What interesting changes emerged in the 2023 fintech industry due to AI?

TechFlow Selected TechFlow Selected

What interesting changes emerged in the 2023 fintech industry due to AI?

The current fintech industry is a bit like oil drilling. As initial supply diminishes, the technology to extract resources from existing wells is no longer scarce.

Author: RockFlow

Key Takeaways

-

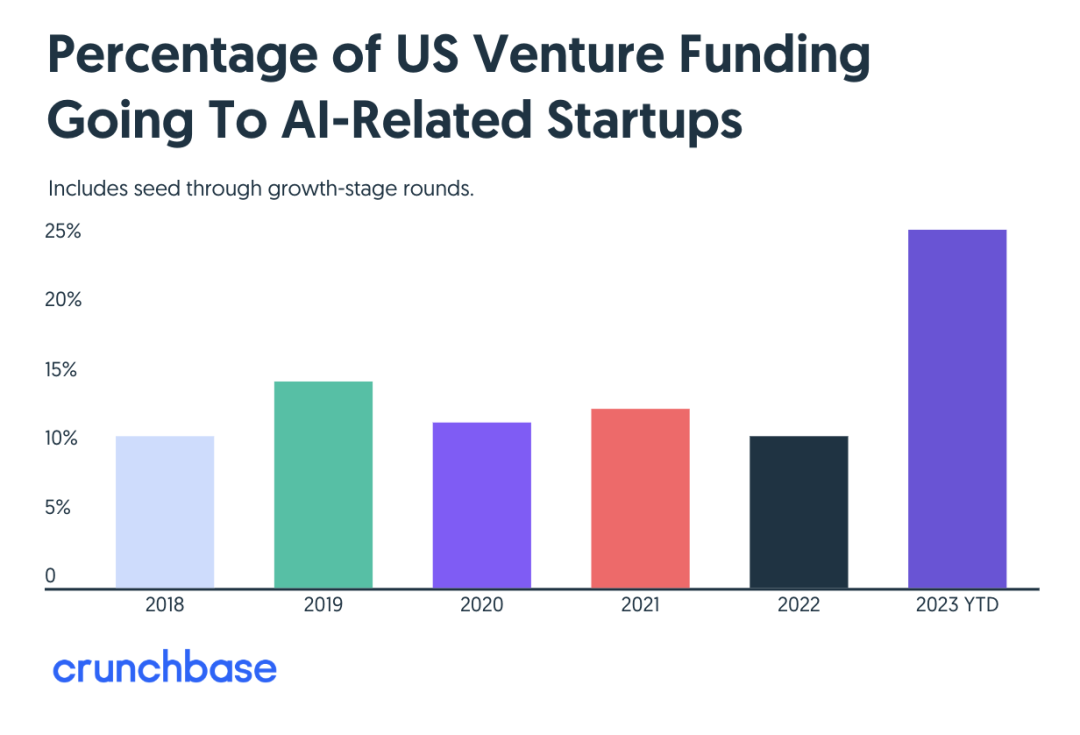

From 2018 to 2022, AI companies on average attracted 12% of venture capital, less than half of the 25% seen in 2023. While the early-stage investment pie has shrunk this year, AI's share remains significant.

-

Most leading AI products are built by startups. The "winner" is far from clear, and competition remains intense across most categories. Compared to the previous generation of products, AI product growth is healthy, with strong consumer willingness and ability to pay.

-

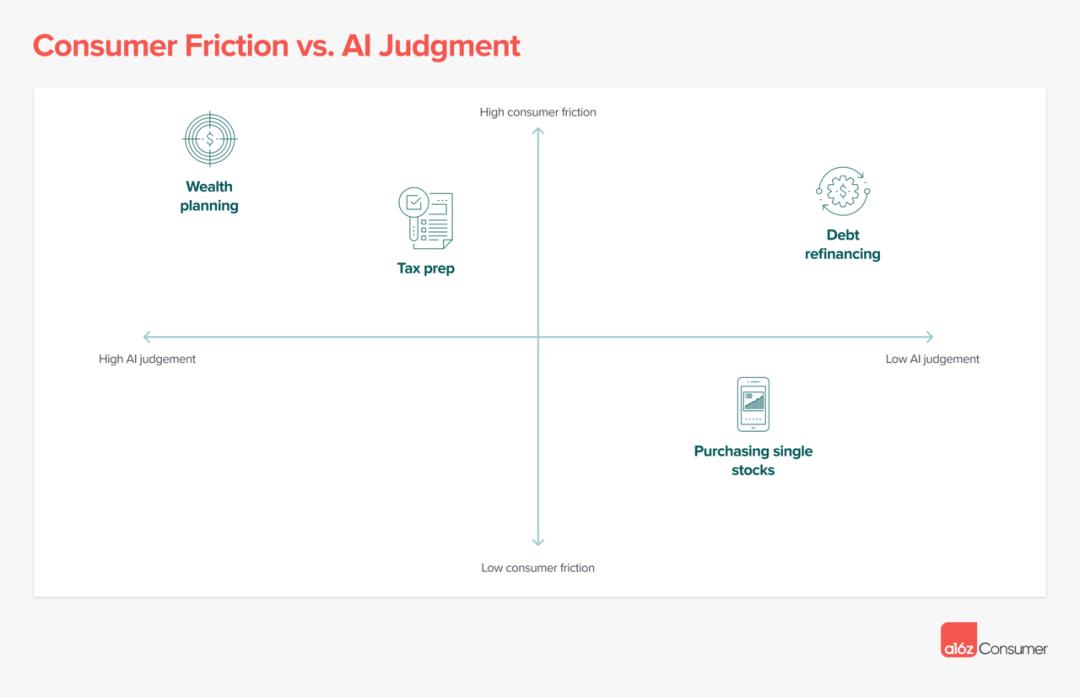

AI’s transformation of the internet will be gradual but decisive. It will first impact product categories with high user friction (painful to complete manually) and low judgment requirements (simple enough to automate).

-

Today’s fintech industry resembles oil drilling. As initial supply diminishes, technologies for extracting resources from existing wells are no longer scarce. With AI enhancement, financial products will see more changes, potentially enabling widespread, ultra-low-cost customization and personalization.

Crunchbase data shows that over a quarter of all U.S. startups receiving VC funding this year are AI companies.

At first glance, this isn’t shocking. AI has drawn more attention than ever, especially after top players in the field (OpenAI, Anthropic, etc.) secured massive funding rounds at the beginning of the year.

However, comparing 2023 to 2022 reveals a striking conclusion: AI’s appeal to VCs has more than doubled.

The chart below illustrates how venture capital attitudes toward AI have evolved over the past six years. From 2018 to 2022, AI companies averaged 12% of total venture capital inflows—less than half of 2023’s 25%.

What exactly happened in 2023 to cause this shift? A few key factors stand out.

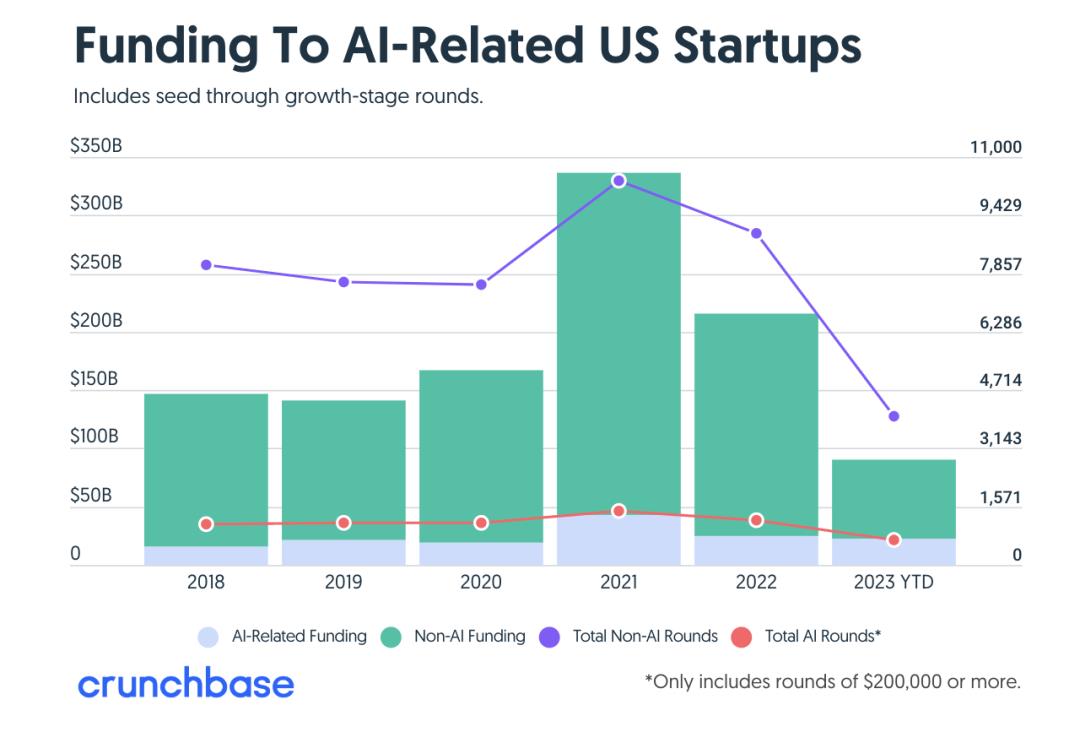

First, overall investment volume dropped sharply—the North American VC market declined by 50% year-on-year in the first half of 2023. Most sectors fell into a slump, with financing deals plummeting across the board (from real estate to fintech, Web3, and other niche segments).

Yet within this downturn, AI stood apart. This category remained highly favored, with deal counts rising annually. In other words, while the early-stage investment pie shrank, AI’s slice grew larger.

Another interesting aspect of AI’s popularity in early-stage investing is that it is not confined to one specific industry—AI technology can be applied across verticals: AI+real estate, AI+fintech, AI+biotech, and so on.

In some ways, today’s AI funding boom echoes 25 years ago, when startups would proudly label themselves “internet companies.” But now, no one emphasizes that distinction because the internet is assumed to underpin nearly every startup’s business model.

Similarly, AI is trending away from being a standalone category—not because it’s unimportant, but because it’s too important to be limited to one category.

1. Current State of AI Products: New Categories Emerge, Market Still Wide Open

It’s been a year since ChatGPT launched, reaching 100 million monthly active users in just two months and ushering in a new era for AI-powered products.

But beyond ChatGPT, what does the competitive landscape look like among old and new AI products? Who might become the next big winner? A16Z conducted a detailed traffic-based analysis of the top 50 GenAI web products and reached the following conclusions:

First, most leading AI products are built by new startups.

Like ChatGPT, most popular AI products today didn’t exist a year ago. This suggests that while many tech giants are enhancing their offerings with AI, the most compelling experiences are often entirely new.

Among the top 50 listed products, only five belong to or were acquired by major tech incumbents: Bard (Google), Poe (Quora), QuillBot (Course Hero), Pixlr (123RF), and Clipchamp (Microsoft).

The listed products fall into three categories: 1) training proprietary models, 2) fine-tuning existing models, and 3) building novel experiences atop existing models. Among the top 10, half have proprietary models, and four are fine-tuned versions.

Excluding OpenAI (a $11.3 billion outlier), companies with proprietary models raised an average of $98 million. In contrast, those fine-tuning open-source models raised $20 million on average, while the third group raised just $9 million.

Second, the “winner” is far from decided—competition remains fierce in most categories.

This is undoubtedly good news for small and mid-sized companies: despite surging interest in AI products, there is still no clear leader in many categories.

Looking at traffic differences between the top two players in each subcategory, the gap is less than 2x for most—indicating markets are far from consolidated. Given that these AI products have grown at an average monthly rate exceeding 50% over the past six months, early-mover advantages are fragile.

Third, AI product growth is robust—consumers show strong willingness and ability to pay.

Over the past five years, due to the absence of major platform-level opportunities (e.g., PC internet → mobile internet), general interest in new products has waned. As homogenized competition intensified, customer acquisition costs rose while customer lifetime value became questionable.

AI has changed the game. Leading AI products are currently capturing large volumes of free traffic, and consumers have proven willing to pay. Most AI products are achieving positive unit economics through subscriptions, with an average revenue of $21/month—far exceeding annual fees of recently popular internet products like Calm, Headspace, and Duolingo ($70/year). By unlocking new value, AI products have elevated consumer payment willingness.

2. In Fintech, Who Needs AI Most?

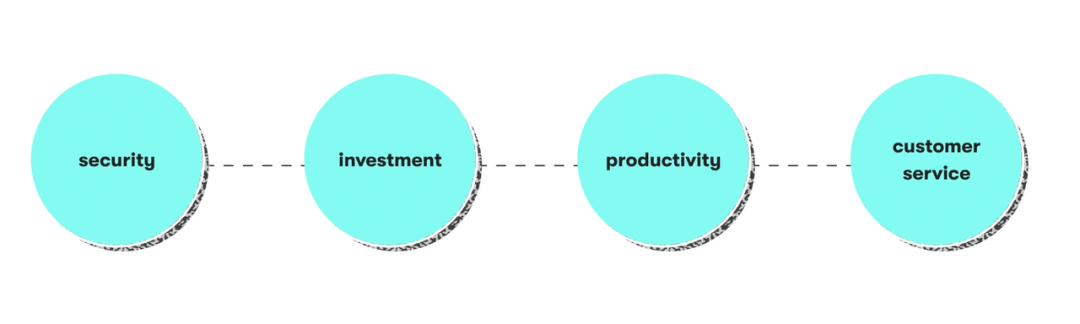

AI’s characteristics are rapidly spreading across industries, with fintech being particularly noteworthy. Even during the earlier wave of AI technologies (like machine learning), fintech firms sensed opportunity and began driving industry transformation. At least in four areas, AI-enhanced fintech companies now have new possibilities:

Security: For example, banks lose tens or even hundreds of billions annually to fraud. With AI, fintech companies can better detect suspicious activity and improve cybersecurity.

Investment: According to PwC’s “2023 Asset and Wealth Management Revolution Survey,” global assets under management reached $115.1 trillion in 2022. Over 90% of asset managers have adopted AI, and assets managed by robo-advisors are expected to grow 136% from $2.5 trillion in 2022 to $5.9 trillion by 2027. Betterment and Wealthfront lead in this space.

Productivity applications: AI-powered tools can enhance data processing or take over clerical tasks (e.g., invoicing), with broad applicability.

Customer service: AI-driven chatbots can assist customers while significantly reducing enterprise costs.

In short, in finance, AI can improve decision quality, optimize user experience, and save money.

According to A16Z, AI’s transformation of internet products will be incremental yet resolute. It will first target product categories with high user friction (painful to do manually) and low judgment requirements (simple enough to automate). The former means consumers are more motivated to try new products, while the latter ensures a better user experience.

3. New Changes AI Brings to Fintech

The once-booming fintech industry took a sharp downturn in spring 2022. As interest rates rose, the seemingly endless supply of capital dried up, leaving many survivors struggling ever since.

Fortunately, after a period of gloom, sentiment in the fintech sector is improving. A new normal is emerging. High-quality fintech companies are raising funds again, and some early-stage startups are regaining VC favor.

Of course, not all companies can secure funding. VCs are now seeking fintech startups that meet key criteria: solid unit economics, clear business models, clear product-market fit, sufficiently large addressable markets, and strong founding teams.

Ten—or even five—years ago, many fintech opportunities were seized by both established players and newcomers:

David Velez founded Nubank possibly inspired by early Jeff Bezos (what’s Brazil’s biggest industry? Banking. What matters most in that industry? Profitability?—similar to Bezos’ original reasoning for Amazon selling books);

Affirm’s Levchin deeply focused on customer pain points (he understood the downsides of credit cards for consumers);

And we’ve seen success stories from infrastructure providers like Stripe and corporate spending redesigners like Ramp.

Some believe the fintech innovation wave is entering its second half—for example, the U.S. may never see another Robinhood. Yet if bold startups propose fresh ideas targeting seemingly entrenched traditional financial services, or focus on new demographics and channels, could new giants still emerge? The outcome remains uncertain.

After all, history repeatedly shows that even in eras unfavorable to rapid growth, new brands and small companies can rise. Though admittedly, they face a tougher game.

Not to mention, numerous niche and emerging markets remain globally underserved. Take India, Latin America, and Southeast Asia—these

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News