2024 Q1 Global Web3 Virtual Asset Industry Regulatory Policies and Events Overview: ETFs, BUIDL, and Comprehensive Compliance

TechFlow Selected TechFlow Selected

2024 Q1 Global Web3 Virtual Asset Industry Regulatory Policies and Events Overview: ETFs, BUIDL, and Comprehensive Compliance

This article will review the global Web3 virtual asset regulatory developments and key events in Q1 2024.

Author: Will Awang

At the beginning of 2024, following Grayscale’s legal victory and driven by Wall Street capital led by BlackRock, Bitcoin (BTC) spot ETFs were historically approved. This marked the first time digital assets entered the mainstream traditional financial arena, ushering in a new bull market.

This bull market is not only reflected in the rising value of cryptocurrencies but also in the gradual acceptance of blockchain technology by mainstream institutions—the most influential example being the successful launch of BlackRock’s tokenized fund, BUIDL. Undoubtedly, traditional financial capital will increasingly integrate with blockchain in the future.

On the regulatory front, the U.S. still lacks a unified framework for virtual asset regulation. However, this has not prevented U.S. regulators from cracking down on illegal activities (such as enforcement actions against KuCoin for violating anti-money laundering requirements), nor has it stopped traditional Wall Street players from gradually embracing digital assets (e.g., BTC ETFs, tokenized funds).

In contrast, both the EU and Hong Kong are actively building comprehensive regulatory frameworks for virtual assets (such as the EU’s MiCA and Hong Kong’s VASP licensing regime and various consultation papers). In practice, we can observe that these frameworks impose significant operational costs and compliance challenges on market participants.

Crypto Friendly is not Crypto Easy.

This article reviews key global Web3 and virtual asset regulatory developments and events in Q1 2024, covering the historic approval of BTC ETFs, regulatory enforcement against KuCoin and its founders, BlackRock’s tokenized fund BUIDL, the EU’s new AML rules for non-custodial wallets, and Hong Kong’s comprehensive push toward virtual asset compliance.

I. The Historic Approval of BTC ETFs

After a decade-long struggle, the arduous journey to approve a spot BTC ETF finally reached a breakthrough. On January 11, 2024, at 4 a.m., the U.S. Securities and Exchange Commission (SEC) simultaneously approved 11 spot BTC ETF applications. This milestone would not have been possible without Grayscale’s legal victory.

1.1 Grayscale's Legal Victory

On August 29, 2023, a U.S. federal court ruled in favor of Grayscale in its lawsuit challenging the SEC’s rejection of its spot BTC ETF application [1]. This decision accelerated the approval process for other major financial institutions like BlackRock and Fidelity.

Previously, the SEC had refused to approve spot BTC ETFs due to concerns about market manipulation and fraud. Although the SEC allowed futures-based BTC ETFs in 2021, it argued that futures products were less susceptible to manipulation because they were tied to prices on the Chicago Mercantile Exchange (CME), which is regulated by the Commodity Futures Trading Commission (CFTC).

However, in the Grayscale case, the judge agreed with Grayscale’s argument: if futures-based ETFs could be approved based on CME price surveillance, then spot BTC ETFs should follow the same logic. The court found that the SEC failed to justify its inconsistent treatment of similar products and deemed its refusal arbitrary and unlawful under administrative law. Ultimately, the court ordered the SEC to rescind its denial.

Following this ruling, the SEC shifted from passive resistance to active review, ultimately approving the ETFs with a 22-page order stating: "This order approves the Proposals on an accelerated basis."

Reference: Grayscale Wins a Battle for the Future — How Close Is the SEC to Approving a Spot Bitcoin ETF?

1.2 What Risks Did the SEC Identify in BTC ETFs?

ETFs themselves are long-established compliant financial instruments with no legal barriers. BTC is also uniquely classified by U.S. regulators—especially the SEC—as a “non-security” commodity. So what risks remain?

According to the 22-page approval document [2], the SEC identifies the risk as stemming from the unregulated nature of the underlying BTC spot market—specifically, the potential for price manipulation in the spot BTC market.

While each ETF has entered into Surveillance Sharing Agreements with regulated exchanges like CME to monitor futures markets, BTC spot trading does not occur on CME, leaving gaps in oversight.

The SEC reasoned that since BTC futures are already regulated products on CME, demonstrating a strong correlation between spot and futures prices would help mitigate manipulation risks. By analyzing data from Coinbase and Kraken since 2021, the SEC found a high degree of correlation between their spot prices and CME futures prices. This implies that any manipulation in the spot market would likely affect the futures market—and thus be detectable by CME’s monitoring systems, enabling regulatory intervention.

Manipulation risks primarily arise from market makers or traders on centralized exchanges (CEXs). To manage these risks, U.S. regulators have focused on bringing major exchanges like Coinbase and Kraken into compliance, while taking decisive enforcement action against the largest player, Binance, effectively forcing it into regulatory alignment.

Reference: The Regulatory and Legal Logic Behind the BTC ETF Approval

1.3 Divisions Among SEC Commissioners

Despite the final approval, there remains deep division within the SEC. In the official press release, SEC Chair Gary Gensler expressed caution [3]:

“Today’s approvals apply only to ETFs holding one non-security commodity, bitcoin. They should not be viewed as an endorsement of listing standards for any other crypto asset securities. Nor do they reflect the SEC’s views on the status of other virtual assets under securities laws, or on the widespread failure of certain market participants to comply with those laws.

As I’ve said before, the vast majority of virtual assets are investment contracts and therefore subject to securities regulations.

While the SEC remains neutral, I must note that commodities in traditional ETFs often have industrial or commercial uses, whereas BTC is primarily speculative and volatile, and widely used in illicit activities including ransomware, money laundering, sanctions evasion, and terrorist financing.

Although the SEC today approved the listing and trading of spot BTC ETFs, we have neither endorsed nor approved bitcoin itself. Investors should remain cautious regarding BTC and crypto-related products.”

Other commissioners raised concerns, arguing that spot and futures BTC ETFs are fundamentally different. Applying futures-market logic to regulate spot ETFs is inappropriate, they contend, because the BTC spot market lacks a central regulator capable of preventing price manipulation and fraud.

1.4 The Historical Significance of BTC ETF Approval

Regardless of the debate, the approval of BTC ETFs is historically monumental. It allows even those dreaming of crypto-punk ideals or overnight wealth to participate directly in shaping history’s powerful currents.

As Silicon Valley investor Chuan Wang (X: @Svwang1) noted: “In hindsight, January 10, 2024, may stand alongside August 13, 1971 (when Nixon severed the dollar from gold) and January 18, 1871 (the unification of Germany, leading Europe and the U.S. into the gold standard era), as pivotal moments in monetary history.”

II. Criminal Prosecution of KuCoin and Its Founders for Violating AML Regulations

On March 26, 2024, the U.S. Department of Justice filed criminal charges against cryptocurrency exchange KuCoin and its two founders for conspiring to operate an unlicensed money transmitting business and violating anti-money laundering (AML) compliance obligations under the Bank Secrecy Act [4].

U.S. prosecutors stated: “KuCoin and its founders deliberately concealed the fact that large numbers of U.S. users were trading on its platform, with daily volumes reaching billions of dollars and annual volumes in the trillions. Financial institutions like KuCoin must register with FinCEN and the CFTC and implement KYC/AML/CTF procedures. But KuCoin allegedly chose not to comply, turning itself into a safe haven for illicit money flows. KuCoin received over $5 billion and sent out more than $4 billion in suspicious and criminal funds.”

“Exchanges like KuCoin cannot have it both ways. Today’s indictment sends a clear message to all crypto platforms: if you serve U.S. customers, you must follow U.S. laws.”

Simultaneously, the CFTC filed a civil suit against KuCoin [5], accusing multiple KuCoin entities of violating the Commodity Exchange Act (CEA) and CFTC rules by offering off-exchange commodity futures, leverage, margin, and financing for retail commodity transactions without proper registration.

In essence, U.S. regulatory actions against KuCoin mirror those taken against Binance. As former U.S. Treasury Secretary Janet Yellen once said: “Any entity wishing to operate in the U.S. and benefit from its robust financial system must strictly comply with U.S. laws.”

III. BlackRock’s Tokenized Fund

In our previous analysis, we highlighted the critical role of tokenized funds in bridging traditional finance (TradFi) and decentralized finance (DeFi). Funds, due to (1) their existing regulatory oversight and (2) standardized digital representation, are ideal vehicles for real-world assets (RWA).

Reference: Comprehensive Report on RWA: The Value, Exploration, and Practice of Fund Tokenization

In March 2024, BlackRock launched its flagship tokenized fund, marking a major step forward.

3.1 What Is the Tokenized Fund BUIDL?

On March 21, 2024, BlackRock partnered with Securitize to launch its first tokenized fund, BUIDL (“BlackRock USD Institutional Digital Liquidity Fund”), on the public Ethereum blockchain. The BUIDL fund offers qualified investors opportunities to earn yield denominated in U.S. dollars through Securitize Markets [6].

Tokenization is a core component of BlackRock’s digital strategy. The launch of BUIDL marks a significant move into the tokenization of real-world assets (RWA) and brings substantial benefits to investors, including on-chain ownership issuance and trading, access to on-chain products, instant and transparent settlement, and cross-platform transferability of rights.

The BUIDL fund maintains a stable value of $1 per token, distributing interest via rebase mechanics—daily accrued dividends are paid directly as new tokens to investors’ wallets. The fund will allocate 100% of its assets to cash, U.S. Treasuries, and repurchase agreements, allowing investors to earn yield while holding assets on-chain. Most importantly, investors can transfer their tokens to other pre-approved investors 24/7/365, and the fund offers flexible custody options.

BNY Mellon will enable interoperability between digital and traditional markets, serving as custodian and administrator. Securitize will act as transfer agent and tokenization platform, managing share issuance and reporting subscriptions, redemptions, and distributions. Securitize Markets will serve as the sales agent for qualified investors. PwC has been appointed auditor. Additional custody partners include Anchorage Digital Bank, BitGo, Coinbase, and Fireblocks.

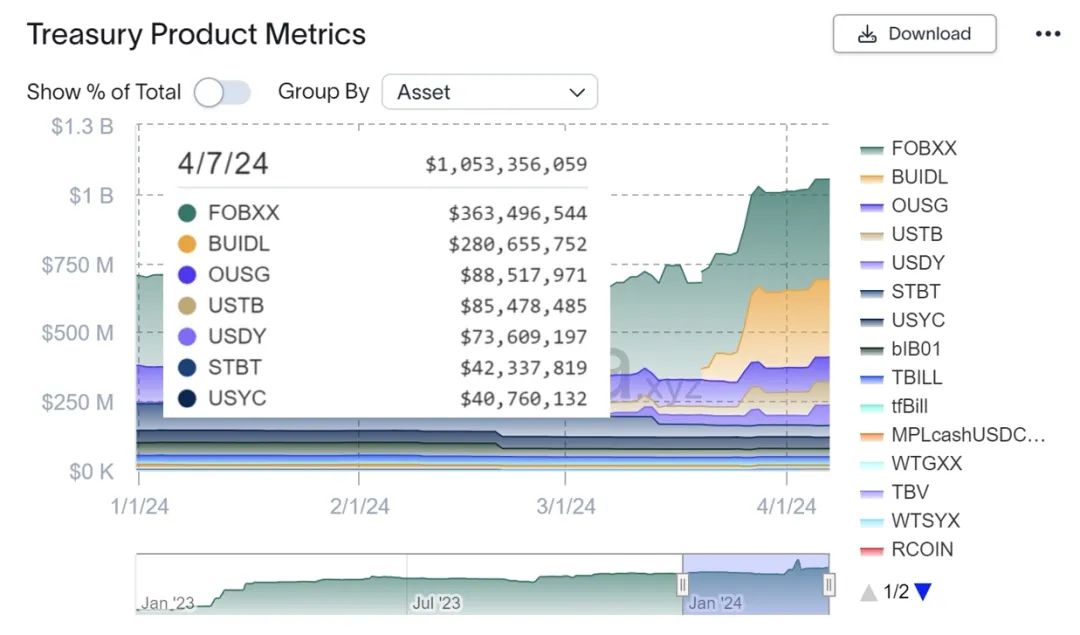

3.2 The Huge Potential of Tokenized Funds

From a TradFi perspective, tokenizing funds using blockchain and distributed ledger technology unlocks immense value.

BlackRock CEO Larry Fink stated in a Bloomberg interview that tokenization is the company’s next frontier: “We believe asset tokenization is the next big trend—meaning every stock and bond will eventually be recorded on a shared ledger.”

Additionally, UK regulators are actively exploring fund tokenization. The Investment Association declared that tokenization could enhance efficiency, transparency, and international competitiveness in asset management, publishing a report titled *UK Fund Tokenisation – An Implementation Blueprint* [7].

Although Franklin Templeton has already launched a tokenized fund on a public blockchain, BlackRock’s entry signals a transformative shift—opening the door for broader integration of traditional financial assets onto blockchains. The next frontier is clearly the tokenization of equity markets.

(https://app.rwa.xyz/treasuries)

IV. The EU’s New AML Rules for Non-Custodial Wallets

On March 23, 2024, according to Cointelegraph [8], EU regulators are updating AML regulations to require Know Your Customer (KYC) checks on commercial transactions involving non-custodial wallets.

This measure continues the EU’s efforts begun with the Markets in Crypto-Assets Regulation (MiCA), forming a key part of its broader AML strategy. The new AML law is expected to take effect in 2027—three years from now—working alongside MiCA to further restrict services to anonymous accounts.

(EU scraps proposed $1K payment limit for self-custody crypto wallets)

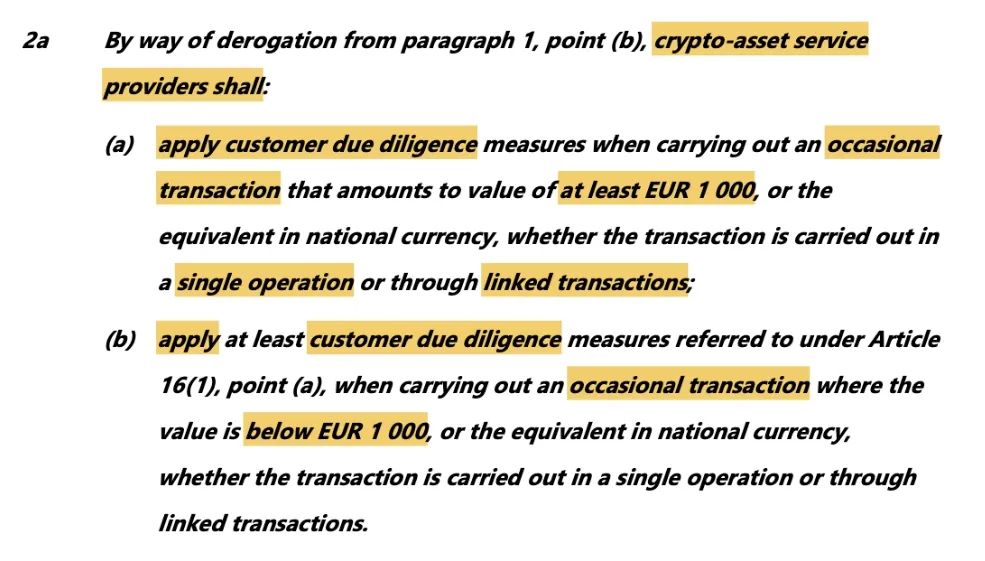

Under the new rules, Crypto Asset Service Providers (CASPs) operating in the EU must conduct customer due diligence and KYC for transactions exceeding €1,000 involving non-custodial wallets. Importantly, this applies only to CASPs regulated under MiCA (such as exchanges and custodial wallet providers): transactions between non-custodial wallets and CASPs above €1,000 will be regulated, but peer-to-peer transactions between non-custodial wallets remain outside the scope.

Undoubtedly, these regulations pose a significant challenge to cryptocurrency anonymity. After bringing CASPs under MiCA, the EU is now extending oversight to their interactions with non-custodial wallets. Once comprehensive regulation is in place, tax enforcement will likely be the next step.

Recently, both existing and prospective crypto service providers in the EU have been actively complying with MiCA requirements. EU member states are engaging in negotiations with industry players. Once fully implemented, these regulations will reshape the previously unregulated growth of the EU’s virtual asset market.

Large players will adapt and compete within the EU framework, while smaller ones may exit due to compliance burdens.

Reference: Can the Markets in Crypto-Assets Regulation (MiCA) Enable the EU to Fully Embrace Web3?

V. Hong Kong’s Comprehensive Move Toward Compliance

With the release of the *Policy Statement on the Development of Virtual Assets in Hong Kong* in October 2022, Hong Kong’s new Virtual Asset Service Provider (VASP) regime officially took effect on June 1, 2023—a landmark development for the city’s virtual asset industry.

To comprehensively regulate all virtual asset trading activities and meet FATF standards, the Hong Kong government has revised the Anti-Money Laundering and Counter-Terrorist Financing Ordinance and established a mandatory VASP licensing regime. Additionally, it has introduced regulations covering stablecoins, OTC onboarding/offboarding, and virtual asset custody—regulating all participants and forms of interaction within the ecosystem.

Although some areas beyond the VASP licensing regime are still in consultation or legislative drafting stages, they collectively outline a comprehensive regulatory framework.

For prior coverage of the VASP licensing regime, see: In-Depth Analysis of Hong Kong’s VASP Licensing Regime (Effective June 1, 2023).

5.1 Stablecoins

On December 27, 2023, Hong Kong’s Financial Services and the Treasury Bureau (FSTB) and the Hong Kong Monetary Authority (HKMA) jointly issued a public consultation paper proposing legislative measures to regulate fiat-backed stablecoin issuers [9].

Background: Given the growing importance of stablecoins in Web3 and the increasing interconnection between traditional finance and digital asset markets, the Hong Kong government sees the need to establish a regulatory regime for fiat-backed stablecoin issuers. A risk-based and flexible approach aims to appropriately manage potential risks to monetary and financial stability while providing clarity to support sustainable and responsible development of Hong Kong’s virtual asset ecosystem.

Key legislative proposals include:

(1) Licensing and supervision of fiat-backed stablecoin issuers. Issuers must meet strict licensing conditions and ongoing regulatory requirements before operating in Hong Kong. Regardless of their reserve mechanisms, all fiat-backed stablecoin issuers will be subject to the same regulatory framework. This means USDC and USDT issuers must obtain licenses to operate in Hong Kong.

(2) Regulation of entities promoting or distributing fiat-backed stablecoins. Only licensed stablecoin issuers, authorized institutions, licensed corporations, and licensed virtual asset trading platforms may offer purchase services or actively promote such services to the Hong Kong public. Only stablecoins issued by licensed entities may be sold to retail investors; others may only be offered to professional investors. Unlicensed issuers like USDC or USDT can still operate through licensed OTC providers—but only for professional investors.

Hong Kong’s stablecoin regulation focuses specifically on fiat-backed stablecoins, excluding other types (e.g., gold-backed). The regime adopts a risk-based approach and follows the principle of “same business, same risk, same regulation.” The government retains the right to adjust the scope as the market evolves.

Alongside the consultation, the HKMA launched a “sandbox” for stablecoin issuers to communicate regulatory expectations and gather feedback to inform final rulemaking [10].

5.2 Over-the-Counter (OTC) Virtual Asset Transactions

On February 8, 2024, the FSTB published a consultation paper titled *Proposed Legislative Measures to Regulate OTC Virtual Asset Transactions* [11], proposing to establish a new licensing regime under the Anti-Money Laundering Ordinance, with Hong Kong Customs as the regulator. Any person conducting OTC virtual asset trading services in Hong Kong must obtain a license from the Commissioner of Customs.

OTC virtual asset services are defined as:

(a) Providing spot trading services for any virtual asset as a business, excluding peer-to-peer personal transactions;

(b) Regardless of whether services are provided via physical outlets (including ATMs) or online platforms; excludes parties not contractually involved in transactions (e.g., platforms merely displaying listings without participating in trades);

(c) Explicitly excludes licensed virtual asset trading platforms already covered under the VASP regime.

Consistent with the “same business, same risk, same rules” principle, the proposed regime aims to cover all forms of OTC virtual asset service providers.

The government proposes that anyone operating an OTC virtual asset business in Hong Kong or actively promoting such services to the Hong Kong public must obtain a license from the Commissioner of Customs and meet fit-and-proper criteria and other regulatory requirements.

“Active promotion” may be assessed based on factors such as having a detailed marketing plan, using promotional channels (internet, newspapers), and systematic outreach efforts.

5.3 Virtual Asset Custody

On February 20, 2024, the HKMA released guidance on virtual asset custody activities, setting out clear standards for governance, risk management, client asset segregation and protection, delegation, and outsourcing for institutions applying for Trust and Company Service Provider (TCSP) licenses [12].

Background: As the virtual asset industry grows, the HKMA observes increasing interest among authorized institutions in offering virtual asset custody services. To ensure adequate protection of client assets and proper risk management, the HKMA deemed it necessary to issue formal guidance.

While VASP licensing already includes custody requirements—for example, requiring exchanges to hold client assets in trust via wholly-owned subsidiaries—this updated guidance further clarifies operational models and strengthens investor protections.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News