Stablecoins: The Foundation of Trust in the Digital Financial Era

TechFlow Selected TechFlow Selected

Stablecoins: The Foundation of Trust in the Digital Financial Era

This article will take you deep into the mysteries of stablecoins, covering their functions, classifications, and future development, giving you a comprehensive understanding of stablecoins.

Author: shanni

1. What is a Stablecoin?

Stablecoin is a type of cryptocurrency. Since virtual currencies generated through algorithms or proof-of-stake mechanisms are prone to volatility and lack the function of value storage, they cannot replace centralized currencies. As a result, cryptocurrencies are generally seen only as speculative assets. The core idea behind stablecoins is to build a decentralized underlying ledger while maintaining a mechanism that ensures monetary value stability.

Wikipedia. Stablecoin [EB/OL]. [2024.2.28]

The volatility of cryptocurrencies, both in the short and long term, makes them largely perceived as speculative investments. Stablecoins backed by more traditional investments provide greater market confidence in their pricing. Therefore, stablecoins are often the preferred choice for institutional and retail users when making financial decisions within the cryptocurrency ecosystem.

2. Functions of Stablecoins

Price volatility makes Bitcoin too unstable for everyday use. We need a decentralized digital asset with stable value. The market requires an asset that can serve as a store of monetary value, enabling entry into and exit from (on-ramps and off-ramps) decentralized financial ecosystems. This asset must also act as a medium of exchange—its value should remain stable over time. Ideally, a digital asset should have low inflation to preserve its purchasing power.

As a value-stable digital currency, stablecoins provide a unit of account and a hedging tool for the cryptocurrency market. In highly volatile markets, stablecoins can act as a value anchor, helping investors mitigate risk. With relatively stable-value stablecoins, volatile cryptocurrencies gain a pivot point for mutual exchange, making asset conversions within DeFi much more convenient. Thus, stablecoins possess certain functions as a unit of account.

For traders, during market downturns, risky digital assets can be converted into stablecoins to achieve risk hedging, all without leaving the broader cryptocurrency ecosystem.

3. Types of Stablecoins

Based on different stabilization mechanisms, commonly seen stablecoins in today’s market can be broadly categorized into four types:

-

Fiat-collateralized stablecoins. Examples include USDC and USDT, as well as exchange-issued stablecoins such as BUSD.

-

Crypto-collateralized stablecoins. For example, MakerDAO's DAI and Synthetix's sUSD.

-

Algorithmic stablecoins. Such as LUNA, AMPL, and Frax.

-

Commodity-backed stablecoins. (Due to limited current implementations, this category will not be discussed in depth.)

3.1 Fiat-Collateralized Stablecoins

Among these, fiat-collateralized stablecoins are the most popular. These stablecoins are typically issued and managed by centralized organizations and are backed by real-world financial assets such as cash in U.S. dollars. These centralized stablecoins are crypto tokens with a "pegged" attribute, aiming to track the value of an off-chain asset and maintain parity with it. To ensure price stability, centralized stablecoins are backed by off-chain assets—for example, Tether holds one dollar in reserves for every USDT issued. To link the stablecoin's value directly to the quantity of supporting assets, issuers typically hire independent accounting firms or auditing institutions to regularly verify the custodial accounts holding these assets. Because they are supported by tangible assets, the price fluctuations of such stablecoins are usually influenced only by short-term supply and demand, and tend to be minimal.

However, due to their high degree of centralization, these stablecoins face issues regarding transparency of asset disclosures. For instance, although Tether, the issuer of USDT, claims to hold 100% USD reserves backing each USDT, it has long been criticized as an opaque "printing press without collateral."

3.2 Crypto-Collateralized Stablecoins

Crypto-collateralized stablecoins are digital currencies pegged to fiat values, created by locking up digital assets like BTC or ETH in smart contracts—typically through over-collateralization. A representative example of this model is DAI, issued by Maker on Ethereum.

These over-collateralized stablecoins are generated via smart contracts designed with specific algorithms and code. They do not create value out of thin air, as they are minted by locking up certain assets. To retrieve the locked assets, the corresponding amount of over-collateralized stablecoins must be burned.

3.3 Algorithmic Stablecoins

Algorithmic stablecoins have a unique mechanism. These stablecoins lack any intrinsic value backing and instead rely on algorithms to regulate supply and demand to maintain price stability—a process somewhat analogous to central banking in the real world.

A typical example is AMPL, launched in 2018 and considered the pioneer of algorithmic stablecoins. Algorithmic stablecoins generally control supply through open market operations, rebasing, or issuing secondary tokens. Without any fundamental value base and relying solely on market consensus, algorithmic stablecoins are highly vulnerable to price volatility caused by speculation.

Below is part of DAI's implementation, essentially an ERC-20 token.

// --- ERC20 Data ---

string public constant name = "Dai Stablecoin";

string public constant symbol = "DAI";

string public constant version = "1";

uint8 public constant decimals = 18;

uint256 public totalSupply;

mapping (address => uint) public balanceOf;

mapping (address => mapping (address => uint)) public allowance;

mapping (address => uint) public nonces;

event Approval(address indexed src, address indexed guy, uint wad);

event Transfer(address indexed src, address indexed dst, uint wad);

Creating a new stablecoin

function mint(address usr, uint wad) external auth {

balanceOf[usr] = add(balanceOf[usr], wad);

totalSupply = add(totalSupply, wad);

emit Transfer(address(0), usr, wad);

}

Implementation of stablecoin burning functionality

function burn(address usr, uint wad) external {

require(balanceOf[usr] >= wad, "Dai/insufficient-balance");

if (usr != msg.sender && allowance[usr][msg.sender] != uint(-1)) {

require(allowance[usr][msg.sender] >= wad, "Dai/insufficient-allowance");

allowance[usr][msg.sender] = sub(allowance[usr][msg.sender], wad);

}

balanceOf[usr] = sub(balanceOf[usr], wad);

totalSupply = sub(totalSupply, wad);

emit Transfer(usr, address(0), wad);

}

4. Mechanisms of Stablecoins

4.1 Centralized Stablecoin Mechanism

Asset Backing: The value of centralized stablecoins such as USDC and USDT is primarily maintained by being pegged 1:1 to fiat currencies like the U.S. dollar. This means that for every stablecoin issued, one dollar (or equivalent asset) is held in reserve. These reserve assets are typically held by third-party custodians.

Issuance and Redemption: Users can obtain an equivalent amount of USDC or USDT by depositing U.S. dollars into the stablecoin issuer’s account. Similarly, users can redeem these stablecoins for an equal value in U.S. dollars. This process ensures that the supply of stablecoins matches the amount of fiat currency backing them.

Compliance and Regulation: As centralized financial products, the issuers of USDC and USDT must comply with relevant financial regulations, including anti-money laundering (AML) and know-your-customer (KYC) policies.

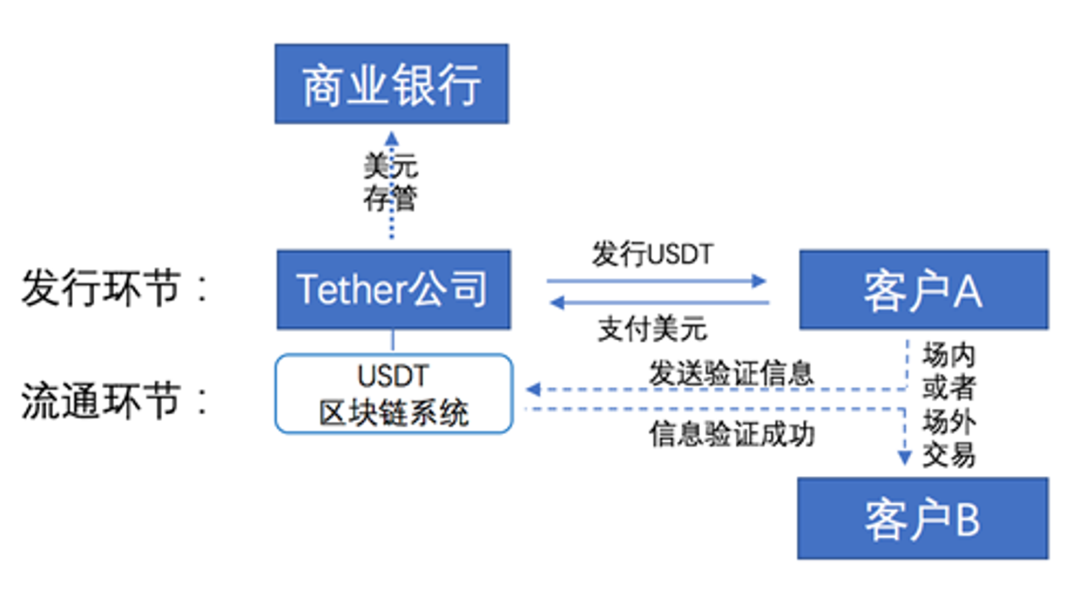

Figure 1: USDT Issuance and Circulation Diagram

Source: “The ‘Stability’ and ‘Instability’ of Stablecoins,” Author: Kodak

In the issuance and circulation mechanism of off-chain stablecoins, three parties are involved: the issuing company, customers, and the custodian bank. Taking USDT as an example, as shown in the figure, when a customer transfers a certain amount of U.S. dollars to Tether’s bank account, Tether confirms receipt of the funds and then transfers an equivalent amount of USDT from Tether’s core wallet to the customer’s Tether wallet—this step constitutes the issuance of USDT. At the monetary policy level, Tether cannot intervene in the price of USDT through regular issuance and redemption activities, nor is there any external affiliated institution manipulating the price of USDT. Kodak. “The ‘Stability’ and ‘Instability’ of Stablecoins” [J]. Law and New Finance, 2018, (35).

Currently, in various countries, stablecoins pegged to local fiat currencies have been introduced. For example, XSGD, jointly launched by Zilliqa and Xfers, is pegged to the Singapore Dollar (SGD). e-CNY, issued by the People’s Bank of China, is a digital version of the Chinese yuan and can be viewed as a state-supported stablecoin, falling under central bank digital currency (CBDC). EURS, issued by STASIS, is a euro-pegged stablecoin. While there is no mainstream British pound stablecoin yet, projects like GBPT are exploring this space. CADT is a stablecoin pegged to the Canadian dollar.

4.2 Overcollateralized Stablecoin Mechanism

For overcollateralized stablecoins such as those issued by Maker Protocol, the mechanism generally includes the following components:

Minting and Burning Mechanism: Dai is created and destroyed through overcollateralized loans and repayments within MakerDAO’s smart contracts. Users deposit accepted collateral types (such as Ether) into the contract and can mint new Dai based on the value of their collateral.

To measure the relationship between collateral and borrowed stablecoins, we introduce the concept of the collateralization ratio.

Collateralization Ratio: At any time, the dollar value of the collateral divided by the number of Dai borrowed is the loan’s “collateralization ratio.” This is calculated using dollar prices of the collateral units periodically reported to the contract by a set of decentralized oracles. Each loan type has a fixed minimum collateralization ratio, typically ranging from 110% to 200%.

Regarding fluctuations in the value of pledged assets causing changes in the collateralization ratio, if the ratio falls below the required minimum, the position typically enters liquidation.

Liquidation Mechanism: If a loan’s collateralization ratio drops below the minimum threshold, anyone can trigger a function in the contract, causing part of the collateral to be sold on a decentralized exchange for Dai, which is then used to repay the debt, with a reward paid to the account that initiated the call.

Interest and Repayment: Once a loan and its accrued interest are repaid, the returned Dai is automatically burned, and the collateral becomes available for withdrawal. Thus, the dollar value of Dai is effectively backed by the dollar value of the underlying collateral held in MakerDAO smart contracts.

Controlling Dai’s Value: By adjusting the types of accepted collateral, minimum collateral ratios, and interest rates for borrowing or saving Dai, MakerDAO can control the circulating supply of Dai, thereby influencing its value.

Governance and MKR Token (MKR as a Recapitalization Resource): The power to propose and implement changes to these variables is granted via code to holders of the MKR token. Governance token holders can vote proportionally based on the number of tokens they hold. MKR tokens also represent an investment in the MakerDAO system. Additional interest paid by borrowers is used to buy MKR tokens from the market and burn them, permanently removing them from circulation. This mechanism aims to make MKR deflationary and tied to DAI borrowing revenue.

This mechanism ensures DAI’s stability as a stablecoin while preserving its value through decentralized governance.

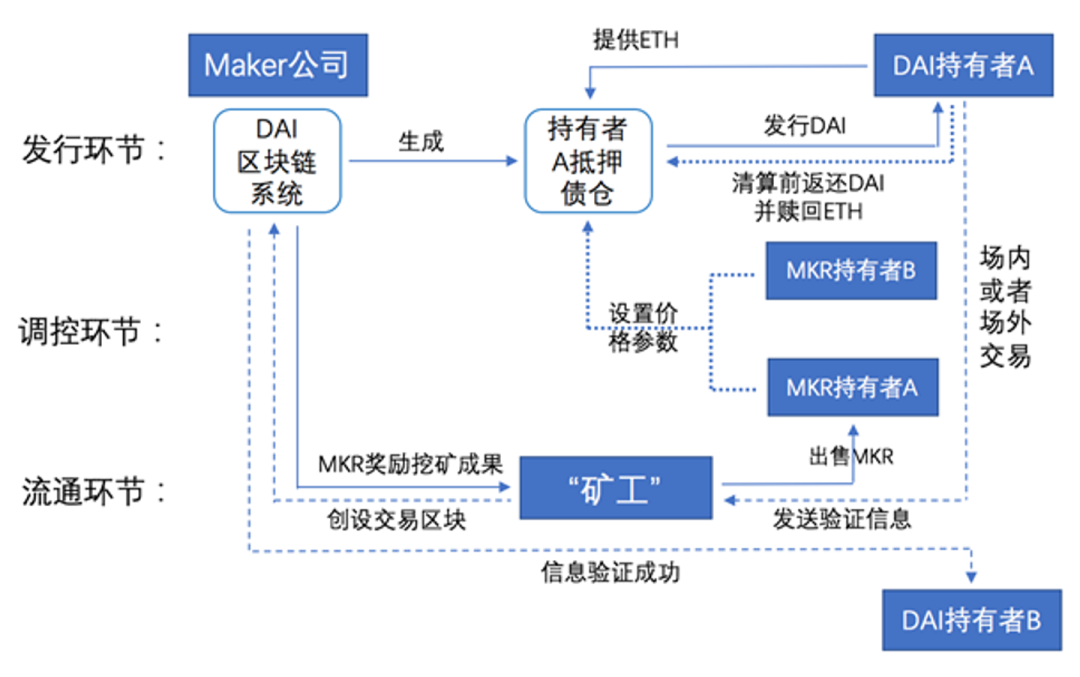

Figure 2: DAI Issuance, Circulation, and Control Mechanism

Source: “The ‘Stability’ and ‘Instability’ of Stablecoins,” Author: Kodak

As shown in the figure above, in the issuance, circulation, and control mechanism of on-chain stablecoins like DAI, two main participants are involved: users and holders of the “governance token” (e.g., MKR). Specifically, users first deposit Ether (ETH) into a “Collateralized Debt Position” (CDP) created by MakerDAO. After confirming the ETH amount, the CDP locks it and issues a corresponding amount of DAI to the user’s digital wallet, based on a ratio below the ETH market value. If users wish to reclaim their collateralized ETH, they must return the equivalent amount of DAI to the CDP and pay a “stability fee.” The CDP then burns the returned DAI and releases the ETH. Within this system, MKR token holders vote on key economic parameters such as collateral ratios, liquidation ratios, and stability fees. These decisions affect the cost and incentives for users to issue or redeem DAI, thereby influencing DAI’s market value. When ETH’s market price drops to the preset liquidation threshold and the associated DAI debt is not promptly settled, the system automatically initiates a forced auction process, selling the ETH collateralized in the CDP through internal auctions.

Summary

Early cryptocurrencies like Bitcoin emerged from skepticism toward national fiat currencies, aiming to achieve transparent, democratic, and stable monetary issuance. However, due to the lack of intrinsic value and other factors, most early cryptocurrencies experienced severe price volatility. Against this backdrop, stablecoins targeting price stability began to appear.

Compared to early cryptocurrencies like Bitcoin, off-chain stablecoins pegged to fiat currencies exhibit the highest price stability, followed by on-chain stablecoins pegged to other cryptocurrencies, while algorithmic stablecoins—lacking intrinsic value and relying solely on private monetary control—show the greatest price volatility. In achieving price stability, stablecoins generate credit and “trust” risks,陷入 a logical dilemma where they cannot simultaneously achieve independence from fiat currencies and price stability. The multi-centralized or fully centralized operational mechanisms of stablecoins fundamentally contradict the original intent behind private cryptocurrency issuance.

Many blockchain optimists believe that in the future, most physical offline assets will be tokenized into blockchain-based digital assets, each divisible into a certain number of tokens for global circulation, greatly enhancing resource allocation efficiency. Concurrently, as offline assets become tokenized, a stable-value digital currency will be needed to enable “delivery versus payment” between digital currencies and tokens via smart contracts, effectively fulfilling the monetary functions of medium of exchange, unit of account, and store of value.

In the author’s view, as a financial infrastructure, ordinary individuals should pay attention to opportunities in decentralized stablecoins. Currently, several over-collateralized stablecoin systems—such as MakerDAO, DAI, sDAI, Aave, GHO, and PRISMA—have operated successfully for years. In the future, we may discover even better stablecoin solutions.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News