Variant Fund: Reflecting on Q2 2024, Thoughts on the Current State of the Crypto Market

TechFlow Selected TechFlow Selected

Variant Fund: Reflecting on Q2 2024, Thoughts on the Current State of the Crypto Market

Observing the current state of each ecosystem and the positive relative characteristics demonstrated by its competitors can serve as a guide for each ecosystem to strive for improvement.

Author: Alana Levin

Translation: TechFlow

Every six months or so, I write an internal reflection on the state of crypto and where things are headed. This time, I've decided to publish one of my recent pieces publicly, in case it sparks interest.

The article is divided into three parts: what's working today, what else is happening (or emerging), and what I'm excited about next. While I'll try to ground my analysis with data, there will inevitably be some personal views mixed in. I hope you find this interesting—if responses are positive or feedback constructive, I may consider sharing more of these reflections in the future.

What’s Working Today

The good news is that many projects are currently operating successfully and achieving meaningful results. Many of these qualify as “big ideas” because they have the potential to significantly shift the status quo. Their success creates new opportunities.

To clarify, I use the term “what’s working today” to refer to projects or trends that demonstrate sustainable product-market fit, are expanding the size of the crypto market, or both.

So, which projects or trends are showing signs of success or growth right now? Below is a (non-exhaustive) list of 10 projects that exhibit notable signs of “success”:

-

Stablecoins

-

Bitcoin as an alternative asset

-

Farcaster, an early but growing social network

-

Asset creation

-

Community-created and trained AI models

-

Solana

-

Ethereum

-

Zora

-

Coinbase

-

On-chain exchanges

-

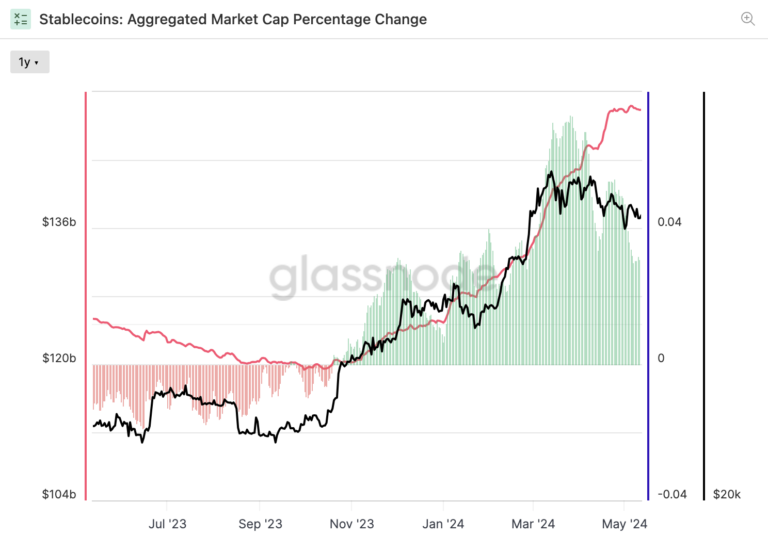

Stablecoins

On-chain stablecoin supply has seen a net inflow of approximately $25 billion year-to-date. Since November 2023, overall inflows have remained positive. Permissionless, global access to the US dollar continues to enjoy strong product-market fit.

-

Bitcoin as an Alternative Asset

In January, nearly ten spot Bitcoin ETFs were approved. By early June, over $80 billion worth had been deposited into spot Bitcoin ETFs. (Data from Blockworks & The Block)

Gold seems like a helpful analogy for understanding institutional adoption of Bitcoin: regardless of whether you believe this asset represents an inflation hedge, it serves as an alternative to traditional equities and enjoys a certain level of social consensus. One might argue Bitcoin is better than gold—it’s easier to transfer, has a known supply cap, and is gaining traction on corporate and national balance sheets—potentially surpassing gold in market value.

In the private markets, Q1 was characterized by a wave of projects aiming to expand Bitcoin’s utility. This includes (many) Bitcoin smart contract layers, on-chain lending protocols, and efforts exploring how to leverage Bitcoin’s economic security budget to help secure other chains. I suspect the fruits of these developments may become evident in the second half of this year.

-

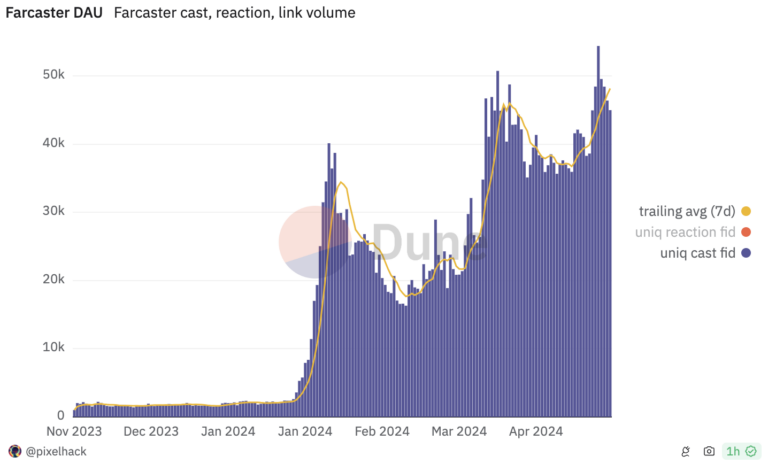

Farcaster

Farcaster is a social network built on an open protocol and is beginning to experience significant growth.

The turning point came at the end of January with the launch of frames—mini application components that users can share and interact with directly within their Farcaster client feeds.

-

Asset Creation

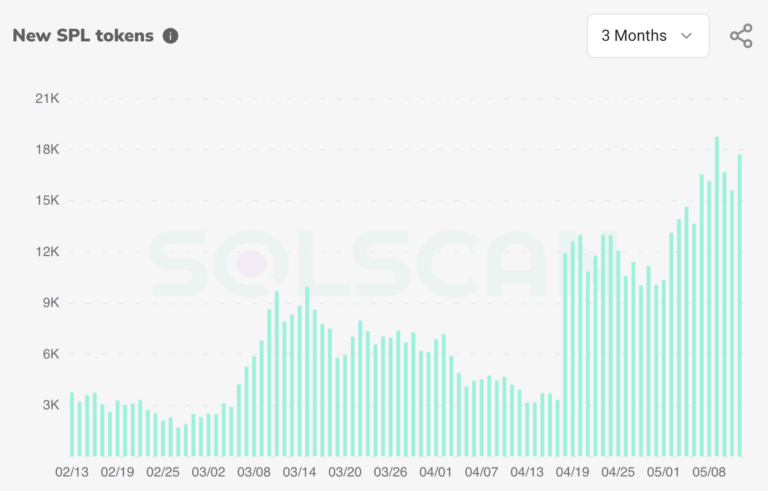

The number of newly created tokens continues to rise. One way to track this trend is by observing the number of new tokens appearing on decentralized exchanges (DEXs). Activity is primarily driven by asset creation on Base and Solana.

Especially on Solana, over 10,000 new tokens have been created daily over the past few weeks.

Many of these new assets take the form of memecoins. I wouldn’t describe myself as an active participant in the memecoin space, but I do recognize a very real and active user base demonstrating enthusiastic engagement.

Notably, the emergence of these new assets has led to some unexpected yet productive side effects across the broader ecosystem. For example, we’re seeing more experimentation with new tools such as Solana’s token extensions. A token called $BERN leveraged Solana’s new token extension to innovate on tokenomics: 5% of any sale transaction is burned (as a redistribution mechanism to remaining holders). The popularity of $BERN became a driving force behind wallet adoption of the token extension standard—these standards enable complex payment distributions, confidential transfers, and more. Without $BERN, who knows how long adoption of token extensions might have taken.

Overall, my main takeaway is that asset creation appears to be a trend with tailwinds. Regardless of your feelings toward these assets, having issuance and trading capabilities remains two excellent positions within value flows.

-

Community-Created and Trained AI Models

Clearly, we're moving toward a world of abundant LLMs (large language models), low-cost content creation, and abundant choice. In such a world, where does value accumulate?

I believe value accumulates around scarce resources. So, in a world abundant in compute, content, and tools, the question becomes: what is scarce? One answer is taste and attention. The challenge is that taste and attention are fairly intangible resources. Even if we could measure them (e.g., "screen time" as a proxy for attention), pricing such a metric remains difficult.

We’re starting to see crypto tracks help by tightly coupling financial incentives with activities based on taste and attention. Specifically, community-created and trained AI models that produce tangible outputs—such as sellable or licensable goods or services (art, films, IP, etc.)—enable rewarding participants. For models with subjective outputs, community participants act as tastemakers by training models according to their cultural preferences. There's strong incentive to cultivate good taste: the better the output, the higher its selling price.

We’re beginning to see some of these projects emerge in real and effective ways. Botto is my favorite example. It’s an autonomous artist whose $BOTTO token holders have weekly input into model training.

Botto’s art keeps improving, and the prices of its weekly auctioned artworks continue to rise. At the same time, the owner-participant network continues to grow:

I believe we’ll begin to see more community-created and trained AI models, especially as proven and successful examples like Botto continue to scale.

Some companies are addressing attribution issues top-down through litigation, data licensing agreements, or a combination thereof. If we assume the current state represents less than 1% of the model outputs that will exist over the next five years, clearly there remains room for other approaches to solve attribution and value distribution to contributors. Crypto tracks offer a uniquely valuable solution. Crypto strengthens both economic and creative attribution. Importantly, it also allows anyone, anywhere to participate.

In an older blog post, Chris Dixon mused:

"There's a famous saying: 'The future is already here—it's just not evenly distributed.' An obvious follow-up question is: if the future is already here, where can I find it?"

Community-created and trained models represent a space where we have a few small but growing projects that strongly point toward a much larger future.

-

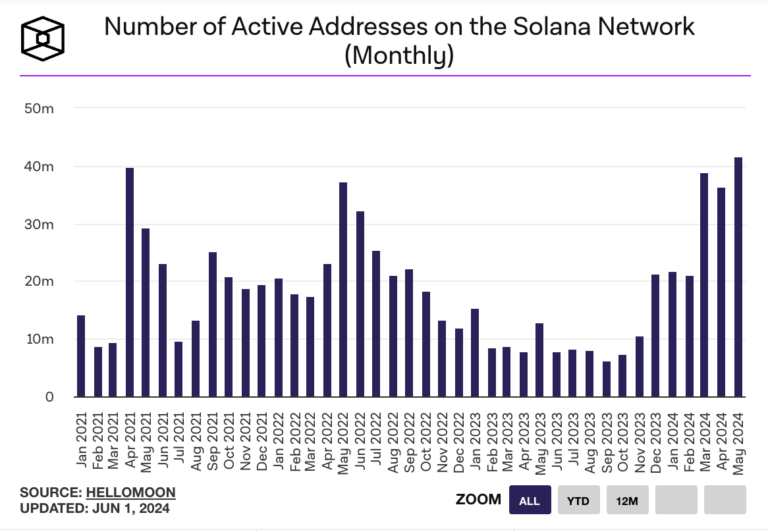

Solana

Daily active addresses interacting with Solana are 2-3x higher than last year and roughly match the peak activity levels seen during the 2021 cycle. Over the same period, monthly active addresses increased 3-4x, reaching a new high in May 2024:

The network is also starting to generate meaningful fee revenue, beginning to validate the hypothesis that Solana’s low fees will be offset by higher user activity and transaction volume.

Conclusion: Solana’s trajectory suggests it is meaningfully working and here to stay.

-

Ethereum

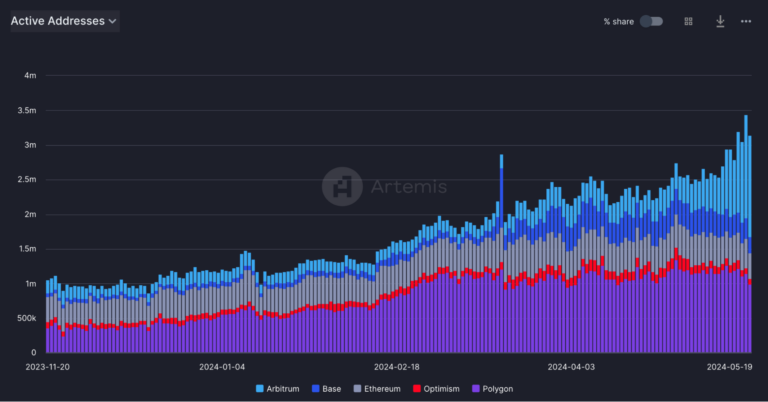

The Ethereum ecosystem has also made significant progress. There are two ways to frame this growth: focusing solely on Ethereum itself, or looking holistically at the Ethereum chain system (i.e., including the Ethereum roadmap).

Monthly active addresses on Ethereum itself have grown substantially. The YTD average over the past 30 days increased by about 30%, only ~10% below the 2021 peak.

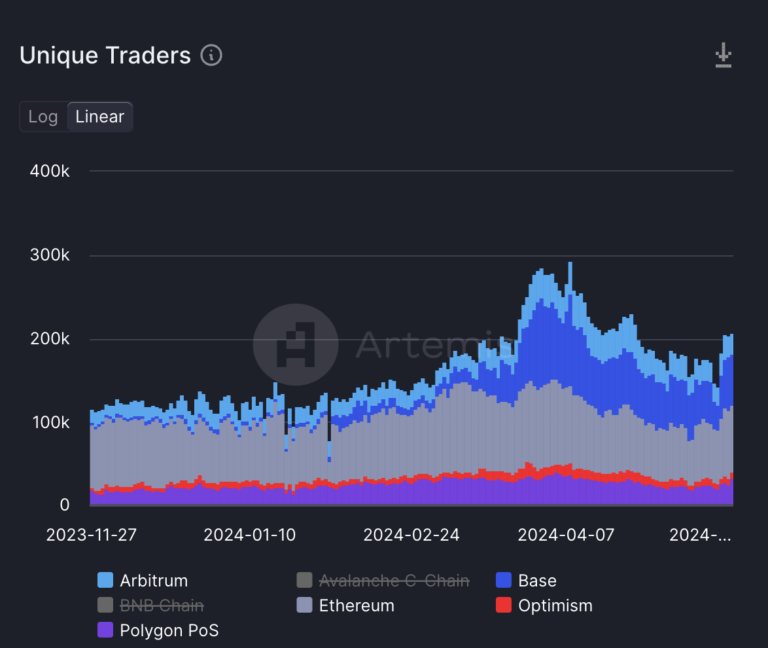

Looking at the broader Ethereum ecosystem also reveals strong signs of growth. I aggregated daily active addresses across five leading Ethereum chains—Ethereum, Arbitrum, Base, Optimism, and Polygon—the selection based on their rich application and developer ecosystems.

Conclusion: Ethereum has been and will continue to be one of the most important ecosystems in crypto.

-

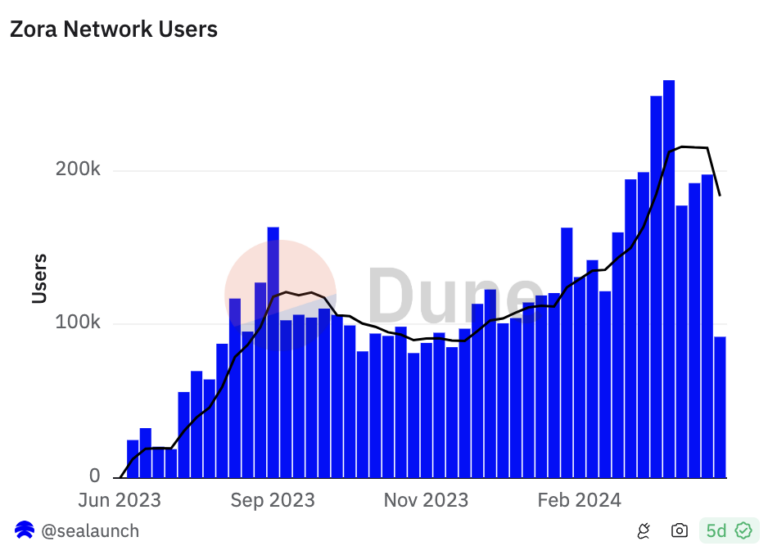

Zora

Zora Chain (also known as Zora Network) launched about a year ago. Since then, the network has continued to find its footing. Weekly active users have grown ~60% year-over-year, recently surpassing 250,000—a new high. The chain also enjoys a ~34% margin, meaning Zora retains about one-third of the ETH users spend on transaction fees.

Zora Chain validates the idea that applications with sufficient distribution power can begin vertically integrating with other parts of the stack (e.g., blockspace), unlocking more attractive economics.

-

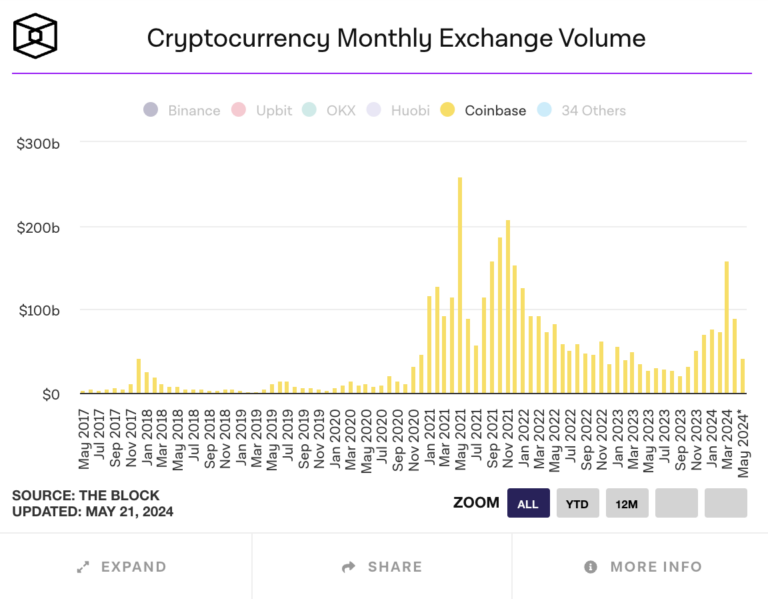

Coinbase

Coinbase also had a strong start this year. It is listed as custodian for 8 out of 11 spot Bitcoin ETFs. Trading activity continues to progress as well—volume reached $157 billion, the highest since November 2021.

Trading fees still make up the majority of Coinbase’s revenue. In Q1, the platform generated over $1 billion in revenue from trading fees (about two-thirds of its quarterly revenue).

Equally noteworthy, Coinbase continues to diversify its revenue streams beyond transaction-based fees. Revenue from blockchain rewards and custody fees both doubled compared to the prior year. Stablecoin revenue approached $200 million, with growth in USDC circulation offsetting (slightly lower) rates. Coinbase One, Coinbase’s membership suite, has over 400,000 subscribers. Base, Coinbase’s Layer-2 protocol, generates millions in on-chain fees monthly.

Coinbase’s success demonstrates (until recently) what many merely assumed: many meaningful new business models can be built around crypto primitives.

-

On-Chain Exchanges

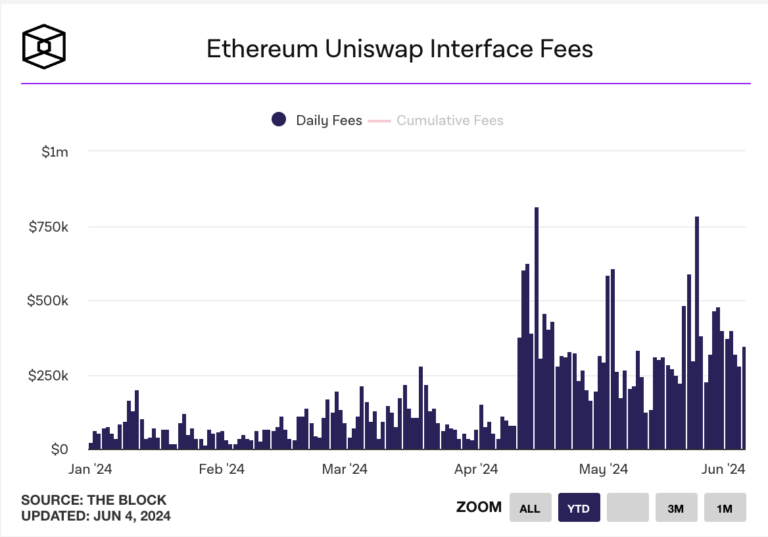

On Ethereum’s mainnet, Uniswap’s number of unique users (traders) has roughly doubled over the past six months.

One definition of a successful protocol is that successful businesses can be built on top of it. We see this with on-chain exchanges—for instance, Uniswap Labs’ revenue growth via its interface:

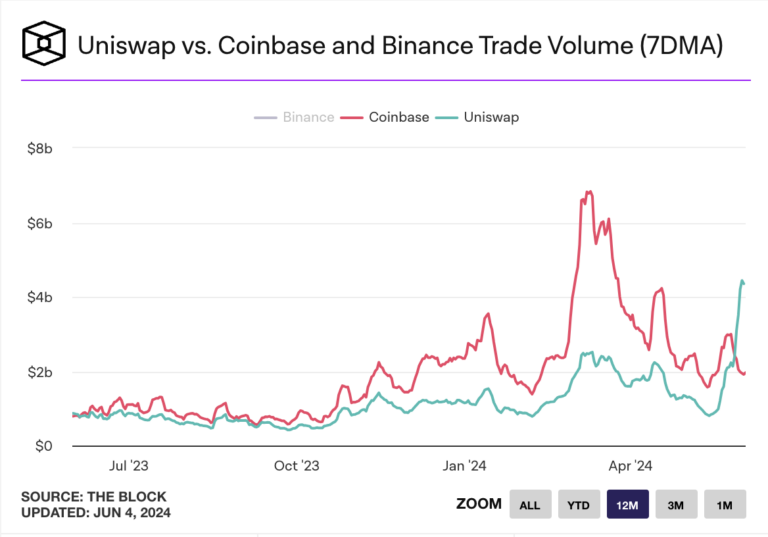

Uniswap’s (protocol) 7-day moving average trading volume recently surpassed Coinbase’s:

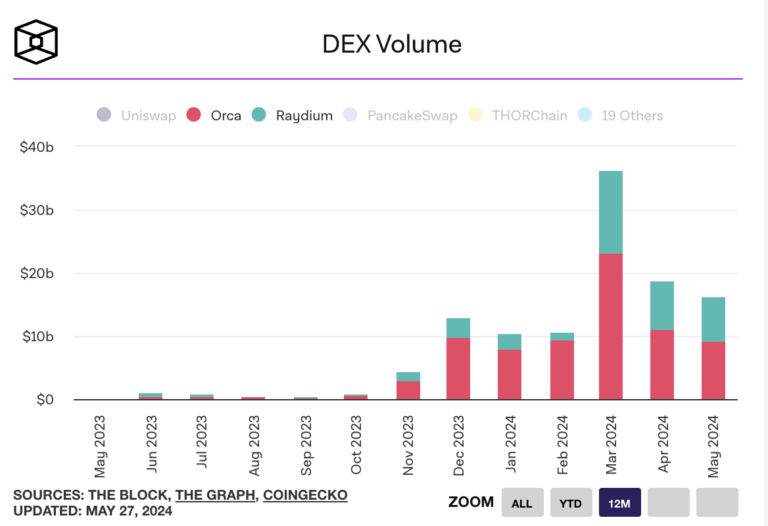

Importantly, we’re seeing growth not only on Ethereum but also on Solana. Orca and Raydium, two leading DEXs, are also showing significant growth:

On-chain protocols facilitating billions (and even tens of billions) of dollars in value exchange each month is no small feat. These protocols and interfaces represent very real, revenue-generating projects. Where centralized entities exist (e.g., interface companies), I hope to see some of these profits reinvested into improving security, robustness, and user experience.

-

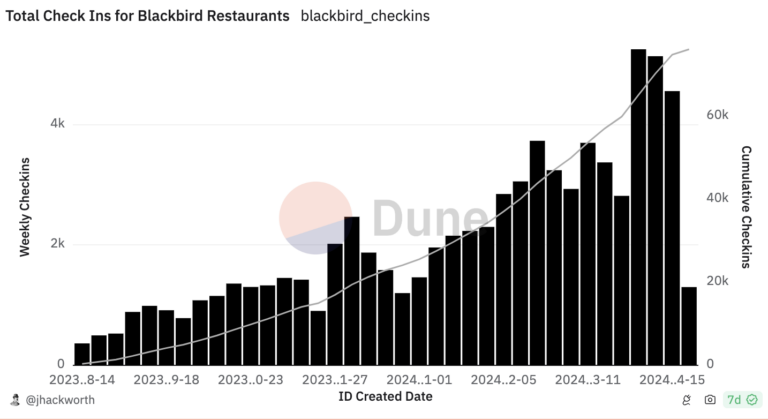

Bonus Project: Blackbird

Blackbird is a loyalty and rewards program designed for the restaurant industry, underpinned by crypto technology. When users check in at a participating restaurant, the app mints an NFT for them—a digital memento of their visit and a data point for restaurants in the network to understand customer dining habits. Currently, Blackbird is primarily present in New York City.

Blackbird’s user check-in count continues to grow steadily.

Personally, Blackbird has changed my dining habits: whereas I used to let friends choose where we eat, I’ve become more proactive in suggesting places and mainly use the Blackbird app to guide us toward restaurants we might enjoy.

Other Things Happening

Other notable trends over the past two quarters include the rise of SocialFi and the proliferation of new chains (mostly L2s and L3s within the Ethereum ecosystem). While I think it’s too early to say whether these trends are truly “successful,” it’s worth noting they are significantly shaping on-chain user behavior and how developers evolve their business models.

-

Growth of Social Finance Applications

Several financialized social (“SocialFi”) applications have emerged. A few have already generated millions in fees. Two of the most popular I know of are Friendtech and FantasyTop. Clearly, users find these apps engaging and are willing to participate. It’s exciting to see new forms of on-chain activity.

I remain skeptical about the sustainability of some of these business models. Speculation alone seems insufficient for long-term success. But that’s okay. These apps may simply need adjustments to achieve more sustainable models. Even speculation-driven attention offers opportunities to monetize that interest in other ways. Of course, that crucial second step is the hardest.

-

Proliferation of New Chains

We’ve also seen a surge of new chains—especially L2s and L3s. For Ethereum ecosystem chains, underlying technology doesn’t seem to be a major differentiator. Instead, brand and community reign supreme. Base, Coinbase’s L2, may be the prime example of strong branding. Despite lacking direct token incentives used by other chains to attract talent, it enjoys a (reportedly) growing developer ecosystem.

So far, we’ve observed three broad ways chains attempt differentiation:

-

Underlying technology. Examples include monolithic vs modular chains, or optimistic vs zero-knowledge rollups.

-

Chain economics. Canto was the first (that I know of) chain in recent years to attempt redistributing transaction fees back to ecosystem developers. Blast and Berachain are now experimenting with various other yield-generation and economic distribution mechanisms. It remains unclear how sustainable these are—both economically and in terms of long-term competitive advantage.

-

Brand and community. A chain’s culture and/or reputation can provide a halo effect for developers: it may enhance perceptions of receiving more support (from community or peers) while building in the ecosystem, offer reputational cover for certain consumers (“no one ever got fired for choosing a MacBook”), and/or align with developers’ own values.

Mature chains possess all three elements. Take the two “successful” chains I highlighted earlier: Ethereum and Solana. Ethereum pioneered the EVM, implemented EIP-1559 (burning part of transaction fees as a redistribution mechanism to ETH holders), and cultivated a strong developer community and ethos around its technology. Solana popularized the integrated blockchain, was the first to make low fees commercially viable, and its community truly proved resilient during the 2022–2023 bear market.

My hypothesis is that the next wave of chain differentiation will come from external integrations. Examples might include seamless access to additional funding sources (e.g., Coinbase accounts), KYC screening within wallets, or verifying personhood. This is a vast design space—one I’m eager to explore further.

Looking Ahead

Reflecting on the past six months, my main takeaway is that we’re still mostly discussing topics from 6–12 months ago—but with greater maturity in what’s working today. As these projects mature, many should evolve into platforms whose successful byproducts will create new opportunities. Growth brings growing pains, and those pains create space for third-party solutions.

Projecting the growth of these major platforms can also serve as a foundation for thinking about the future. What excites me most are new distribution channels and better building blocks.

New Distribution Channels and Better Building Blocks

On distribution, I’m excited about several growth vectors: scaled-up Farcaster, Telegram apps with stronger wallet functionality, and interfaces like World App continuing to onboard more people (it already has 10 million users).

There are also many new and exciting building blocks. Coinbase launched a smart wallet enabling users to pay directly from their Coinbase account. Reservoir’s Relay protocol helps eliminate UX friction in cross-chain bridging, finally making “one-click” checkout experiences on-chain possible. World ID continues to grow, aiming to provide a method for authenticating humans versus bots. And more.

This may sound vague. I occasionally get frustrated reading things that feel more like abstract hope than reality, so I’ll try to avoid that by illustrating with a concrete example of how these building blocks and new distribution channels could work.

Take modern advertising—a multi-billion-dollar market touching nearly every business. Despite decades of improvements in attribution and targeting, I suspect it remains riddled with inefficiencies. Now imagine what “advertising” on Farcaster might look like:

-

A company could directly send coupons to target customers’ wallets (since each account has an associated wallet).

-

Coupons could be based on similar products mentioned in consumer posts or liked content.

-

Businesses could operate confidently knowing data will always remain open and accessible (i.e., no fear of API shutdowns or rate hikes), allowing them to invest in optimizing this channel’s effectiveness.

-

Marketing budgets allocated by merchants would only be spent when consumers actually make purchases using the coupon.

Altogether, open social graphs, embedded payment rails, and verifiable digital identities could create win-win outcomes for businesses and consumers alike.

Maturing Chains with Futures-Oriented Trajectories

Another notable takeaway from the “what’s working” section is that there are now several credible and growing ecosystems (Ethereum, Solana, Bitcoin). These three ecosystems compete on distinct differentiators, and each one’s strengths apply positive pressure on others to improve continuously. For example, Solana’s success in low fees and high throughput pushes Ethereum to innovate constantly at both base layer and L2 levels. Similarly, Ethereum’s multiple clients may set a goal for Solana to achieve client diversity (e.g., its upcoming Firedancer client). Bitcoin was first to achieve real institutional adoption but is now experimenting with new programmability features (like Ordinals, Runes, and potential OP_CAT upgrades). Overall, I’d summarize that each ecosystem is striving toward rough functional parity with others. Observing each ecosystem’s current state and the positive relative attributes demonstrated by competitors can serve as a roadmap for improvement.

This feels very positive. I’m a tennis fan, so allow a loose tennis analogy: if Federer, Nadal, and Djokovic hadn’t competed against each other, their levels likely wouldn’t have reached what they did. Each pushed the others to elevate their game, producing truly exceptional tennis. I believe we’re seeing something similar across different crypto chains today. Each chain advances faster because the pressure to be productive is high. The result is net positive growth for the entire industry.

A Few New Ideas

There’s still much infrastructure and applications worth building. Some underexplored areas I find promising include:

-

Different forms of credentials. Credentials (verifications, attestations, etc.) are valuable resources to put on-chain: timestamped issuance and issuer verification benefit from public ledgers. One such credential could be workplace verification—a receipt issued by an employer confirming someone worked at a company for a certain period. Within crypto, I’ve seen many attempts at verification. The key is identifying credentials with real economic value—like employment verification—and focusing on those markets.

-

Price-discriminated assets (PDAs). These are goods with real economic value but wide variance in market participants’ willingness to pay. Restaurant reservations are a great example. Recently, a widely shared article covered New York City’s underground reservation market: hot bookings are attacked by bots and resold on exclusive secondary markets for thousands of dollars. To me, if financialization is inevitable, making these “assets” as transparent and accessible as possible seems net positive for both restaurants and diners. Restaurants could more easily audit reservation transfer history, and more potential customers could participate. Tokenizing reservations could even enable programmable price caps or revenue sharing with restaurants. This is just one example. Many other markets involve real assets with fundamental economic value but are mispriced or inefficiently priced due to opaque or limited market access.

-

New forms of token distribution. There are many opportunities to fine-tune activities people already do via token rewards. Blackbird is the first and most prominent example: dining out is already widespread, but the presence of Blackbird rewards may influence users’ choices of location and frequency. This could be applied more broadly to areas where people already spend time and money but lack consistency or loyalty in consumption. In particular, I’d look for categories where merchants could benefit from alliance or cooperative effects (in gaining richer data/insights) and where there’s strong potential to boost customer loyalty through nudged incentives (nudge-style incentives).

Whether these ideas have a unique “why now” opportunity remains debatable. Most feel like good ideas that have existed for a while but haven’t been sufficiently explored—making them worth pursuing.

Conclusion

This reflection captures what I believe are many of the important things happening in crypto recently—but importantly, not all of them. Some areas not covered here—but perhaps could (or should) be—include the growth of permanent storage solutions (like Arweave), DeFi protocols maturing into true financial platforms (like Morpho), and Telegram’s impressive push behind TON.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News