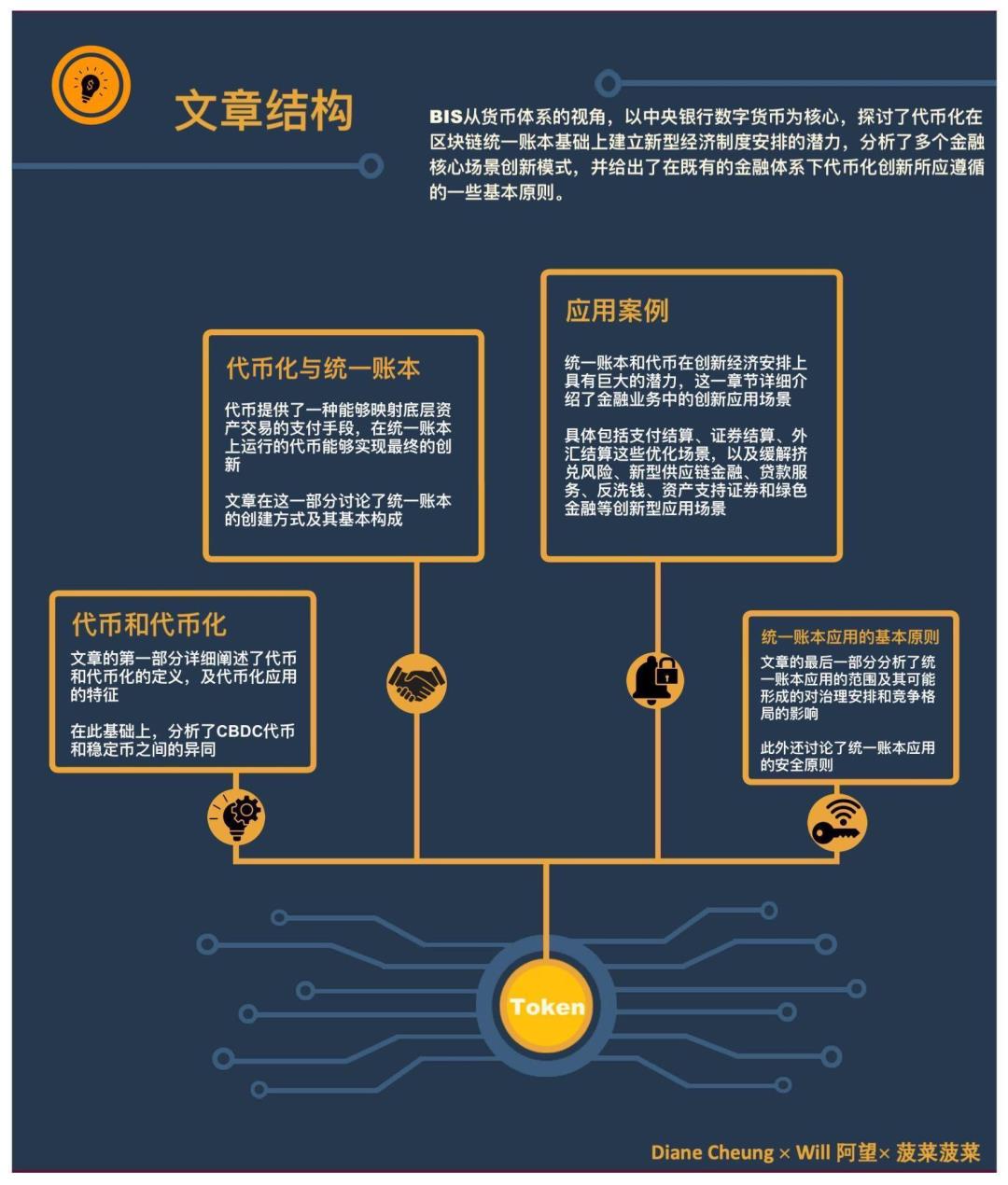

Tokenization and Unified Ledger: Building the Blueprint for the Future Monetary System

TechFlow Selected TechFlow Selected

Tokenization and Unified Ledger: Building the Blueprint for the Future Monetary System

This article outlines a blueprint for a future monetary system that leverages the transformative potential of tokenization to improve existing structures and unlock new possibilities.

Authors: Diane Cheung, Will Awang, Bobo Bobo

Today, the global monetary system stands on the brink of a historic leap forward. After digitization, tokenization—the digital representation of asset ownership on programmable platforms—is the key step toward this transformation. Tokenization enhances the capabilities of money and financial systems by transforming how intermediaries serve users and eliminating barriers in information transmission, reconciliation, and settlement. It will enable new forms of economic activity that are currently unattainable within traditional monetary frameworks.

Cryptocurrencies or decentralized finance (DeFi)—such as the recent trend of DeFi aggressively absorbing real-world assets (RWA)—have only revealed one facet of tokenization. These approaches remain limited, not only because of their weak integration with the real world but also due to the lack of central bank-backed trust in their monetary value—even so-called stablecoins often prove unstable.

In our previous translation of the Citi RWA Report: Money, Tokens, and Games (Blockchain’s Next Billion Users and Trillion-Dollar Value), we introduced a brand-new $10 trillion tokenized market. Yet before embarking on this grand era of exploration, we must return to first principles—examining tokenization, RWA, and even token-based payments through the lens of blockchain’s foundational concepts, just as we once carefully studied the Bitcoin whitepaper.

To this end, we have compiled the section on tokenization from the 2023 Annual Economic Report of the Bank for International Settlements (BIS), offering industry professionals a reference to better understand the underlying logic of tokenization.

BIS analyzes tokenization from the perspective of monetary and banking systems, revealing a blueprint for the future of global finance. The cornerstone of this vision is the integration of CBDCs, tokenized deposits, and tokenized rights over financial and physical assets into a new type of financial market infrastructure—the “Unified Ledger”—where the full advantages of tokenization can be realized to improve outdated systems and build new ones.

Key Insights

-

Tokens and asset tokenization hold immense potential, but the success of tokenization hinges critically on central bank money providing trusted backing and connectivity to the financial system;

-

The Unified Ledger—a novel financial market infrastructure—can integrate CBDCs, tokenized deposits, and tokenized assets onto a single programmable platform, maximizing the benefits of tokenization;

-

CBDCs and tokenized deposits offer advantages in maintaining the singleness of money, ensuring settlement finality, providing liquidity, and managing risk;

-

The application of tokenization within a Unified Ledger can not only improve existing financial market infrastructures through seamless integration of multiple systems but also unlock entirely new economic arrangements via programmable platforms, creating substantial commercial value;

-

Multiple specialized ledgers can coexist and interconnect via application programming interfaces (APIs) to ensure interoperability while promoting financial inclusion and fair competition;

-

Governance arrangements are crucial to advancing the adoption of Unified Ledgers and tokenization technologies, with appropriate incentives being essential to attract participants and ultimately achieve network effects.

Glossary

Token – A digital representation of a right or asset recorded on a blockchain or distributed ledger.

Tokenisation – The process of recording rights to financial or real-world assets from traditional ledgers onto a programmable platform.

Private Tokenised Monies – Tokens issued by private-sector entities (non-central banks).

Singleness of Money – Refers to a monetary system where only one primary currency exists, and different forms of money (whether public, like cash, or private, like deposits) are interchangeable at par value regardless of form.

Settlement Finality – The point at which a funds transfer becomes irrevocable and legally binding upon receipt.

Unified Ledger – A new type of Financial Market Infrastructure (FMI) that integrates data from multiple sources, platforms, or systems (financial transactions, records, contracts, digital assets, etc.) into a unified system without reliance on centralized institutions.

Programmable Platform – A platform unrestricted by specific technology, capable of executing programs—including environments with ledgers, execution engines, and governance rules—akin to a Turing machine.

Ramp – A smart contract connecting non-programmable platforms to programmable ones. Ramps lock assets on their original platform as collateral for tokens issued on the programmable platform.

Atomic Settlement – Links the transfer of two assets such that both occur simultaneously or neither does, making settlement conditional. This enables T+0 settlement.

Payment-versus-payment (PvP) – A settlement mechanism ensuring one currency is transferred only if another (or others) is simultaneously settled on a final and irrevocable basis—i.e., both sides settle at exactly the same time.

Delivery-versus-payment (DvP) – Delivery versus payment ("hand-to-hand" exchange), a mechanism linking asset delivery to fund transfer, ensuring delivery occurs only when corresponding payment is made.

I. Tokens and Tokenisation

1.1 Definition of Tokens and Tokenisation

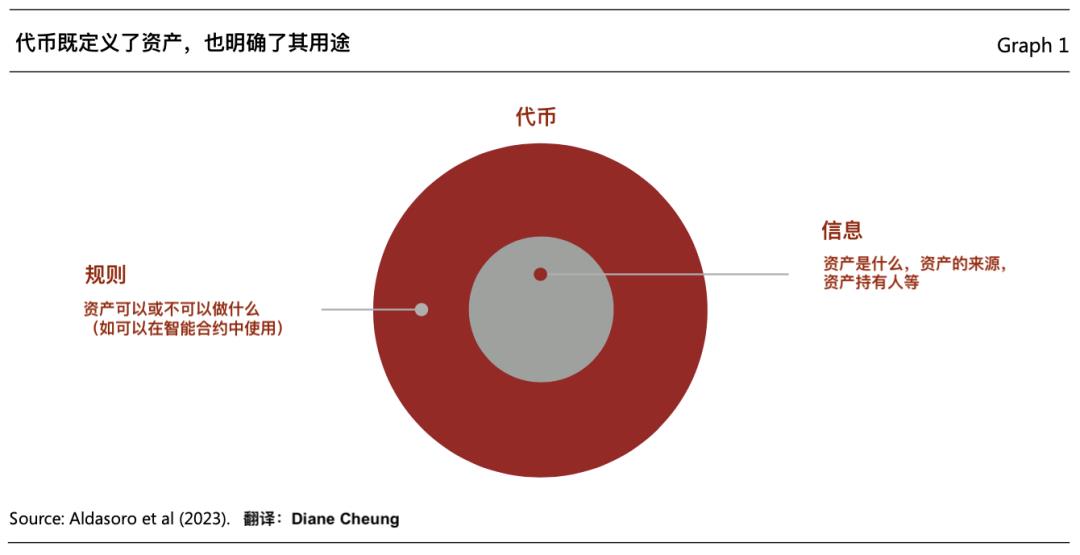

A token is a tradable ownership claim recorded on a programmable platform [1]. Tokens are more than mere digital representations—they typically embed the rules and logic governing the transfer of underlying assets traditionally managed on conventional ledgers (see figure below). Thus, tokens are programmable and customizable to meet specific use cases and regulatory compliance needs.

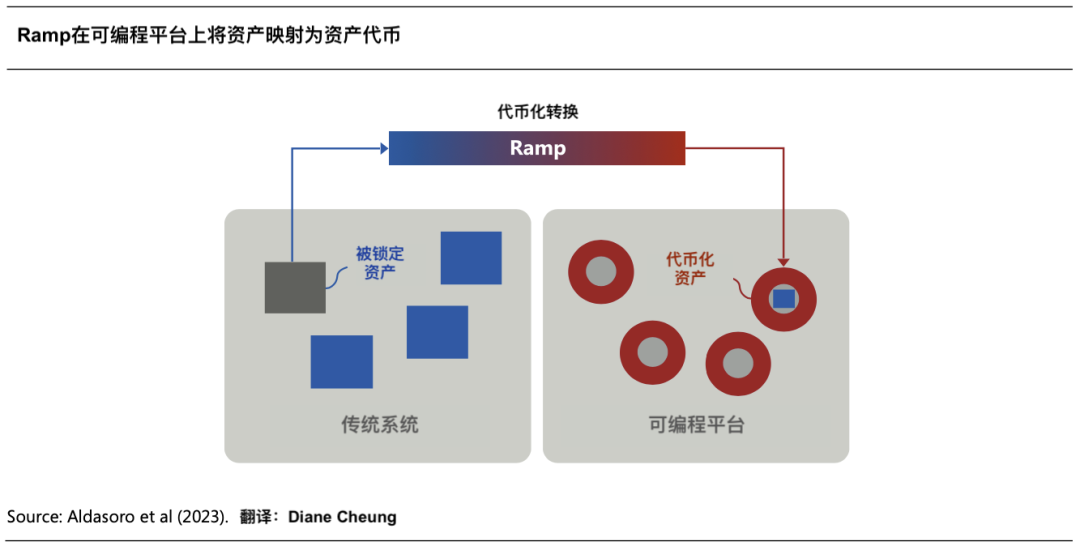

Tokenisation refers to the process of recording ownership claims on financial or real-world assets from traditional ledgers onto a programmable platform [2]. This process is achieved via Ramp contracts (see figure below), which map assets from traditional databases (e.g., securities, commodities, real estate) into tokenized forms on the programmable platform. The assets in the legacy database are frozen or "locked" to serve as collateral backing the tokens issued on the programmable platform. This locking ensures that whenever a token is transferred, the underlying asset ownership changes concurrently.

Tokenisation introduces two critical features: decentralized operational execution and conditional execution via smart contracts.

Decentralized Operational Execution – Unlike traditional systems requiring intermediary custodians to update ownership records, in a tokenised environment, tokens become "executable objects" maintained on the programmable platform. Participants transfer assets by issuing programmatic instructions, eliminating the need for custodial bookkeeping. This expands composability, allowing multiple operations to be bundled and executed together. While this doesn't eliminate intermediaries entirely, it shifts their role from record-keepers to rule managers of the programmable platform, removing dependency on manual ledger updates.

Conditional Execution via Smart Contracts (Contingent Performance of Actions) – Programmable platforms can execute actions conditionally using logical statements such as "if, then, or else."

By combining composability and conditional execution, complex, multi-step transactions can be significantly simplified.

1.2 CBDCs and Private Tokenised Monies

Tokenisation requires both a unit of account and a means of payment to function effectively. Compared to using stablecoins as payment instruments in DeFi applications, CBDCs provide a stronger foundation due to their settlement finality and central bank backing. Programmable platforms can directly embed fiat settlement as an integral part of tokenised arrangements, making CBDCs the optimal choice for tokenisation.

Wholesale CBDC development is key to enabling tokenisation. As a settlement instrument, wholesale CBDCs can replicate the role of reserves in today’s monetary system while gaining new functionalities—such as enabling composability and conditional execution—through tokenisation. These enhanced CBDC tokens could also serve as retail variants accessible to households and businesses, reinforcing monetary singleness by giving the public direct access to sovereign digital currency.

While the role of CBDCs in tokenised environments is relatively clear, the appropriate form of complementary private tokenised monies remains open for discussion. Currently, two main models exist: tokenised deposits and asset-backed stablecoins. Both represent liabilities of the issuer, who promises redemption at par in sovereign currency units. Their differences lie in transfer mechanisms and roles within the financial system, affecting their suitability as complements to CBDCs.

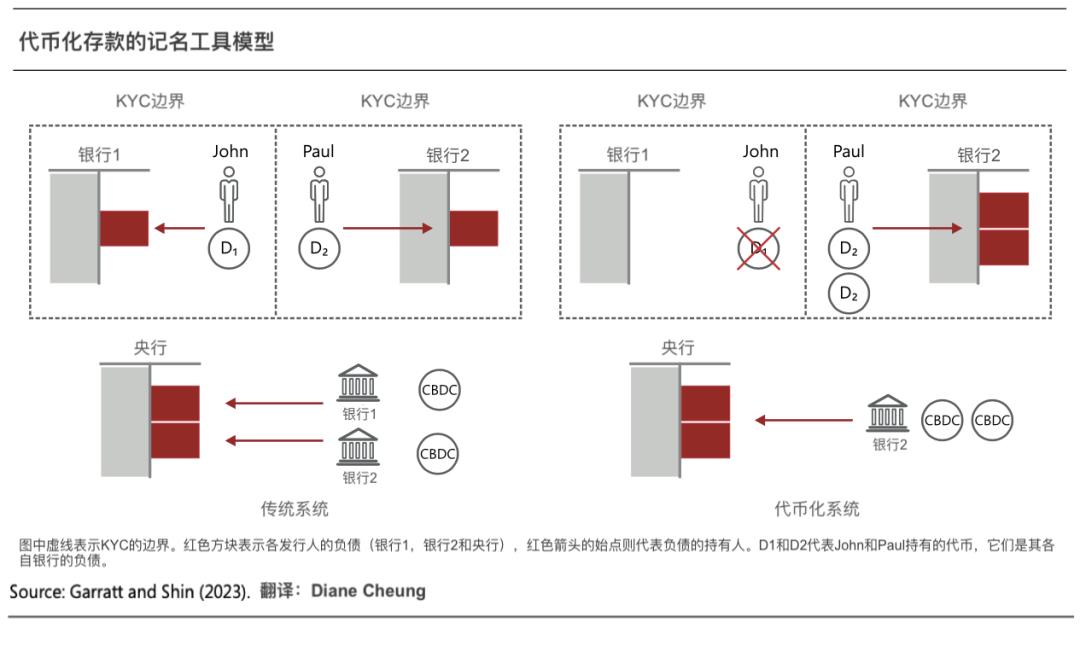

Tokenised Deposits

Tokenised deposits can be designed similarly to conventional bank deposits. Banks issue them as liabilities, and like traditional deposits, they cannot be directly transferred. Central bank-provided clearing liquidity continues to support payment functionality.

For example, consider John and Paul, customers of different banks, both KYC-verified.

In a traditional system, when John pays Paul £100, Paul does not receive a deposit in John’s bank. Instead, John’s bank reduces its balance by £100, and Paul’s bank increases its balance by the same amount. The adjustment between banks is settled via transfers in central bank reserves.

In a tokenised environment, the same outcome can be achieved by reducing John’s tokenised deposit at his bank and increasing Paul’s tokenised deposit at his bank, while concurrently settling the payment via wholesale CBDC transfer. Paul still holds a claim only against his own bank—he has no claim against John or John’s bank.

Tokenised deposits preserve and strengthen key advantages of the current two-tier monetary system.

First, they help maintain monetary singleness. In existing systems, central banks operate settlement infrastructures ensuring final transfer in sovereign currency, preserving uniformity across commercial bank deposits. Tokenised deposits retain this mechanism, and with smart contract-based CBDC settlement, improve timeliness, reduce timing gaps, and lower risks.

Second, CBDC-settled tokenised deposits ensure settlement finality. When the central bank deducts funds from the payer’s account and credits the recipient’s, the transaction becomes final and irreversible. In the above example, settlement finality ensures Paul holds a claim only against his own bank—not against John or John’s bank.

Finally, tokenised deposits allow banks to continue flexibly providing credit and liquidity. In the current two-tier system, banks extend loans and liquidity support (e.g., credit lines) to households and firms. Most money in circulation is created this way—when borrowers receive loans, deposits are credited to their accounts. Unlike narrow banking, this model allows banks to adapt to changing economic conditions, though it requires robust regulation to prevent excessive lending and risky behavior.

Stablecoins

Stablecoins represent another form of private tokenised money but come with inherent flaws. Unlike tokenised deposits, stablecoins represent transferrable claims issued by the issuer—similar to digital bearer bonds. Paying with stablecoins effectively transfers the issuer’s liability between users.

Returning to the John and Paul example: John holds one unit of a stablecoin (i.e., one unit of the issuer’s liability). When he sends it to Paul, the claim is transferred. Before the transfer, Paul held no claim against the issuer. Now, Paul passively holds a claim against an issuer he may not trust. Does Paul trust the stablecoin issuer?

Because stablecoins resemble bearer instruments, the issuer does not need to update its balance sheet during transfers. And since they are privately issued, central banks do not settle these transactions on their balance sheets. The stablecoin itself serves as proof of claim, transferable without the issuer’s consent.

Compared to tokenised deposits, stablecoins have several disadvantages:

First, stablecoins may undermine monetary singleness by causing inconsistent valuations. Since they are tradable, differences in liquidity or issuer credibility can cause prices to deviate from par. For instance, during the Silicon Valley Bank crisis, concerns about liquidity caused massive sell-offs, crashing stablecoin values and breaking singleness. The absence of clear regulation and central bank backing contributes significantly to such issues.

Second, unlike tokenised deposits that flexibly supply liquidity, asset-backed stablecoins operate more like narrow banks. In principle, all USD backing stablecoins should be invested in safe, liquid assets, reducing funds available for other purposes and limiting elastic liquidity provision.

Additionally, compared to tokenised deposits, stablecoins often lack adequate KYC, AML, and CFT oversight, posing risks. In the earlier example, when John sends a stablecoin to Paul, the issuer does not verify Paul’s identity, increasing fraud risks. Enforcing compliance would require significant regulatory overhaul, whereas tokenised deposits can operate within existing frameworks by mimicking traditional deposit transfers.

II. Tokenisation and the Unified Ledger

The full potential of tokenisation depends on integrating monetary and asset transactions within a programmable platform. Tokenisation provides the necessary means of payment linked to underlying asset transfers, with central bank-issued tokenised money at its core to ensure settlement finality. The Unified Ledger acts as a shared space, bringing together CBDCs, private tokenised monies, and other tokenised assets on a single programmable platform to seamlessly enable novel economic arrangements.

2.1 Establishing the Unified Ledger

The concept of a Unified Ledger does not imply a single, universal ledger dominating all others. The implementation approach depends on balancing short-term costs and long-term benefits, especially given the need for new Financial Market Infrastructures (FMIs) and varying jurisdictional requirements.

Linking multiple ledgers and existing systems via APIs to form a Unified Ledger [4] involves lower upfront costs, easier stakeholder coordination, and greater adaptability to local needs. API integration enables partial automation of data exchange, allowing multiple ledgers to coexist and evolve gradually. Governance structures determine participant involvement. However, this incremental approach faces limitations due to compatibility constraints with legacy systems, which tighten over time and may eventually stifle innovation.

Direct deployment of a new Unified Ledger FMI entails higher initial investment and transition costs but allows comprehensive evaluation of long-term technological benefits. Tokenisation presents a transformative opportunity—value generated from programmable platforms will far exceed short-term costs.

Neither approach is universally superior—the choice depends heavily on technical foundations and jurisdictional contexts.

2.2 Architecture of the Unified Ledger

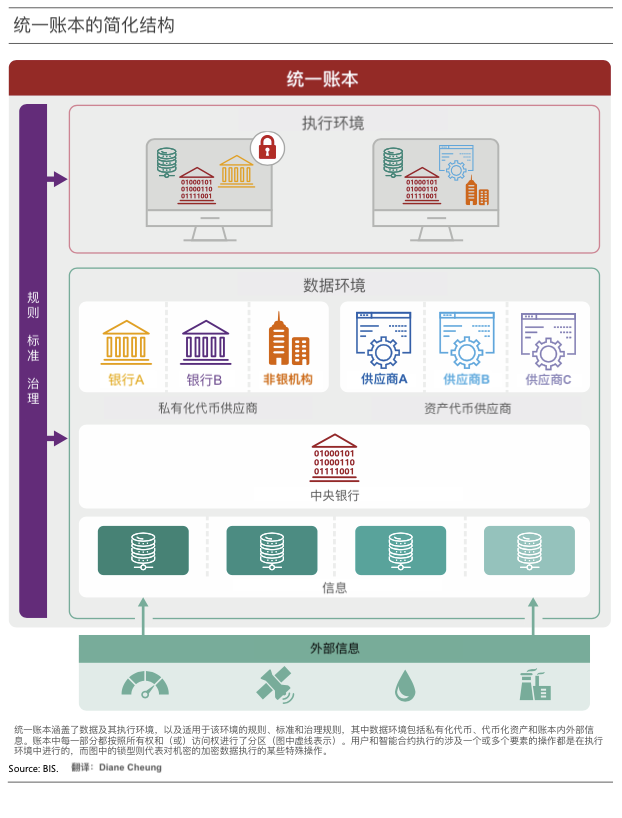

The Unified Ledger maximizes the advantages of tokens within a secure, encrypted, and shared data environment, enabling new types of transactions and optimized contract execution. Two design principles are critical: (1) all components required for transactions must reside on the same platform, and (2) tokens or tokenised assets must be executable objects, securely transferable without relying on external messages or identity verification.

The diagram below illustrates a simplified Unified Ledger structure, consisting of data and execution environments, governed under a common framework.

Data Environment. Comprises three parts: private tokenised monies and tokenised assets, essential operational data (e.g., information needed for secure fund and asset transfers), and real-world data required for contingent operations (from on-ledger results or external sources). Private tokens and assets are stored in isolated partitions operated by qualified entities.

Execution Environment. Executes operations initiated by users or smart contracts, combining only the institutions and assets relevant to a given application. For instance, a peer-to-peer payment via smart contract brings together the users’ banks (issuers of tokenised deposits) and the central bank (issuer of CBDC), incorporating external conditions as needed.

Common Governance Framework. Defines interaction rules among components in the execution environment and privacy protocols to ensure strict confidentiality. Data partitioning and encryption are key tools. Partitioning isolates data zones, granting access only to authorized entities; encryption protects data in transit and storage, decryptable only by authorized parties. Together, they ensure security and trust in financial operations.

III. Use Cases

As discussed, tokenisation and the Unified Ledger can enable new economic arrangements, improving existing models and creating innovative ones.

3.1 Enhancing Existing Models

Tokenisation can enhance current payment and securities settlement systems.

3.1.1 Payment Settlement

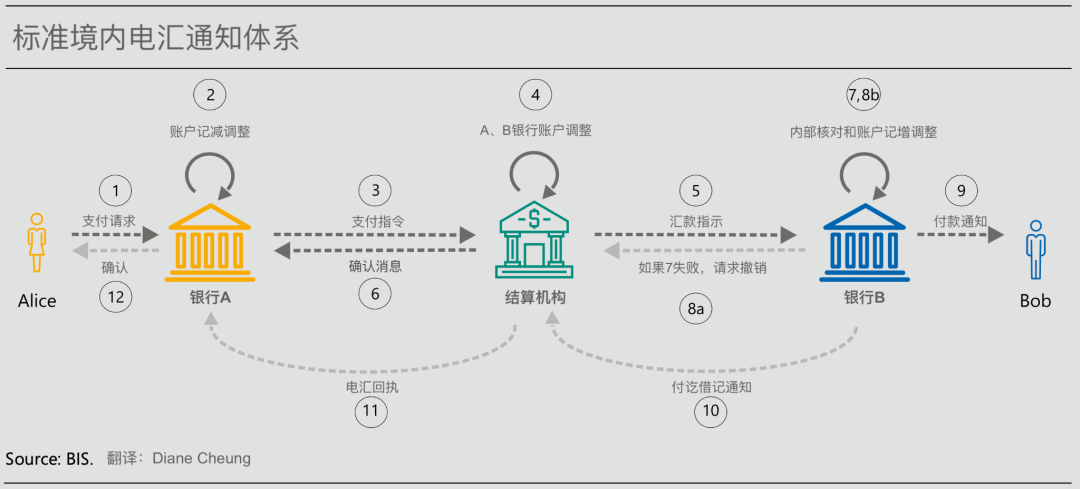

Current payment systems meet basic needs but suffer from high costs, slow speeds, and low transparency. Digital money resides at the edge of communication networks, requiring proprietary databases operated by banks and non-banks to coordinate via external messaging. Separating messaging, reconciliation, and settlement causes delays, and participants lack full visibility, leading to high error-correction costs and operational risks [5].

The diagram below shows a simple domestic wire transfer flow. Transferring funds from sender Alice to recipient Bob involves numerous notifications, internal checks, and account adjustments, making progress hard to track. Senders and recipients remain passive observers of status updates [6]. Cross-border payments are even more complex, involving international messaging, time zones, holidays, and FX settlement, further delaying transactions and increasing risk.

The Unified Ledger addresses these issues. With private tokens and CBDCs on the same programmable platform, sequential messaging between proprietary databases becomes unnecessary. The Unified Ledger uses atomic settlement—simultaneous exchange of two assets—ensuring concurrent asset transfers. This integrates message flows with payment execution, eliminating delays and reducing risk. Data partitioning and access controls simultaneously ensure data privacy and transaction transparency, enhancing user experience.

3.1.2 Securities Settlement

Securities settlement [7] is another prime area where the Unified Ledger adds value.

Current processes involve many intermediaries—brokers, custodians, central securities depositories (CSDs), clearing houses, registrars—leading to complex messaging, fund flows, and reconciliation, resulting in long cycles, high costs, and exposure to replacement cost and principal risk.

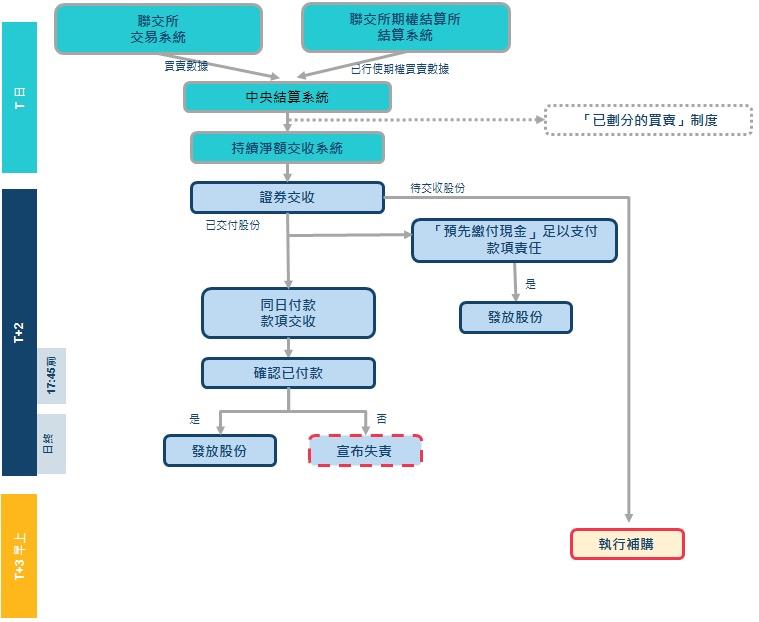

In traditional systems, CSDs manage securities for beneficial owners directly or indirectly. Buyers or sellers initiate trades through brokers or custodians, with final settlement taking up to two business days (see Hong Kong Exchange’s process below), exposing parties to replacement cost risk (risk of having to re-trade at worse prices if settlement fails). Asynchronous delivery and payment also create principal risk—sellers may not get paid, or buyers may not get securities.

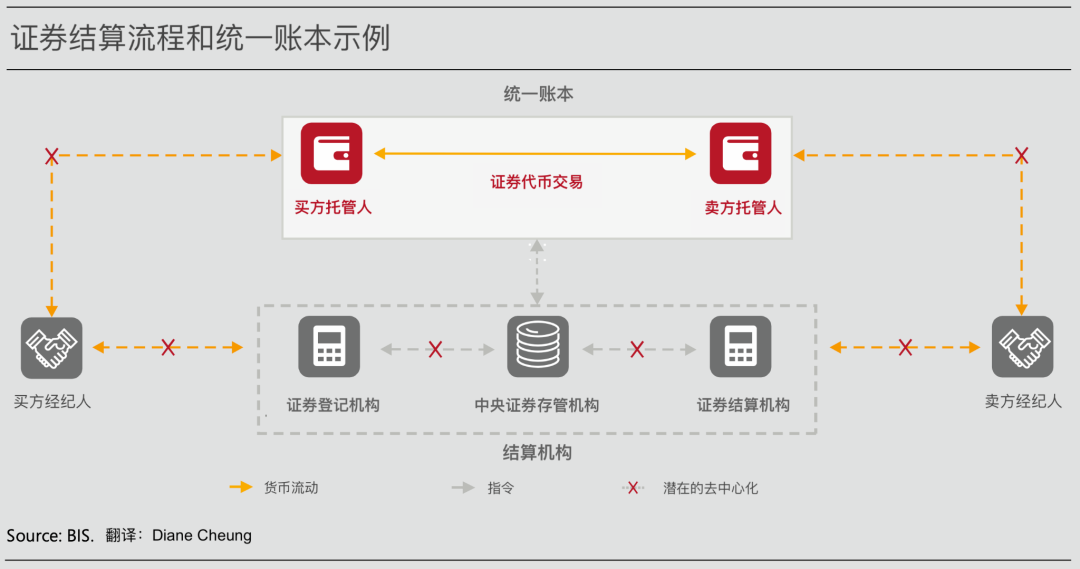

The Unified Ledger and tokenisation can improve securities settlement. As shown below, integrating tokenised money and securities on a programmable platform shortens settlement times, eliminates messaging and reconciliation, and reduces replacement cost risk. Synchronized delivery and payment expand DvP coverage, lowering principal risk. Implementing this requires liquidity-saving mechanisms [8], as atomic settlement demands higher liquidity—similar to transitioning from deferred net settlement (DNS) to real-time gross settlement (RTGS).

The Hong Kong Monetary Authority's Evergreen project in 2022 is a prime example of the Unified Ledger enhancing securities settlement—see Green Finance section below.

3.1.3 Foreign Exchange Settlement

The Unified Ledger and tokenisation can also reduce settlement risks in the multi-trillion-dollar FX market.

Existing PvP mechanisms help mitigate settlement risk, but risks persist, and PvP isn't always available or cost-effective for all trades.

24/7 atomic settlement eliminates settlement delays and further reduces risk. Smart contracts combining FX pairs with authorized providers can expand PvP scope and lower transaction costs.

3.2 Creating New Business Models

Beyond improving existing services, the Unified Ledger can create entirely new arrangements by combining smart contracts, secure and confidential data storage and sharing, and tokenised transaction execution.

3.2.1 Mitigating Bank Run Risks

Smart contracts can broaden collective action, overcoming individual free-rider [9] behavior and reducing bank run risks.

Time deposit contracts are bilateral agreements between banks and depositors. Under liquidity stress, deposit value may depend on collective depositor decisions. Since banks invest primarily in illiquid assets, early withdrawals under "first-come, first-served" rules protect early movers, triggering runs.

Smart contract-based deposits can mitigate this: conditional enforcement ensures all depositors share equal outcomes regardless of withdrawal order, removing incentives to withdraw early out of fear. While not eliminating all runs, it reduces first-mover advantage and coordination failure in typical scenarios.

3.2.2 New Supply Chain Finance

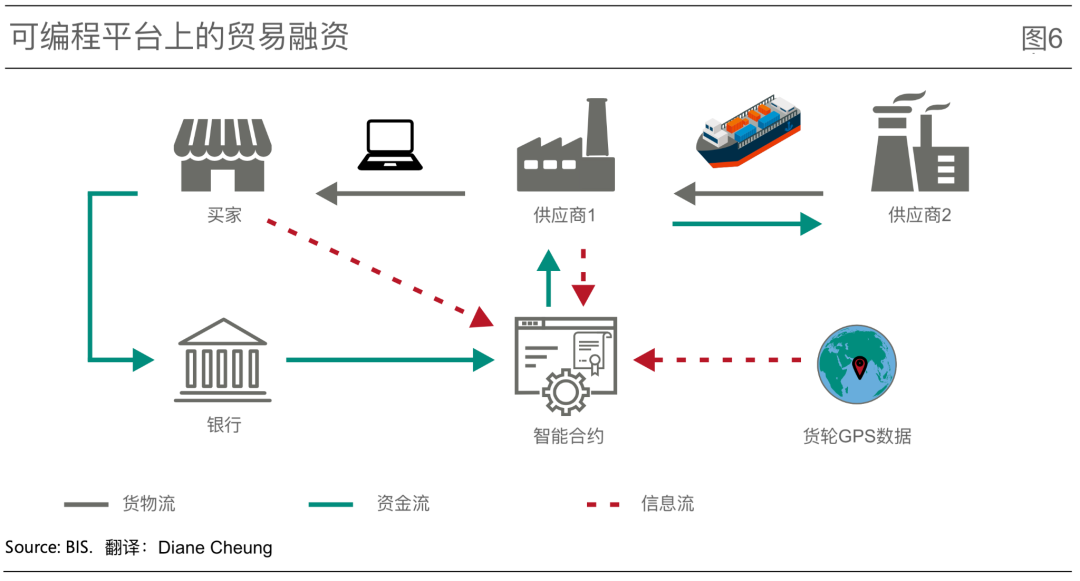

Integrating real-time data into smart contracts enables improved supply chain finance via the Unified Ledger.

Below is a simple supply chain: a buyer (typically a large firm) purchases goods from Supplier 1 (often an SME), who sources raw materials from Supplier 2. The buyer usually pays after delivery, but Supplier 1 must pay wages and material costs beforehand, necessitating financing until payment arrives.

Due to risk of non-payment post-delivery, SME financing typically takes the form of secured trade loans. For example, an Italian SME importing semi-finished goods from India secures a loan using in-transit cargo as collateral. If the SME defaults, creditors can reclaim the goods. But risks of damage (piracy, storms) mean lenders may offer insufficient credit or charge higher rates. SMEs might also commit fraud—pledging the same collateral to multiple lenders. These common issues force suppliers to rely solely on internal capital.

The Unified Ledger can alleviate trade finance problems by integrating supply chain relationships and financing steps. Smart contracts between buyer and supplier can automate payment upon delivery or partial payment at milestones, reducing non-payment risk. Loan smart contracts between banks and suppliers can use IoT data to automatically adjust terms—e.g., lowering interest or extending credit after passing high-risk zones. This supports early working capital needs. Since collateral is recorded on the ledger and cannot be double-pledged, lender risk drops, boosting willingness to lend.

3.2.3 Optimizing Lending Services

Through secure and confidential data sharing, the Unified Ledger can leverage data to lower credit costs and improve access.

First, integrated data enables lenders to incorporate diverse data into credit risk assessments, reducing borrowing costs and collateral dependence.

Second, encryption allows users to retain control over their data, mitigating high borrowing costs caused by network effects. While network effects aggregate user data and facilitate lending, growing service popularity creates a Data-Network-Activities (DNA) cycle. Rising market concentration leads to excessive profits and inflated borrowing costs. By preserving user data control, the Unified Ledger lets users decide whether lenders can access their data, curbing monopolistic profits and lowering borrowing costs for households and businesses.

Moreover, improved data sharing can enhance financial inclusion, incorporating data from minorities and low-income households. "Thin-file" applicants benefit from alternative data screening, as traditional credit scores disproportionately penalize their perceived default risks. More comprehensive data improves assessment accuracy, lowering borrowing costs for these groups.

3.2.4 Anti-Money Laundering

Using encryption, the Unified Ledger can introduce stronger AML and CFT methods.

Financial institutions must protect sensitive proprietary data, yet inability to share such data without exposing confidentiality hinders AML/CFT efforts. The Unified Ledger provides transparent, auditable records of transactions, transfers, and ownership changes, while encryption enables secure cross-border data sharing compliant with local regulations to detect fraud and money laundering.

Leveraging tokens’ dual attributes—carrying identification data and encoding transfer rules—further enhances effectiveness. For example, regulatory compliance data (parties involved, geographic attributes, transaction type) can be embedded directly into tokens. BIS Innovation Hub’s Aurora project explores using enhanced privacy tech and advanced analytics to combat cross-institutional and cross-border money laundering.

3.2.5 Asset-Backed Securities

Combining smart contracts, data, and tokenisation can streamline securitization and bond issuance/investment.

Take mortgage-backed securities (MBS): pools of mortgages are layered into tranches and sold to investors. Even in the US, where MBS markets reach $12 trillion in liquidity, the process involves over a dozen intermediaries and is highly complex.

Automated smart contracts can eliminate delays in information and fund flows, simplifying securitization. Tokens can integrate real-time data on borrower repayments, collections, and investor distributions, further reducing reliance on intermediaries.

3.2.6 Green Finance

Green finance is another prominent use case for innovation via the Unified Ledger and tokenisation.

A digital platform allows investors to download an app and invest any amount in tokenised government green bonds funding sustainable projects. During the bond term, investors can view accrued interest and real-time metrics like clean energy generated and carbon emissions reduced. The bond also enables transparent secondary market trading.

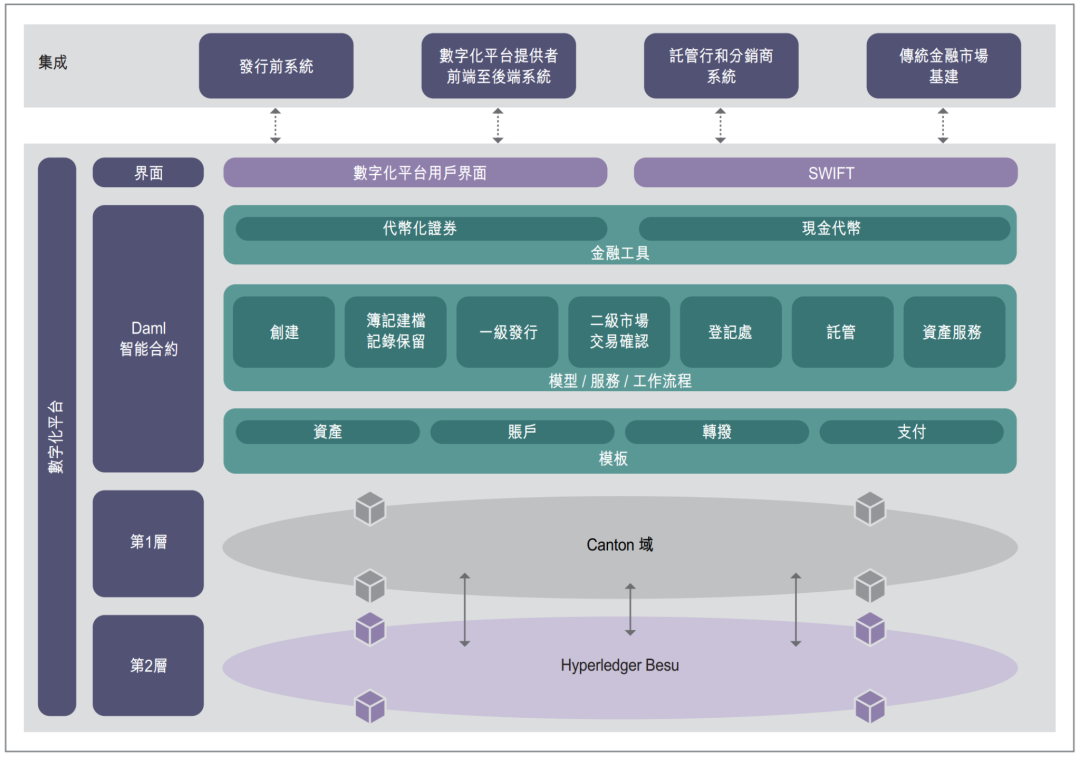

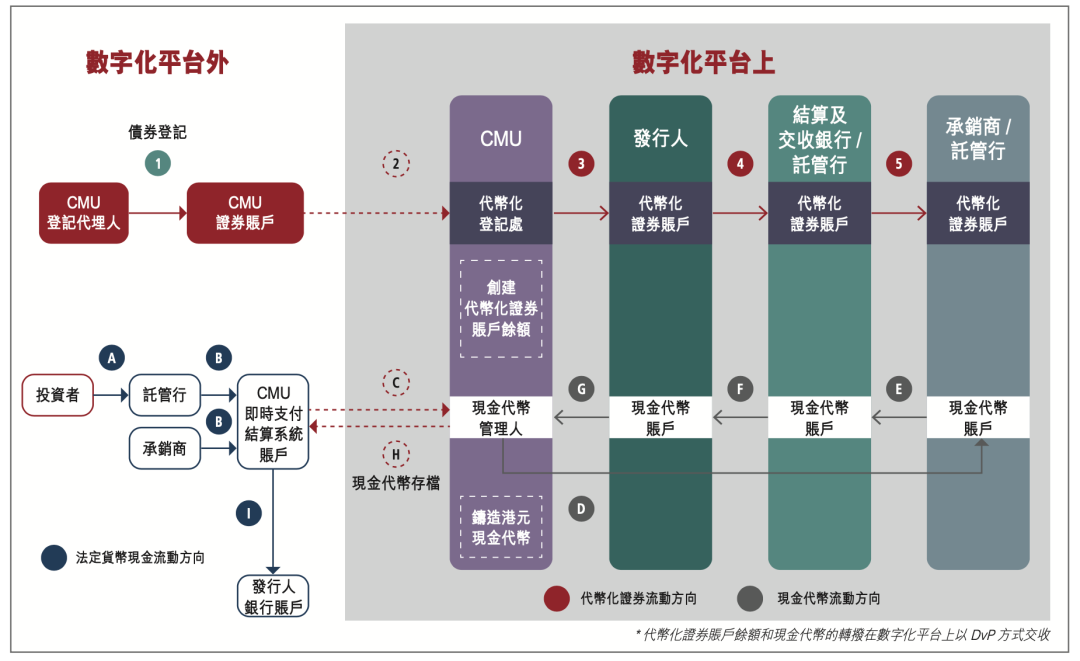

Under the BIS Innovation Hub’s Genesis project, BIS and HKMA have jointly explored this domain, launching the Evergreen project in 2022 to issue green bonds via tokenisation and the Unified Ledger. The project’s architecture and primary issuance workflow are shown below. It fully leverages the distributed ledger to integrate all participants on a single data platform, supporting multi-party workflows with role-based authorization, real-time validation, and digital signatures—enhancing efficiency. Bond settlement achieves DvP, reducing delay and risk. Real-time data updates improve transparency. Though the project uses API integration between legacy systems and the Unified Ledger, it marks a meaningful step in efficiency gains and risk reduction.

Evergreen Project Overall Architecture

Primary issuance workflow of Evergreen project with DvP settlement

IV. Foundational Principles for Unified Ledger Applications

Applying the Unified Ledger and tokenisation requires adherence to overarching principles. The foremost is alignment with the two-tier monetary structure: central banks maintain monetary singleness via wholesale CBDC settlement, while the private sector innovates for public benefit.

Additional principles around scope, governance, competition, data privacy, and operational resilience are equally vital. They ensure a level playing field, foster competition, protect data, and maintain system robustness. Implementation depends on jurisdictional needs and specific use cases.

4.1 Scope, Governance, and Competition

4.1.1 Scope of the Unified Ledger

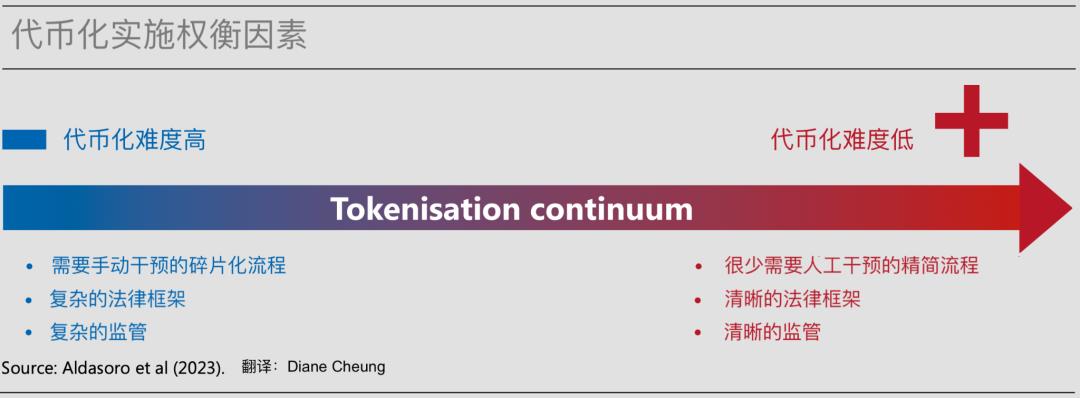

As noted, the Unified Ledger can host multiple specialized ledgers. Applications can begin with targeted use cases for clearer impact. The diagram below outlines the scope and characteristics of tokenisation applications. When implementing, a balanced assessment is needed: easier applications may yield modest returns, while harder ones could generate substantial benefits. In the short term, focus should be on identifying assets suitable for tokenisation with high transaction volumes. Starting with specific use cases, the Unified Ledger’s scope can expand over time, shaped by jurisdictional needs and constraints.

The Unified Ledger is essentially a new FMI (or combination thereof). As stated in the Principles for Financial Market Infrastructures [10], FMIs must provide clear, final settlement in central bank money wherever feasible and available—a principle applicable to payment systems, CSDs, securities settlement systems, CCPs, and trade repositories.

4.1.2 Governance and Competition

The scope of the Unified Ledger directly affects governance, competitive landscape, and participant incentives.

Governance can follow existing models: central banks and regulated private participants collaborate under established rules. For payment settlement, central banks handle final settlement, while regulated private providers deliver user services, complying with KYC, AML, CFT, and ongoing due diligence to ensure privacy.

As scope expands, governance complexity increases. A cross-border payment Unified Ledger requires seamless interoperability between private PSPs and central banks across jurisdictions with differing regulations, demanding extensive coordination. In contrast, a domestic securities settlement ledger requires less coordination.

For competition and financial inclusion, an open, fair environment is essential. Regulators must assess how introducing a universal platform affects industry structure and the broader financial system. Open platforms promote healthy competition and innovation, lowering end-user costs by reducing excessive profits. Regulators should design platforms and rules to serve consumer interests, preventing monopolistic dominance.

Providing proper economic incentives is key to encouraging participation. Without incentives, private PSPs may opt out. If new technologies disrupt existing incentive structures, reducing incumbents’ influence or profits, adoption may stall. Mandating participation while enabling private-sector innovation may be critical—participants gain economic benefits, network effects grow with scale, creating positive feedback.

4.2 Data Privacy and Operational Resilience

Aggregating money, assets, and data on one platform makes data privacy and operational resilience paramount.

4.2.1 Privacy Protection

Consolidating diverse data raises concerns about theft or misuse. Adequate safeguards are essential. A conservative approach to data management on the Unified Ledger helps protect privacy. Commercial secrets pose similar challenges—firms will only join if their confidential information is adequately protected.

Creating data partitions within the Unified Ledger’s data environment is crucial for privacy. Each participant sees only data in their authorized partition. Private keys further strengthen protection—partition updates, identity authentication, and authorizations are performed via private keys, ensuring only authorized accounts manage data.

Encryption is another effective tool. When participants interact, data from different partitions must be shared and processed in the execution environment. Secure computation techniques allow mathematical operations on encrypted or anonymized data without exposing sensitive details. This satisfies financial institutions' and users' desire for privacy-preserving data sharing, while decentralization fosters competition and innovation. Commercial secrets can be protected by encrypting individual smart contracts—only the owner or designated parties can access code details.

Various technologies enable confidentiality and privacy on the Unified Ledger, each with trade-offs in privacy level, computational burden, and implementation difficulty.

Furthermore, as a public-interest institution with no commercial interest in personal data, the central bank can embed privacy protections at the design stage—e.g., directly encoding privacy laws into tokens. Data privacy laws grant consumers rights to authorize or deny third-party data use. For example, the EU’s GDPR requires companies to delete personal data upon request; California’s CCPA grants consumers insight into collected data. By embedding options like “do not sell” or “delete my data” directly into token and smart contract logic, the Unified Ledger strengthens enforcement of data privacy laws.

4.2.2 Cybersecurity Threats

Beyond privacy, operational resilience is critical. Cyberattack-related losses have surged in recent years, requiring strong institutional and legal safeguards. When an FMI or Unified Ledger suffers a cyberattack, the resulting systemic paralysis and societal damage are incalculable—far exceeding financial and reputational losses. Broader scope increases single points of failure and potential loss. Hence, sufficient investment in cybersecurity is essential, with multi-layered measures to protect data integrity and confidentiality.

V. Conclusion

To fully realize innovation in money, payments, and broader financial services, central banks play a pivotal role in shaping a future monetary system adaptable to real-world needs and technological advancement.

This article outlines a blueprint for the future monetary system, harnessing the transformative power of tokenisation to improve existing structures and unlock new possibilities. This vision centers on the Unified Ledger—a new FMI integrating CBDCs, tokenised deposits, and tokenised rights over financial and physical assets on a single platform. Its advantages include enabling seamless, automated execution of broader financial transactions with synchronized, instant settlement, and consolidating all data on one platform to overcome information and incentive challenges for public good.

While tokenisation and the Unified Ledger reveal the trajectory of future monetary systems, actual implementation depends on jurisdiction-specific needs and constraints. Multiple ledgers can coexist and interoperate via APIs.

Achieving this vision requires joint efforts from public and private sectors to develop technical solutions, build common digital platforms, and ensure appropriate regulation and oversight. Through collaboration, innovation, and continuous integration, we can build a trust-based monetary system enabling new economic arrangements, enhancing financial efficiency and accessibility, and meeting the evolving needs of households and businesses.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News