Opinion: Why is TVL an ineffective metric for derivatives DEXs?

TechFlow Selected TechFlow Selected

Opinion: Why is TVL an ineffective metric for derivatives DEXs?

High TVL: High trading volume implies low capital efficiency, which goes against the goal of perpetual contracts.

Author: Tristan

Translation: TechFlow

I said it once, and I’ll say it again: TVL is a terrible metric for derivatives trading.

The appeal of leverage is getting $10 of buying power with just $1 of margin. High TVL-to-volume means low capital efficiency—exactly opposite to the goal of perpetual contracts 🧵

Why does anyone care about TVL?

Under proof-of-stake (PoS) systems like Ethereum or Solana, it makes sense to assess a network’s economic security based on the amount of capital staked. The more dollars staked in Ethereum, the harder it is to attack the network.

But when it comes to trading, what do we care about? Putting your capital to work.

That’s precisely why lending markets and margin trading are powerful. You can lock up a small amount of collateral or margin and cover the rest via loans, so your buying power far exceeds available cash.

In decentralized finance (DeFi), no one has fully cracked undercollateralized lending yet due to counterparty default risks. But that’s exactly what drives traditional finance and centralized markets forward.

Why do you think market makers love their “credit lines”?

Derivatives, especially perpetual contracts, offer an excellent way to achieve similar leveraged trading.

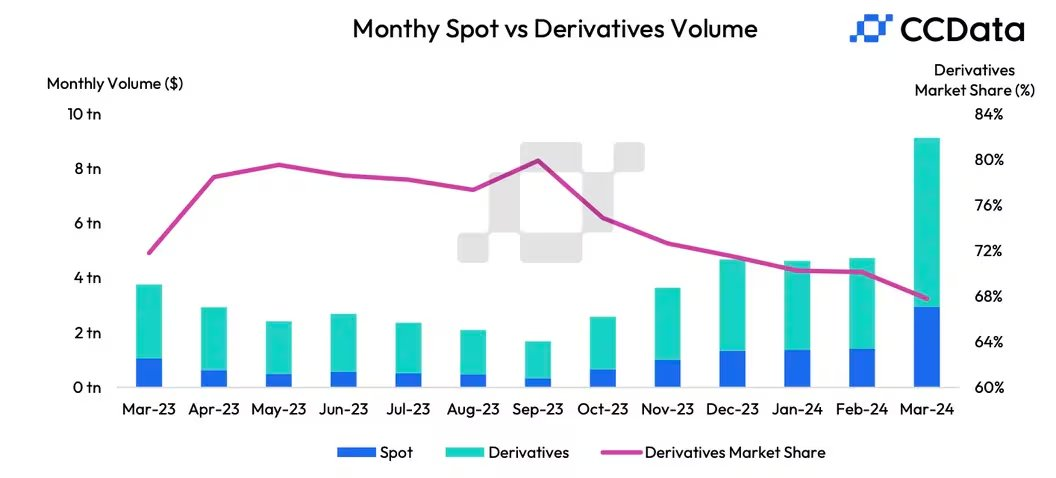

That’s why they’ve become the de facto tool for crypto traders, accounting for over 68% of all cryptocurrency trading volume (mostly perps; crypto options remain negligible).

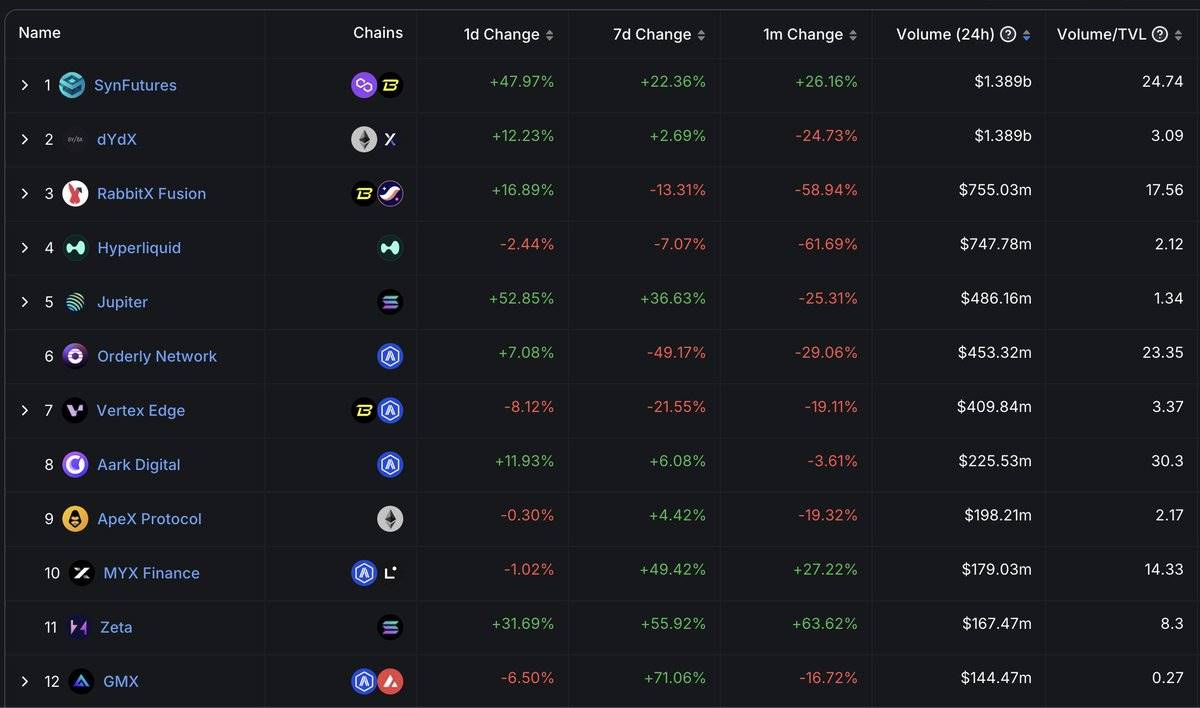

So it’s no surprise that success metrics for derivatives trading revolve around volume (capital turnover) and open interest (total value of outstanding positions).

Anyone touting TVL either doesn’t know what they’re talking about—or is misleading you.

Moreover, this is why the design of decentralized exchanges (DEXs)—both spot and perp—has shifted toward order books and concentrated liquidity AMMs. You want your LP capital actively used by counterparties, not sitting idle in a corner of an xyk (constant product) curve.

So think about it: Do you want your perp trading to execute as many trades as possible with limited capital? Do you want your LP position to generate substantial fees for every dollar you deposit? Or do you want it to sit like a flashy vault full of vanity TVL?

P.S. I’m an engineer, not a finance expert, but this feels extremely intuitive and obvious. I don’t understand why DeFi remains stuck on TVL obsession years later. How do we fix this?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News