Will DeFi be taxed? The IRS holds hearing

TechFlow Selected TechFlow Selected

Will DeFi be taxed? The IRS holds hearing

Expanding the tax scope to non-custodial wallets will also place significant pressure on the market.

Author: Matthew Lee, OKLink Research Institute

On November 15, the U.S. Internal Revenue Service (IRS) held a highly anticipated hearing on expanding the tax scope for cryptocurrency assets. The hearing covered numerous key issues, including user privacy, the range of crypto entities required to report transaction information, inclusion of stablecoins, application of proposed regulations to participants in decentralized finance (DeFi), and wallet address reporting.

The rapid development of DeFi has made it a focal point for regulators. According to Barclays Research, the cryptocurrency tax gap is at least $50 billion. This initiative faces challenges due to ambiguous definitions of DeFi projects, lack of taxation history, no prior experience with on-chain transactions, and other entities masquerading as DeFi platforms—making regulation more difficult. Therefore, the IRS aims to include these within its regulatory framework to ensure tax transparency and completeness.

The central topic of the hearing was the definition of “broker”. Under proposed regulations issued in August, the definition of broker could be expanded to include “digital intermediaries who directly or indirectly facilitate sales of digital assets.” This broader definition would bring DeFi protocols, non-custodial wallets, and wallet developers under the broker category. Brokers would then be required to report:

-

Taxpayer’s name, address, and taxpayer identification number;

-

Name, type, quantity, date, and time of the sold digital asset;

-

Total proceeds received by the seller from the sale (including exchange and on-chain earnings);

-

Total fees paid to the broker for the transaction;

-

Wallet address from which the seller transferred the digital asset;

-

On-chain transactions related to the sale or deposit into an account, along with associated transaction identifiers or hashes.

In simple terms, the IRS would require code-operated decentralized projects like Uniswap, SushiSwap, and MetaMask to perform KYC on all users, track transactions occurring both on exchanges and on-chain, monitor wallet addresses, and have full visibility into users’ on-chain transaction activity and revenue.

Although this hearing has drawn public criticism, several market issues justify the expansion of tax oversight: 1. Significant growth in trading volume on decentralized exchanges; 2. Inability to trace fund transfers through non-custodial wallets; 3. Increase in illicit activities due to private wallets lacking third-party reporting. As a result, many experts believe that expanding the tax net is inevitable, with the formal legislation expected around 2025.

What Impact Will Expanding Tax Scope Bring?

Users

Beyond reduced income, users will face complex data processing and administrative burdens. Provisions in the 2021 U.S. Infrastructure Investment and Jobs Act already directed the IRS to implement new rules for crypto brokers. If the tax scope expands, digital brokers must report cost basis—the original value of an asset for tax purposes. However, the complexity of cost basis introduces additional challenges for brokers, taxpayers, and the IRS. Taxpayers have two methods to calculate cost basis:

-

First In, First Out (FIFO, default): If you bought Bitcoin at $1,000 and $2,000, then sold when the price reached $4,000, FIFO assumes you sold the Bitcoin purchased at $1,000 first;

-

Specific Identification: This method allows taxpayers to choose which units of digital assets they are selling, enabling strategic minimization of tax liability—but requires clear identification and tracking of each transaction.

Under specific identification, taxpayers must dig deep—not only into exchange records but also years-old on-chain transaction histories—and mark specific Bitcoins within their inventory intended for sale, even if delegating to a broker, since the specific asset being sold must still be identified on-chain or via exchange history.

While FIFO is simpler, it may lead to higher taxes because U.S. tax rates differentiate between short-term and long-term holdings. Short-term gains (held less than one year) are taxed at progressive ordinary income rates, up to 37%, while long-term gains (held over one year) are capped at 20% even for the highest earners.

The IRS acknowledges that collecting crypto taxes will generate massive paperwork—potentially increasing the number of 1099-DA forms from 13–16 million taxpayers to 8 billion due to vast on-chain data. Currently, brokers lack the capability to identify specific transactions, so users must rely on self-education in basic tax principles and use on-chain data tools to track and record digital asset trades, transfers, and holdings for accurate tax filing.

Industry

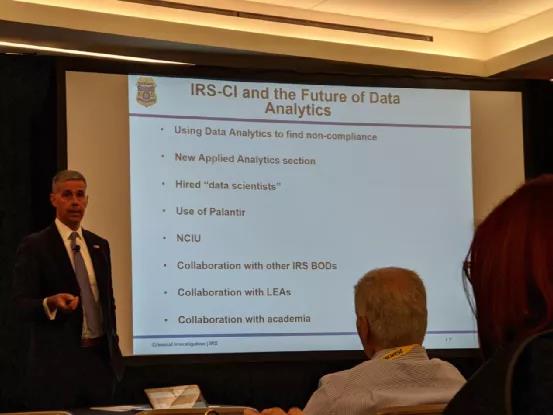

Taxation requires complete transaction records to compute cost basis, capital gains, and fair market value. However, tracking asset movements across exchanges, wallets, and decentralized protocols is extremely complex. The IRS cannot easily generate tax reports directly. Industry estimates suggest over millions of crypto investors file inaccurate tax returns.

IRS discloses cryptocurrency tax investigation methodology; Source: Cointracker

In the future, businesses and tax authorities may build smarter automated tax-filing systems—similar to TurboTax or H&R Block—based on on-chain and centralized data. These systems would integrate records such as purchases, sales, airdrops, forks, minting, swaps, and gifts. However, such mechanisms would expose large amounts of personal data and undermine the industry’s ideal of “decentralization.”

Public Backlash

Tens of thousands submitted objections to the hearing. Most argue that excessive regulation would infringe on personal privacy and individual freedom. These concerns reflect broader public anxiety about government overreach, emphasizing that regulation should maintain social order without compromising fundamental rights. Congress previously attempted to define intermediaries to include “any decentralized exchange or peer-to-peer marketplace,” but the proposal was ultimately rejected. Now, the IRS has reused language similar to that of intermediaries to reinterpret the definition of “broker,” going beyond statutory limits, leading the public to question whether this action potentially violates administrative law.

In the author’s view, taxing DeFi is impractical. Over 95% of projects in the market do not generate positive cash flow and remain in very early, fragile stages. Taxation would impose additional burdens on DeFi projects. Expanding the tax scope to non-custodial wallets would also place immense pressure on the market. After Biden increased capital gains taxes on the wealthy in 2021, Bitcoin experienced a sharp decline. If a new tax regime extends to on-chain assets, more users may engage in tax-loss harvesting, selling profitable positions before formal tax collection to reduce liabilities.

There remains a long road ahead for effective crypto taxation, involving multiple government agencies and unresolved ambiguities—such as whether stablecoin transactions must be reported and how non-financial assets should be classified. Coinbase’s tax vice president stated during the hearing, “Requiring tax reporting for transactions with no gain or loss (including stablecoins) would result in a high volume of low-value reports.” A senior advisor from the Blockchain Association also noted: “The proposal is overly broad, forcing decentralized projects to choose between: 1. Abandoning decentralized technology; or 2. Leaving the United States.”

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News