"User-Set Interest Rates": How Will Liquity V2 Shake Up the Stablecoin Lending Market?

TechFlow Selected TechFlow Selected

"User-Set Interest Rates": How Will Liquity V2 Shake Up the Stablecoin Lending Market?

Liquity V2 aims to create an efficient interest rate market between lenders and borrowers through a "user-set interest rate" mechanism.

Compiled by: 1912212.eth, Foresight News

Currently, the crypto industry lacks any protocol capable of creating an efficient interest rate market between borrowers and stablecoin holders.

In DeFi, we have:

-

Fixed one-time fees – e.g., Liquity V1

-

Governance-determined interest rates – e.g., MakerDAO

-

Algorithmically controlled rates – e.g., crvUSD

Each of these systems involves different trade-offs:

-

Fixed-rate protocols cannot adapt to high-interest-rate environments;

-

Governance can be slow and arbitrary;

-

Algorithmically controlled rates are prone to volatility and hard to predict.

How does Liquity V2 solve this dilemma?

Compared to money markets with large spreads between lenders and borrowers, Liquity V2’s “user-set interest rate” mechanism enables fast, adaptive adjustments that narrow the gap between both sides.

To understand how user-set interest rates work—and why borrowers would willingly pay above 0%—we first need to understand what keeps Liquity’s stablecoin stable.

Reviewing Liquity’s Liquidity Mechanism

In April 2021, Liquity V1 launched the first CDP system with a built-in redemption mechanism, introducing a downwardly protected stablecoin not reliant on centralized collateral.

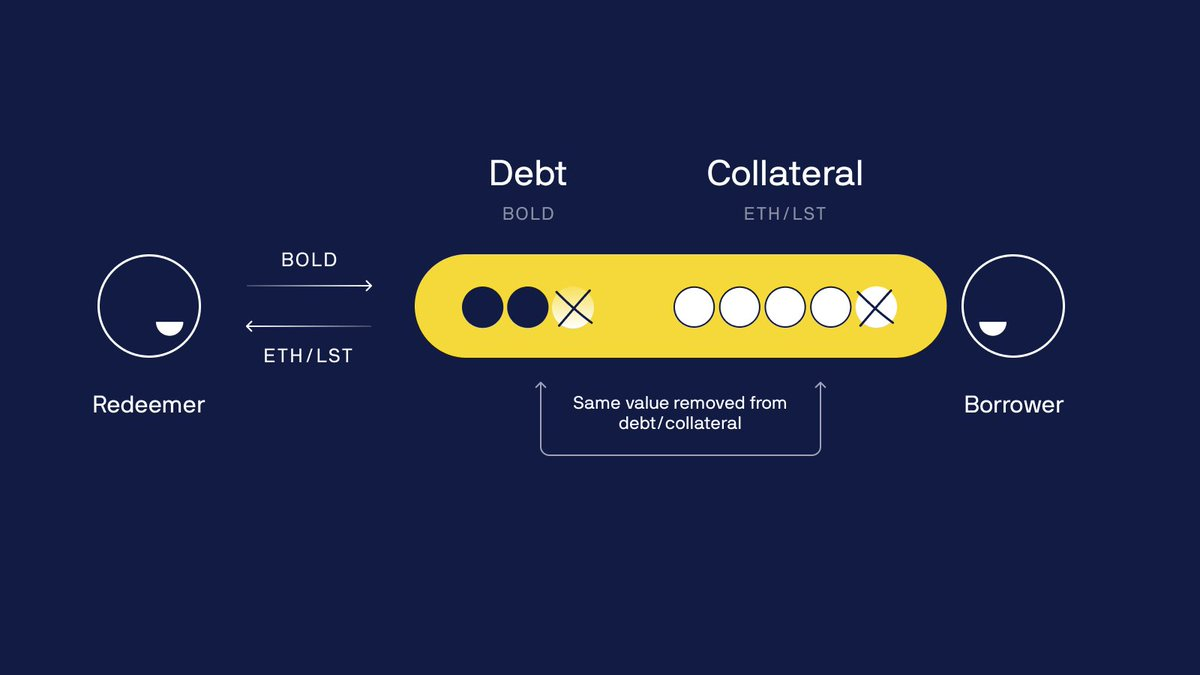

The redemption feature allows any LUSD holder to exchange their stablecoin for ETH worth $1.

When LUSD trades below $1, users can buy it at the market price (e.g., $0.99) and redeem it with the protocol at $1.

While this mechanism maintains a hard floor near $1 through direct arbitrage (minus fees), it impacts the riskiest borrowers because redeemed LUSD is used to repay loans with the lowest collateral ratios in exchange for equivalent ETH.

Affected borrowers see equal reductions in both their collateral and debt value, meaning no net loss—but reduced ETH exposure.

Why is this a problem?

Due to rapidly rising market interest rates over recent months, borrowing demand has outpaced holding demand for LUSD, causing excessive sell pressure and triggering redemptions. As a result, many LUSD borrowers have raised their collateral ratios to unprecedented levels just to avoid being redeemed against.

This severely undermines Liquity V1’s ability to provide highly capital-efficient loans in today’s high-DeFi-rate environment.

Liquity V1, being essentially interest-free with fixed costs and reward schemes, has proven reliable in low-rate environments and remains a viable option for borrowers under such conditions. However, in high-rate environments, users tend to seek stablecoins with higher yields.

Clearly, floating rates are better suited to sustainably and flexibly respond to various market conditions. At the same time, the redemption mechanism remains critical in preventing stablecoins from losing their peg: many existing stablecoins have suffered downward peg deviations under high sell pressure.

What is the “user-set interest rate”?

With user-set interest rates, redemptions seamlessly integrate with dynamic rates: in Liquity V2, redemptions will occur in ascending order of individual interest rates, rather than targeting loans with the lowest collateral ratios.

Thus, borrowers with lower interest rates face the highest risk of redemption. Users can freely manage their redemption risk by adjusting their rate relative to peers (or delegate management to third parties).

Based on individual risk tolerance, the market establishes a range of personal interest rates. Borrowers willing to accept redemption risk may set rates below average to enhance capital efficiency, while more risk-averse or “set-and-forget” borrowers may opt for above-average rates to gain security.

Contrary to most existing CDP protocols, in V2, interest income will be autonomously reinvested—with minimal human governance—to incentivize stablecoin demand and liquidity. For safety and efficiency, most revenue flows into the Stability Pool (SP), boosting stablecoin demand and protocol solvency.

Additionally, a significant portion of revenue is directed to LPs on external AMMs to ensure sufficient stablecoin liquidity across multiple pairs, such as PIL (Protocol-Incentivized Liquidity). Since fees are collected as interest, this ensures continuous and smooth incentives for both SP and LP depositors.

The New Stablecoin: BOLD

The core new stablecoin in Liquity V2 will be named BOLD. It enables a market-driven mechanism where interest rates are no longer decided by a few but chosen by the majority. User-set interest rates also influence how the BOLD peg mechanism operates.

When BOLD trades above $1, redemption risk is low, so borrowers tend to lower their rates. This makes borrowing and leveraging ETH (and LSTs) more attractive, while holding BOLD becomes less appealing.

Conversely, when BOLD falls below $1, borrowers face higher redemption risk and may raise their rates. Consequently, borrowing becomes less attractive, while increased interest payments boost stablecoin yields, raising demand for BOLD and pushing its price back up.

User-set interest rates should prevent collateral ratios from being pushed to unreasonable levels, instead achieving a capital-efficient balance between borrowers and stablecoin holders in a fully market-driven way.

Borrowers will be able to truly benefit from Liquity V2’s loan-to-value ratios, accessing as much capital as possible based on their chosen collateral, within the limits of their acceptable liquidation risk.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News