A Brief Analysis of the Blockchain Transaction Lifecycle and the Emerging Trend Toward Rollup-Centric Architectures

TechFlow Selected TechFlow Selected

A Brief Analysis of the Blockchain Transaction Lifecycle and the Emerging Trend Toward Rollup-Centric Architectures

This article aims to share personal insights based on recent observations of the primary market in the infrastructure sector.

Author: Jiawei, IOSG Ventures

Unnoticed, 2023 is approaching its fourth quarter.

Overall, the recent primary market has been relatively dull, with most projects being old ideas repackaged in new forms.

Judging solely by valuations, however, enthusiasm remains strong. This article aims to share some personal insights based on recent observations of infrastructure-sector investments in the primary market.

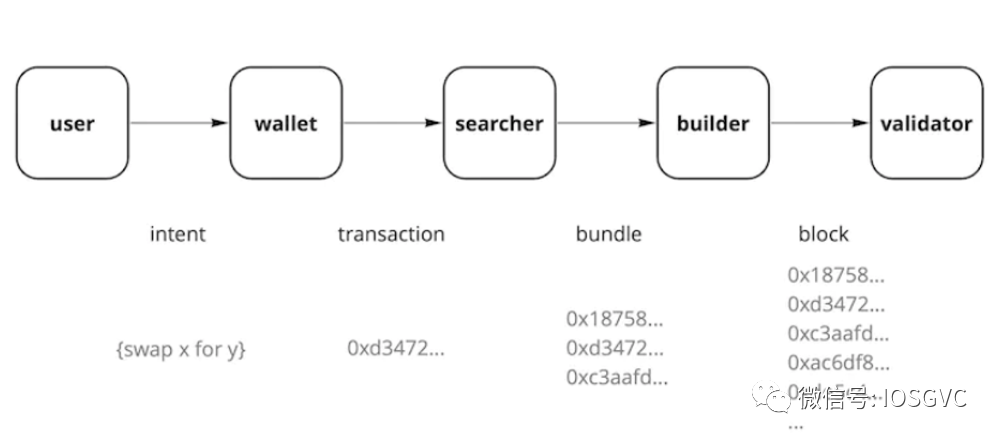

Transaction Lifecycle

Based on the transaction lifecycle, certain infrastructure projects can be categorized as follows:

-

Validator

-

Validators can be classified into Solo Staker, Staking Service Provider, CEX Staking, and Liquid Staking; alternatively, they can be grouped into crypto-native (e.g., Lido) and compliant (e.g., Liquid Collective) categories.

-

Currently, Ethereum’s staking rate stands at approximately 22%. I estimate there remains around 15% growth potential over the next one to two years, with a significant portion likely coming from traditional institutions allocating ETH as part of their asset portfolios. Institutional participation in Ethereum staking would help consolidate and diversify the validator set.

-

Custodians (such as Fireblocks and BitGo) typically partner with Staking Service Providers to offer customized, end-to-end yield aggregation services. Meanwhile, most wallets—especially hardware wallets—have also integrated staking entry points. These partnerships constitute distribution alliances within staking, offering high flexibility—even allowing competitors to collaborate. Typically, staking providers capture about 10%-30% of profits, while those supplying user traffic receive larger revenue shares.

-

Currently, driven by events (e.g., SEC blocking Kraken’s U.S. staking operations), price competition (reducing staking fees), and client differentiation (crypto-native vs. compliance tracks), the Ethereum staking market exhibits dynamic competitive dynamics. In my view, the compliant market will become a key battleground going forward. Geographically, as U.S. crypto regulations tighten, most staking services are seeking opportunities in Asia-Pacific, which, along with the Middle East, represents emerging growth regions for staking businesses.

-

-

Builder

-

Builders aggregate order flow through various channels and bid against each other in auctions to win block space. Conversely, Builders act as intermediaries who wholesale block space from Proposers, disaggregate it, and resell it to Searchers, capturing a margin. The core competitiveness of a Builder lies in two aspects: Orderflow and Infrastructure.

-

The former refers to the fundamental input for Block Building—the more order flow a Builder accesses, the greater the opportunities to extract MEV. Without sufficient order flow, even superior strategies are futile, leaving the Builder uncompetitive.

-

The latter—also known as simulation capability—requires continuously simulating and executing incoming transactions to update bids, while monitoring rivals’ bids for real-time adjustments. This process operates at millisecond precision, with Builders potentially updating their bids hundreds of times within a single 12-second slot.

-

Builders may also need to strategically apply subsidies (i.e., spending money to gain or maintain market share). Roughly speaking, a Builder’s market share reflects Execution/Inclusion Guarantee—the probability that a Searcher’s bundle will be included in the next block when entrusted to them. Since this directly affects profitability, Searchers demand high execution certainty. Thus, subsidies function as marketing tools. Given that bid differences among Builders are often minimal, only small per-slot subsidies are needed. Under such competitive conditions, deciding wisely when and how much to subsidize becomes a strategic game.

-

Since The Merge and the gradual adoption of MEV-Boost, the Builder landscape has undergone several shifts. Due to accumulated advantages in order flow, infrastructure, and experience, leading Builders have achieved near-monopolistic positions that are difficult to challenge. Overall, I believe the market has reached a winner-takes-all state, with the top four Builders controlling 85% of the market. Their business models yield thin margins, and long-term stability remains uncertain. Mid-tier or downstream Builders struggle to secure sustainable economic incentives and may eventually exit, further consolidating upstream dominance. (This analysis applies to neutral Builders; Searcher-Builder entities might fare better, though their profitability—especially involving CEX-DEX arbitrage—is harder to assess.)

-

-

Users and Wallets

-

OFA (Orderflow Auction): OFA allows users or wallets to send orders to an auction, disclosing partial order information so buyers can assess value and bid accordingly. Winning bids are returned to users or wallets as rebates. Currently, two main products exist: MEV-Share and MEV Blocker. To date, the latter has returned approximately 443 ETH in rebates to around 320,000 users.

-

OFA is generally beneficial for users (despite a recent Blocknative article suggesting OFAs lead to higher slippage and slower execution), as it enables them to capture value previously lost and receive rebates, while avoiding frontrunning and sandwich attacks. Wallets can also monetize order flow. Additionally, OFA offers Searchers and Builders a new channel to acquire diversified order flow. However, if more users and wallets adopt OFA instead of sending transactions to public mempools, acquiring order flow becomes costlier, squeezing upstream supply chain profits.

-

-

Intent represents a broad concept across the transaction lifecycle and signifies a paradigm shift in blockchain transaction models.

-

Traditional transactions require users to specify execution paths—like choosing a restaurant and ordering specific dishes. Intent, by contrast, involves stating a goal and a willingness to pay, then opening it to competitive bidding, ultimately selecting the best solution. For example, setting a $500 per-person budget and letting different restaurants propose meal plans, with the optimal one chosen. Competition thus manifests in pricing, with reverse auctions lowering user costs.

-

I consider Intent a significant investment direction, for three reasons: First, transactions are fundamental to on-chain expression, and Intent introduces a paradigm-level transformation. Second, the field is still early-stage, with projects like Flashbots and Essential, developers, and communities still exploring—no clear winners yet. Third, Intent is inherently complex, with wide design spaces in both technical architecture and economic incentives, leading to vastly different approaches, making it too early to predict victors.

-

Despite this, I believe we’ll remain in a transitional phase where traditional and Intent-based transaction models coexist for the foreseeable future. Claiming an “Intent-centric” era may be premature.

-

In summary, analyzing by transaction lifecycle reveals a trend of infrastructure expanding toward upstream stages, marked by increasing specialization and refinement, growing diversity in competition, and efforts to maintain balanced competitive conditions.

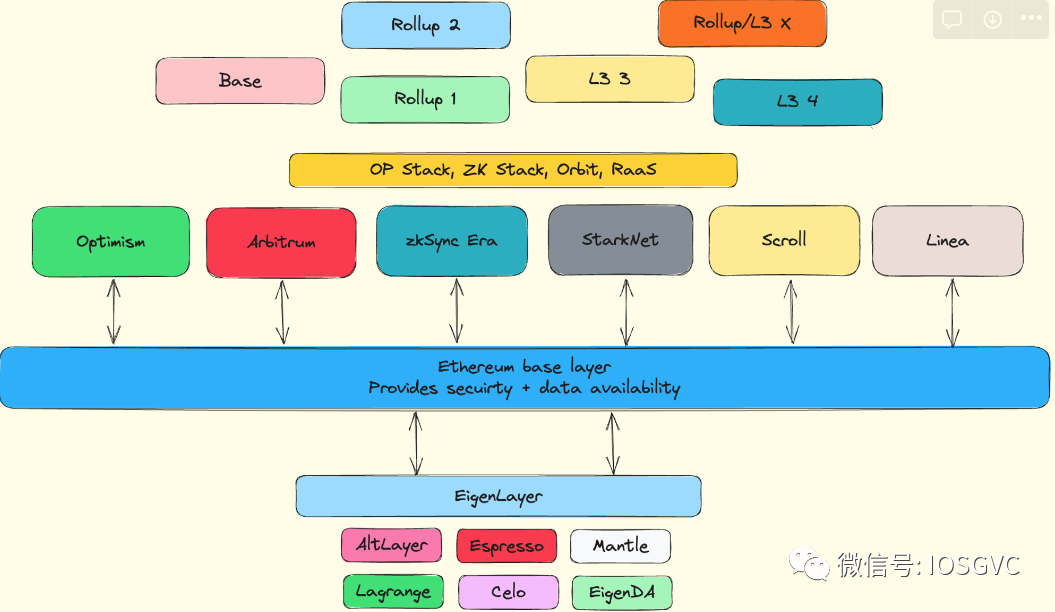

Rollup-Centric Roadmap

In October 2020, Vitalik proposed the Rollup-Centric Roadmap, advocating that Ethereum prioritize supporting Rollups in the medium term. First, Ethereum’s base layer scalability would focus on increasing block data capacity to enhance data availability—later materialized through data sharding and EIP-4844. Second, Ethereum’s infrastructure would adapt to support Rollups (e.g., ENS L2 integration, wallet L2 support, seamless cross-L2 asset transfers).

Given the thriving development of modular components today, we’re beginning to see the initial realization of the Rollup-centric vision. Under this framework, Ethereum gradually recedes, shedding execution-layer responsibilities to become a highly secure settlement and data availability layer. General-purpose Rollups primarily handle scaling, hosting most applications and user traffic, and further enabling specialized execution environments (e.g., privacy, gaming) via L3s (Fractal Scaling). RaaS provides developers with rapid infrastructure deployment tools. Restaking leverages existing Ethereum staking positions to provide economic security, decentralization, and alignment for new modular components. As ETH’s utility expands, these components reinforce Ethereum’s foundational role and create value feedback loops.

Monolithic vs. modular architectures remain hotly debated. When systems reach sufficient complexity, modularity tends to prevail through practical validation—for instance, automobiles are classic modular products. As an engineering principle, modularity offers standardized interfaces, independence, reusability, and flexibility.

Infrastructure projects continue to be driven by narratives and problem-solving rather than standalone business models, which alone cannot justify high valuations. Within this modular context, competition increasingly resembles BD games, with bear-market sentiment amplifying the importance of business development, testing teams’ operational, marketing, and branding capabilities. Rollups and DA projects clearly need users and clients. Sequencers must capture sufficient value to achieve network effects. RaaS is not a new story—Substrate enabled one-click chain deployment back in 2019. Tools matter less than what applications developers build using them, which determines subsequent value accrual. Shared security projects like EigenLayer and Babylon depend on demand-side participants providing adequate and sustainable economic incentives. Merely replicating a DEX or similar app on every Rollup doesn’t constitute an ecosystem—it requires differentiated hits like Friend.tech.

Currently, Ethereum and its L2 ecosystem retain a dominant position, reinforced by mainstream applications, solid user bases, and proven long-term security—deepening its moat. Celo, as an L1, recently pivoted to becoming an Ethereum L2 supported by restaking. As alt-L1 narratives fade and application-specific chains give way to App-Rollups, new projects must now answer whether they should align with Ethereum. For example, although Celestia leads the modular blockchain narrative, it lacks direct ties to Ethereum. As a general-purpose DA layer, Celestia competes broadly with Ethereum and faces direct competition from EigenDA—a restaking-based alternative—at the same level. Under such categorization frameworks, perceived legitimacy increasingly shapes macro-level project assessments. Nevertheless, returning to investment logic, the key questions remain: Does the project solve real problems rather than fabricate demand? Does it actively communicate externally rather than operate in isolation?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News