BitMEX founder's latest article: After Bitcoin falls below $35,000, getting ready to buy the dip

TechFlow Selected TechFlow Selected

BitMEX founder's latest article: After Bitcoin falls below $35,000, getting ready to buy the dip

Bitcoin and cryptocurrencies overall represent the last truly free global marketplace.

Written by: Arthur Hayes

Translated by: Mary Liu, BitpushNews

U.S. Treasury Secretary Janet Yellen and clueless Federal Reserve Chair Jerome Powell vacillate between decisive action and empty rhetoric. When they act, you should not stand in their way; but when they merely talk, beware—many market signals may mislead you down a path destined for losses.

On November 1, 2023, the U.S. Treasury’s Quarterly Refunding Announcement (QRA) included a statement that Janet Yellen would shift most of its borrowing toward short-term Treasury bills (T-bills) with maturities under one year. This prompted money market funds (MMFs) to withdraw from the Fed's Reverse Repo Program (RRP) and invest in higher-yielding Treasuries. The outcome, detailed in my article "Bad Gurl," has provided liquidity injections—past and present—that will total close to $1 trillion upon completion.

In mid-December 2023, Powell declared during the FOMC press conference that they were discussing rate cuts in 2024—a dramatic reversal from his statements just two weeks earlier, when he assured markets the Fed would remain restrictive to ensure inflation wouldn’t rebound. Markets interpreted this as signaling the first cut of this hiking cycle would occur in March this year. Then earlier this month, Dallas Fed President Logan threw out a smokescreen, suggesting the pace of Quantitative Tightening (QT) would gradually slow once RRP balances neared zero. The rationale: the Fed doesn’t want any dollar liquidity issues to arise when it stops printing money.

Let’s distinguish what was talk versus actual action. Yellen shifted departmental borrowing into T-bills, adding hundreds of billions in liquidity so far—an actual flow of funds into global financial markets. Powell and other Fed governors talked about a grand scenario involving distant future rate cuts and slowing QT. That talk added no monetary stimulus. Yet the market treated both actions and words as equal, rallying after November 1 and continuing upward throughout the month.

The markets I refer to are the S&P 500 and Nasdaq 100 indices, both of which hit new all-time highs. But not everything is smooth sailing.

The real canary in the coal mine for the direction of dollar liquidity—Bitcoin—is flashing warning signs. After the launch of U.S. spot ETFs, Bitcoin has fallen from its high of $48,000 to below $40,000. Coinciding with Bitcoin’s local peak, the 2-year U.S. Treasury yield hit a local low of 4.14% in mid-January and is now rising.

The first argument for Bitcoin’s recent plunge is outflows from the Grayscale Bitcoin Trust (GBTC), but this doesn't hold water—netting GBTC outflows against inflows into newly listed spot Bitcoin ETFs results in a net inflow of $8.2 billion as of January 22.

The second argument—and my stance—is that the Bitcoin market anticipates the Bank Term Funding Program (BTFP) will be paused.

This event won’t have positive implications because the Fed hasn’t yet cut rates to levels that would push 10-year yields into the 2%-3% range. At those levels, non-Too-Big-To-Fail (TBTF) banks’ bond portfolios would return to profitability, whereas currently they sit on massive unrealized losses. Without government support via BTFP until rates fall to such levels, these banks cannot survive. A booming financial market has given Yellen and Powell false confidence that once BTFP ends, markets won’t allow non-TBTF banks to fail. Thus, they believe they can halt the politically toxic BTFP without negative market reactions. However, I believe the opposite: stopping BTFP will trigger a small financial crisis, forcing the Fed to stop talking and compelling Yellen to begin cutting rates, slowing QT, and/or restarting quantitative easing (QE). Bitcoin’s price action tells me I am right, and they are wrong.

The Fed prefers to stimulate markets through speeches and Wall Street Journal op-eds because they are deeply fearful of inflation. The warmongering puppet running America’s Pax Americana foreign policy is now bogged down in another Middle East war, with an endless conflict against Yemen’s Houthi movement. Later in this article, I’ll detail why this war matters and could cause an alarming spike in commodity inflation ahead of the U.S. election in November.

Contrary to what Western mainstream financial media tell you, inflation remains an issue for most bankrupt Americans. Voters decide presidents based on the economy, and right now, President Joe Biden and his Democrats are doomed to lose to redneck representative Trump and the Republicans.

As I wrote in “Signposts,” I believe Bitcoin will decline before the BTFP renewal decision on March 12. I didn’t expect it to happen this quickly, but I think Bitcoin will find a local bottom between $30,000 and $35,000.

As SPX and NDX fall due to a mini-crisis in March, Bitcoin will rise, reflecting the Fed finally turning its talk of rate cuts and money printing into action—pressing the “Brrrr” button.

Now, I’ll quickly walk readers through some charts explaining why I believe the Fed needs a small financial crisis to end the “talkathon.”

This is the dollar liquidity chart. As the Fed began hiking rates and QT in March 2022, the index plummeted. However, since RRP declined starting June 2023, the index has returned to lows last seen in April 2022.

This chart shows a sub-component—the net change in RRP and TGA balances. Since the U.S. government passed its budget in June 2023, nearly $800 billion in new liquidity has been injected.

From a macro perspective, despite a $1.2 trillion reduction in the Fed’s balance sheet, risk assets continue to surge due to relatively high dollar liquidity.

First Crisis

Looking deeper at failed non-TBTF banks, we see Yellen and Powell were forced to act to rescue the U.S. banking sector. The above chart shows the white S&P Regional Banking ETF (KRE) versus the yellow 2-year Treasury yield. Banks in this index are small-to-mid-sized institutions that don’t enjoy the same government deposit guarantees as the more prominent and profitable TBTF banks. A sharp rise in yields in Q1 2023 caused KRE to crash, leading to the collapse of three non-TBTF banks (Silvergate, Signature, and Silicon Valley Bank) within two weeks. Once markets realized the Fed would have to print via BTFP to save the system, yields plunged.

Second Crisis

Things were calm for a while, but markets started focusing on runaway U.S. deficits and the massive bond issuance needed to finance them. Powell complicated matters during his September 2023 FOMC press conference, stating financial markets would do the Fed’s monetary tightening work. Bond markets wanted the Fed to fight inflation with further hikes and higher government borrowing costs—not just watch Bloomberg terminals passively. Interest rates rose across the curve, most concerningly with long-end rates steepening in a bearish manner—deadly for the financial system. KRE reacted by falling to levels last seen during April’s banking crisis peak. Yellen was forced to act in November, shifting borrowing into T-bills. This saved the bond market and triggered a vicious short-covering rally in stocks and bonds.

Hopium

Markets now speculate when RRP balances will near zero and wonder what comes next. There’s much discussion, including speculation about how the Fed might add liquidity without calling it money printing. But no action has been taken. The 2-year yield has rebounded, yet KRE continues rising—markets are drinking the Kool-Aid. If Yellen and Powell are correct, 10-year yields will magically drop from 3% to 2%. That won’t happen without new dollar demand for bonds. This explains the divergence between 2-year yields and KRE. I believe markets face an unpleasant surprise because it’s clear Powell will only “roar” without making bold moves.

This busy chart shows the difference between Bitcoin (white) and the 2-year Treasury yield (green)—telling the same story—while SPX (yellow) tells a different one. From November 1, 2023 onward, as 2-year yields fell, both Bitcoin and SPX rose. Once 2-year yields bottomed and reversed, Bitcoin declined while SPX continued climbing.

Bitcoin is telling the world the Fed is caught between inflation and banking crises. The Fed’s solution is trying to convince markets banks are sound without providing the necessary funding to make that fantasy real.

Fragile Foundations

Jim Bianco produces excellent charts, and the rest of this article will focus on analyzing them.

As readers know, I spent the northern winter in Hokkaido, Japan. One noticeable seasonal shift is the sheer number of Americans. Even for Asians, visiting this powder-snow paradise is painful—it’s even more time-consuming and expensive if you live in the U.S.

Yet, there’s a visibly growing number of American baby boomers skiing at resorts. Baby boomers are the wealthiest generation they’ve ever been. Stock and home prices are at historic highs. Plus, their cash reserves are earning yields for the first time in decades. For a group that nearly died during the pandemic (flu deaths mostly affected elderly obese individuals—i.e., boomers), now is the time to travel the world.

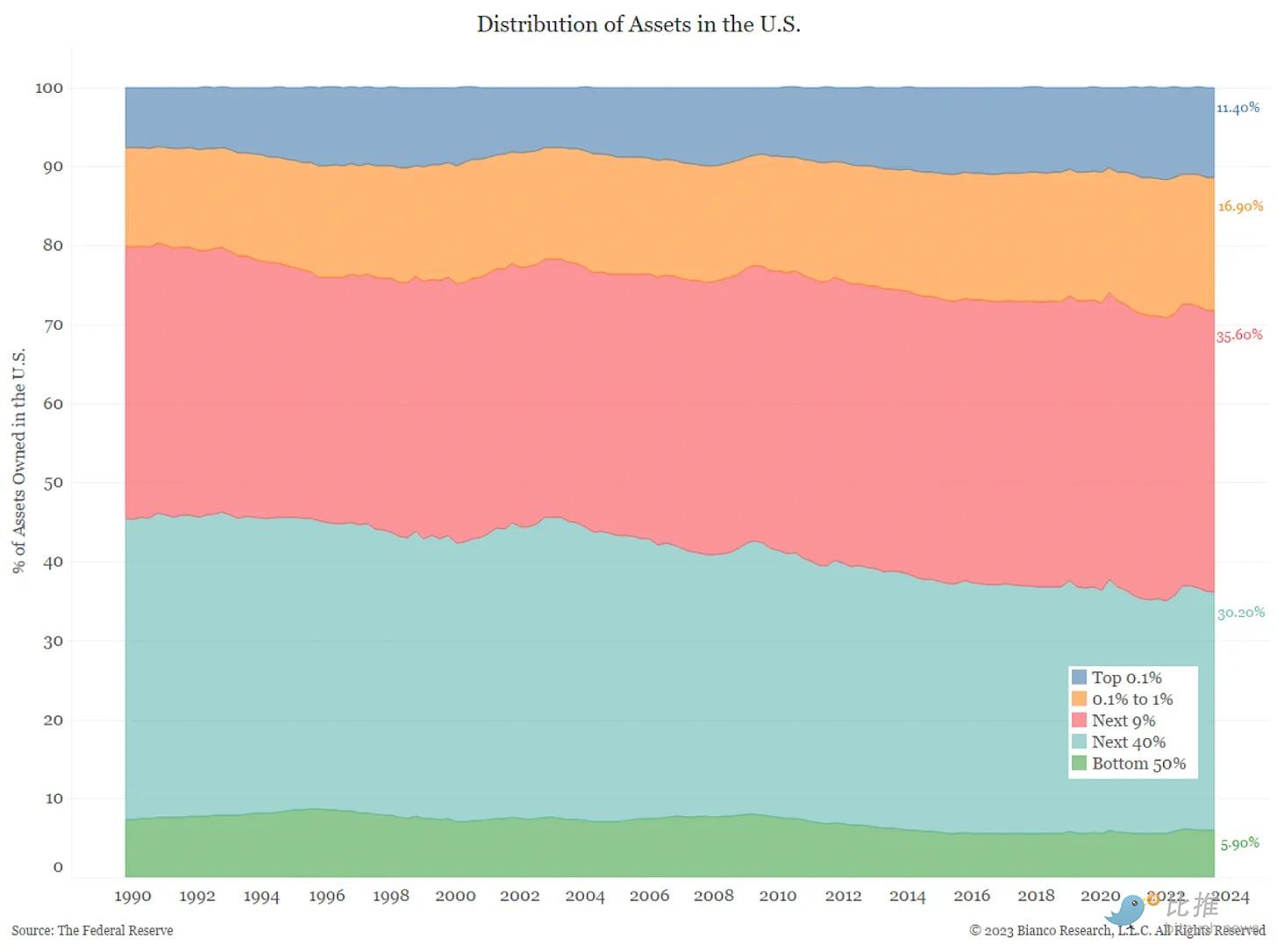

The wealthiest 10% of U.S. households own about 65% of the financial assets injected by the Fed’s various money-printing programs. Boomers are the richest generation, and their spending is fueling a very strong U.S. economy.

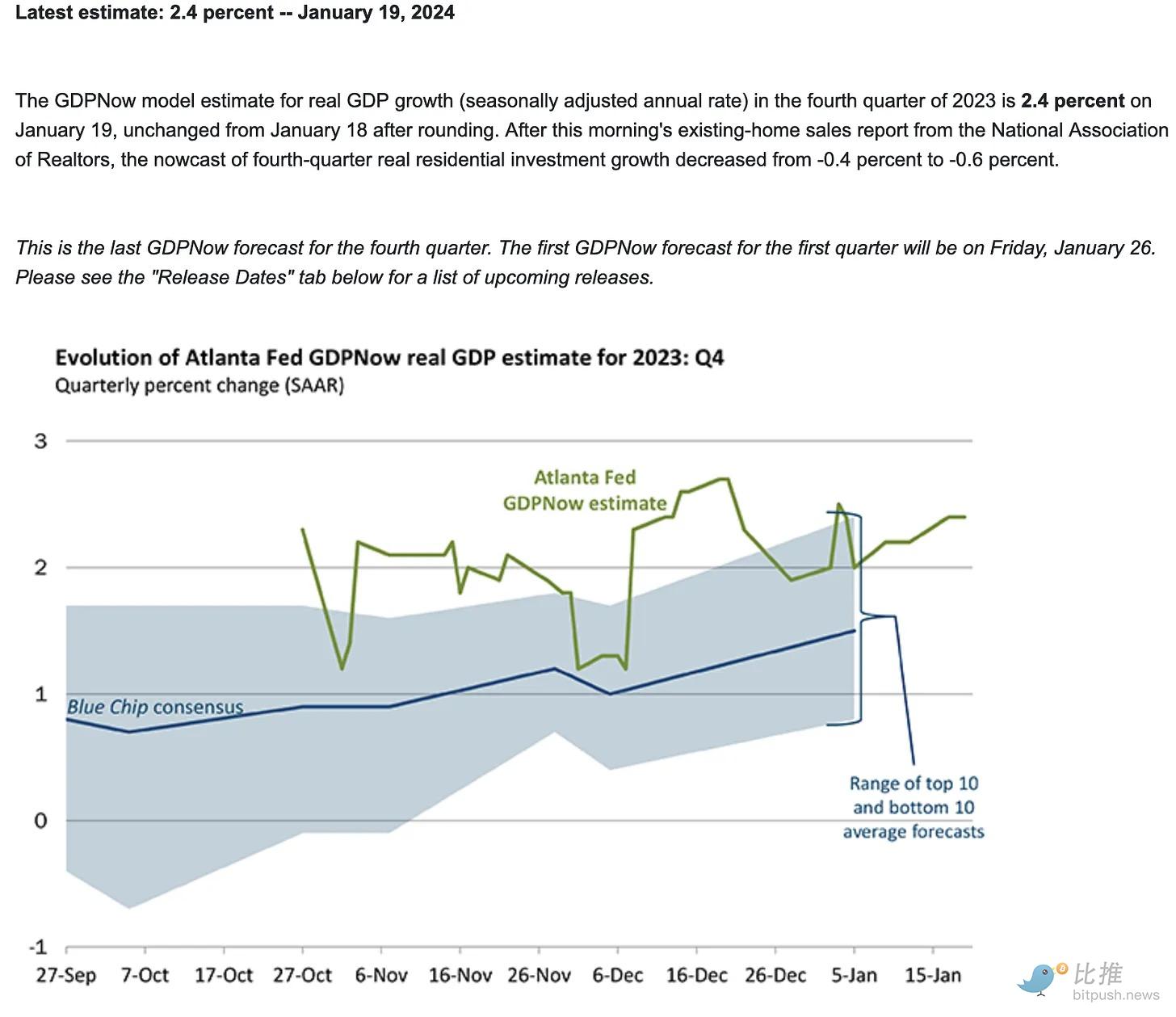

The Atlanta Fed projects strong +2.4% GDP growth for Q4 2023—too strong, very strong!

Yet, the rest of America is already bankrupt and deep in debt.

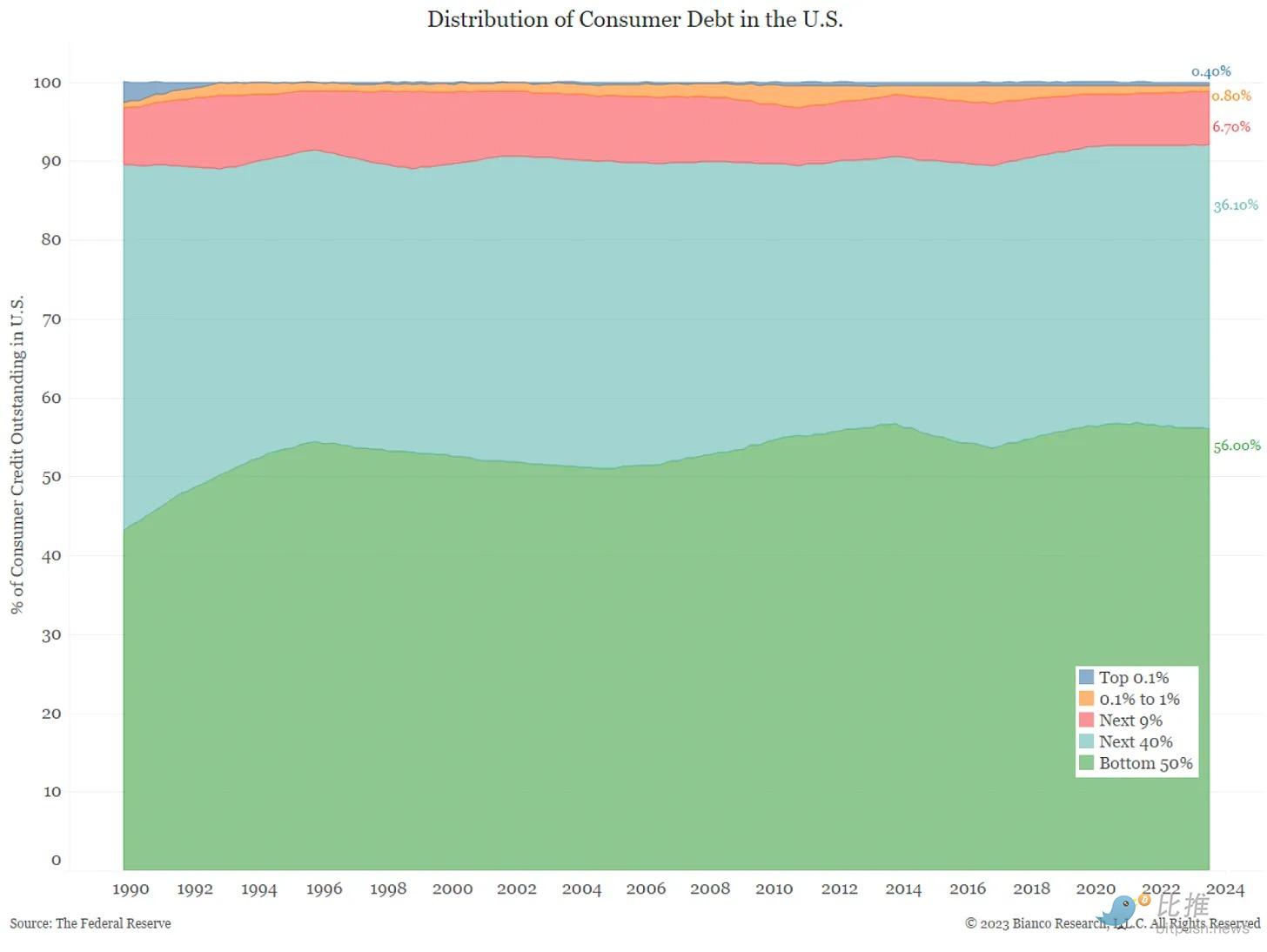

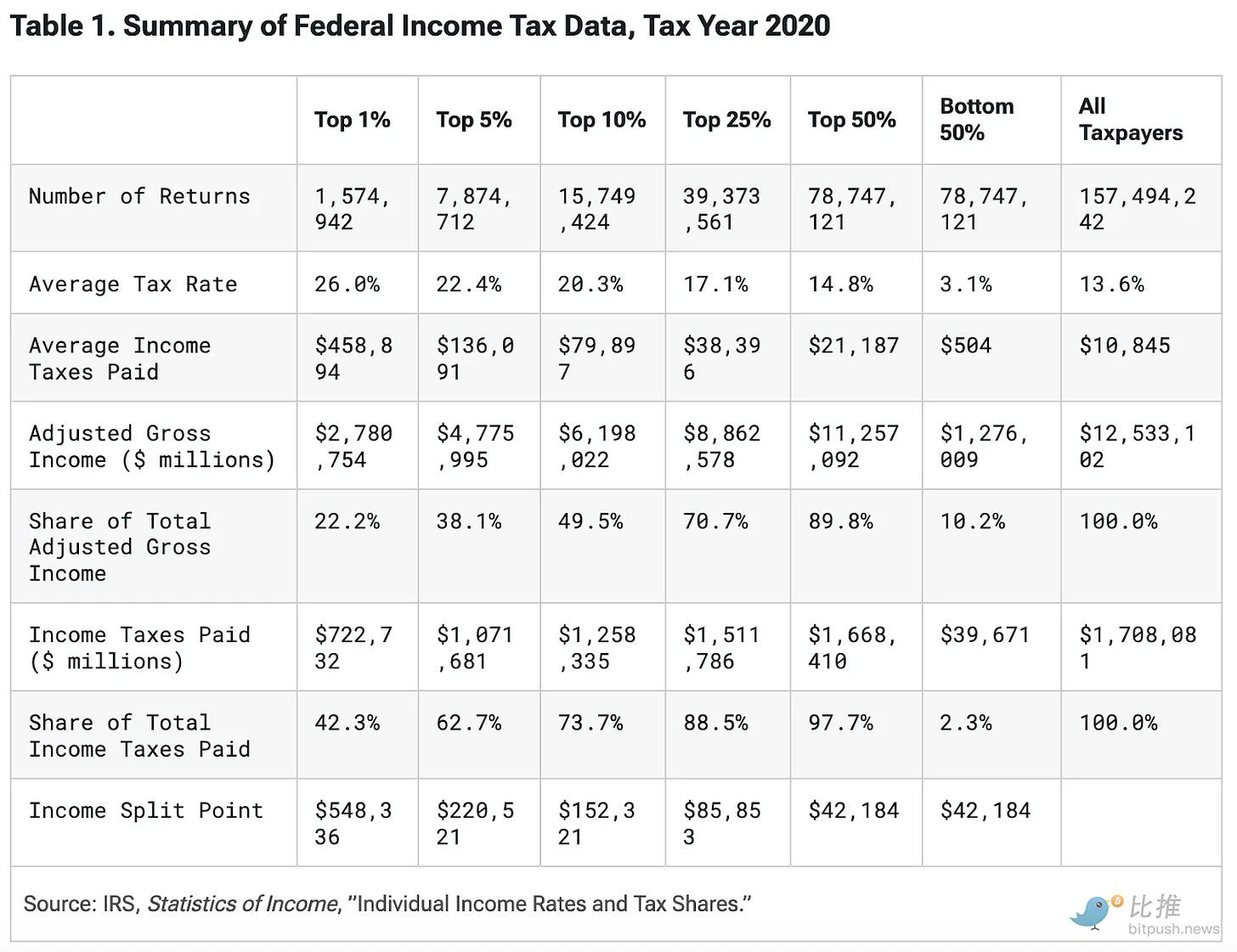

The top 10% hold about 65% of financial assets but only 8% of debt. The bottom 90% hold 92% of debt but only 35% of assets.

This extreme inequality in wealth and debt distribution presents politicians in democracies with a problem. While politicians are determined to enrich the rich at all costs, they need bankrupt citizens’ votes to get elected. That’s why inflation becomes an issue.

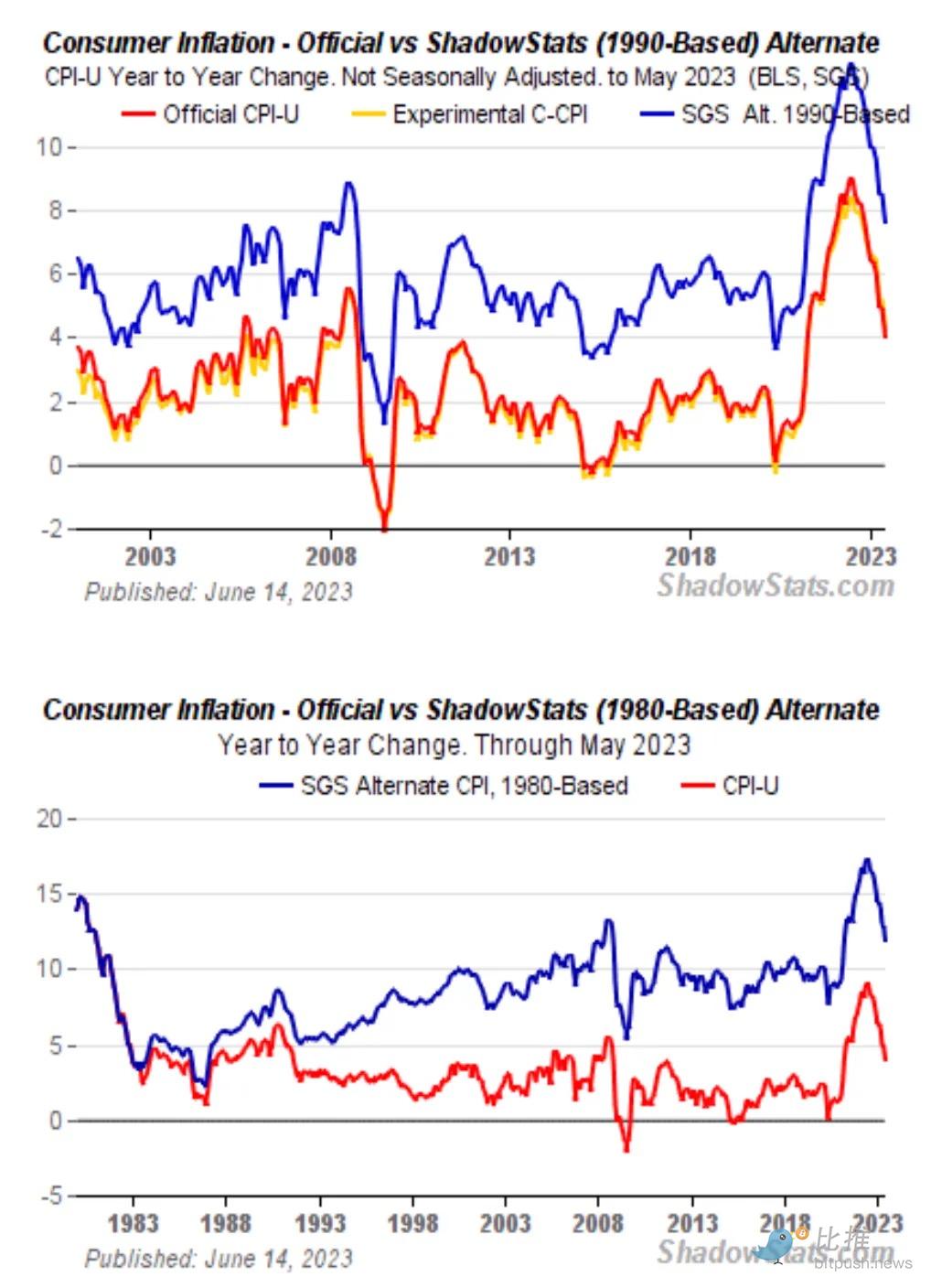

The current Consumer Price Index (CPI) calculation method is Fugazi. If we reverted to CPI calculations from 1980 or 1990, real inflation would be around +10%, compared to the +3% you read in the news.

That’s why, according to latest polls, Trump has a slight edge over Biden.

In short, U.S. politics resembles a circus where the rich buy ads to promote their favorite clowns, who dance and sing to win commoners’ votes. Biden must hand out goodies to both rich and poor to win. Cynically, at the macro level, the strategy is to inflate stock markets owned by the rich, increasing tax revenue, then use loot collected from the rich to provide relief to the poor.

The top 10% pay 74% of income taxes. Their massive contributions stem from large capital gains taxes collected by the government during stock market rallies. Thus, the U.S. government’s fiscal health is tied to stock market performance.

Biden has two “financial generals” with distinct missions. Yellen must use the Treasury’s power to boost the stock market—by adjusting Treasury issuance schedules or shrinking the TGA. Powell must reduce inflation to acceptable levels—via rate hikes and balance sheet reduction.

Yellen’s job is far easier than Powell’s. She can unilaterally boost equities by issuing more T-bills and bonds or reducing the TGA from its current $750 billion to zero. Powell can reduce money supply and raise rates, but he has zero control over geopolitical issues. He also cannot influence the size of government deficits or surpluses. Assuming the government remains committed to massive deficits, Yellen will appropriately fund them, increasing demand for goods and services. In such cases, Powell’s anti-inflation efforts at the Fed will be undermined.

Post-pandemic U.S. inflation was so pronounced because the government distributed stimulus funded by Fed money printing at a time when global freight transport was difficult. Pandemic lockdowns and vaccine policies caused labor shortages and disruptions. Result: inflation reached levels unseen since the late 1970s and early 1980s.

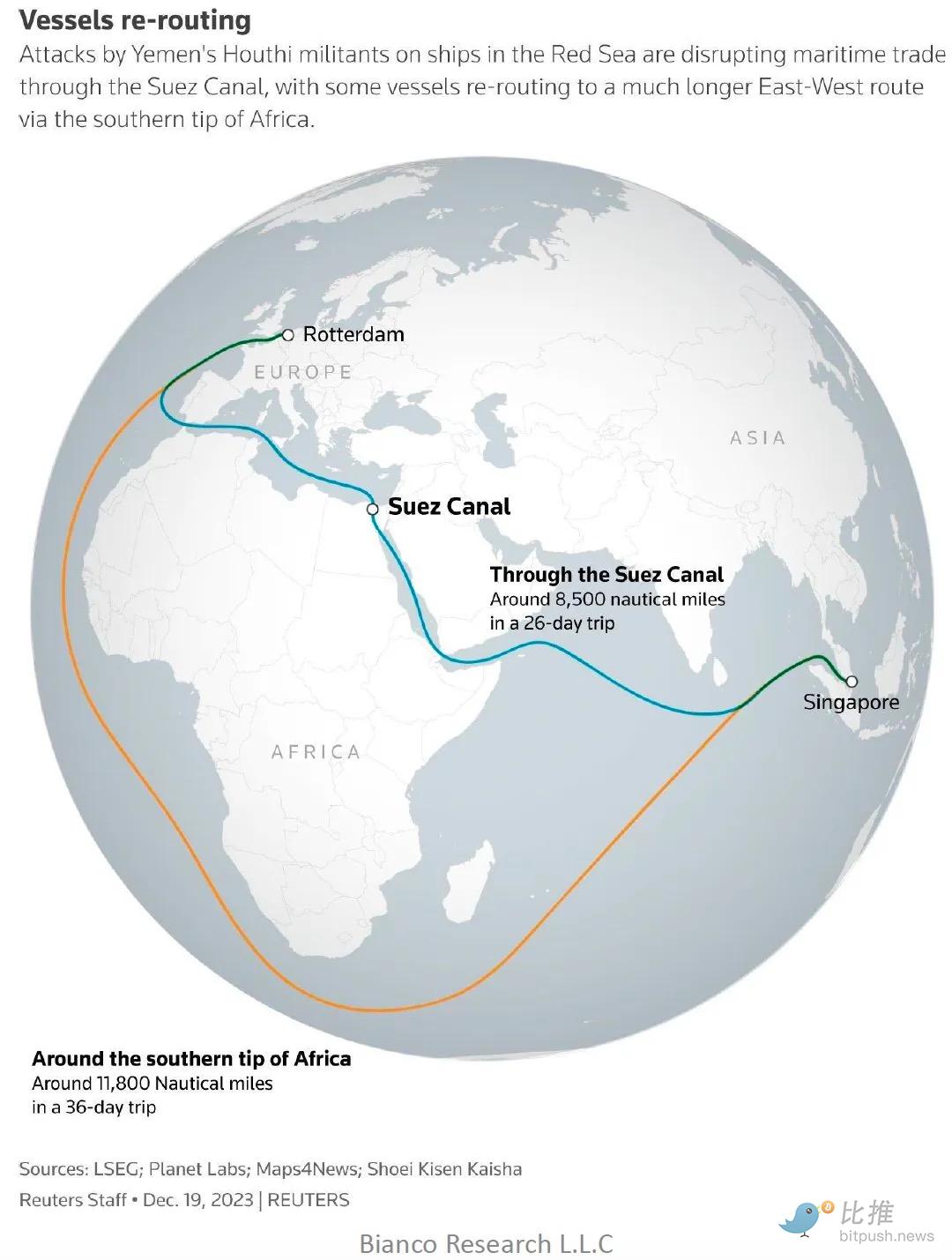

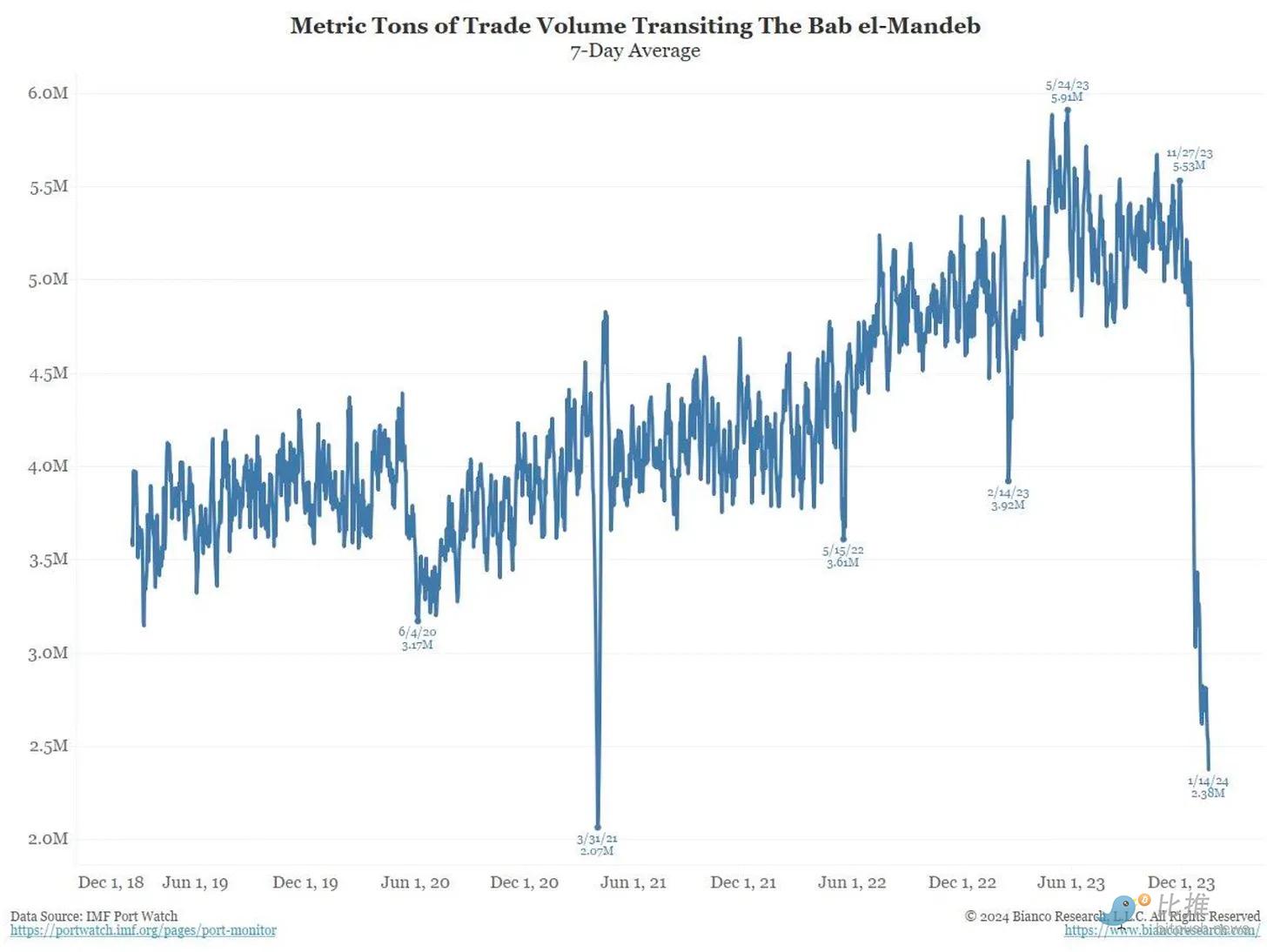

A similar global supply chain crisis is unfolding now—but this time, shipping difficulties stem from El Niño and Western vessels avoiding the Bab-el-Mandeb Strait.

Horns and Hope

Shipping is an ancient but vital business. Compared to rail, road, or air, maritime transport is cheapest per kilometer traveled. Without the Panama Canal or Bab-el-Mandeb Strait, ships must detour around Cape Horn or the Cape of Good Hope. El Niño weather patterns have caused drought in the Panama Canal, lowering water levels and reducing the number of transit-capable vessels. Yemen’s Houthi asymmetric drone warfare has effectively blocked Western vessels from using Bab-el-Mandeb. They must now sail around the Cape of Good Hope.

These detours affect 20% to 30% of global shipping, adding significant time and cost. For inflation statisticians, everything shipped by sea becomes more expensive, ceteris paribus. Given inflation’s considerable lag, the full impact won’t be felt for months. While markets cheer declining year-over-year inflation data in the U.S. and elsewhere, this may prove a costly victory.

The El Niño pattern has only just begun. Mild El Niño events typically last one to two years. Regardless of severity, El Niño will still be active in November. Sadly, if you’re a Biden supporter, he is powerless over weather—humans aren’t Kardashev Type I civilizations. El Niño and climate change overall lower Panama Canal water levels, reducing vessel throughput.

Reduced Panama Canal traffic is significant because the U.S. is rerouting some cargo via Europe to eastern seaboard ports to avoid the canal. But given Asian-to-Europe freight on Western vessels must now bypass Africa instead of transiting the Red Sea, transport costs and time increase.

The Houthis claim they will attack any vessel from any country supporting Israel. They view Israel’s Gaza war as a genocide prosecuted by war criminals like Prime Minister “Bibi” Netanyahu. To show solidarity with their Muslim and Arab kin, they use $2,000 drones to attack commercial ships. A cheap drone can completely disable a $200 million vessel—that’s asymmetric warfare defined. Consider: the U.S. must fire a $2.1 million missile to neutralize a $2,000 drone. Even if Houthi drones never hit targets, each drone incurs a 1,000x higher defensive cost for the U.S. Mathematically, this is a war the U.S. cannot win.

According to three additional Defense Department officials, the cost of using expensive naval missiles (up to $2.1 million each) to destroy simple Houthi drones (estimated at several thousand dollars apiece) is becoming increasingly concerning.—Politico

Given the U.S., as issuer of the global reserve currency, bears responsibility for maritime security, the world watches how Pax Americana responds to this brazen military challenge. From Houthi statements, attacks would cease if the U.S. severed ties with Israel and forced Bibi to end the war. Yet even if America views Bibi as a genocidal maniac, the U.S. empire won’t abandon an ally just because a “shithole” nation’s government launched a few cheap drones and closed one of the world’s most critical waterways.

Even if Biden loudly calls on Bibi to end the war and stop murdering so many Gazan men, women, and children, he will never cease financial and military support for Israel over fear of losing face. The result: the entire world lives under the threat of war escalation.

I predict we’ll witness firsthand how difficult it is for the red, white, and blue fist to crush swarms of drones. For shipping firms to regain confidence in Red Sea transit, the U.S. Navy must perform flawlessly in every engagement. Every drone must be destroyed. Because even a direct payload strike could incapacitate a merchant vessel. Additionally, with the U.S. now engaged in conflict with Yemen’s Houthis, shipping insurance premiums will soar, making Red Sea passage even less economical.

Rising transport costs from weather and geopolitical factors could trigger an inflation spike in Q3 and Q4 this year. Aware of these risks, Powell will do everything possible to talk big about rate cuts without actually cutting. Inflation driven by higher transport costs may rise moderately, but rate cuts and QE restart could exacerbate inflation further. Markets haven’t realized this yet—but Bitcoin has.

Only a financial crisis trumps fighting inflation. That’s why, to achieve the cuts, QT slowdown, and potential QE resumption markets expect by March, we first need some bank failures when BTFP isn’t renewed.

Tactical Trading

After ETF approval, BTC’s range high of $48,000 saw a 30% correction to $33,600. Hence, I believe Bitcoin will find support between $30,000 and $35,000. That’s why I bought $35,000 put options expiring March 29, 2024, and exited Solana and Bonk trades at minor losses.

Bitcoin and crypto overall represent the world’s last free-trading markets. Thus, they anticipate changes in dollar liquidity before TradFi fiat stock and bond markets react. Bitcoin tells us to watch Yellen—not the talk.

Yellen has a chance to inject more juice into markets with the QRA release on January 31. If she announces plans to reduce the TGA from $750 billion to zero, we’ll know of another unexpected liquidity source capable of propping up markets. Then the question becomes: once BTFP expires, will that be enough to prevent bank failures?

I believe BTFP won’t be renewed, as neither Yellen nor Powell has mentioned it once. The natural assumption is it will expire, forcing banks to repay nearly $200 billion in borrowings. If circumstances change and they clearly signal an extension, game on. I’ll close my puts and maximize crypto exposure by selling T-bills and buying cryptos.

If my base case unfolds, once Bitcoin drops below $35,000, I’ll start accumulating and continue buying Solana and WIF.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News