Analyzing Decentralized Gambling Tools: A Risk Study of the f(x) Project

TechFlow Selected TechFlow Selected

Analyzing Decentralized Gambling Tools: A Risk Study of the f(x) Project

f(x) splits the underlying asset stETH into a certain number of stablecoin-like products fETH and a high-volatility, high-return leveraged product xETH.

Preface

The four-year cycle of the cryptocurrency market is truly fascinating. Each time, we feel like it's different this time — yet the outcome remains the same: "It’s still just like before!" I've never liked predicting markets, buying altcoins, or leveraged trading, but even so, I still get caught in every bear market cycle. The reason? As long as there's a trace of greed inside you, even if you don't want to participate, you can't help but act — and fall into similar traps. Just like crowdfunding for altcoin projects back in 2013, ICOs in 2017, DeFi Summer in 2020, and especially the two major crashes in 2021 where I had to proactively liquidate my CDPs to survive.

In my view, the right way to break free from this endless loop in crypto and achieve steady wealth growth is by using technical mechanisms to cage our own greed within predefined DeFi rules. The idea that a financial protocol can operate autonomously through pure mathematical logic and code implementation is truly beautiful. @aladdindao’s series of products follow exactly this philosophy. Readers interested may refer to my previous articles:

https://mirror.xyz/darkforest.eth/gQuWj8-HKOxmCPKdx9etmCPGSylXWmXSVjRm-C_G2wE

As the fourth product launched by @aladdindao — f(x) — it introduces an entirely new offering to Ethereum’s DeFi ecosystem through several simple mathematical equations, creating a structured financial product similar to tranches in traditional finance. It splits the underlying asset stETH into a certain amount of stablecoin-like fETH and a high-volatility, high-yield leveraged asset xETH.

These two assets built on Ethereum’s native infrastructure correspond to two simultaneous market demands: hedging demand and leverage demand.

1. Leverage Demand Scenario

Suppose we are now at the transition point from bear to bull market, meaning that core assets like Ethereum have a relatively high probability of significant appreciation over the coming years. For HODLers, all they need is patience — simply waiting will suffice. But for leveraged traders, if I believe such upside is likely, why not go big and add some leverage to bet on the future?

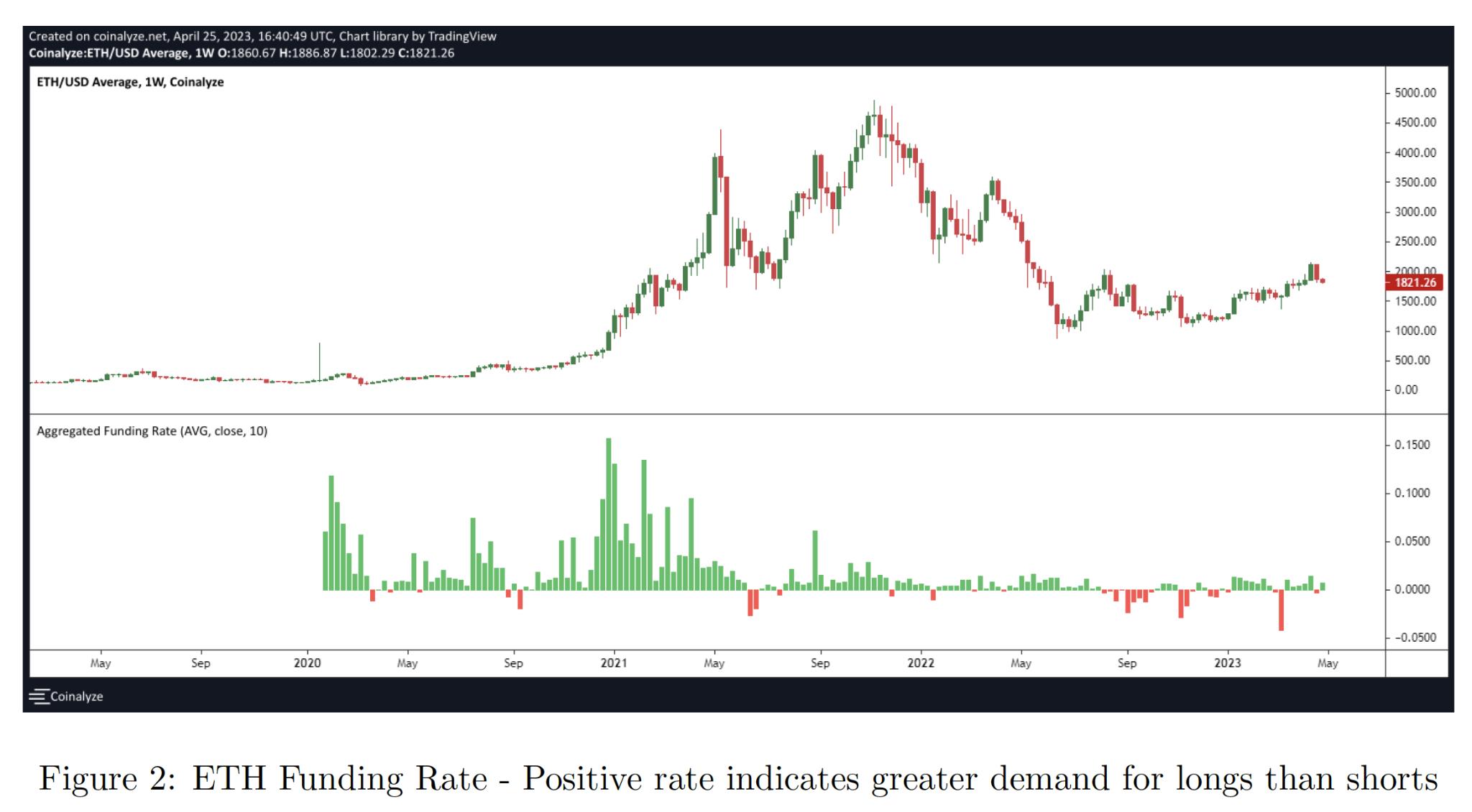

However, we all know that during major bull runs, sharp short-term drawdowns frequently occur. The fatal flaw for leveraged players is failing to endure the darkness before dawn — not surviving until sunrise. Moreover, perpetual contracts on centralized exchanges typically charge positive funding rates most of the time, which means your gains must overcome these continuous costs — an uncertain challenge.

But what if there existed a product allowing you to maintain leverage while avoiding the constant risk of sudden liquidation — and better yet, with zero or even negative funding rates and very low holding costs? Wouldn’t many HODLers then be tempted to add just a bit of leverage to amplify their returns?

2. Hedging Demand Scenario

On the other hand, suppose we're in the midst of a raging bull market, with prices climbing rapidly. You clearly have a hedging need but are reluctant to switch fully into stablecoins and completely forfeit future upside. Besides, haven't all stablecoins faced their own share of FUD (fear, uncertainty, doubt)? What you actually need at this moment is precisely something like fETH — a native Ethereum-based asset free from external RWA ("Real World Assets") risks — to reduce the overall volatility of your portfolio.

https://mirror.xyz/darkforest.eth/7O4rGUDHCMwA45m33zUYYwnjw3jl1rps8mgxRCcgZbY

Imagine Ethereum drops 90% after you mint fETH (a terrifying thought), yet your fETH only loses 9%. You’ve successfully weathered a super bear market — a perfect “top exit” strategy without giving up on the last penny of potential gain.

This idea excites me, especially considering that in crypto, native assets are inherently much safer than various mined LP tokens wrapped in complex yield schemes. Yet, having endured countless setbacks, I know no protocol offers benefits without trade-offs. To make real financial decisions, I need a complete understanding of its risks.

The Three Fundamental Questions About f(x) Protocol

How does the f(x) protocol achieve volatility tiering? How stable is the system under extreme market conditions? And where lies the breaking point of the system?

1. Principle of Volatility Tiering

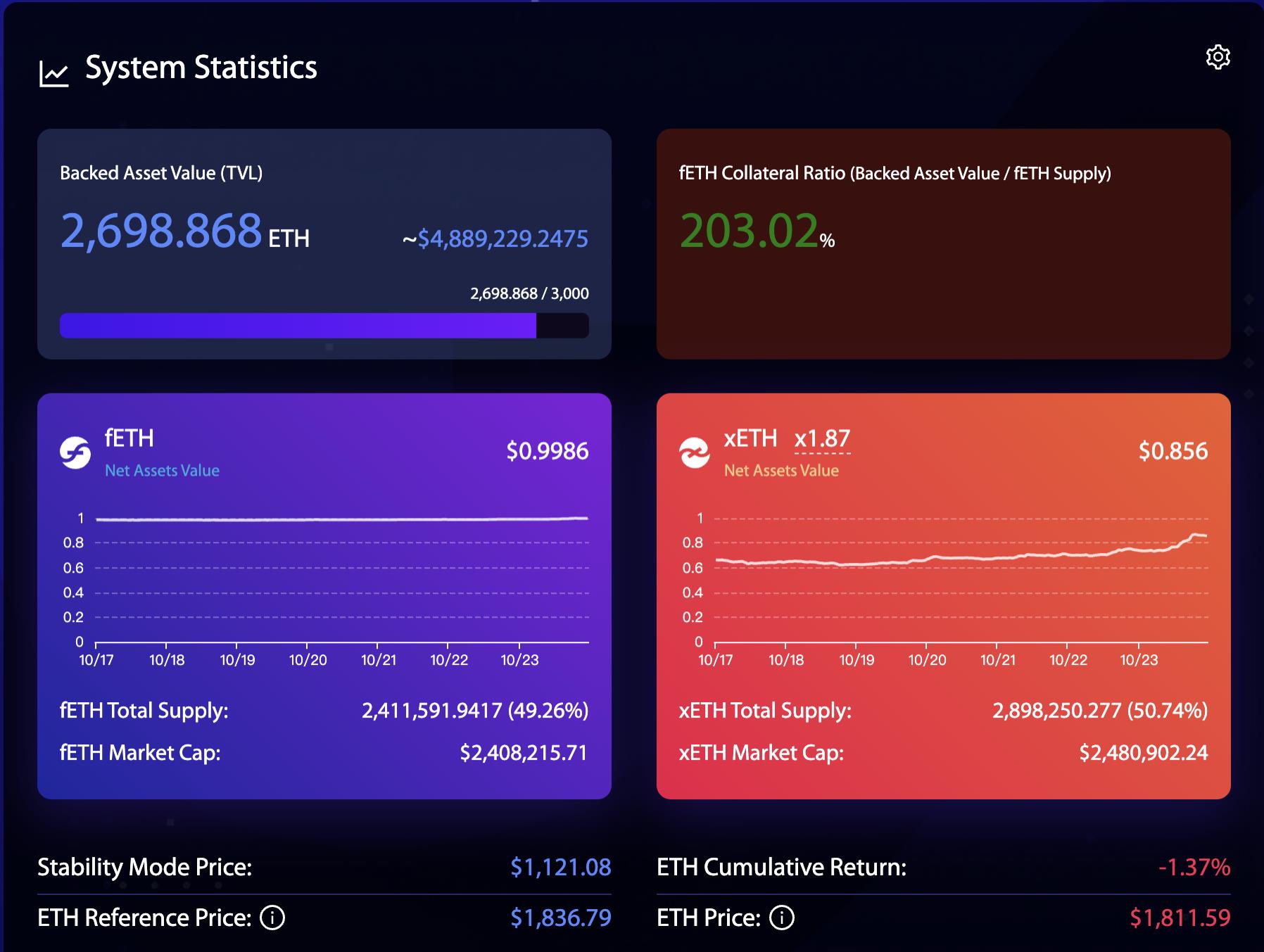

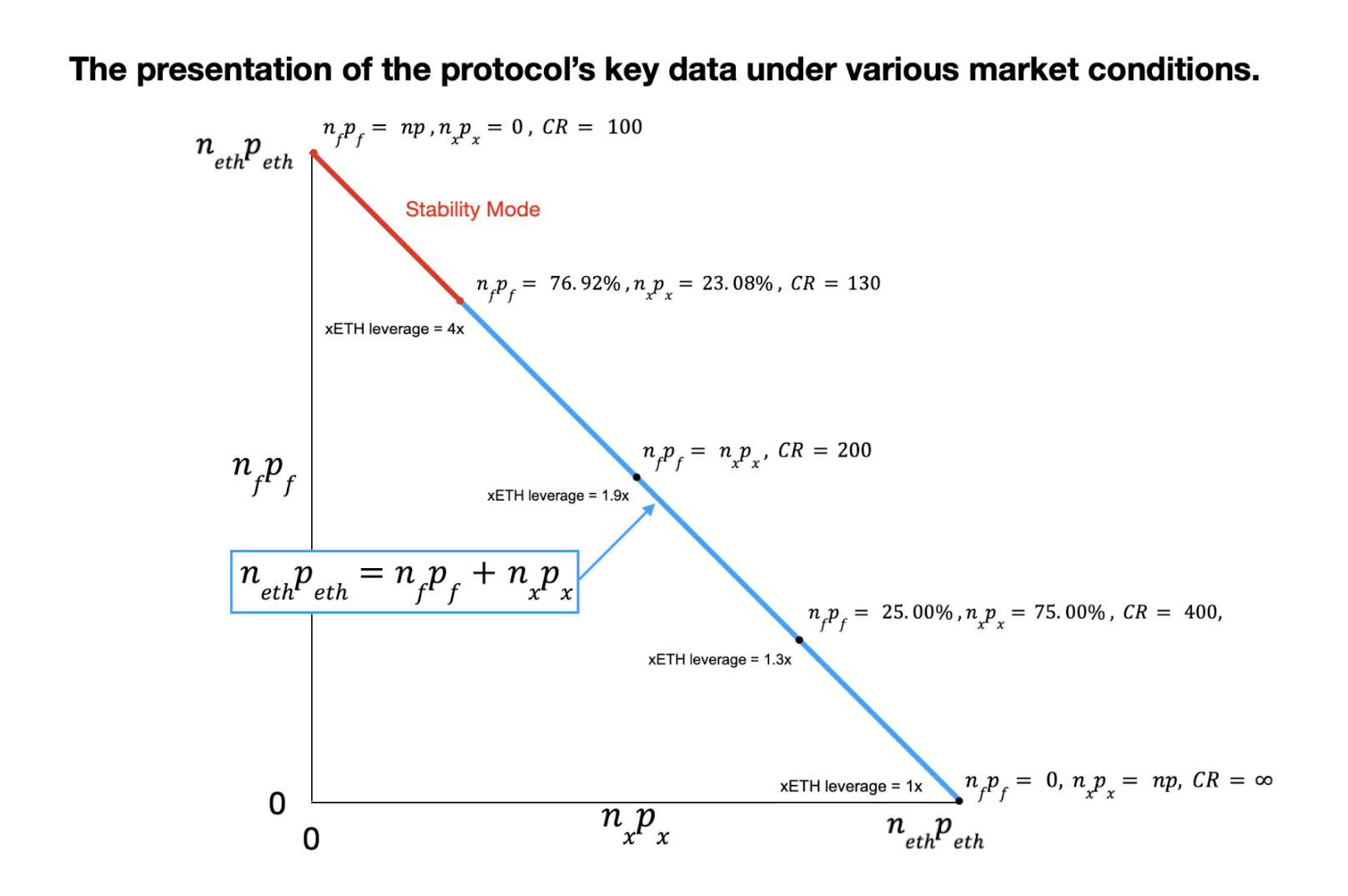

To understand the f(x) protocol, grasping the dashboard below is crucial. The base asset ETH becomes stETH via Lido staking, then gets split into a fixed quantity of stablecoin-like fETH and leveraged xETH. fETH has only 10% of the volatility of the underlying asset, while xETH absorbs all remaining volatility.

The entire brilliance of the protocol lies in the following simple formula:

We observe that the protocol’s underlying asset is 2698.868 ETH, with a TVL of $4,889,229 — equal to the sum of the NAVs (net asset values) of the two derived assets: fETH market cap + xETH market cap. The price of fETH is pegged to 10% of Ethereum’s price volatility, so the fETH price pf is determined. With nf and nx being fixed quantities, px can thus be calculated.

Let’s illustrate with an example:

An initial user deposits 1 ETH worth $2000, minting 1000 fETH and 1000 xETH. The next day, ETH drops 10%, falling to $1800. According to protocol design, fETH can only drop 1%, so its price becomes $0.99. Using Formula 1, we calculate that xETH’s price falls to $0.81. What is xETH’s volatility? (1–0.81)*100% = 19%, equivalent to 1.9x leverage.

From the volatility curves shown on the dashboard, we can clearly see that fETH exhibits minimal fluctuation, while xETH’s volatility exceeds that of ETH itself. The project could improve UI clarity here.

2. How Is System Stability Guaranteed?

f(x) Stability First Law: The volatility of the quasi-stablecoin fETH remains precisely locked at 10% of ETH’s volatility.

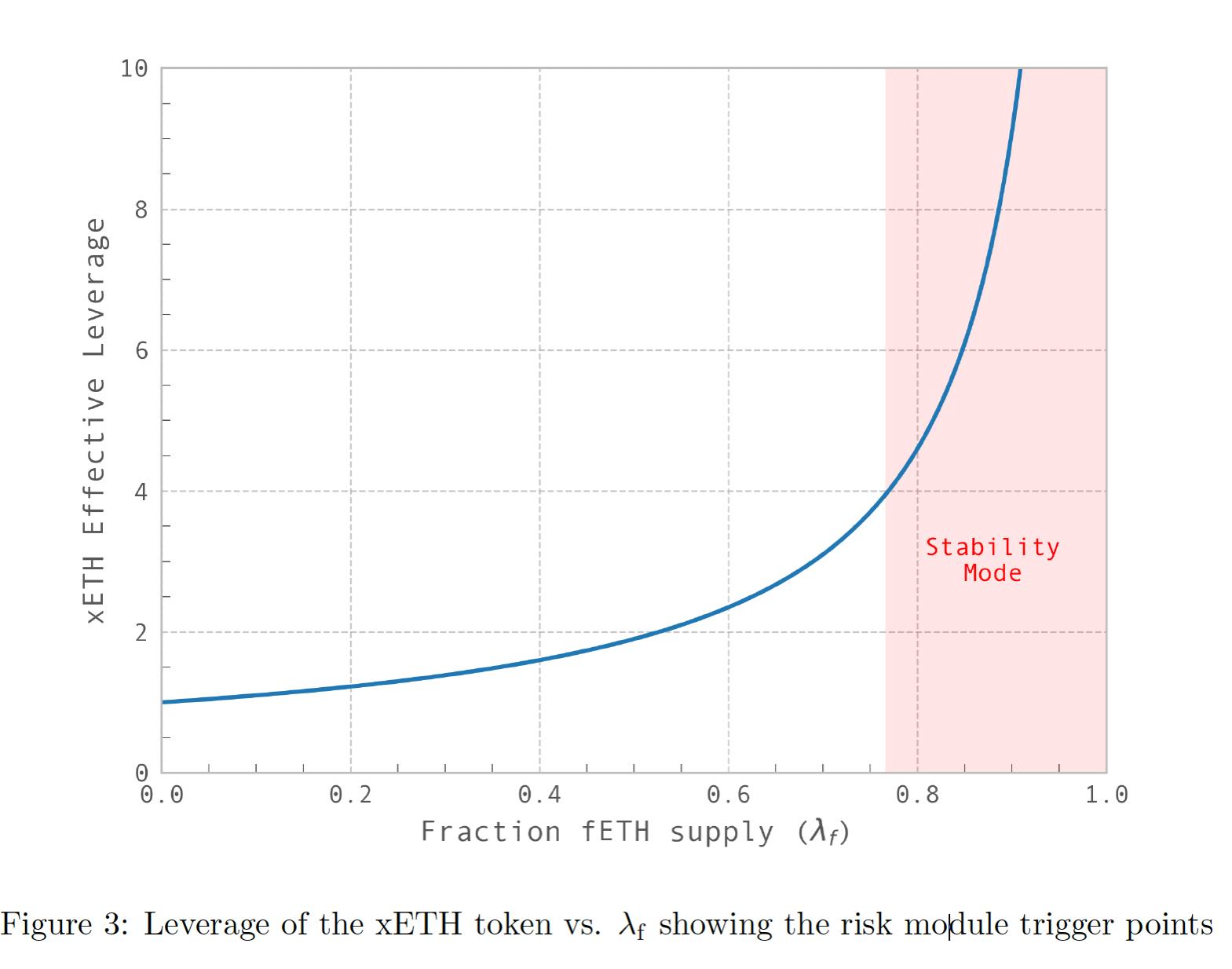

First corollary: To satisfy the first law, sufficient xETH must exist to absorb excess volatility beyond fETH’s 10% cap. If xETH supply is relatively small, leverage increases (see red area on right side of chart); if xETH supply is large, leverage decreases (left side), enabling lower leverage to dilute volatility.

These two simple principles form the foundational conditions of the f(x) protocol. However, this curve does not represent a self-correcting financial system. We must pay close attention to the extreme cases on both ends of the curve.

(1) Left end of the curve: xETH significantly outweighs fETH. This scenario is more common during bull markets, when more users prefer leveraged products over stablecoins. In extreme cases, xETH leverage approaches 1x — nearly identical to holding native ETH. Even so, the protocol remains unharmed, and the system naturally regresses toward the center of the curve.

The f(x) whitepaper notes that although fETH demand determines fETH supply, the maximum mintable fETH is usually much higher (limited only by xETH supply).

Here, the protocol has room for AMO (Algorithmic Market Operations)-like actions similar to Frax. For instance, if excessive xETH growth causes leverage to fall too low, reducing market appeal, f(x) could proactively mint additional fETH to keep leverage above, say, 1.5x. Later, if xETH demand declines, the protocol can burn the excess fETH to prevent leverage from spiking again.

(2) Right end of the curve: xETH supply is too low relative to fETH. This situation poses significant danger to the system and must be guarded against — typically occurring during periods of extreme market pessimism, when prices keep falling and everyone seeks safety, leaving few willing to take on leveraged long positions. On the chart, we observe a sharp spike in xETH leverage, potentially triggering a deadly negative death spiral: fewer people willing to go long → higher leverage → even less willingness to leverage → and so on...

In such scenarios, free markets cannot self-correct. Fortunately, the f(x) protocol employs specific measures to prevent such tragedies.

3. Risk Boundaries of the f(x) Protocol

The f(x) protocol adopts the concept of CR (Collateral Ratio) from CDP lending protocols. From the protocol’s perspective, the underlying assets deposited are collateral, and the minted fETH stablecoin is the loaned asset. The protocol must ensure that the value of issued fETH never exceeds the value of the collateral — i.e., CR > 100%. Otherwise, bad debt arises, leading to insolvency. xETH value is excluded because, in extreme cases, xETH could go to zero; nevertheless, the protocol must continue functioning without defaulting.

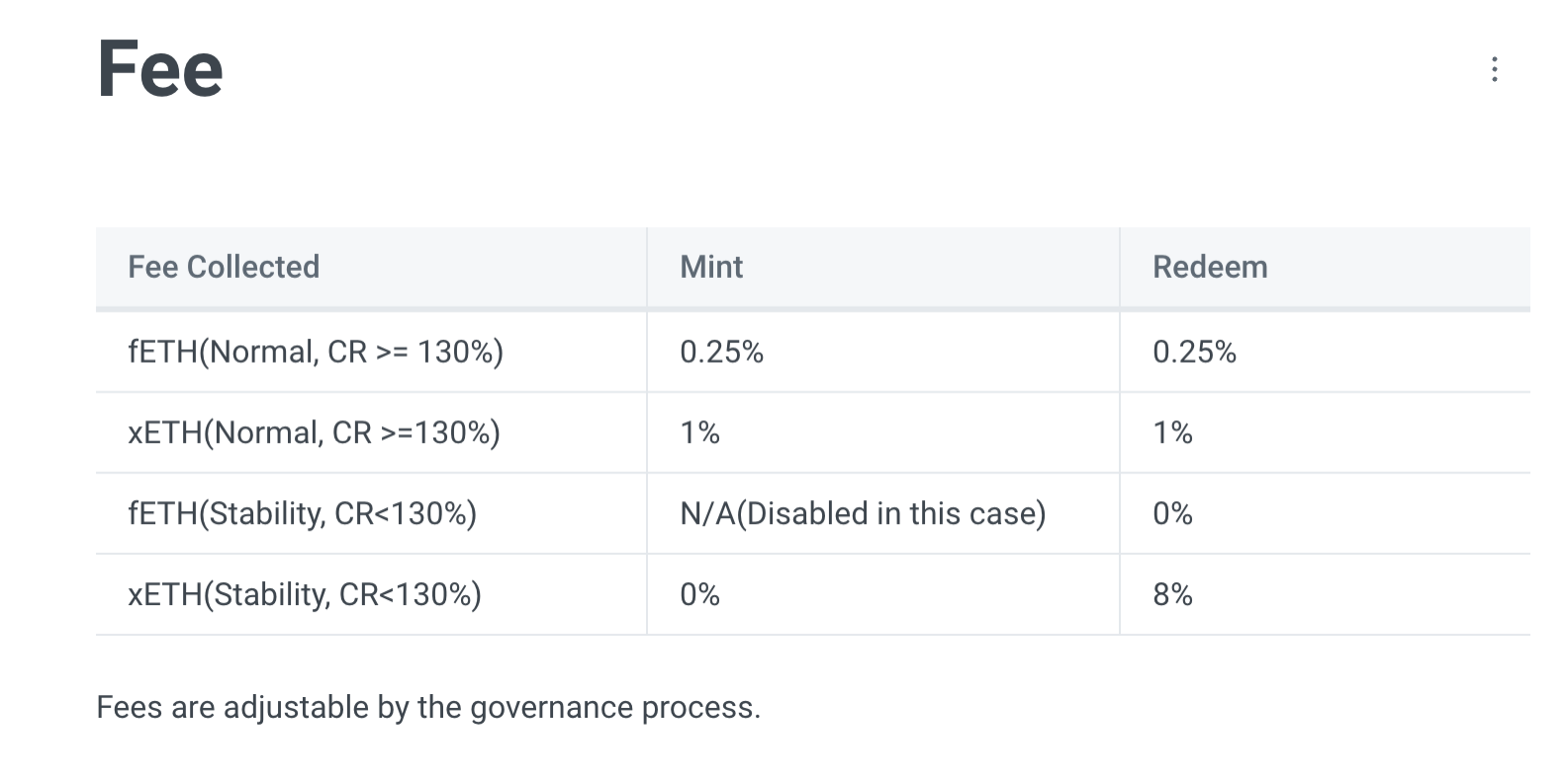

Using daily Ethereum price data since January 1, 2017, the protocol estimates that under a 0.1% or lower risk threshold — equivalent to a one-day 25% crash in ETH — a 130% CR is sufficient to withstand the shock. Thus, 130% CR is set as the safety threshold. Once CR drops below this level, the protocol automatically enters "Stability Mode." At this point, fETH’s value exceeds 0.78× the underlying asset value, and xETH leverage reaches exactly 4x. In Stability Mode, the following measures are implemented:

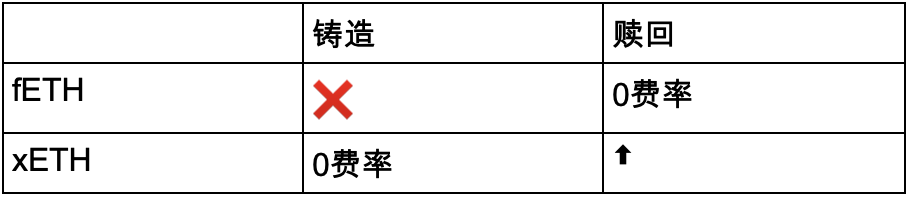

(1) Control Over Protocol Entry/Exit Points

The f(x) protocol adjusts minting and redemption fees for fETH and xETH, or even halts fETH minting altogether, aiming to increase xETH’s relative value and enhance the protocol’s ability to absorb underlying asset volatility.

(2) Internal Asset Rebalancing — Rebalancing Pool

Similar to Liquity’s Stability Pool, the protocol incentivizes fETH holders to deposit their tokens into a dedicated pool to earn staking rewards. The protocol retains the right to use these funds to redeem fETH for reserve assets (i.e., stETH) when CR falls below the safety threshold.

Risk-averse fETH holders can reduce volatility exposure while increasing yield via the Rebalancing Pool. Through incentives, the protocol temporarily aggregates fETH liquidity (recently changed from two-week lockup to one-day lockup), effectively adjusting CR away from dangerous levels.

If assets in the Rebalancing Pool are exhausted and CR continues to decline, the f(x) team will use protocol revenue to incentivize xETH minters.

Unlike Liquity, where rewards come from native token emissions causing long-term selling pressure on $LQTY, rebalancing pool providers in f(x) earn yield externally — specifically from Lido’s Ethereum staking rewards. This reflects the cost of relying solely on native ETH as collateral.

In my opinion, f(x) could borrow from Liquity’s approach: once CR drops below 130%, offer redemption bonuses akin to liquidation rewards to encourage more fETH into the Rebalancing Pool.

This differs from LUSD, whose primary function is circulation. fETH’s main purpose is hedging during ownership — it doesn’t require large-scale circulation.

(3) Treasury Subsidies for xETH Minters

While the Rebalancing Pool raises CR by reducing TVL, subsidizing xETH minters increases CR by expanding TVL — a more constructive approach. The actual effectiveness and scale of such subsidies remain to be tested in practice.

User Decision-Making Under Extreme Market Conditions

Risk-Averse Users

For fETH holders who deposit into the Rebalancing Pool, monitoring whether CR might fall below 130% is essential. If signs appear, timely withdrawal is advised. The recent update reduces lock-up to just one day — highly user-friendly. However, mass withdrawals could severely impact protocol security.

For truly conservative users, holding fETH directly is safest, avoiding potential forced redemptions. But even at the protocol’s boundary — CR = 100% — fETH volatility equals ETH volatility. This isn’t unbearable; by then, after an epic crash, the worst drawdown has likely already passed.

Leverage Traders

For leveraged traders, low leverage means losing excitement — not critical, but concerning when CR drops below 130%, causing leverage to spike. This usually coincides with severe market downturns, leading to massive losses accelerating by the day. Redeeming incurs an 8% fee, and near CR = 100%, xETH approaches zero value.

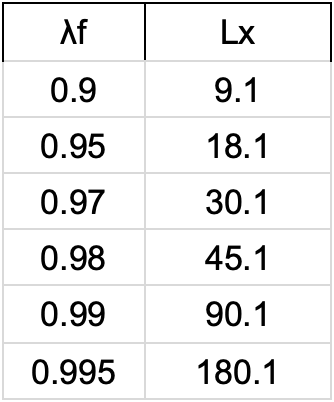

But here’s my analysis: during sharp declines, fETH and xETH holders aren’t static — a dynamic equilibrium exists. As CR nears 100%, holding fETH loses meaning due to added contract risk, prompting some users to redeem ETH and hold it at lower prices. Meanwhile, xETH leverage could surge to 20x, even 100x. At that point, the risk-reward ratio overwhelmingly favors leveraged players — even tiny investments could yield 100x returns. Would no one step in? I find that hard to believe. This inevitably drives CR upward, restoring system stability.

Using the f(x) leverage formula, we can compute a table showing leverage at various fETH proportions of total assets.

Therefore, CR won’t truly reach 100%, because leverage cannot become infinite — 100% CR is merely a mathematical limit. In this sense, the system possesses inherent self-stabilizing properties. Of course, this is purely theoretical; real market behavior and protocol performance under stress may differ.

Another external risk must not be ignored: issues with Lido or other factors causing stETH depegging. If stETH deviates more than 1% from ETH, minting is temporarily suspended. Redemptions continue normally, but fETH redemptions use the higher of the two prices (stETH or ETH), while xETH uses the lower. This protects fETH holders’ interests.

Conclusion

After thorough analysis, the official claim — “xETH is the first ever levered ETH you can HODL” — appears genuinely valid. The current ETH price triggering Stability Mode is $1078, while the protocol’s CR stands at 207%, indicating substantial safety margin.

To me, the greatest significance of the f(x) protocol lies in providing decentralized financial tools for users with varying risk appetites. It enables users to completely avoid centralized exchanges, eliminate real-world asset risks, and rely solely on native crypto assets to execute strategies — truly becoming masters of their own wealth. This aligns perfectly with Satoshi’s vision and represents the deepest purpose and value of DeFi.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News