10 DeFi Trends on Solana to Watch in 2024

TechFlow Selected TechFlow Selected

10 DeFi Trends on Solana to Watch in 2024

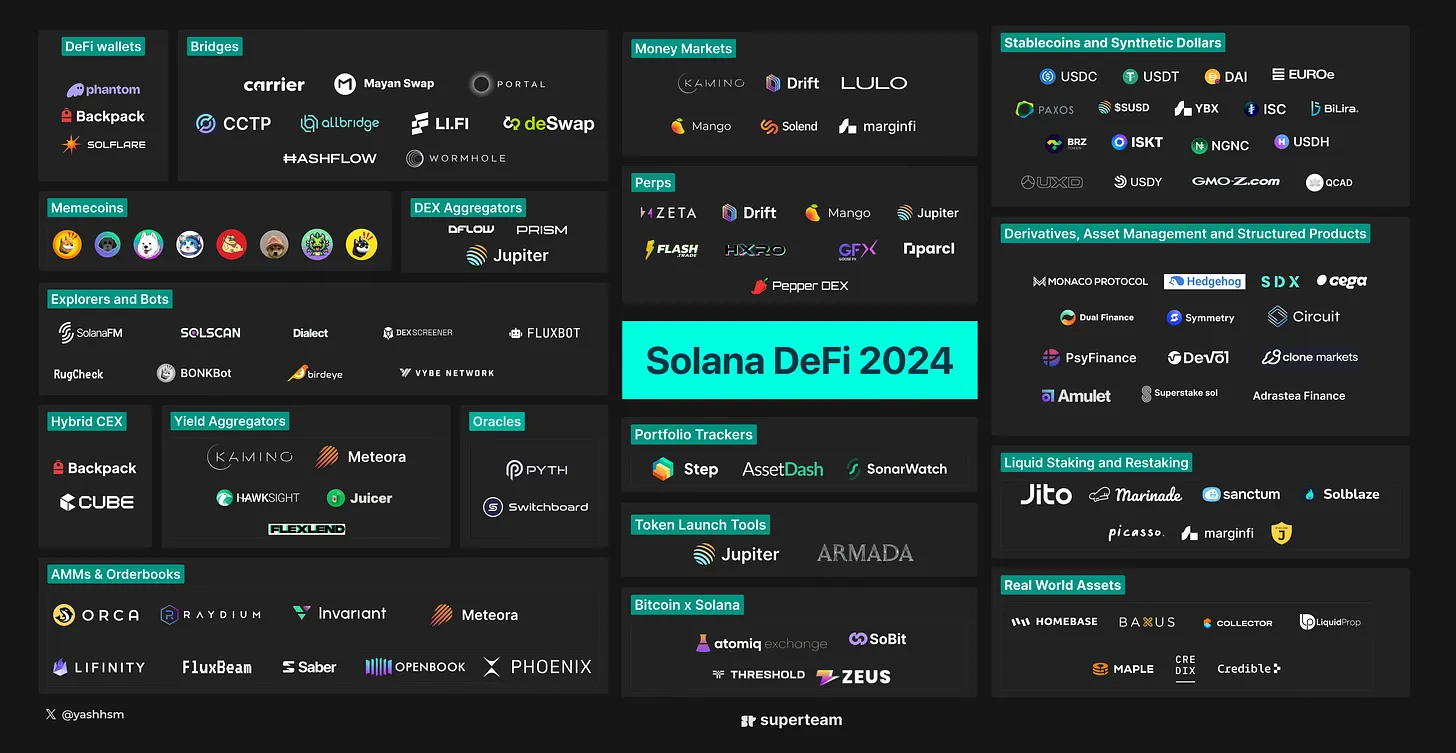

Solana has one of the strongest aggregators, with Jupiter leading the way.

Author: YASH AGARWAL

Translation: TechFlow

Introduction

Solana DeFi is performing exceptionally well, with both total value locked (TVL) and daily DEX trading volume exceeding $4 billion. Led by top-tier DeFi 1.0 protocols such as Marinade, Phoenix, Jito, MarginFi, Kamino, BlazeStake, Solend, Jupiter, Meteora, Orca, Raydium, Lifinity, Sanctum, and Drift, the Solana DeFi ecosystem is in full swing. These teams have weathered the FTX collapse, built through bear market lows, and are now reaping the rewards.

However, newer entrants into the Solana DeFi ecosystem have shown relatively lackluster performance, partly due to a lack of fresh narratives and limited focus on Solana’s new Only Maybe (OPOS) mechanisms.

Now is the time to explore new DeFi ideas and encourage more builders to innovate within DeFi, thereby boosting economic activity on Solana.

This article aims to present the top 10 themes, each containing promising opportunities worth exploring. While we focus on Solana, some of these themes can also apply to other high-performance blockchains.

In this article, we will discuss:

-

DeFi Stablecoins

-

LSTs, MEV, and Restaking

-

Money Markets

-

Interest Rate Derivatives

-

RWA and DeFi Composability

-

Perpetuals and Derivatives

-

DeFi Infrastructure

-

MemeFi and Social DeFi

-

Protocols Evolving into Platforms

-

Interfaces (UX Aggregators)

Theme 1: DeFi Stablecoin Mechanisms Will Become More Diverse

We need more DeFi-native stablecoins serving as DeFi money, forming liquidity pairs across DEXs and lending protocols. Primarily, their utility is yield-driven. However, DeFi stablecoins currently lack practicality as mediums of exchange (i.e., for transactions).

Stablecoins or synthetic dollars can be broadly categorized as follows:

-

Fiat-backed stablecoins such as USDC, USDT, and EURC. M0 is another upcoming stablecoin player on Ethereum.

-

CDP-based stablecoins such as DAI and Frax.

-

LST-backed stablecoins, including:

-

CDP structures like Lybra’s eUSD and Prisma’s mkUSD.

-

Delta-neutral projects such as Ethena and Resolv Labs (UXD on Solana was a pioneer).

-

RWA-backed stablecoins such as USDV, USDY, USDM, and ISC.

-

Synthetic versions issued by perpetual DEXes such as Synthetix (sUSD) and Aevo (aUSD).

-

Algorithmic stablecoins such as Gyroscope, which uses isolated vault reserves to reduce correlation risks and implements dynamic stabilization mechanisms using declining bond curves for redemptions.

On Solana, two LST-backed stablecoins are emerging: MarginFi’s YBX and Jupiter’s SUSD, along with early-stage projects like Surge Finance.

Alpha for Builders:

-

Explore updated design mechanisms inspired by Ethereum stablecoins.

-

Go-to-market strategy: Most stablecoins struggle with initial liquidity and traction; since primary utility is yield, this presents an interesting angle. For example, increasing DAI’s Enhanced DAI Savings Rate (EDSR) led to a ~$1.5 billion increase in DAI deposits (about 30% of total DAI supply). USDV offers yield to verified miners such as DeFi projects to boost circulation, and could further reward its users (think how Arbitrum DAO distributed ARB to projects that incentivized user engagement).

-

Ethena, Ethereum’s hottest stablecoin (with over $1.3 billion in issuance), is soon launching on Solana. One could also build a “Solena” with Ethena-like mechanics but using SOL. However, CEX listings for Solana LSTs and depth in SOL perpetuals remain key hurdles—but they’re likely coming.

The Case for On-Chain Foreign Exchange (FX) Markets

The FX market is massive, with over $6 trillion traded daily. The emergence of fiat-backed stablecoins with sufficient liquidity could pave the way for spot FX markets on-chain via order books and AMMs. Imagine merchants accepting USDX payments and instantly swapping them to YENX, routing trades via Jupiter across multiple liquidity venues. Someone will eventually build a spot FX trading platform on Solana.

Theme 2: (Re)staking and LSTs – The Monetization of SOL

Solana’s LST landscape is now consolidated around three main players: Jito, Solblaze, and Marinade. Sanctum is another interesting player in the LST space, addressing liquidity issues and offering LST-as-a-service. Still, the number of LSTs remains low, and more LSTs would benefit network decentralization. Additionally, LSTs are major contributors to DeFi—increasing their deposits in lending/borrowing markets or LP pools would boost on-chain TVL.

Alpha for Builders:

-

More LSTs: With token launch hype and incentives, new LSTs still have a chance to capture significant market share. For example, Solblaze leveraged BLZE incentives and focused on DeFi integration, growing from 30K SOL to 3M SOL in just eight months.

-

Another approach is adopting novel design mechanisms. For instance, mirroring Frax Ether (over $1B TVL), which uses a dual-token model:

-

frxETH: Pegged 1:1 to ETH, does not accrue staking yield.

-

sfrxETH: Accrues staking yield.

-

This enables higher yields for staked ETH while ensuring frxETH has deep liquidity and broad ecosystem integration. Compared to peers like rETH, frxETH enjoys higher DeFi TVL due to Fraxlend integration and liquidity incentives.

-

Validator-led LSTs: As MEV and priority fees grow, we may see validators launching their own LSTs and sharing more rewards with delegators to attract stake. Sanctum is a key project driving this shift.

-

LST yield maximizers: For example, Kamino Multiply offers one-click vault products designed for leveraged LST yield through looping (stake LST, borrow SOL → restake SOL → repeat). This space can support many such products (discussed later).

-

SOL restaking: Solana has an opportunity to adopt Ethereum-style shared security/restaking layers, allowing projects to further boost yields by restaking and accessing top validators. Unlike Ethereum, where AVSs are rollups/application chains/bridges requiring economic security, Solana hasn’t embraced modularity yet.

Still, this is worth exploring—AVSs on Solana could include Clockwork-style Keeper networks, Pythnet-style application chains, or any economically secured, “SOL-aligned” network like DePIN. If Rollapp/application chain narratives gain traction on Solana, the restaking story could become huge!

-

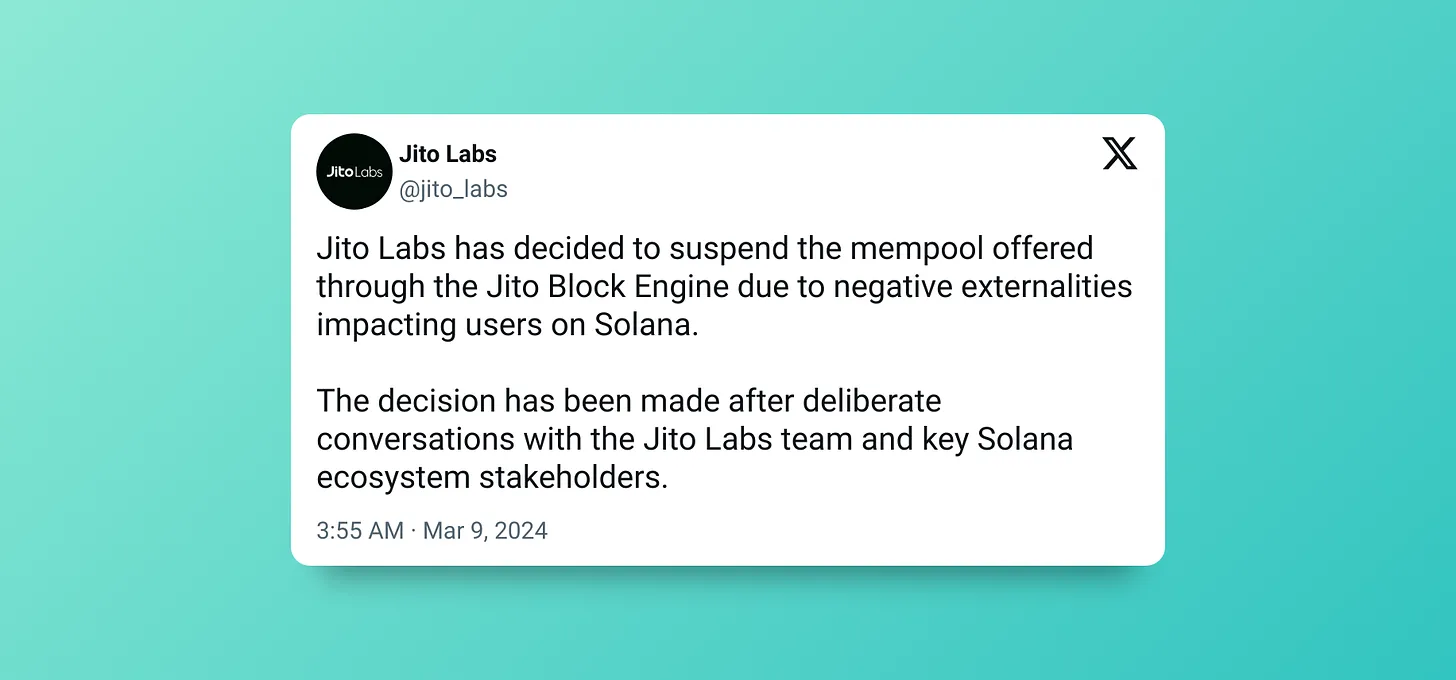

On MEV: Recently, Jito Labs paused mempool services via its Jito Block Engine due to rising sandwich attacks. This decision sparked mixed reactions—some praised Jito’s proactive stance, while critics argued it might push trade flow off-chain or spur private mempools.

As DeFi activity grows, MEV will only increase—projects (and LSTs) can capitalize on this.

Compared to Ethereum, the amount of SOL in LSTs remains disappointing (<5%), which needs to be addressed. Overall, it’s time to enhance SOL’s monetization so price appreciation of SOL is captured by the DeFi ecosystem.

Theme 3: Next-Gen Money Markets

While core money markets (lending) like Solend ($300M), MarginFi ($800M), and Kamino ($1.1B) are established, it’s time to innovate in design mechanisms to improve efficiency. For example, MarginFi still lacks eMode (a feature from Aave v3) to boost capital efficiency.

Focus on higher capital efficiency: As blue-chip lending/borrowing platforms like MarginFi and Kamino distribute points and issue tokens, users will demand better capital efficiency—especially in liquid staking markets.

Alpha for Builders:

-

New design mechanisms: Some interesting mechanisms explored by EVM projects include:

-

Alchemix’s self-repaying loans allow leveraging a basket of tokens without liquidation risk.

-

Euler v2’s modular architecture consists of ERC-4626 credit vaults (lending pools) connected via Ethereum Vault Connector (EVC) contracts. This allows permissionless creation and activation of lending vaults with custom configurations (e.g., choosing collateral, oracle, TVL, interest rates). It creates network effects and compounds liquidity—vault shares can serve as collateral in any other vault within the Euler ecosystem.

-

Morpho Blue enhances capital efficiency.

There's no harm in drawing inspiration from upcoming Ethereum protocols and innovative designs—better than just forking Aave v3.

-

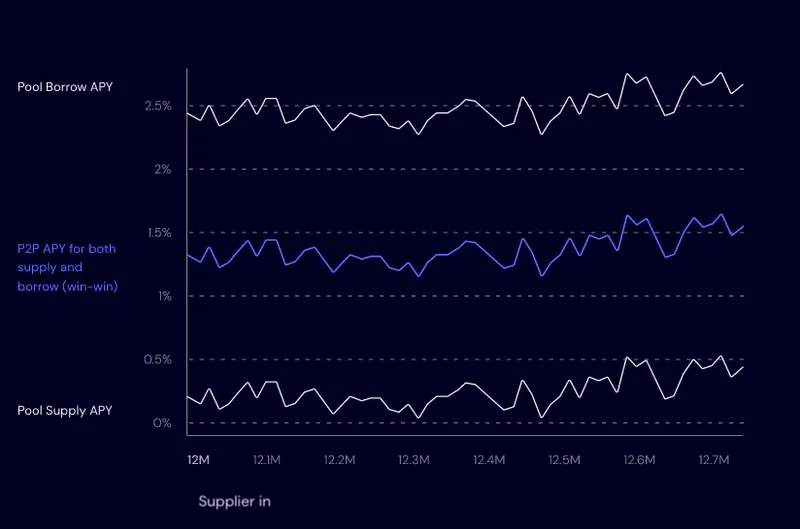

Optimizers for existing money markets: Take MarginFi’s SOL market—the gap between lending and borrowing rates is substantial, a common issue across all markets. This stems from liquidity pool inefficiencies—low utilization leads to lower yields: [Supply Rate = Borrow Rate × Utilization].

A potential solution is building something like Morpho Optimizer, where supplied liquidity is dynamically matched peer-to-peer when borrowers appear (effectively achieving 100% utilization). For matched liquidity, lenders earn the same rate as borrowers—matched lenders don't share interest. In unmatched cases, it falls back to underlying lending pools like MarginFi or Kamino. Altitude is another good reference. Flexlend and JuicerFi are well-suited to build this.

-

Fixed-rate loans: Most P2P lending protocols (e.g., MarginFi, Solend) currently use floating (variable) rates, leading to wide spreads at low utilization—essentially creating a TradFi-style banking system with high spreads mediated by pools. Fixed-rate loans offer a solution.

Fixed-rate loans represent less than 1% of DeFi, while dominating ~98% of TradFi, due to several reasons:

-

Passive: Peer-to-pool models lack maturity dates, requiring far less maintenance.

-

Lindy Effect: Floating rates are battle-tested, creating a Lindy effect akin to sticky TVL.

As noted in Delphi's report, fixed-rate lending in DeFi remains underdeveloped. Yield Protocol shut down, Notional Finance v2 collapsed (launched with $1B TVL, now down to $17M), signaling weak demand. Notional v3 pivoted to variable loans and leveraged vaults. Exactly Finance gained momentum with novel ideas but relied heavily on OP incentives and native token emissions. Term Finance is another project to watch. A team solving key challenges (e.g., easy loan maintenance) with strong incentives could capture a large latent market.

Lulo Finance (same team as Flexlend) has experimented with this on Solana but hasn’t gained significant traction. While fixed-rate loans face issues and may seem “ahead of their time,” exploration is worthwhile.

-

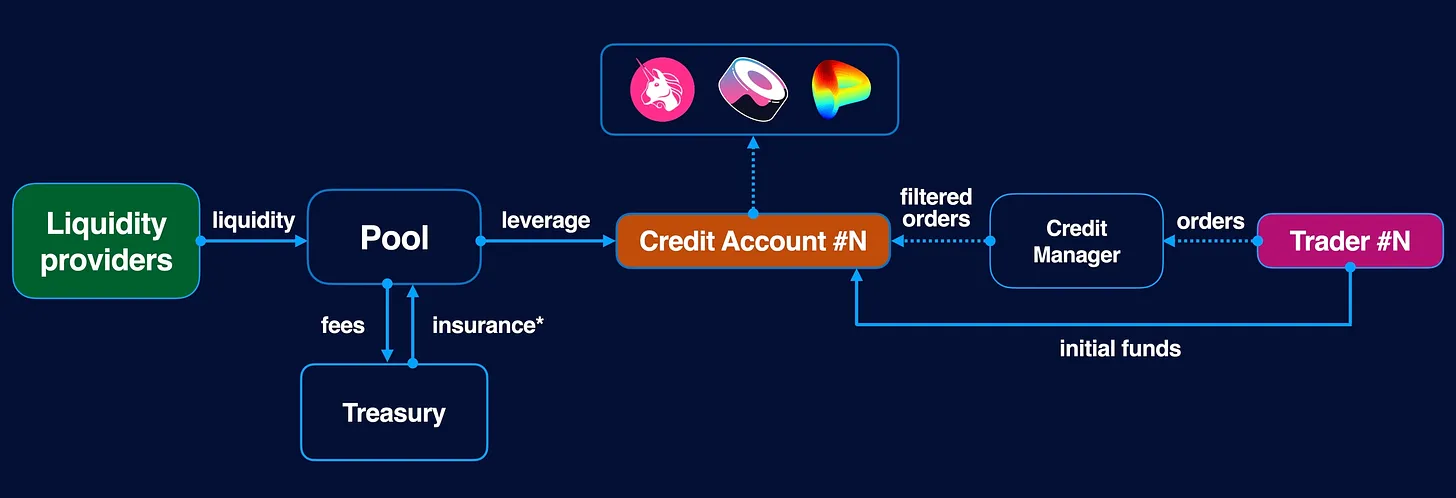

Gearbox for Solana: Gearbox is a composable leverage protocol (leverage via borrowing, with ecosystem-wide integrations). Solana is inherently composable and could integrate with AMMs, LSTs, and more. If markets turn bullish and more projects launch high-APY incentive programs, they could plug into such a protocol for leveraged liquid staking.

A related idea could be corporate debt—on-chain revenue-generating companies issuing bonds to raise capital. Think of it as revenue-based financing (RBF), but on-chain and fully transparent. This allows profitable on-chain entities to raise funds without diluting their tokens.

Theme 4: Interest Rate Derivatives – The Untapped Frontier

Interest rate derivatives (IRDs) are the second-largest market after FX, with a notional value of $450–600 trillion. Direct comparison with TradFi may not be meaningful, but the nascent nature of DeFi (especially on Solana) presents massive opportunities. Beyond generating yield via asset management contracts, this could foster organic yield generation.

Alpha for Builders:

Drawing inspiration from TradFi, some intriguing ideas include:

-

LST Interest Rate Swaps: A forward contract allowing parties to exchange fixed for floating rates (or vice versa). Simply put, if you want a fixed staking yield, you can enter an agreement with someone willing to take on variable staking risk.

This would appeal strongly to a new class of institutional and retail clients seeking DeFi exposure without excessive speculation. In TradFi, swaps occur between institutions; in DeFi, they’d be peer-to-peer. Users could choose to pay or receive fixed yields. LSTs like JitoSOL or mSOL are ideal target assets via dividend rate swaps (SRS), as they represent the “risk-free rate” of SOL in DeFi.

-

ERC-4626 is Ethereum’s standard for yield-bearing token vaults, ensuring composability across all vaults with >$10B TVL. Building and driving adoption of a similar standard on Solana could be pivotal. It could unlock a suite of vault products, such as Sommelier.

-

Yield stripping for Solana (Pendle): Yield stripping is a cash flow discount game. Users get predictable returns from future value, while speculators acquire future assets at a discount. It involves separating interest payments from principal. Pendle implements yield tokenization in this manner.

Examples of tradable Solana yields include: liquid-staked SOL, Lifinity revenues, Meteora Pool yields, Kamino_Finance kTokens, and Solend Protocol cTokens (yield-bearing deposit receipts).

An early-stage project called Exponent is exploring this direction, starting with MarginFi loan yield trading, then expanding to other yield derivatives. Solana DEX is also exploring a “Pendle for Solana.”

Theme 5: Making RWA Composable with DeFi

With more RWAs coming on-chain—especially liquid, yield-bearing assets like Treasuries—the logical next step is enabling composability. Most RWAs are permissioned due to KYC and regulatory constraints. However, Ondo launched USDY (tokenized Treasuries) as permissionless, opening a new design frontier. Ondo also demonstrated an interesting mechanism for tokenizing equities—if executed well, it could spark another wave of DeFi composability.

Alpha for Builders:

-

Token Extensions: There are abundant opportunities in RWA, especially leveraging token extensions. Our article dives deeper into these details.

-

TradFi Giants: As giants like Franklin Templeton, BlackRock, and Fidelity pilot RWAs on Solana, massive opportunities could unlock in the next 1–2 years. Initially, these may be permissioned, but building permissionless wrappers and deeper DeFi integrations (e.g., Flux Finance for lending) could be key. For example, holders could achieve higher yields by tokenizing U.S. Treasuries, pledging them as collateral on DeFi lending markets, borrowing stablecoins, buying more Treasuries, and repeating the cycle.

It’s rumored BlackRock funds could be composable with USDC.

Theme 6: The Era of Derivatives Has Arrived!

During the last bull run, structured products and on-chain derivatives (excluding perpetuals) were all the rage. Especially on Solana, before the bear market hit, DeFi Options Vaults (DOVs) via protocols like Ribbon, Katana, and Friktion saw TVL surge past $500M. Now, with the bull market returning and demand for yield rising, it’s no surprise these products are making a comeback.

Alpha for Builders:

-

Vertical Perpetuals or Prediction Markets: Just as Parcl allows long/short positions, people could build perpetuals for different verticals like commodities. This is a highly creative category—Parcl created hype and attracted over $100M TVL.

-

Power Perpetuals: An idea proposed by Paradigm in 2021 here, which didn’t take off last cycle due to timing, but is worth revisiting this cycle. Several protocols like Exponents are experimenting with this on Berachain. Another adjacent idea is exploring Everlasting Options (think perpetuals to futures, what would that be for options?), proposed by SBF.

-

Perpetual Aggregators: Just as we have aggregators for lending and spot DEXs, despite design challenges, building a perpetual aggregator is a big enough opportunity. With perpetual aggregators like Rage Trade and MUX emerging, a similar trend could emerge on Solana—especially for designs like Flash and Jupiter.

-

Perpetuals on Solana App-Chains: In the EVM world, most order-book-based perpetual DEXes—like Aevo, dYdX, and Hyperliquid—are transitioning to their own app-chains. In the future, Solana perpetual DEXes could do the same, offering benefits such as:

-

Immunity from mainnet congestion

-

Improved trading experience for users (gas-free trading for traders)

Indeed, Zeta has already started moving in this direction.

-

Structured Products: Build something like Friktion. In fact, Friktion’s code is still available for anyone to fork. Asset management protocols like Investin (a prior Flash team project) could also make a comeback. Order books like Phoenix or Drift require active liquidity provision, which could be enabled via market-making vaults. This ensures decentralized market-making—otherwise, all liquidity would be controlled by market makers (we saw what happened with Alameda post-FTX crash).

-

On-Chain Options: Protocols like Ribbon, Ava, and Gravity Markets serve as examples of existing on-chain options platforms. One could also build binary options like Decalls (i.e., price up/down), but gaining traction and building moats is crucial.

-

HXRO: As a foundational layer for Solana derivatives and liquid staking, builders can develop on top of:

-

Dexterity, Hxro’s derivatives protocol, provides fundamental building blocks (for traditional DEX UIs, advanced trading terminals, APIs, etc.), offering all necessary risk and exchange infrastructure for on-chain expiry, perpetuals, zero-day futures, and other margin-based derivatives markets.

-

Hxro’s parimutuel protocol powers on-chain betting apps via a “smart” AMM that enables event betting with continuous liquidity. It supports various on-chain betting markets for gaming, sports, crypto, and other events.

Theme 7: Building Infrastructure and Tools for DeFi Protocols

With several billion-dollar DeFi protocols on Solana, now is the perfect time to build infrastructure and tools for them.

Alpha for Builders:

-

OEV: A subset of MEV, Oracle Extractable Value (OEV) arises when applications rely on oracle updates, allowing arbitrageurs or liquidators to exploit state inconsistencies. As highlighted by multicoin, there’s an opportunity for apps to capture OEV.

-

DeFi Infrastructure-as-a-Service: Many protocols like Aave/Compound have been forked repeatedly; similarly on Solana, protocols forked Solana Lab’s reference implementation. Development, auditing, and maintenance incur significant costs. Standardizing and establishing a sustainable dev firm offering “plug-and-play DeFi protocols”—akin to “Metaplex for DeFi”—could work. Rari Capital (now defunct) had a similar vision, building vault infrastructure. One outcome could be building ERC-4626-equivalent infrastructure for Solana and monetizing Solana’s yield narrative by providing services to DeFi projects.

-

Risk Management Organizations: These could operate as risk DAOs or advisory boards conducting research and risk analysis for DeFi protocols. They could publish public “risk dashboards” with key Solana ecosystem metrics and offer paid research, risk assessment frameworks, and risk rating services to DeFi projects.

-

Bribery Aggregators or Markets: In EVM, Curve Finance lets token holders decide how much incentive to allocate to each pool. This created dynamics where projects “bribe” voters to vote for pools containing their tokens. Votium Protocol aggregates these bribes and automatically votes on behalf of token holders to maximize received incentives. An aggregator simplifies coordination between bribe givers and voters, improving market efficiency. On Solana, this could apply to:

-

LSTs directly delegating voting power to validators via governance tokens

-

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News