"1·23" Plunges Into Technical Bear Market, Can Crypto Escape the "TradFi Curse"?

TechFlow Selected TechFlow Selected

"1·23" Plunges Into Technical Bear Market, Can Crypto Escape the "TradFi Curse"?

In hindsight, each milestone event in TradFi has historically signaled a market peak in the crypto space.

By Frank, Foresight News

After the ETF dust settles, is there no new narrative to carry the bull market forward?

Under gloomy market sentiment, Bitcoin has experienced a "clearly foreseeable sharp drop": after breaking below the psychological $40,000 mark in the early hours of January 23 (based on OKX spot data, same below), it began falling again from 15:00 today, briefly dropping below the $39,000 USDT level, with a 24-hour decline exceeding 4.4%.

ETH also successively broke through the $2,400 USDT and $2,300 USDT levels within 24 hours, hitting a low of $2,212 USDT. Meanwhile, the altcoin market is even more chaotic—previously strong performers such as SOL and BNB have generally fallen over 20% or more from their recent highs.

Overall, since the approval of spot Bitcoin ETFs on January 11, the crypto market has not seen a wild rally but instead entered a volatile downtrend: it has dropped over 20% cumulatively from its recent high of 48,988 USDT, entering a technical bear market.

What’s Behind the Plunge?

If we revisit the usual suspects behind potential bearish factors, we find that “open secrets” are a defining feature of this downturn.

Ongoing BTC Selling Pressure from Grayscale's ETF

First is the sustained BTC selling pressure caused by Grayscale Investments’ GBTC trust following its successful conversion into a spot ETF:

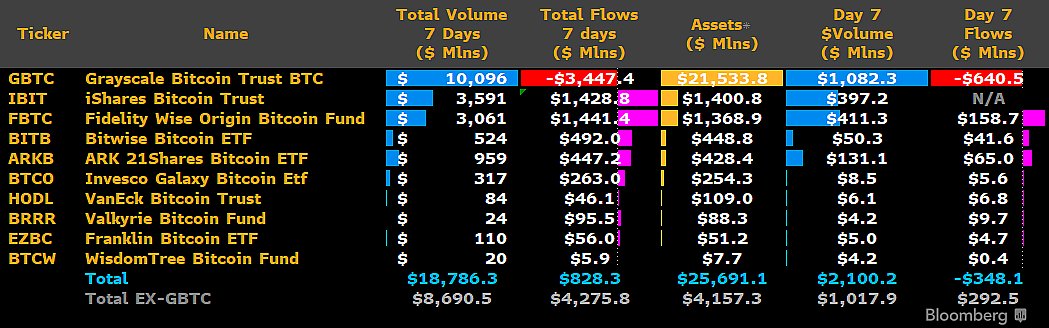

At the time of writing, GBTC saw another single-day outflow exceeding $640 million, marking its largest daily capital outflow to date. Since converting to an ETF, total outflows have reached $3.45 billion, while all other 10 Bitcoin ETFs combined remain in net inflow territory.

In particular, during the first seven trading days after approval, total volume across all spot Bitcoin ETFs was approximately $19 billion, with GBTC alone accounting for over half—indicating that the incremental capital brought by new ETFs is still largely offsetting the ongoing outflows from GBTC.

Of course, a significant portion of the sell-off also comes from the bankrupt FTX—its liquidation of 22 million shares of GBTC is worth nearly $1 billion.

Overall, although Grayscale and GBTC were among the biggest engines of the previous bull run—providing compliant crypto investment access via trust funds for years—the post-ETF outflows and selling pressure were predictable:

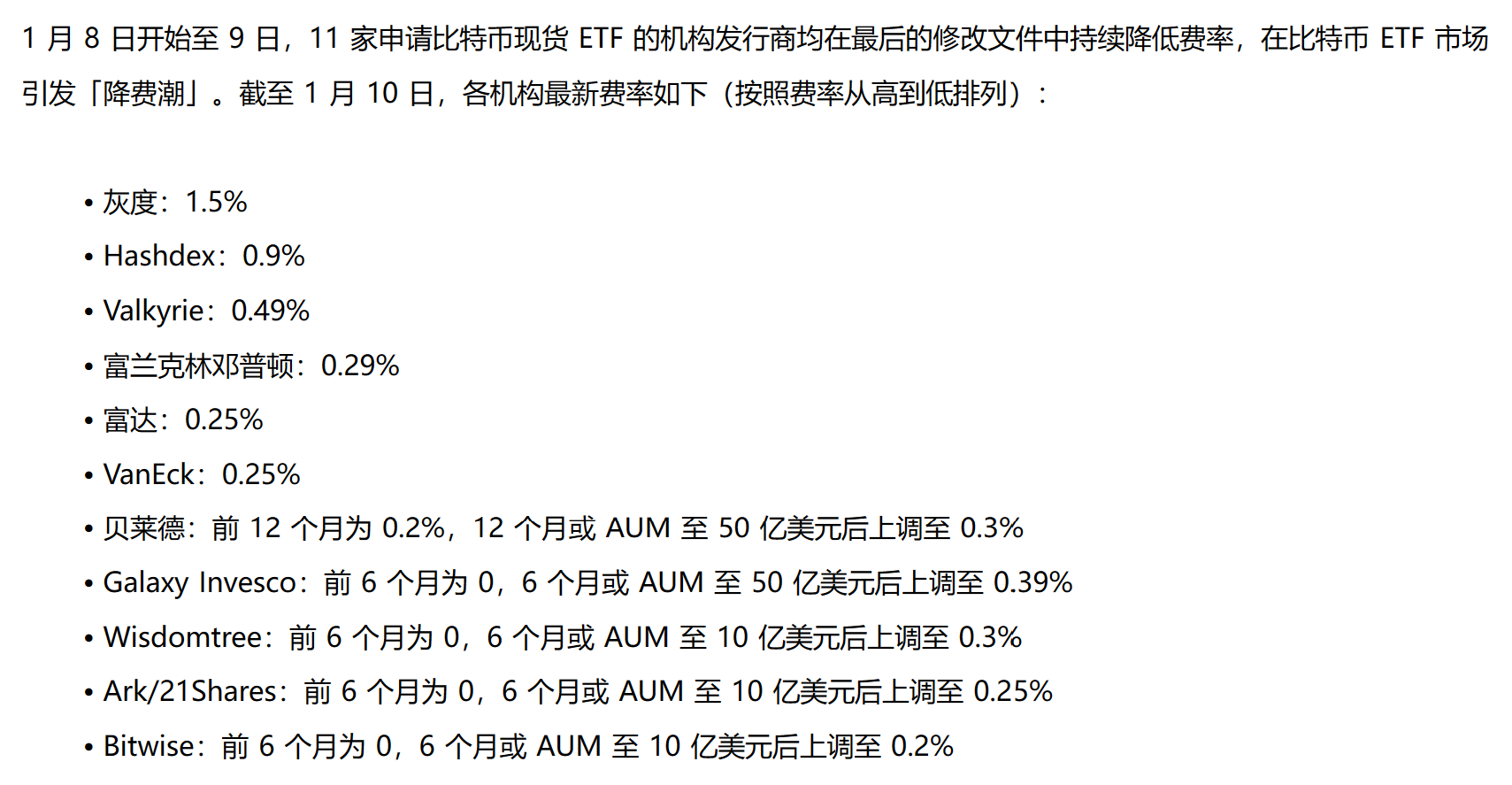

First, GBTC’s 1.5% management fee is far higher than other ETF providers’ range of 0.2%-0.9% (see “Cheap Is the New Profit? The Battle Behind Bitcoin Spot ETF Fees…”)

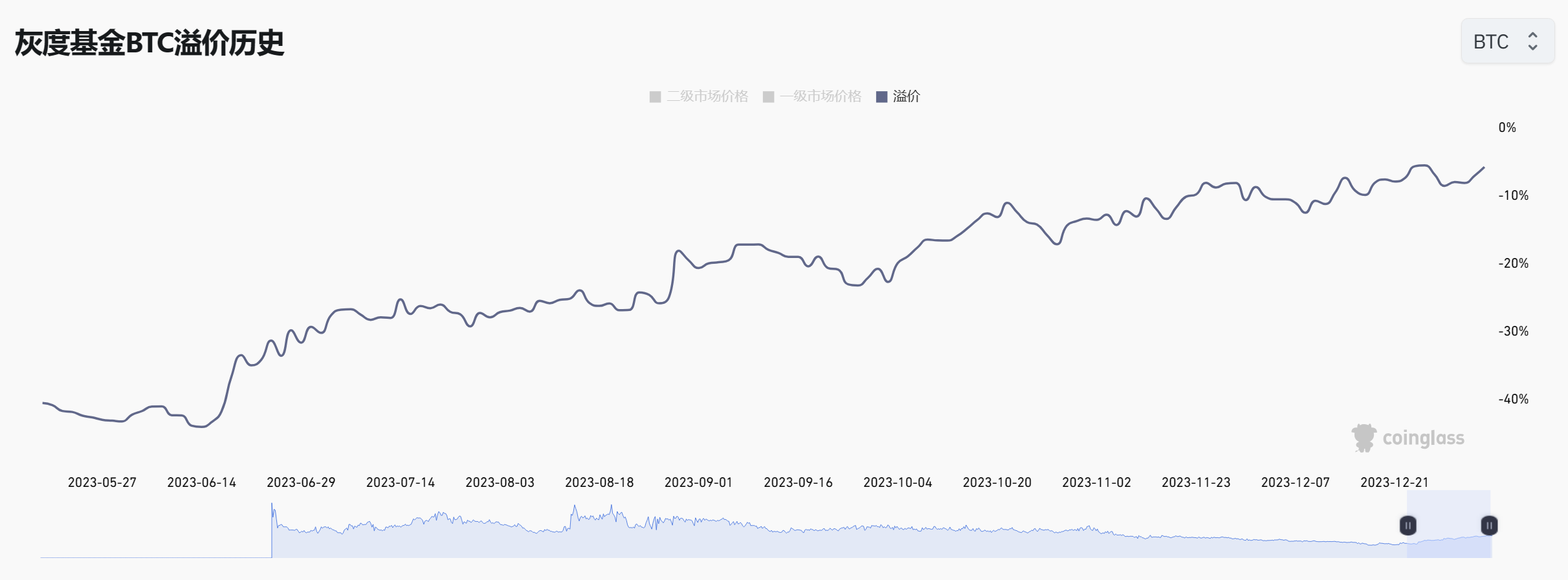

Second, during the prolonged anticipation and speculation around ETF approval over the past several months, GBTC’s negative premium steadily narrowed—from a discount of around 30% to nearly zero today—meaning the majority of early investors who bought in at a discount have now reached a profitable exit point (e.g., Cathie Wood).

To some extent, this sets up a transparent game ahead: GBTC still holds over 500,000 BTC (worth about $20 billion). Institutional players waiting on the sidelines will undoubtedly look for optimal moments to accumulate positions and erode its share.

This implies that, for the foreseeable future, GBTC’s selling pressure may continue to outweigh investor appetite for inflows.

Mt. Gox: The Sword of Damocles

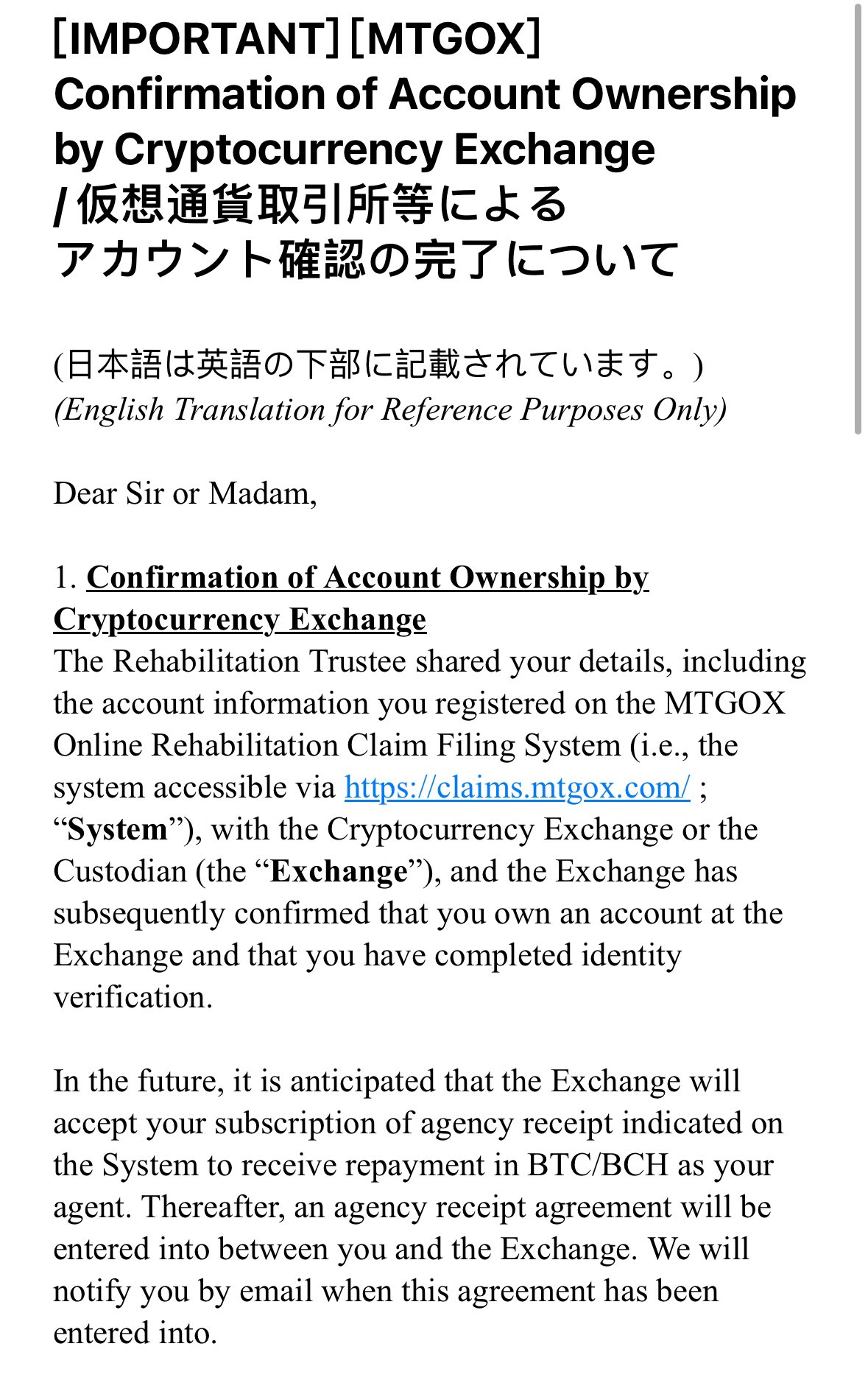

Additionally, DeFi founder Mike Cagney recently tweeted that Mt. Gox creditors have received emails confirming ownership of exchange addresses previously submitted, which will be used to receive BTC/BCH payouts.

Cagney added, “Around 200,000 BTC will be unlocked over the next two months to pay creditors, and PayPal fiat channels have already started disbursing payments.”

Although the official repayment deadline for Mt. Gox trustees has been extended to October 31, 2024, eligible creditors began receiving repayments as early as late 2023. If this pace continues, the disbursement of 200,000 BTC over the next two months—paid out in fiat—could equate to $8 billion in outright selling pressure.

However, it’s worth noting that official disclosures list holdings at only 142,000 BTC, 143,000 BCH, and 69 billion JPY—not 200,000 BTC.

Potential Selling Pressure from Celsius?

In addition, recent on-chain activity has frequently shown large transfers of ETH and other crypto assets from Celsius wallets to centralized exchanges (CEX) or market maker addresses.

As of mid-month, the Celsius wallet held approximately 584,000 ETH (around $1.4 billion), with 92,000 ETH already transferred to Coinbase and FalconX—suggesting potentially over 500,000 ETH could still be available for sale.

However, analysis indicates that of the 584,000 ETH, about 536,000 ETH will be distributed in-kind to unsecured claimants; 62,000 ETH will be distributed physically to facilitate claims; and roughly 26,000 ETH may have already been sent to Coinbase and PayPal to handle custodial claim distributions.

This means most ETH will be directly distributed to creditors, leaving Celsius with extremely limited capacity to act on remaining holdings (see “Over 500K ETH Up for Sale? The Data and Madness Behind Celsius”). In short, Celsius cannot “sell all its ETH,” otherwise it would fail to meet its legal obligations to creditors.

Other Factors

Notably, CoinShares’ 2023 mining report forecasts that after the halving, the average production cost per Bitcoin will be $37,856. Unless Bitcoin remains above $40,000, only Bitfarms, Iris, CleanSpark, TeraWulf, and Cormint can remain profitable (see “CoinShares Mining Report: The Bitcoin Cycle Code Hidden Behind the Halving”).

Currently, Bitcoin’s market price is already near this critical cost threshold. With the April block reward halving approaching, miners will likely increase capital spending to gain advantage in the upcoming arms race—potentially leading to continued miner selling and triggering a new cycle of industry consolidation.

Summary

History doesn’t repeat itself exactly, but it often rhymes.

Looking back in hindsight, for the crypto industry, nearly every major TradFi-related milestone in history has later proven to be a signal of short-term market topping:

-

On December 10, 2017, the Chicago Board Options Exchange (CBOE) launched Bitcoin futures, followed by the Chicago Mercantile Exchange (CME). Bitcoin briefly surpassed $20,000 USDT, reaching a then-record high—but soon began a multi-year bear market lasting over two years;

-

On April 14, 2021, the day Coinbase went public, Bitcoin hit a record high of $64,000 USDT, only to lose half its value within two months, falling to $28,000 USDT;

-

Later in October that year, after ProShares launched the first U.S. Bitcoin ETF (a futures-based product), Bitcoin peaked within two weeks and entered a sustained downtrend.

While “sell the news” certainly plays a role, these events also reflect that traditional finance’s impact on crypto is not simply one-directional—it’s easy to overestimate short-term effects and underestimate long-term implications.

In retrospect, each of these milestones contributed to the industry’s broader mainstream adoption over long cycles, despite significant short-term pullbacks.

Stay optimistic, avoid euphoria—history moves upward in a spiral of setbacks. As Brent Donnelly, President of Spectra Markets and currency trader, told the media:

“This is a logical, almost inevitable evolution process—a nascent security with extreme uncertainty in value and price is becoming a mainstream asset embraced by millions of participants.”

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News