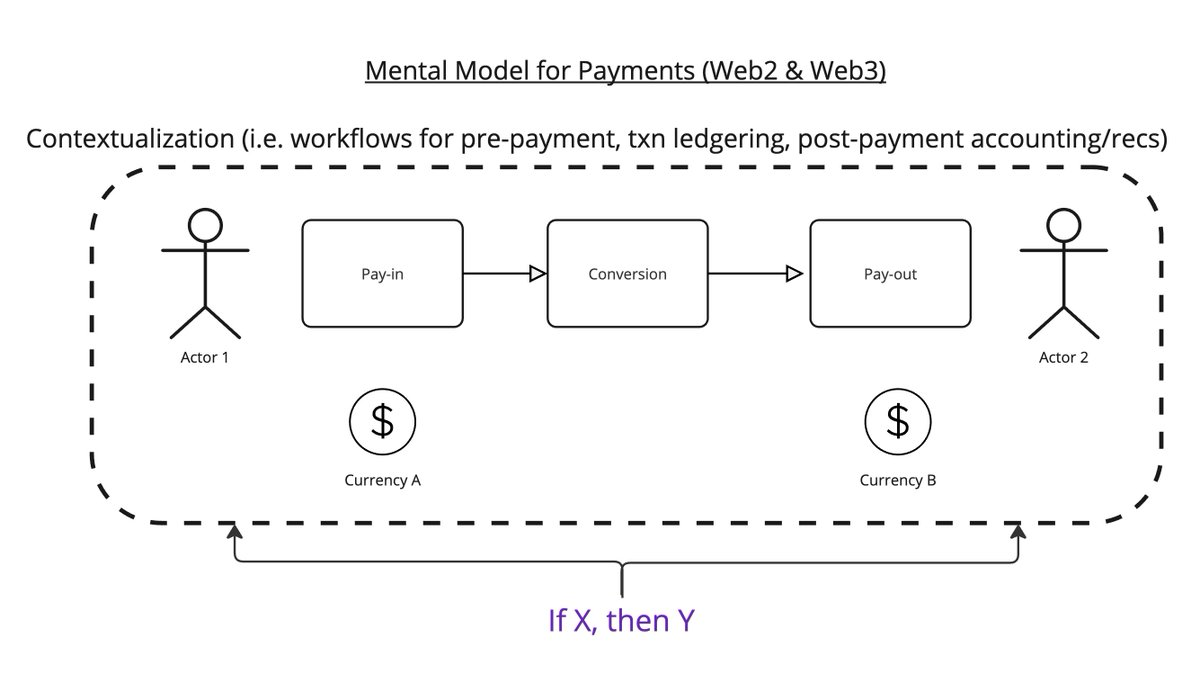

Imagine that the essence of payments is transmitting $x from one place to $y under certain conditions.

Here's my mental model.

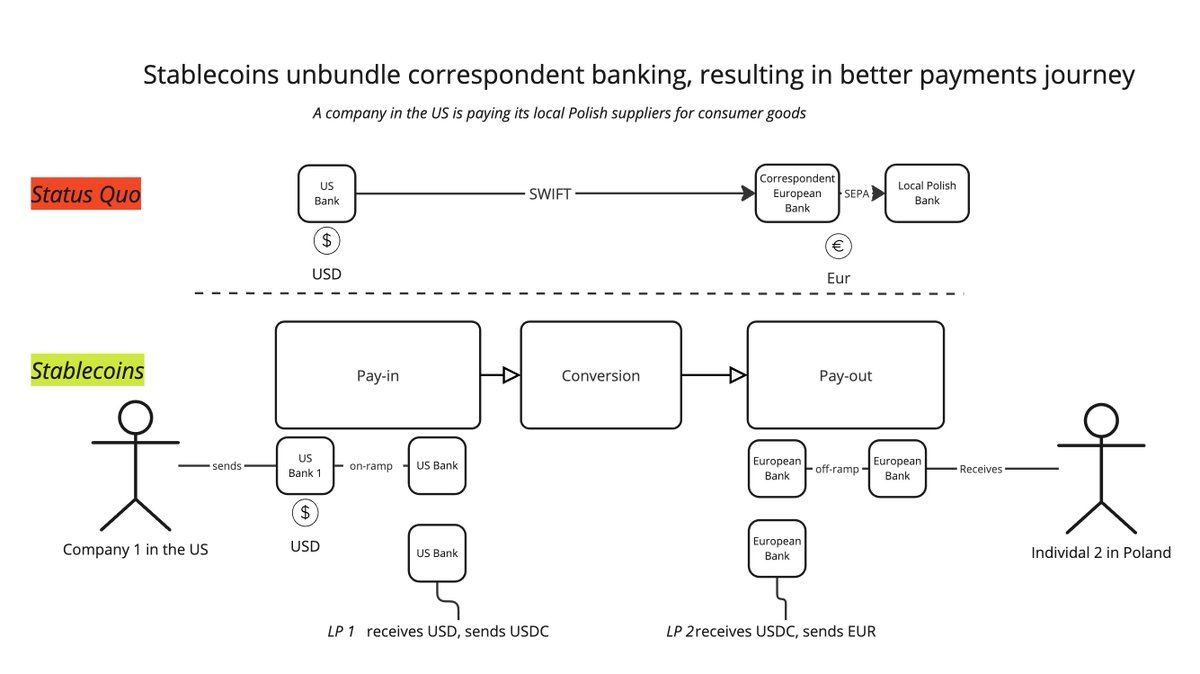

The payment process consists of three steps:

-

Payment Ingress

-

Conversion

-

Payment Egress

Within this workflow, you need to consider things like: What is this payment for? After the transaction completes, you need to record it on a ledger. Upon receiving the transaction, you need to reconcile it with an invoice.

Currently, stablecoins have one clear utility: deconstructing traditional correspondent banking networks through a new set of service providers. Instead of relying solely on SWIFT transactions, you can now break it down into: Ingress → BaaS → LPs Conversion → BaaS → Egress. This allows you to integrate best-in-class services at each stage, delivering a better user experience.

In fact, this is exactly how @mgiampapa1, @will_beeson, and @bkohli described it on @rebankpodcast.

(Listen here)

But is cross-border payment the only use case for stablecoins?

I don’t think so.

There is vast untapped potential around programmable money.

What if "if X, then Y" logic could be applied across the entire payment workflow — what about value transfers between machines?

(See thread)

How could a company like @sentient_agi monetize data sources for large language models (LLMs) every time inference is called?

(See thread)

On Regulation

How do regulators view the utility of stablecoins? In my opinion, the only thing that matters is Know Your Customer (KYC).

The most obvious regulatory conflicts I see are:

-

If stablecoins are truly analogous to Banking as a Service (BaaS), should regulators treat stablecoins the same way they regulate BaaS? This is a question of functional equivalence.

-

Should stablecoins be allowed anonymity like cash?

If the first scenario happens, the entire stablecoin industry would collapse, with market cap and trading volume halved. The U.S. would lose a major source of demand for U.S. Treasuries (UST).

(See thread)

The second scenario is possible, but I expect strong opposition from incumbent businesses and offshore banks benefiting from the status quo.

(See thread)

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News