Interview with MakerDAO Core Engineer: RWA is the Bull Market Engine, Stablecoins are the Killer App

TechFlow Selected TechFlow Selected

Interview with MakerDAO Core Engineer: RWA is the Bull Market Engine, Stablecoins are the Killer App

Decentralized finance can only thrive again by internalizing interest rates into its ecosystem.

Author: Sunny, TechFlow

MakerDAO: Sam Macpherson and Tadeo

"I believe the entire financial system will eventually run on blockchains, at which point there will be no more default risks as seen in traditional finance; it will simply be finance, with all transactions settled on-chain. So I don't know how long it will take, but to me, this future is inevitable."

--Sam Macpherson, Core Developer at MakerDAO

Background of the Discussion

At Token2049 in Singapore this year, Rune Christensen, founder of MakerDAO, introduced the "Endgame Plan." This plan aims to address scalability and inefficiency issues within MakerDAO by redefining the role of the Maker core. Instead of directly pursuing various small-scale projects and growth initiatives, the Maker core would transition into a role more akin to a "wholesale creditor." In this new capacity, the Maker core would provide loans or support to other subDAOs (sub-decentralized autonomous organizations), which would operate independently. These subDAOs are described as mini-versions of MakerDAO, each focusing on different growth strategies and projects, while being isolated and independent from one another.

Spark Protocol is an emerging subDAO designed to build a lending protocol focused on DAI and already integrated with MakerDAO. Sam Macpherson, founder and CEO of Spark Protocol, previously served as a core engineer at MakerDAO. Tadeo is a developer relations engineer at Spark. Since late 2022, Spark Protocol has achieved a total value locked (TVL) exceeding $1 billion. At last month’s Ethereum developer conference in Istanbul, SparkFi sponsored ETHGlobal Istanbul with a prize pool of 20,000 DAI awarded to winning builders who created projects under the SparkLend category. The Spark team aims to build a decentralized lending engine that provides modern lending platform features and capabilities for Dai users, as the existing MakerDAO core contracts are considered somewhat outdated.

In our interview with Sam and Tadeo, we learned about Spark's independence from third-party liquidity compared to other DeFi lending protocols, the market impact of tokenized U.S. Treasuries on Web3, and whether stablecoins could become the killer application for Web3.

Sam firmly believes that real-world assets (RWAs) will trigger the next full-market upcycle. With interest rates in traditional finance so high today, they have essentially drained nearly all liquidity from decentralized finance (DeFi). Therefore, the first step is to bring these yields on-chain, allowing DeFi and traditional finance interest rates to converge until they match. Only when these rates are internalized within DeFi can DeFi flourish again—and this process is already underway.

Below is TechFlow's summary and synthesis of the interview:

Knowledge Recap

MakerDAO:

-

MakerDAO is a decentralized autonomous organization operating on the Ethereum blockchain. It is best known for its stablecoin DAI, which is backed by collateralized assets. MakerDAO allows users to generate DAI by locking collateral in smart contracts known as vaults or Collateralized Debt Positions (CDPs).

-

Users can interact with MakerDAO through Web3 wallets and other decentralized applications such as Lido and Aave v3.

-

DAI, issued by MakerDAO, has become one of the leading stablecoins by market capitalization.

DAI's Over-Collateralization Model:

-

Dai is described as an “over-collateralized” stablecoin. This means that to create and maintain DAI, users must deposit collateral assets (cryptocurrencies or other forms of value) worth more than the amount of DAI they wish to mint. This over-collateralization acts as a safety mechanism to maintain the stability of the stablecoin.

-

Importantly, the collateral backing DAI includes native crypto assets (such as ETH), other assets like “sticky assets” (possibly referring to stable assets within the MakerDAO ecosystem), and Bitcoin. It also includes cash-like assets, potentially stable assets or fiat currencies.

-

The over-collateralization ratio for DAI is precisely 0 or equal to 1, differing from other stablecoins that require higher ratios (e.g., 150% or 200%). This means you can generate DAI using collateral equivalent in value to the amount of DAI you are creating—a unique feature of DAI.

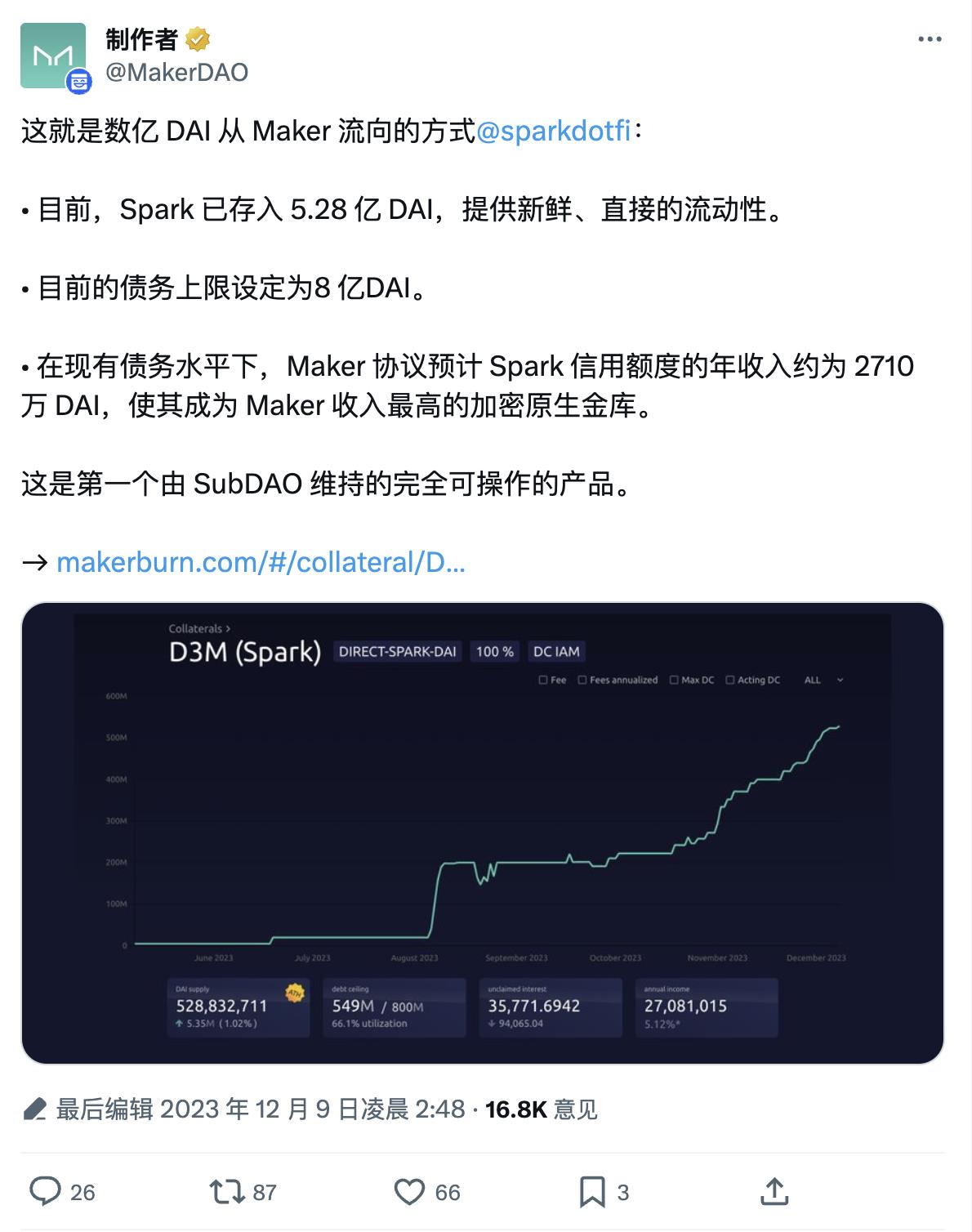

MakerDAO’s Native DeFi Protocol: Spark

Since launching a modern lending engine within the MakerDAO ecosystem, Spark has experienced significant growth, positioning itself among the top 20 DeFi protocols by total value locked (TVL).

Secondary Lending Markets: The discussion referenced secondary lending markets such as Compound and Aave, which allow users to borrow and lend various cryptocurrencies, including stablecoins like DAI, USDC, or Tether (USDT).

Need for Intermediaries: These secondary lending markets require intermediaries or lenders to provide liquidity. These lenders need to hold reserves of certain assets (e.g., DAI, USDC) and seek profit by lending them out to borrowers.

Maker’s Role in Spark: The innovation introduced by Spark is that MakerDAO itself can act as a lender on this platform. In other words, instead of relying on profit-driven individual lenders, MakerDAO directly supplies liquidity.

Minting DAI: MakerDAO can directly mint DAI tokens onto Spark’s lending platform. When users want to borrow DAI, they are effectively borrowing directly from MakerDAO—similar to how the internal vault system operates within MakerDAO.

Predictable Borrowing Rates: A major advantage of Spark is that users can borrow at predictable interest rates set by MakerDAO. In contrast, rates in other secondary markets can be highly volatile and depend on liquidity availability. Sometimes, rates may spike to very high levels, introducing uncertainty for borrowers.

Governance Process: Spark maintains predictable rates through a well-defined governance process. Users are notified several weeks in advance of any upcoming rate changes, allowing them time to plan and adjust their positions accordingly.

Minimum Rates: Due to MakerDAO’s substantial liquidity ("unparalleled liquidity," as Sam noted), interest rates on Spark are expected to be among the lowest in the market, making borrowing more cost-effective for users.

The Evolution of RWAs

Historical Context: Two years ago, traditional banks and money market funds offered very low interest rates (around zero) to users holding USDC. This meant users were content keeping their USDC on-chain for various purposes, such as trading Ethereum (ETH).

Change: Over the past two years, traditional banks have started offering higher interest rates (5% in this example). This shift makes holding USDC on-chain within DeFi more expensive, as users now forgo potential interest income they could earn by moving USDC to their bank accounts.

User Behavior Shift: As a result of this rate change, users are increasingly inclined to move their USDC out of DeFi and into their bank accounts. This action removes liquidity (funds) from the DeFi ecosystem, potentially affecting DeFi projects and markets.

Tokenization of Treasury Bonds: To address this issue, "tokenization of Treasury bonds" was mentioned. This refers to converting U.S. Treasury bonds into digital tokens usable within the DeFi ecosystem. Users can use these tokenized Treasury bonds as collateral for lending and other DeFi activities.

Impact on DeFi Interest Rates: By bringing Treasury yields (interest rates from Treasury bonds) into DeFi via tokenization, users can now earn interest on their tokenized Treasury bonds while participating in DeFi activities. As more users use these tokenized assets as collateral, DeFi platforms begin offering higher lending and service rates. This effectively raises the base interest rate within the DeFi ecosystem.

Rate Comparison: Sam noted that DeFi lending rates, once close to 0%, now typically range between 3% and 4%. This means DeFi lending rates have become competitive with the risk-free rates offered by Treasuries.

The Next Killer App for Mass Adoption

Web3 Needs a Killer Application: Sam and Tadeo acknowledge the importance of having a compelling, widely adopted application—a “killer app”—that can drive adoption and usage of blockchain and cryptocurrency technology among everyday retail users. However, they admit they don’t yet have a concrete idea for such an app, emphasizing instead the importance of building foundational infrastructure.

Current Retail Use Cases: Currently, the primary retail use case in the crypto space is speculative investment—individuals buying and holding cryptocurrencies, hoping their value will increase over time. However, Sam believes this will change as blockchain scalability solutions become more widespread.

Potential of Stablecoins: Tadeo points out that stablecoins already show promise as a retail use case. Stablecoins are digital assets designed to maintain stable value, making them suitable for daily transactions. They are seen as a superior alternative to traditional fiat currencies, especially for cross-border payments, primarily due to the inefficiencies of systems like SWIFT and the high fees associated with international fund transfers.

Challenges with Stablecoins: Despite their potential, the speakers note that challenges remain. They express hope for improvements to make stablecoins more practical and user-friendly for everyday transactions (e.g., buying coffee).

Both Sam and Tadeo agree that speculative investment and using stablecoins for cross-border payments are currently the two most prominent retail use cases, but there remains room for improvement and innovation in making crypto more accessible for daily transactions.

Closing Thoughts

When finally asked whether more engineers are now choosing to join Web3, Tadeo pointed to an interesting phenomenon—the correlation index between developer commits and Ethereum price. As the price rises and falls, so do commit counts (the recent drop over the past month might be due to holidays). Thus, as RWAs drive the next bull market, we can expect increasing numbers of developers to enter the industry and advance infrastructure development.

Source: https://cryptometheus.com/project/ETH

Note: Protocol Security

Sam acknowledges the inherent smart contract risks present in the DeFi space. However, they emphasize extensive precautions taken to minimize these risks. This includes undergoing multiple audits by independent auditors and conducting internal reviews to ensure deep understanding of the code. The goal is to provide the highest level of security for user funds and adhere to standard practices in smart contract development.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News