Grayscale Report: "The Public Chain and Tokenization Revolution": Who Are the Biggest Beneficiaries of RWA?

TechFlow Selected TechFlow Selected

Grayscale Report: "The Public Chain and Tokenization Revolution": Who Are the Biggest Beneficiaries of RWA?

While various assets can benefit from the tokenization trend, the most promising are protocols that provide a universal global platform.

Author: Zach Pandl

Translation: Frank, Foresight News

-

Asset tokenization refers to recording asset ownership on blockchain infrastructure in the form of tokens, enabling assets to benefit from blockchain functionalities such as more efficient settlement and the ability to interact with smart contracts;

-

Modern financial systems are already highly efficient in many respects, so tokenization itself may not deliver immediate efficiency gains. Instead, we believe the primary benefits may come from bringing users, assets, and applications together onto a shared global platform;

-

From a crypto market perspective, while various assets could benefit from the trend toward tokenization, the greatest potential likely lies with protocols capable of serving as this universal global platform. Currently, Grayscale Research believes the Ethereum blockchain is most likely to fulfill this role in the future;

Public blockchains can be viewed as general-purpose technologies with numerous potential use cases—from payments to video games to digital identity systems. The value of this technology stems partly from bringing diverse applications onto a permissionless and open architecture. When users, capital, and applications converge in one place, everyone in the ecosystem benefits from network effects.

Tokenization is one of many applications of public blockchain technology. In some cases, moving asset management onto blockchain infrastructure may immediately improve efficiency if existing "back-end" processes are particularly cumbersome. However, for many asset types (e.g., listed equities), current digital infrastructure functions quite well, and it's not obvious that public blockchains would perform significantly better. In these instances, the potential benefits of tokenization may stem from network effects: by migrating global assets onto a common platform, we could create a financial system that is more powerful, more accessible, and lower cost.

From a crypto market perspective, while various assets could benefit from the trend toward tokenization, the greatest potential likely lies with protocols that serve as a unified platform for tokenized assets, investors, and related applications. Currently, Grayscale Research believes the Ethereum blockchain is most likely to fulfill this role in the future.

System Upgrade

When blockchains achieve broader adoption, securities may be fully issued and tracked entirely on-chain. But today, ownership of security yields, as well as physical assets like real estate, commodities, and collectibles, are recorded on traditional off-chain ledgers (typically electronic book-entry accounts). Tokenization refers to the process of registering asset ownership on blockchain infrastructure so market participants can benefit from blockchain capabilities. By design, the price of a blockchain-based token should closely track the price of its underlying reference asset.

Some potential benefits of converting asset ownership into blockchain-based tokens include:

-

Settlement efficiency: Blockchain transactions can settle nearly instantly and can be programmed to exchange assets conditionally, reducing settlement failure risk;

-

Programmability: Tokenized assets can be integrated into software applications to enable enhanced functionality. For example, this could include conditional transfers based on off-chain information (such as compliance approvals) or using tokens as collateral on decentralized lending platforms;

-

Accessibility: Like the internet itself, blockchains are borderless. Thus, tokenized assets could grant investors across a wider range of countries access to top-tier global capital markets. Blockchains can also open access to new asset classes through fractionalization;

-

Cost reduction: By increasing automation and reducing reliance on intermediaries, tokenized assets could lower issuance costs through reduced underwriting fees and interest rates;

Researchers at the Bank for International Settlements (BIS) have defined a tokenization "continuum" to assess how this process might affect specific markets. On one end are markets still requiring substantial manual workflows—such as real estate or bank loans. These assets may be difficult to tokenize, but the process could generate meaningful efficiency improvements.

On the other end, many other markets currently operate efficiently using electronic book-entry systems—for instance, listed equities, mutual funds and ETFs, and listed derivatives. These assets may be easier to tokenize, but the efficiency gains from doing so are more limited.

The best candidate assets for tokenization may lie somewhere in the middle of the BIS continuum: markets that could benefit from slightly improved electronic record-keeping and smart contract functionality—this list may include many types of fixed-income securities, such as government bonds and structured products.

However, as discussed further below, the largest gains may come from moving all assets onto a unified global platform.

Current and Future Tokenization

The first application of tokenization technology to achieve product-market fit (PMF) was stablecoins, which tokenized the simplest and most liquid asset of all—cash.

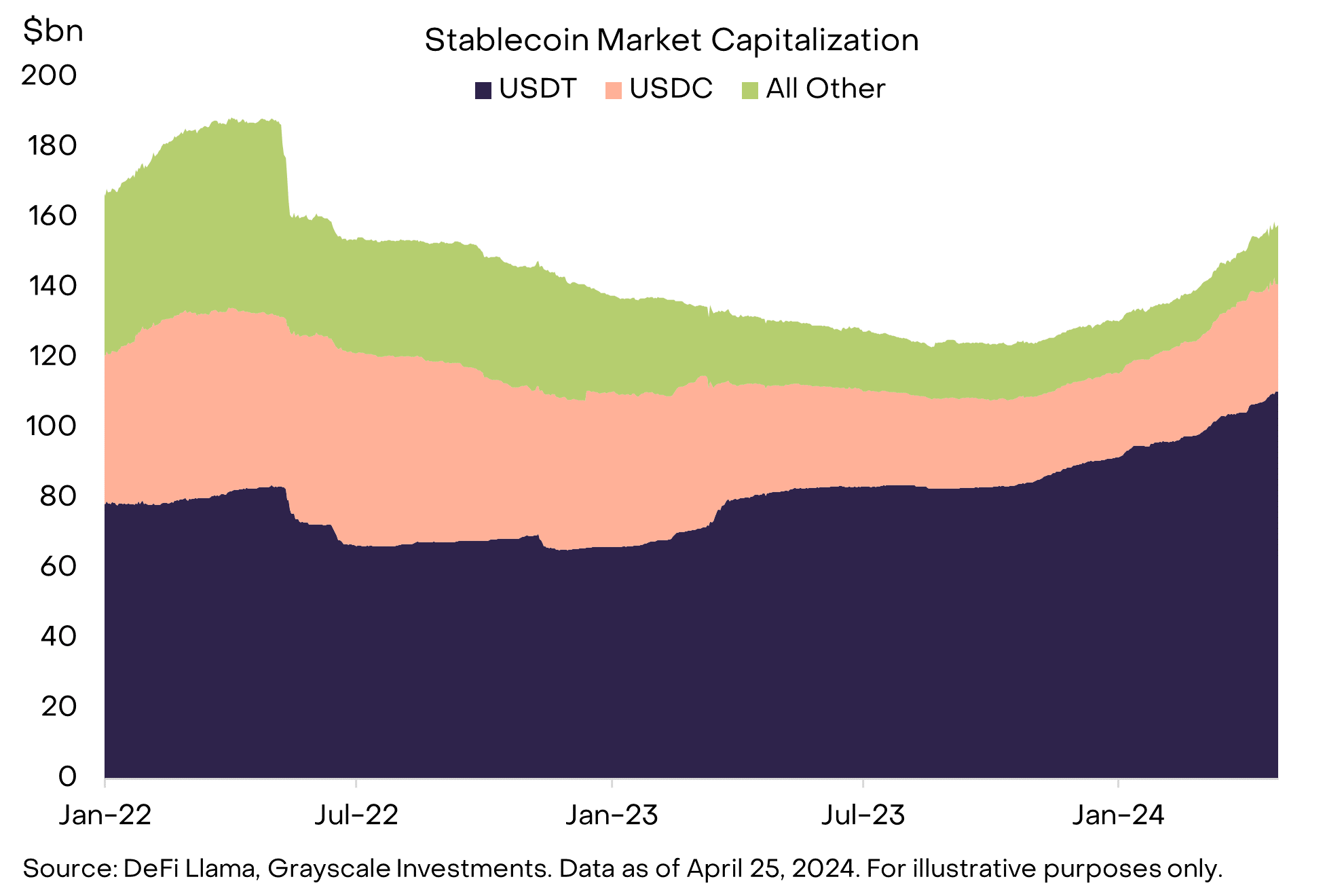

The total market capitalization of stablecoins now stands at $158 billion, led by Tether (USDT) and USDC (Chart 1). Stablecoins take various forms, but both USDT and USDC can be considered fiat-collateralized stablecoins.

They operate similarly to other tokenized assets: traditional assets are held by off-chain custodians, while tokens represent claims that can be held in blockchain wallets. This form of digital cash can then be used for payments, benefiting from blockchain’s near-instant settlement, lower costs, and potential to interact with smart contracts.

Chart 1: Stablecoins Have Achieved Product-Market Fit

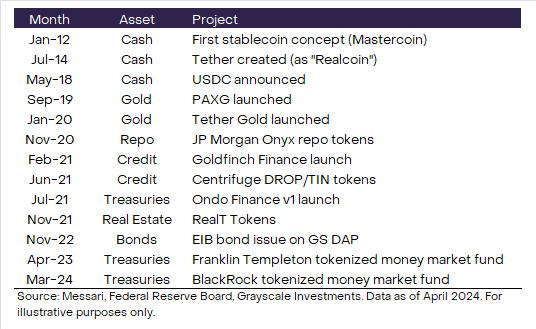

Following stablecoins, the next widely adopted tokenized asset has been gold (Chart 2). The two largest projects, Tether Gold (XAUt) and PAX Gold (PAXG), have a combined market cap of approximately $1 billion. While there are many ways to invest in gold, these products offer certain blockchain-native features, such as the ability to transfer exposure over weekends or outside traditional market hours. This functionality proved useful during recent geopolitical tensions in the Middle East: when other markets were closed, both XAUt and PAXG posted notable gains during the week of April 13–14.

Chart 2: Timeline of Selected Tokenized Projects

The latest wave of tokenization focuses on two distinct markets: U.S. Treasuries and closely related assets, and credit products.

Tokenized U.S. Treasury products are designed as cash equivalents and can be viewed as yield-bearing alternatives to stablecoins. According to data provider RWA.xyz, the weighted average maturity of all currently available products is less than two years.

In other words, these products aim to provide yield while functioning similarly to cash. When cash interest rates were near zero, the opportunity cost of holding stablecoins was relatively low. But now, with dollar interest rates approaching 5%, investors have stronger incentives to seek yield-generating alternatives, potentially accelerating demand for tokenized Treasury products.

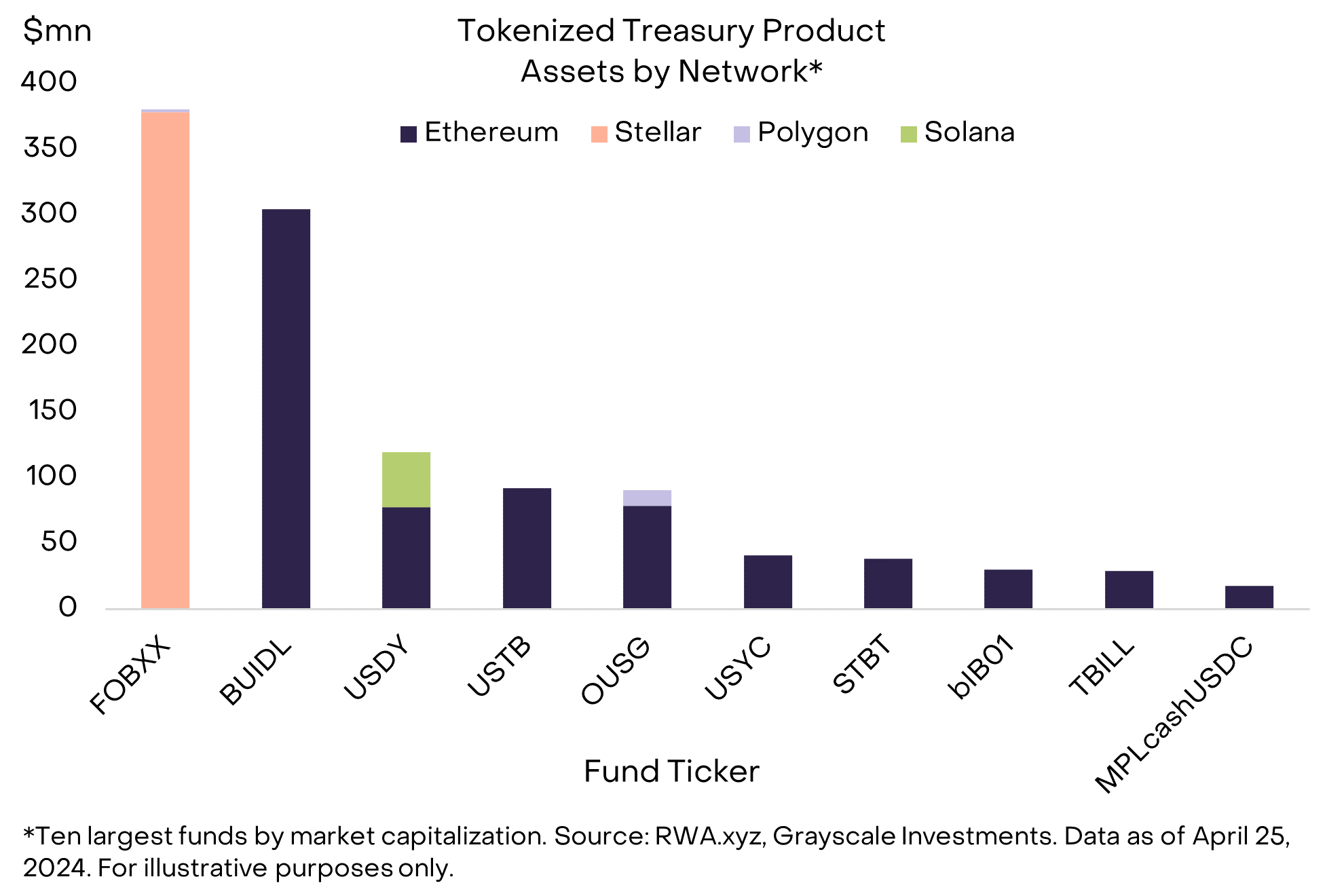

Currently, tokenized Treasury funds in circulation, led by Franklin OnChain U.S. Government Money Fund (FOBXX) and BlackRock USD Institutional Digital Liquidity Fund (BUIDL), exceed $1 billion in size (Chart 3). Many of these existing products have launched on Ethereum and appear targeted at crypto-native institutions, such as cryptocurrency hedge funds and DAOs (decentralized autonomous organizations).

However, the largest fund, FOBXX, takes a different approach: it launched on the Stellar chain and is accessible to retail investors via a mobile app. Overall, about 60% of tokenized Treasury fund AUM resides on Ethereum, 30% on Stellar, and the remainder on other blockchains.

Chart 3: Approximately 60% of Tokenized Treasury Products Are on Ethereum

Companies have also launched tokenized credit products. This is a diverse category including direct loans to single counterparties, structured pools of credit products (e.g., ABS, CLO), and loans to intermediaries in specific sectors (e.g., real estate financing, emerging markets). While these products may carry risks and complexity and are currently designed only for institutional investors, their goal is simple—to route capital from lenders to borrowers via blockchain infrastructure. According to RWA.xyz, this category currently includes $612 million in outstanding loans, with an average yield of about 10% (Chart 4).

Chart 4: Tokenized Credit Products Cover Diverse Borrower Portfolios

There are many other potential applications for tokenization technology, though few have moved beyond the pilot stage. For example, RealT, a tokenized real estate platform, allows investors outside the U.S. to co-own properties; the protocol currently has $103 million in total value locked. There is also hope that tokenized private equity could broaden investor access to alternative investments, though it remains to be seen whether these new issuance channels will meaningfully contribute to AUM in the sector.

Various fixed-income securities have already been issued directly on-chain, by both public-sector issuers (e.g., European Investment Bank) and private-sector issuers (e.g., Siemens). While attempts have been made to tokenize equities, we suspect these projects will need clearer regulatory frameworks before making further progress.

If adoption continues, tokenization could drive significant blockchain activity and fee revenue, given the massive scale of the addressable market—in the U.S. alone, the Treasury market represents $26 trillion, and domestic non-financial sector loans total $36 trillion. Currently, the size of on-chain tokenized assets represents only a negligible fraction of these totals. However, for these products to expand beyond today’s crypto-native institutions, they will need more effective integration with existing pools of capital. This may require linking to brokerage or bank accounts, or offering investors compelling enough reasons to move their assets on-chain.

The Revolution Won’t Happen on Private Chains

A common misconception is that tokenization may not benefit crypto assets because the activity will occur on private, permissioned blockchains rather than public, permissionless ones like Ethereum. While banks have indeed experimented with private blockchain infrastructures (e.g., JPMorgan Onyx, HSBC Orion, Goldman Sachs DAP), this reflects at least partly current regulations that prevent depository institutions from interacting with public chains. Asset managers not bound by these restrictions have instead been active on public chains or hybrid models combining public and private chains.

In practice, virtually every successful tokenization application to date—including stablecoins, tokenized Treasuries, and tokenized credit products—has been deployed on public blockchain infrastructure.

The reason is simple: that’s where the users are.

We expect moving certain assets onto blockchain infrastructure will bring efficiency gains, but the greater promise of tokenization lies in seamlessly connecting assets and investors (or borrowers and lenders) globally, and building richer experiences through interoperable applications.

Beyond tokenization, public blockchains host many other applications, making them natural hubs over time for user assets and activities. As a result, they are also likely to remain the primary destination for asset issuers and developers building open financial applications. We believe privately operated, permissioned blockchains run by corporations or national governments are unlikely to credibly serve as the globally neutral platform required to host the world’s tokenized assets.

Transactions, Fees, and Value Accrual

Blockchain transactions typically generate fees, which can flow directly to token holders (e.g., as dividends) or indirectly through mechanisms that reduce token supply (e.g., buybacks). Therefore, if asset tokenization generates transaction activity and fees, it can accrue value to blockchain-based tokens. However, the mechanism for this will depend on the protocol type and token characteristics (Chart 5).

Chart 5: Assets Across Various Crypto Sectors Could Benefit from Tokenization

Components of our smart contract platform crypto segment should see the most direct impact. L1 blockchains in this market—and perhaps eventually some components of their L2 ecosystems—can serve as universal global platforms for tokenized assets. These protocols’ native tokens are typically used to pay transaction fees ("gas") and may accrue staking rewards or benefit from reductions in token supply.

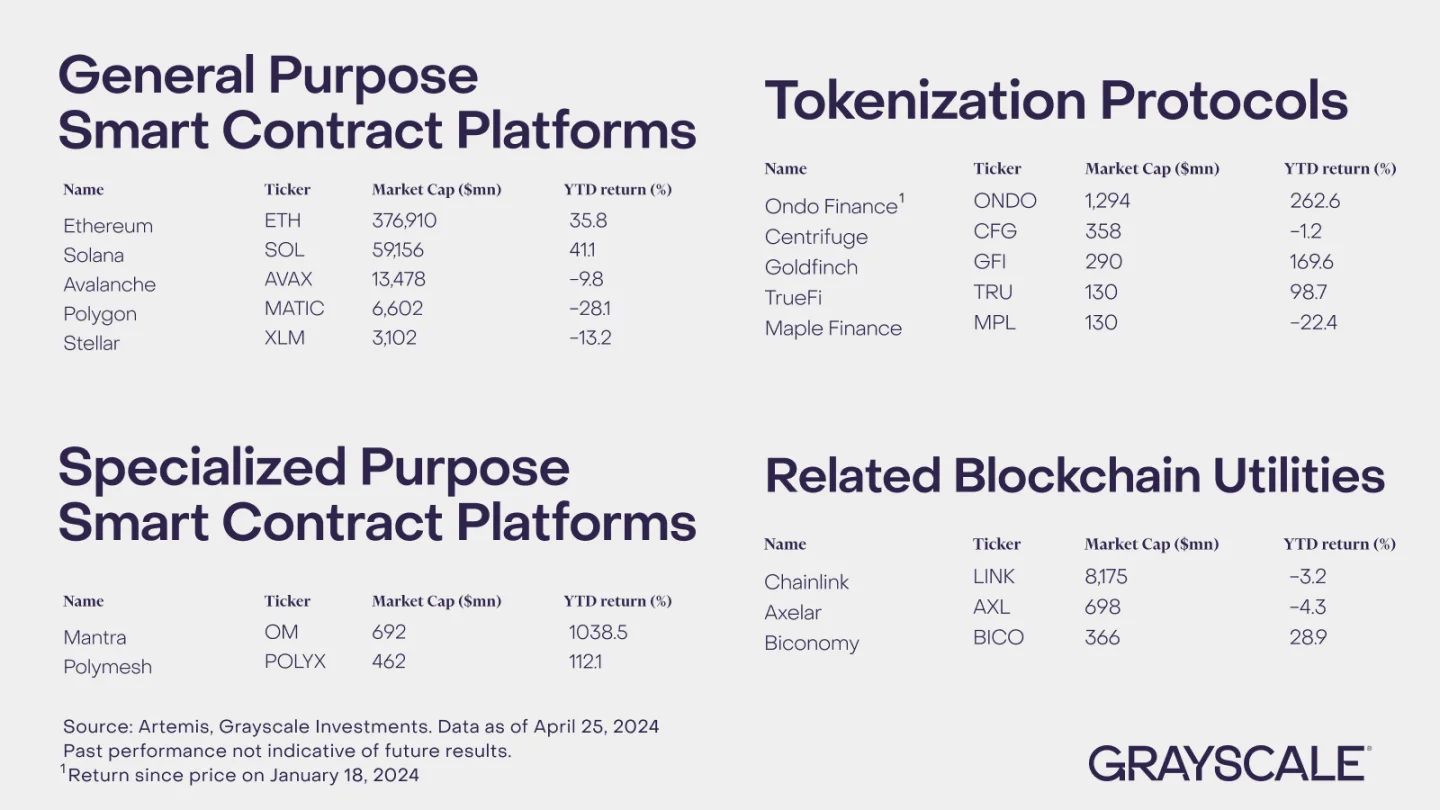

The smart contract platform space is highly competitive, but the Ethereum ecosystem continues to dominate other blockchains in terms of users, assets (total value locked), and decentralized applications. Moreover, we view Ethereum as highly decentralized and neutral toward network participants—a likely prerequisite for any global tokenized asset platform.

Therefore, we believe Ethereum is currently best positioned among smart contract blockchains to benefit from the tokenization trend. Other smart contract platforms that could benefit include Avalanche (used by financial institutions for various proof-of-concept projects), Polygon and Stellar, as well as L1 blockchains designed specifically for tokenization, such as Mantra and Polymesh.

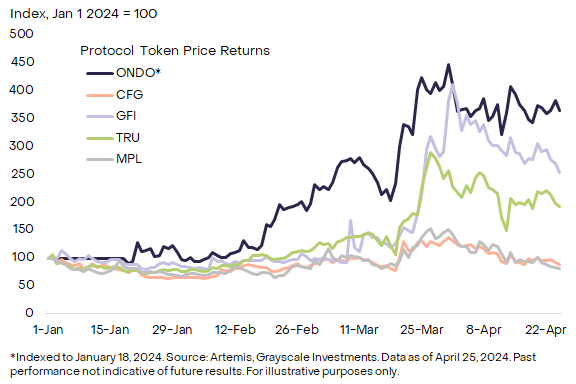

The next group of beneficiaries includes the tokenization protocols themselves—platforms that facilitate bringing traditional assets onto blockchain-based software applications (Chart 6). Many such providers do not have governance tokens (e.g., Securitize, Superstate), but some do.

For example, Ondo Finance, which issues tokenized Treasury products, and Centrifuge, a tokenized credit platform and part of the financial crypto sector. Before considering these tokens, investors should evaluate the nature of governance rights conferred and whether they entitle holders to any share of protocol revenues.

Chart 6: Year-to-Date Returns of Selected Tokenization Protocols

Finally, increased blockchain activity driven by tokenization could support many other components within the crypto ecosystem. For example, Chainlink aims for its Cross-Chain Interoperability Protocol (CCIP) to serve as core infrastructure for messaging and data transfer across blockchains—including between private and public chains. Similarly, the Biconomy protocol offers technical solutions that help traditional financial institutions interact with blockchain technology (e.g., "paymaster" services allowing users to pay gas fees in tokens other than the blockchain’s native currency).

Both Chainlink and Biconomy fall within our utilities and services crypto segment.

The Vision for Tokenization

In summary, many digital commerce use cases are transitioning from closed, centrally intermediated platforms to open, decentralized platforms built on public blockchain infrastructure. Tokenization is just one of many blockchain adoption trends.

But given the size and scope of global capital markets, it could be a major trend. If public chains succeed in connecting borrowers and lenders (or asset issuers and investors) and disintermediating existing fintech, the resulting increase in network activity should create value for public chain tokens.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News