Deep Dive into Ethena Labs: Can 27% Stablecoin APY Be Sustained?

TechFlow Selected TechFlow Selected

Deep Dive into Ethena Labs: Can 27% Stablecoin APY Be Sustained?

Ethena was built to address the largest and most obvious immediate need in the crypto space.

Author: ROUTE 2 FI

Translated by: TechFlow

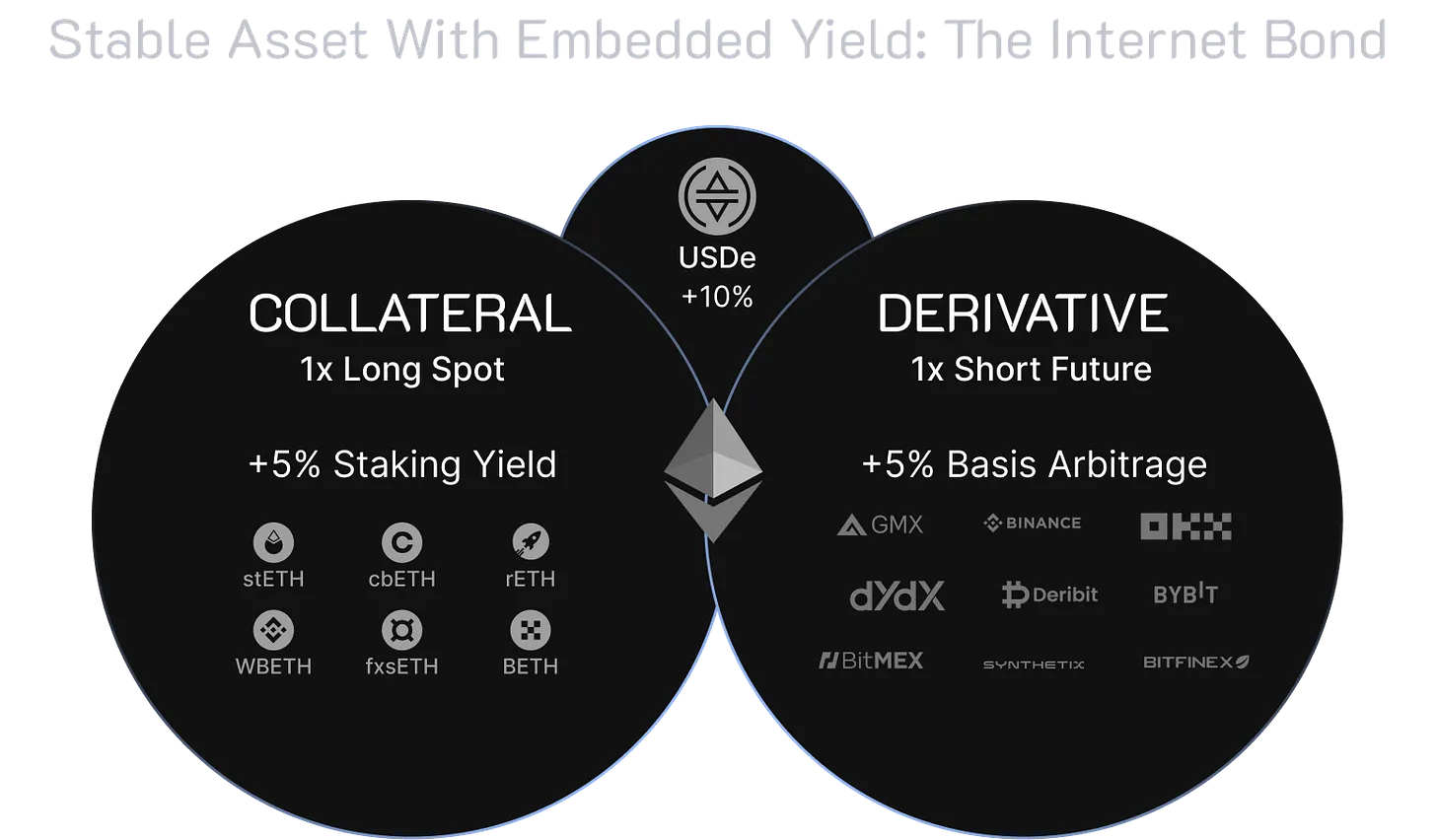

Ethena is a synthetic dollar protocol built on Ethereum, offering a crypto-native solution for money independent of traditional banking infrastructure, while providing a globally accessible, USD-denominated savings tool—the “Internet Bond.”

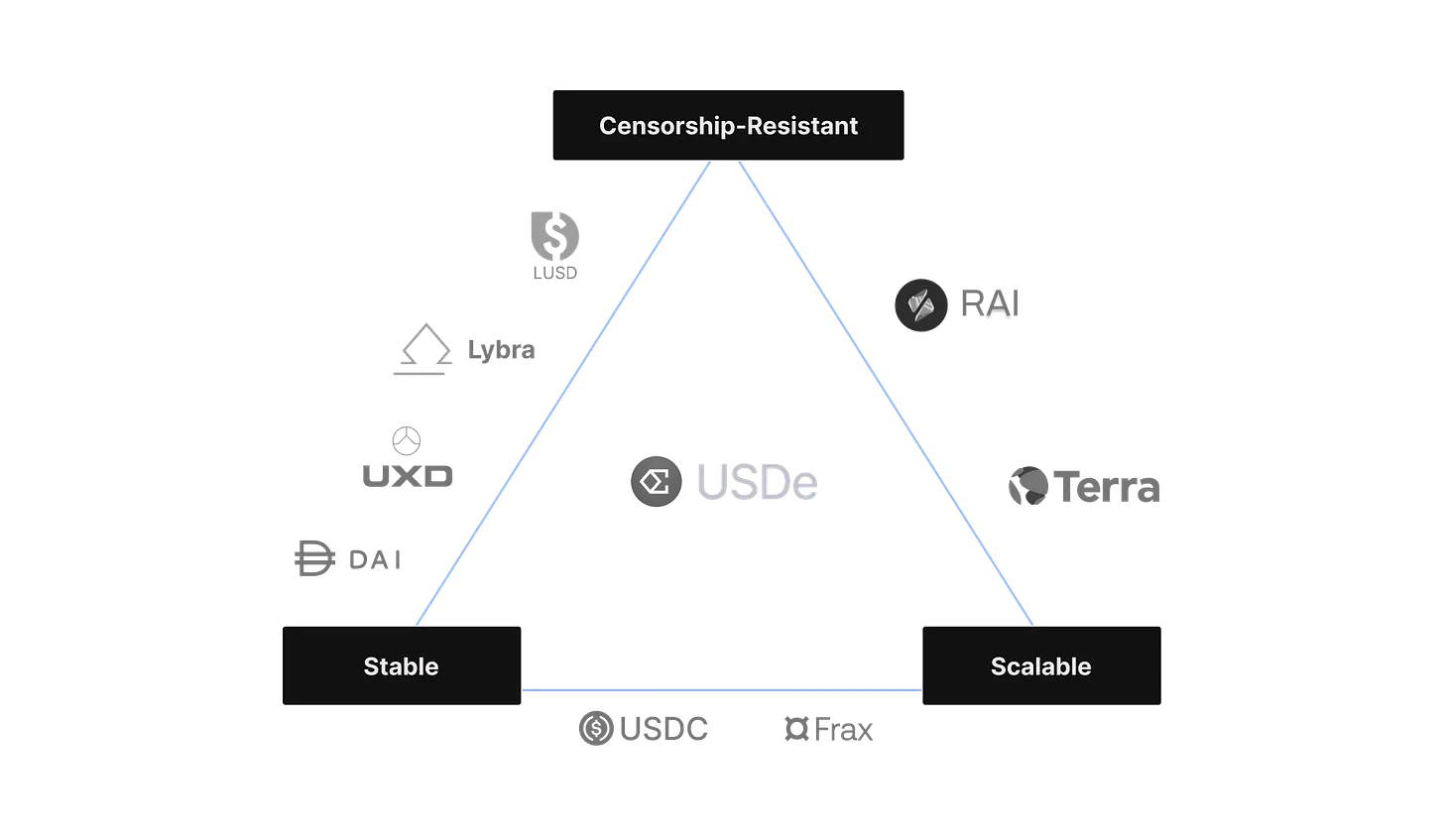

USDe, Ethena’s synthetic dollar, will deliver the first censorship-resistant, scalable, and stable crypto-native monetary solution by delta-hedging staked Ethereum collateral.

USDe will be fully transparently backed on-chain and freely composable within DeFi.

The stability of USDe’s peg is ensured through delta-hedging derivative positions on the protocol’s collateral, combined with minting and redemption arbitrage mechanisms.

The “Internet Bond” combines yield from staking Ethereum with funding rate and basis spread returns from perpetual and futures markets.

Ethena was created to address the largest and most immediate need in crypto. DeFi aims to build a parallel financial system, yet stablecoins—the most critical financial tools—remain entirely dependent on and subject to traditional banking infrastructure.

Why Are Stablecoins So Important?

Stablecoins are the single most important tool in crypto.

All major spot and futures market pairs are quoted in stablecoin terms, over 90% of order book trading and more than 70% of on-chain settlements occur in stablecoins. This year alone, stablecoins settled over $12 trillion on-chain, constitute two of the five largest assets in the space, account for over 40% of TVL in DeFi, and are by far the most widely used asset in decentralized money markets.

Centralized stablecoins like USDC or USDT offer stability and capital efficiency but introduce:

-

Unhedgeable custody risk via bond collateral held in regulated bank accounts vulnerable to censorship

-

Dependency on existing banking infrastructure and shifting regulations in specific jurisdictions

-

A “no-reward risk” for users, as issuers internalize yields while passing depeg risks onto users

Historically, decentralized stablecoins have faced challenges around scalability, mechanism design, and lack of embedded yield.

-

“Overcollateralized stablecoins” historically struggled with scalability because their growth inevitably ties to leverage demand on Ethereum. Recently, some stablecoins improved scalability by introducing treasuries, but at the cost of censorship resistance

-

“Algorithmic stablecoins” face inherent fragility and instability due to their mechanism designs. We do not believe these designs are sustainably scalable

-

“Delta-neutral synthetic dollars” have struggled to scale due to heavy reliance on decentralized venues lacking sufficient liquidity

Therefore, USDe offers the following advantages:

-

Scalability via derivatives, allowing USDe to expand efficiently. Since staked ETH can be perfectly offset by equivalent short positions, synthetic dollars require only 1:1 collateralization

-

Stability provided by immediately hedging transferred assets upon issuance, ensuring the synthetic dollar value backing USDe under all market conditions

-

Censorship resistance achieved by separating supporting assets from the banking system and storing trustless collateral in decentralized liquidity pools—on-chain, transparent, continuously auditable, and outside programmatic custody solutions

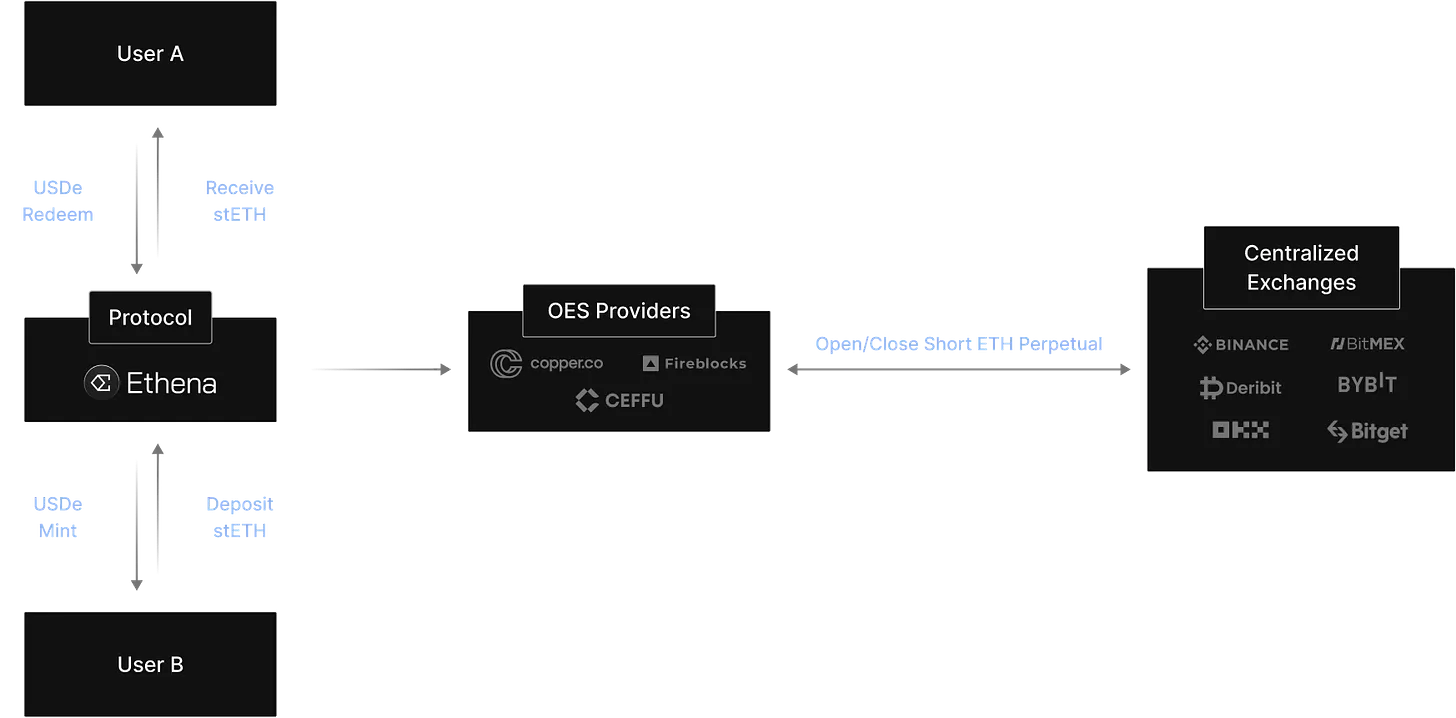

How Does Ethena Labs Work?

-

Users deposit approximately $100 worth of stETH and automatically receive about $100 of USDe after deducting execution costs for hedging

-

Ethena Labs opens a roughly equivalent short perpetual position on derivative exchanges

-

Received assets are moved to an “off-exchange settlement” provider. Collateral remains both on-chain and on off-exchange servers to minimize counterparty risk

-

Ethena Labs delegates collateral to derivative exchanges but never transfers custody, holding perpetual short hedges in margin form

Ethena Labs generates two sustainable yield streams from deposited assets.

Yields returned to eligible users come from:

-

Staking Ethereum for consensus and execution layer rewards (3.5% APR)

-

Funding rates and basis spreads from delta-hedged derivative positions (5–20% APR)

Yield from staked Ethereum is inherently floating when denominated in ETH. Funding and basis spread yields may be either floating or fixed.

Historically, positive funding and basis spread returns have emerged due to imbalances in supply and demand for leveraged crypto positions, along with consistently positive baseline funding rates.

If funding rates remain negative long enough that staking rewards cannot cover funding and basis spread costs, Ethena’s insurance fund will absorb the shortfall.

Click here to view historical yield data.

Once users exchange USDe for sUSDe, they begin accruing protocol yield without any further action or fees.

The amount of sUSDe users receive depends on how much USDe they deposited and when. Ethena’s sUSDe uses the same “Token Vault” mechanism seen in Rocketpool’s rETH or Binance’s WBETH.

The protocol does not re-stake, lend, or otherwise use deposited USDe for any purpose. There is no need, as the mechanism behind USDe itself generates protocol yield.

If the protocol incurs losses due to funding or other factors, Ethena’s insurance fund—not the staking contract—will bear the cost.

-

When users mint USDe, Ethena Labs opens a short position

-

When users redeem USDe, Ethena Labs closes the position

-

Ethena Labs realizes unrealized PnL by closing/opening positions on exchanges

If USDe trades below Ethena Labs’ intrinsic value on external markets, users can:

-

Buy 1 USDe at a 0.95 discount using USDC on Curve

-

Swap USDe for USDC on Curve at a price greater than 1.00

-

Use USDC to buy ETH on Curve

-

Thus realize a profit

What Are the Risks?

Funding Risk

“Funding risk” refers to the possibility of persistently negative funding rates. Ethena earns from funding rates but may also need to pay them (resulting in lower protocol yield).

An Ethena insurance fund exists and will intervene when LST assets (e.g., stETH) face negative funding relative to short perpetual positions. This ensures USDe’s collateral remains unaffected. Ethena will not pass any “negative yield” to users who exchange USDe for sUSDe.

Combining annualized stETH yield and funding rate values, only 10.8% of days showed negative net yield. Compared to ~20.5% of days with negative funding rates without stETH yield, this is favorable.

If you recall Anchor Protocol’s yield reserve, Ethena’s insurance fund works similarly, supporting yields during “negative” days.

Liquidation Risk

Ethena uses staked Ethereum spot assets as collateral to hedge derivative positions. Ethena uses staked Ethereum assets such as Lido’s stETH as collateral for short ETHUSD and ETHUSDT perpetuals on CeFi exchanges. Therefore, the asset Ethena uses (stETH) differs from the underlying asset of the derivative position (ETH).

The spread between ETH and stETH would need to widen beyond 65%—something that has never occurred historically (maximum was 8%, pre-Shapella and during Luna’s depeg in May 2022)—before Ethena’s positions begin gradual liquidation and incur realized losses.

Through programmatically delta-neutral hedging against underlying collateral, $USDe’s peg stability is automatically maintained.

To mitigate “liquidation risk” from the above scenarios:

-

In the event of any risk scenario, Ethena will systematically allocate additional collateral to improve margin health of hedging positions

-

Ethena can temporarily cycle collateral across exchanges to support specific situations

-

Ethena can rapidly deploy its insurance fund to support hedging positions on exchanges

-

In extreme cases, such as a critical smart contract vulnerability in staked Ethereum assets, Ethena will act immediately to protect collateral value—this includes closing hedging derivatives to avoid liquidation risk and swapping affected assets for alternatives.

Custody Risk

Since Ethena Labs relies on off-exchange settlement providers to custody protocol-backed assets, there is dependency on their operational capacity. Ethena must be able to deposit, withdraw, and delegate to exchanges. Any unavailability or degradation of these capabilities would hinder trading workflows and the availability of USDe minting/redemption functions.

Exchange Failure Risk

Ethena Labs uses derivative positions to offset delta exposure of digital asset collateral. These derivatives trade on CeFi exchanges such as Binance, Bybit, Bitget, Deribit, and Okx. If an exchange suddenly becomes unavailable—as with FTX—Ethena would face consequences. This is “exchange failure risk.”

Collateral Risk

“Collateral risk” here refers to the mismatch between USDe’s collateral asset (stETH) and the underlying asset of the perpetual futures position (ETH).

Currently, all protocols relying on stETH (and any ETH LST) accept this liquidity risk. This means that if users need immediate access to external markets, the amount of stETH that can be unstaked via Lido may be delayed, or users may have to accept slight slippage.

Approved Ethena users can always redeem USDe for stETH (or any ETH LST) on-demand or request alternative assets, leveraging Ethena’s access to multiple liquidity pools.

A critical smart contract vulnerability in an LST could undermine confidence in its integrity. In such a case, users might rush to unstake or swap LSTs for alternative collateral. This could lead to excessively long validator exit queues on protocols like Lido and liquidity drain across DeFi and CeFi exchanges.

Discussion

This is quite a technical discussion. Now, let’s explore why this product is interesting.

-

27.6% annualized yield on stablecoin

-

Yield comes from using LSD $ETH as collateral for a 1x short ETH position

-

LSD $ETH yield + short $ETH funding rate = $sUSDe yield

-

Upcoming airdrop (“Ethena Shards”), running for 3 months or until $USDe supply hits $1 billion

-

Liquidity Providers (LPs) + locked LP tokens = 20 shards/day

-

Buying and holding $USDe = 5 shards/day

-

Staking and holding $sUSDe = 1 shard/day

-

TVL growing rapidly: already reached $300 million TVL so far

-

All stablecoin pool caps are currently full (expecting increases—just my intuition)

-

Low smart contract risk, but higher centralization risk (funds on exchanges), and performs best in bull markets when leverage demand is high (don’t expect positive funding rates when everyone wants to short ETH)

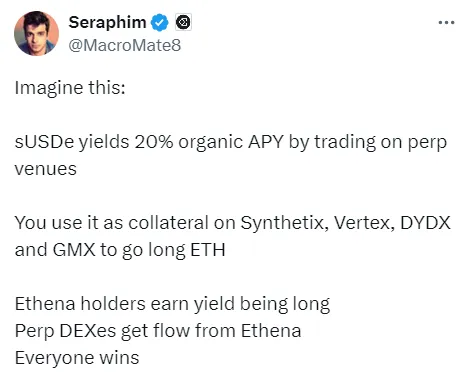

Moreover, you’ll soon be able to use your sUSDe in DeFi—see the example below from Seraphim, Ethena Labs’ Growth Lead:

Still, one point people struggle to understand is why we need funding rates.

Funding rates exist to align perpetual futures prices with index spot prices: whenever long $ETH demand is excessive, $ETH perpetual price exceeds $ETH spot price, so CEXs need a mechanism to discourage further longs.

Thus, funding rates maintain dynamic equilibrium between futures and spot prices. Because the market is generally long-biased (more longs than shorts), if you short $ETH, you earn from longs to counteract excessive demand, pulling $ETH perpetual price back toward $ETH spot price.

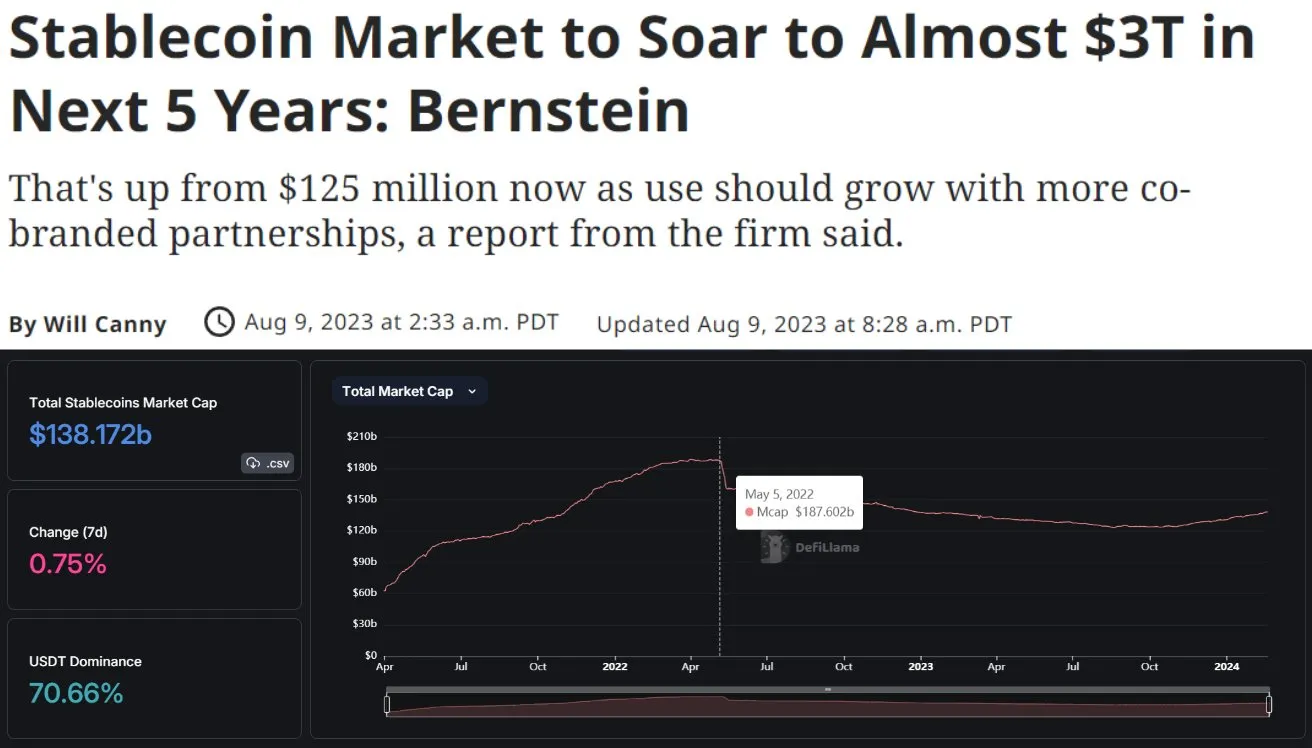

Global asset manager AllianceBernstein forecasts stablecoin market cap reaching $3 trillion by 2028. Considering today’s market—stablecoin market cap currently $138 billion, peak $187 billion—this represents a potential 2000% growth!

Additionally, Ethena has raised $14 million from top global investors including @binance, @CryptoHayes, @Bybit_Official, @mirana, @lightspeedvp, @FTI_US. Notably, angel investors include @dcfgod, @cobie, and @blknoiz06.

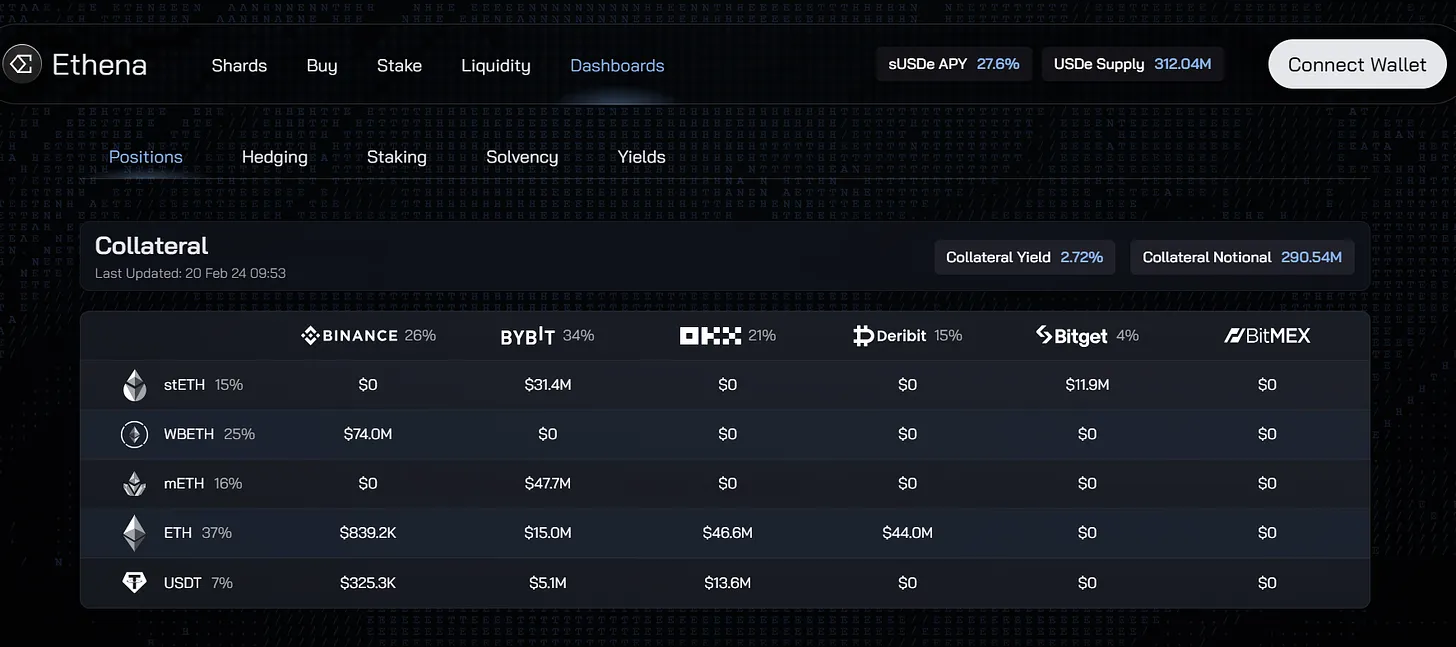

Ethena has a solid dashboard where you can monitor metrics—at least it provides some psychological comfort regarding risk.

Drawbacks of Ethena

Simply put, it's just a basis trade. When yields reverse, you start losing money—and the larger the stablecoin grows, the bigger the losses. Currently, long $ETH traders pay shorts yield. This can last a long time, especially in bull markets. But eventually, yields will reverse—people will short ETH and get paid. Suddenly, Ethena must bear that cost. They have an insurance fund to temporarily cover it. But as sUSDe yield drops, I suspect people may want to withdraw. That said, it’s not a death spiral—just that people might seek yield elsewhere.

Using stETH as collateral provides a higher safety margin than negative rates. This means Ethena only cares about days when ETH funding rates are more negative than stETH yield. However, stETH liquidity is crucial for maintaining the peg. USDe cannot scale to $100 billion without ample stETH liquidity.

Now, in such a scenario:

-

Users redeem

-

Insurance fund can be used to cover. According to Ethena, every $1 billion of USDe can survive with $20 million—enough to withstand nearly all pessimistic funding rate predictions (Chaos Labs estimates $33 million per $1 billion needed).

-

The project’s biggest risk may not be blow-up, but whether people will keep money locked in a zero-yield token when “trusted” alternatives exist (I say “trusted” to highlight legacy stablecoins like USDT or USDC—not claiming they’re better, but since they’ve existed longer, most assume they’re more credible).

-

Counterparty risk from CEXs and smart contracts could be one of the biggest issues. As @tbr90 notes, long-term risk lies in negative rates gradually draining the insurance fund, leading to slow depegging.

As Cobie pointed out, people can execute this trade themselves.

For example, short ETHUSDT and collect funding every 8 hours, go long stETH or mETH (for higher temporary yield). No 7-day staking queue, you choose your own risk. You’ll need to rebalance manually.

@leptokurtic_ (Ethena’s founder) agrees but notes, “Ethena Labs wasn’t created to save you the hassle of executing cash and carry trades. The exciting part is tokenizing this asset, making it highly liquid across DeFi and CeFi, then enabling new, interesting use cases—combining different monetary Legos.”

Regardless, I like this project. Something new is always exciting. I can see perpetual DEXs launching their own stablecoins, DeFi protocols adopting it as monetary Lego—much like what happened with EigenLayer and restaking narratives.

People may recall I was once a big fan of Anchor Protocol—Ethena feels like a healthier way to do it. Personally, I won’t use the protocol much because I think there are bigger opportunities in bull markets than chasing 20% annual yield. Still, we’ll chase the airdrop.

Another thing I don’t like: 7-day unstaking delay from staking, 21-day withdrawal from LPs. If instant unstaking were possible, I’d consider using it during market downtime—but waiting 7 days in crypto feels long.

That said, they may integrate sUSDe into several DeFi protocols, letting you earn yield while trading or liquid staking. Once those solutions launch, I’ll explore further.

Overall, I’m positive about the product—even if this article may seem somewhat negative overall.

Click here to view all FUD against Ethena.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News