Exploring the Frenzied Crypto Market: Where Is the Next Narrative Headed?

TechFlow Selected TechFlow Selected

Exploring the Frenzied Crypto Market: Where Is the Next Narrative Headed?

Digital currencies are rising, airdrops are coming non-stop, but the euphoria of a market peak has yet to arrive.

Author: Ignas

Translation: Luccy, BlockBeats

Editor's note: With Ethereum’s Dencun upgrade approaching and the Bitcoin halving on the horizon, crypto market sentiment is rising alongside Bitcoin breaking past $60,000. Against this backdrop, crypto researcher Ignas offers an in-depth analysis of current cryptocurrency market dynamics and shares forward-looking perspectives on major blockchain projects such as Ethereum, Bitcoin, and Solana.

The article explores technical upgrades, market performance, and potential risks across various blockchain projects, providing unique insights into key trends and development directions within the cryptocurrency space.

Digital currencies are rising, airdrops are flowing, yet the euphoria of a market peak has not yet arrived.

So where do we stand now, and what might happen over the coming months?

I believe there are several crypto-native catalysts that support continued bullish momentum. But first, I’d like to share this week’s airdrop farming opportunities.

This Week’s Airdrop Farms

-

Ethena: If you hold stablecoins, here’s finally a farm tailored for you. Ethena’s USDe generates a 27% annualized yield through a triangular arbitrage strategy. Convert to USDe and provide liquidity to Curve pools to earn points. I’ll share more thoughts on Ethena in this blog post.

-

FlashTrade: FlashTrade enables trading in gold, silver, forex, and cryptocurrencies. It’s an underdeveloped protocol on Solana. Its unique feature is dynamic NFTs that evolve based on trading history. No token has been launched yet.

-

Nostra: Lending and trading on Starknet. I’m bullish because Cairo, the development language, limits the deployment of major lending protocols like Aave on Starknet. This positions Nostra (or zkLend) as a primary liquidity hub on Starknet.

-

Merlin Chain: A new and popular BTC Layer 2 solution backed by OKX. Stake BTC, ETH, stablecoins, or Bitcoin-native assets to earn points via farms. 20% of the total MERL supply will be distributed through airdrops.

This is my third crypto cycle, and each one seems increasingly wild. Numbers no longer matter, as irrational FOMO buying draws in retail players who don’t understand market caps or fully diluted valuations.

In November 2023, I wrote about navigating bull markets amid chaos.

We’re not there yet—meme indicators of a market top haven’t appeared: Coinbase hasn’t topped the Apple App Store, there were no crypto ads during the Super Bowl, and retail FOMO hasn’t kicked in.

How Inflated Is the Current Market?

In my personal experience, the second most important article focuses on how we create new narratives to issue more tokens at higher valuations.

In 2017–18, the entire crypto market bubble was inflated by ICO tokens—lacking technological innovation and supported only by whitepapers and compelling stories.

The 2020–21 bull run was more complex.

Leverage rapidly accumulated in both DeFi and CeFi. Leverage piled up on Grayscale’s “Widowmaker” trade, while centralized lenders borrowed from each other with little clarity on where funds actually went.

DeFi expanded due to innovations like yield farming (rewarding governance tokens for providing liquidity) and lending protocols (e.g., Aave and Maker) enabling on-chain leverage.

We also invented new token models like Olympus OHM (the 3,3 Ponzi scheme) and SNX (for minting sUSD) to capitalize on their ecosystems.

The problem is that with every new bull cycle, minting tokens becomes easier. Before ERC20, token creation was difficult. Bitcoin forks like Bitcoin Cash, SV, and Gold required expensive PoW machines.

So where are we now in the 2024–25 bull market bubble?

Yes, bubbles always form in crypto.

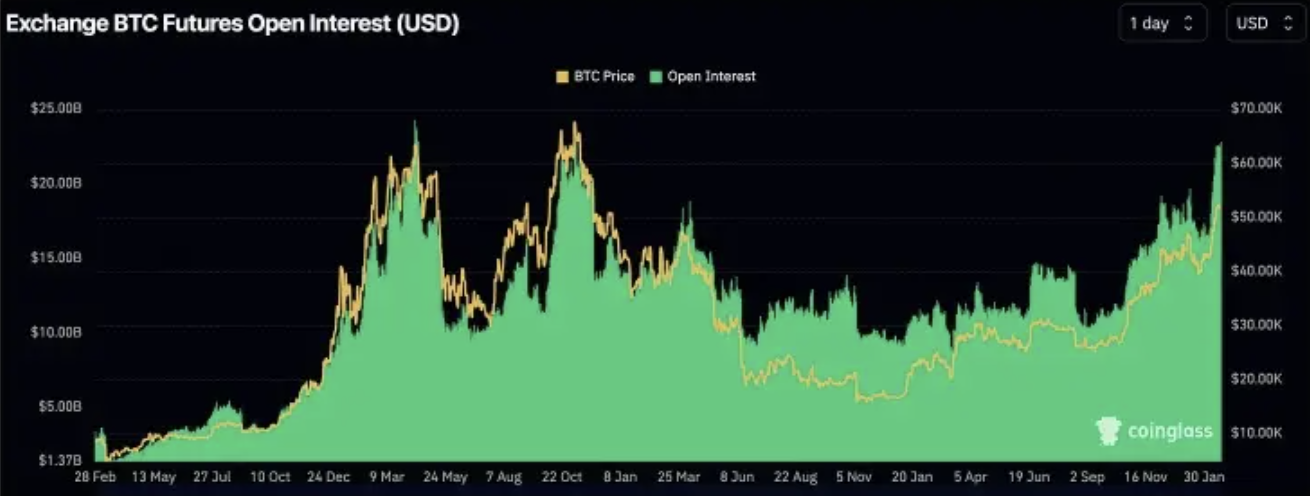

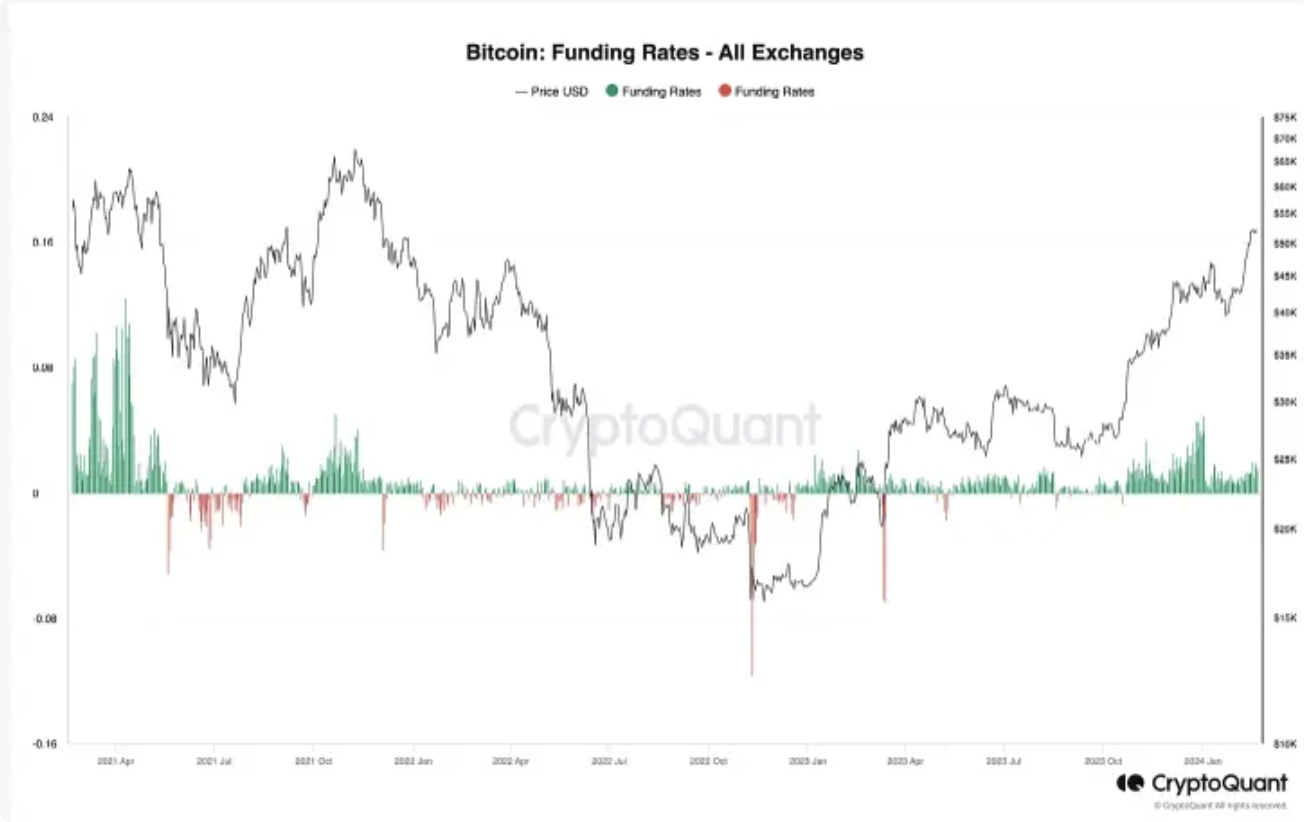

All CEX Bitcoin funding rates have reached historic highs, which is concerning. Positive funding rates signal bullishness—as traders bet prices will rise—but remain risky if the market drops sharply and longs get liquidated.

On-chain DeFi data looks healthier and more bullish, as leverage appears low (though growing).

Aave, the most liquid lending market, is quietly seeing its TVL rise. Typically, borrowers deposit ETH/BTC and other assets to borrow stablecoins, either to buy more ETH/BTC or use them for tax-efficient purposes.

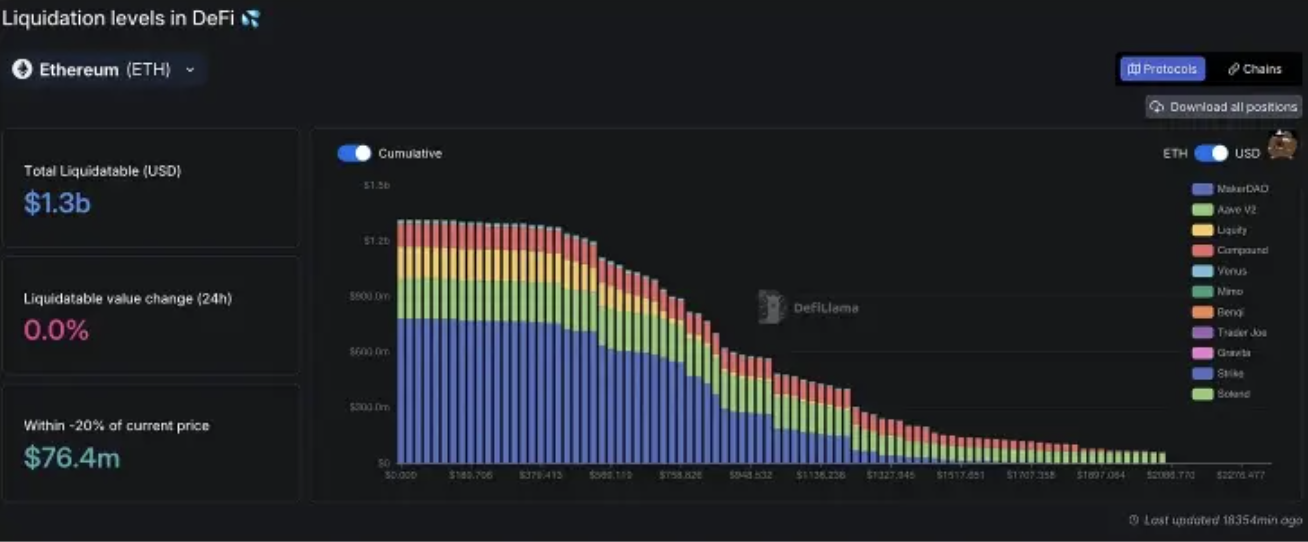

DeFi’s TVL stands at $75 billion—still 270% below the all-time high of $175 billion on November 11, 2022. However, borrowing rates across DeFi are rising. Ipor’s index shows annualized borrowing rates reaching as high as 10%.

Another critical factor to monitor is on-chain liquidations. Defillama has a dashboard, but it hasn’t been updated in weeks.

Where Is Inflation Most Pronounced Now?

There are several areas of concern regarding market inflation and leverage.

The first kind of "inflation" refers to new token issuance. I could create 1 billion IGNAS tokens and sell one to you for $1, giving IGNAS a $1 billion market cap.

For more on this, see the thread below.

The challenge lies in convincing you to buy my token. To do so, I’ll launch a new “Research4YouBaby” protocol, introduce points, and pitch you a compelling story.

You’ll deposit ETH/SOL/stablecoins into my protocol to earn points, hoping for a free airdrop. Other speculators follow suit. The higher the TVL, the stronger the market’s belief that my protocol represents the future of finance.

That’s great for me—I’ve built a loyal community and collect fees from all TVL. Research4YouBaby achieves product-market fit (PMF).

But I’m not the only clever protocol builder—everyone is handing out points. It’s a full-blown feast.

Points are inflating at a crazy pace, but points aren’t tokens. My plan is to wait for peak hype before launching my token. Jito timed its JTO release well; Jupiter did even better.

Yet both tokens are now dumping.

Initial hype drove extremely high fully diluted valuations (with low circulation), as those missing the airdrop bought from secondary markets. Ongoing unlocks will significantly impact prices.

You may have bought JTO or JUP simply because they were hot tokens. But in 2021–22, all tokens were boring—nobody wanted to buy them.

But for every hot airdrop, someone must buy into the narrative that “this protocol is the future of finance.” If you bought JTO or JUP and are now at a loss, you might hesitate before buying the next hot token.

Fortunately, rising BTC and ETH prices fuel the market, allowing speculators to sell BTC/ETH to buy memecoins. But just imagine what happens when BTC and ETH start falling.

Slight tangent, but issuing protocols are becoming complacent.

They assume that the longer they distribute points, the more users and TVL they’ll accumulate. But the more tokens issued, the less capital people have to buy these new tokens. Timing the market is crucial.

So yes, we’re issuing tokens.

Track price movements of new tokens to gauge market demand. Currently, signals are mixed: JUP and JTO are down, but DYM, TIA, and PYTH are performing well.

TIA, PYTH, and DYM have stronger narratives than JTO and JUP—people believe holding them leads to more memecoin airdrops. This may work temporarily, but eventually, airdrops will dwindle. When nobody cares about earning a few dollars from airdrops without additional value propositions, people will dump TIA, PYTH, and DYM.

In short, with each new hot token, capital and user attention become diluted. Eventually, we’ll reach a point where incoming capital can’t sustain the volume of tokens being issued—leading to a severe collapse.

We’re not there yet, but we’re rapidly issuing new tokens. Two main categories are driving this:

· RaaS (Rollup as a Service): Enables quick chain or protocol launches within minutes. Dymension, AltLayer, Caldera, and even Arbitrum L3 chains fall into this category. Dymension alone could host hundreds of RollApps. Just think—who will actually buy these tokens?

· Restaking: A multi-layered token issuance machine:

AVS: dApps using restaked ETH to enhance utility are called AVSs. For example, AltLayer is also an AVS. Multiple AVSs are expected soon, with many more launching after Eigenlayer’s mainnet goes live.

LRT Protocols: Every liquidity restaking protocol will have its own token.

Then comes a second type of inflation and leverage—through token derivatives.

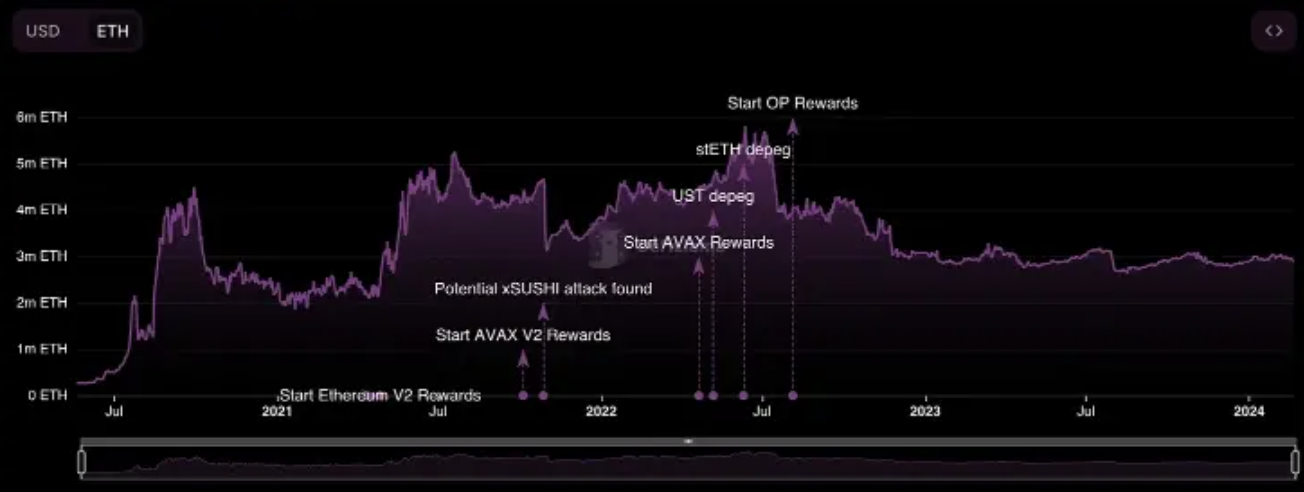

LRT (Liquidity Restaking Tokens)

LRTs are the most obvious and potentially systemic risk.

If you're unfamiliar with LRTs, check my previous post.

LRT ETH, such as KelpDAO’s rsETH, is a complex derivative asset influenced by:

· Multiple ETH LSTs (like ETHx, stETH, etc.). If any LST gets compromised, rsETH is affected.

· Multiple AVS protocols. The ETH backing rsETH will ultimately secure AVS protocols. You could lose your ETH during slashing events.

· Eigenlayer itself. Let’s hope Eigenlayer doesn’t get hacked.

Now, we’re seeing LRT ETH integrated into the DeFi 1.0 ecosystem. I expect Aave and multiple stablecoin protocols to soon accept LRTs due to their higher yields.

Restaking + liquidity restaking has already entered the top 10 by TVL—even though Eigenlayer isn’t fully launched. God help us all.

However, I don’t believe it poses systemic risk yet. Read this research for deeper risk analysis.

Ethena—The New Hot Stablecoin

Next, a new non-Ponzi protocol has emerged—the old classic: a stablecoin.

Ethena enjoys backing from half the crypto industry insiders—you’ll likely see many posts about it.

It’s built on a simple yet powerful concept: deposit stETH to mint USDe 1:1. Price stability is maintained by shorting ETH across various DEXs and CEXs, creating a hedged position.

USDe earns stETH yield (~4%) plus variable yield based on positive funding rates on exchanges. Since long positions dominate, funding rates stay positive—longs pay shorts. If you’re unsure how funding rates work, see the post below for a simple explanation.

The short side is tricky—some funds must be held on CEXs, though many decentralized perpetual exchanges exist.

What if an exchange goes bankrupt? What if withdrawals freeze? What if funding rates turn negative? These are key concerns raised on X.

Currently small-scale, Ethena has issued $250 million in USDe. Yet with its cleverly designed points system ("fragments"), referral program offering 10% rewards, and support from prominent investors like Binance, it’s poised to grow.

It may even become “too big to fail.”

Currently, Ethena holds a 3.57% dominance in open interest on select exchanges. But what happens as its dominance grows? The impact will be significant, though market effects will take time to unfold.

Either way, it directly increases market leverage via open interest and deepens reliance on stETH.

What could go wrong? I don’t know, but my principle is to start farming early. Also, if you’re sitting on stablecoins and sidelined, this is a new hot opportunity. They’re running a three-month campaign—or until USDe supply hits $1 billion.

Note: You cannot mint USDe directly with stETH (KYC required), so you’ll need to buy USDe and deposit it into one of the Curve pools to earn 20x points.

Rising Risk, Circular Farming?

Finally, there may be excessive leverage risks as airdrop farmers loop positions on lending protocols to maximize points. For example, deposit SOL on MarginFi to borrow USDT, swap USDT for more SOL on Jupiter, then deposit SOL on Kamino to borrow more USDT.

So what’s next? At least a few key catalysts lie ahead for the three major blockchains.

Ethereum

Ethereum has at least four bullish catalysts.

First, market attention is shifting from Bitcoin ETFs toward expectations of an Ethereum ETF.

Second, Ethereum’s major Dencun upgrade is scheduled for March or April, featuring nine EIPs—with EIP-4844 (proto-danksharding) being the most significant.

Proto-danksharding aims to reduce L2 transaction fees and lower data availability costs by introducing a new segmented space called “blobs.” It could cut L2 transaction costs by 10x, boosting network activity on L2s and potentially lifting L2 token prices.

Moreover, shortly after the upgrade (perhaps not immediately), Uniswap v4 is set to launch. V4 relies on EIP-1153 (“transient storage”), essential for reducing network costs.

Uniswap v4 introduces “hooks”—programmable contracts that operate at different stages of a liquidity pool’s lifecycle. This transforms Uniswap from a single protocol into a platform developers can build upon.

For more on Uniswap v4 and other exciting releases, refer to my previous blog post.

The v4 launch could boost UNI’s price (short-term, as the token is hard to hold long-term).

Third, Eigenlayer is expected to launch on mainnet in the first half of 2024.

ETH APY will rise, drawing more attention. As riskier assets fall out of favor and speculative energy shifts back to ETH, I believe further token issuance will amplify bullish sentiment toward ETH, as profits from these tokens eventually flow into ETH and BTC.

Thanks to LRTs, we can now earn ~5% staking yield + ~10% from Eigenlayer restaking rewards + ~10% or more from LRT protocol token emissions. Once Eigenlayer fully launches, we could see ~25% APY on ETH. On Pendle, you can already get 40% APY—see “Restaking Heats Up: Full Picture of LRT War and Participation Guide.”

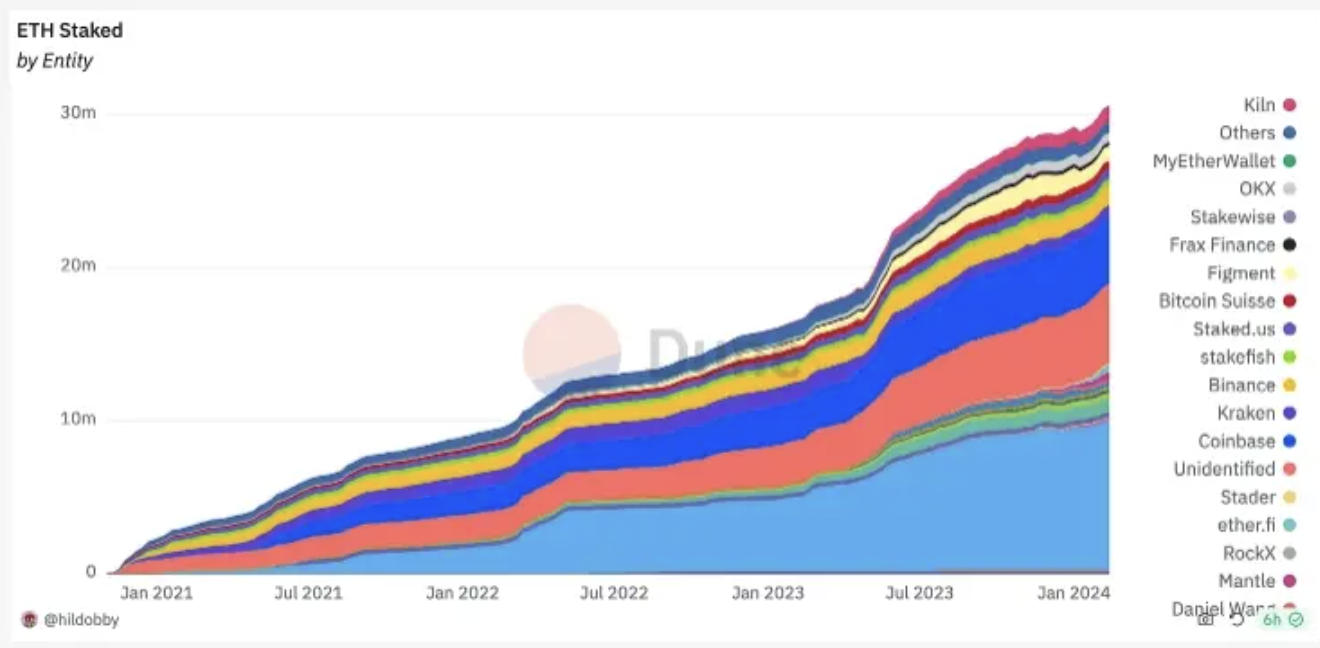

Finally, the amount of staked ETH is increasing—a key indicator, as ETH stakers demonstrate confidence in long-term price appreciation.

I believe tracking withdrawal vs. deposit dynamics is a useful metric for timing market tops.

Bitcoin Halving

The “halving” is both a fun meme and a serious event.

The meme aspect is clear—Bitcoin tends to appreciate around halving events. But there’s a serious side too, involving multiple dimensions.

First, block rewards will drop from 6.25 BTC to 3.125 BTC, reducing monthly selling pressure by ~$225 million. Second, the halving will strengthen Bitcoin’s ecosystem narrative—effects are already visible.

Stacks’ STX rose 75% in a week as the team prepares for the Nakamoto upgrade, which will reduce block time from unusable 10 minutes to just 5 seconds. This is a major upgrade making Stacks finally fun to use. I expect more dApps and airdrops in the Stacks ecosystem.

Stacks isn’t the only (but possibly the main) Bitcoin L2 solution. The Bitcoin L2 narrative is gaining traction, especially with multiple L2s—including Merlin—planning launches around the halving.

But these L2s are complex—do your own research.

Ultimately, at block 840,000, the founder of Ordinals Theory will launch the Runes protocol. It will usher in a new era of coin trading—one even Solana users will envy.

Overall, with institutional inflows into Bitcoin ETFs and heightened excitement around BTCFi, Bitcoin’s outlook remains strong.

Solana

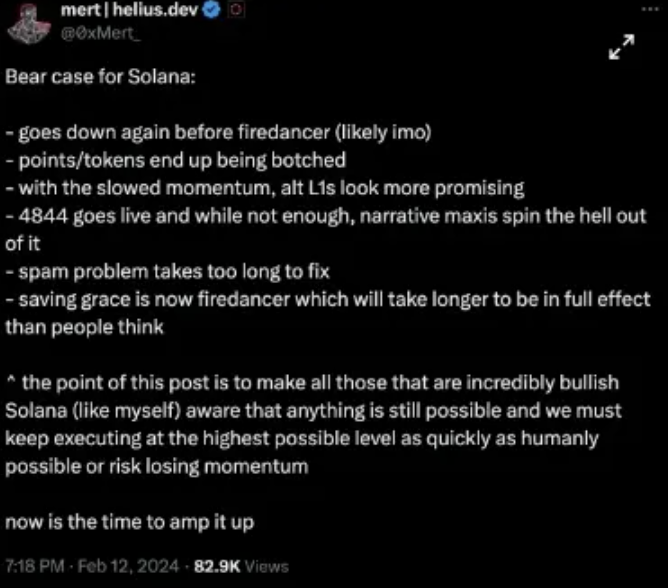

I must admit, Solana has disappointed me—actually, it’s made me quite sad.

It produced blocks almost uninterrupted for nearly a year. Yet bullish sentiment around Solana has cooled. However, Solana Firedancer presents a key catalyst to restore confidence. Firedancer aims to make Solana faster, more secure, and more decentralized. It’s a new software version used by validators (nodes processing transactions) on the Solana network.

This matters because it helps Solana process far more transactions—targeting 1 million per second. That could make Solana faster than many traditional payment systems like Visa.

Firedancer also focuses on improving security by changing how parts of the network interact, helping prevent hacks and enhancing stability. Developed by Jump Crypto, Firedancer is slated for full rollout in summer 2024.

Overall, Mert’s strategy seems applicable here: before Firedancer launches, Ethereum may steal Solana’s spotlight.

But it’s not guaranteed. It’s possible Solana continues to face issues even after the Firedancer upgrade.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News