Token Design Rating: The Key to Measuring DeFi Protocol Value

TechFlow Selected TechFlow Selected

Token Design Rating: The Key to Measuring DeFi Protocol Value

Which tokens are well-designed? Which tokens need improvement?

Author: Nate | eatsleepcrypto.eth

Translation: TechFlow

Recently I've been thinking a lot about token design and have created a tier list for tokenomics. This article evaluates and analyzes the token designs of several well-known DeFi protocols to explore what constitutes a good token economic model—elements such as value capture, governance rights, and economic security—which are crucial for understanding a token’s intrinsic value. Let's examine which tokens are well-designed, which need improvement, and what insights we can draw from them.

Of course, none of this is investment advice—while solid tokenomics are necessary, they are not a sufficient condition for long-term returns, and a high ranking does not guarantee a protocol’s economic security.

I excluded all tokens from the S-tier because...

1) I never give perfect scores;

2) I'm even hesitant to give an A;

3) I’m not familiar with the “S” tier.

The criteria for this ranking are: protocol utility, value capture, and economic security, each accounting for 30%—these are demand-side factors; the remaining 10% is based on supply-side factors.

I would place Curve Finance at A-.

$CRV has supply issues—some quite serious—but these are cleverly mitigated by veTokenomics. However, I focus more on demand than supply because, in the long run, demand is what matters. Demand for $CRV is proportional to the flow of value from bribes paid to $veCRV holders.

Curve Finance’s fundamental innovation isn’t ve-tokenomics—it’s the bribery system.

Liquity Protocol is also in the A-tier.

Liquity uses over-collateralized $ETH to mint $LUSD. Liquity’s $LUSD is a secure decentralized stablecoin, and this mechanism helps protect its peg.

$LUSD is not without risk, but it comes as close as possible to solving the stablecoin trilemma. Additionally, Liquity rewards $LQTY holders with real yield.

Maya Protocol also lands in the A-tier.

Maya has a dual-token system: $CACAO is used for liquidity pairs, while $MAYA captures system fees.

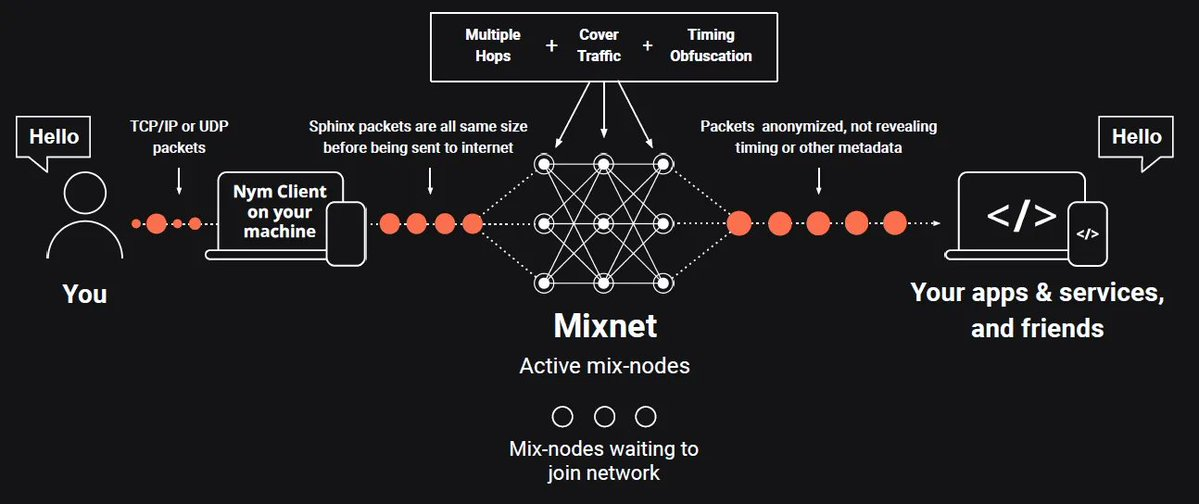

Nym Project has A-tier demand-side tokenomics. The supply side, however, is another story—once they stop distributing $NYM tokens to miners, the price could rebound. I suggest Nym allocate these rewards to community managers who recruit real users through webinars.

Synthetix gets a C+.

$SNX captures significant value, but its use cases are limited—it lacks privacy and has a public founder. If its DAO stops manipulating monetary policy, everything collapses.

Synthetix operates similarly to Mirror on Terra, but with less asset diversification. Because $SNX’s founder is not anonymous, Synthetix cannot issue synthetic versions of commodities or traditional assets (like $TSLA, $GOOG, etc.).

This resulting lack of diversification also makes $SNX more vulnerable and prone to economic security risks, much like Terra’s Anchor protocol.

I went back and forth around the B-tier and ultimately decided to place SushiSwap in the C-tier.

Sushi was lucky during the vampire attack on Uni, and since then it hasn’t really innovated. Real yield is nice—$SUSHI beats $UNI—but that bar is set extremely low. Moreover, real yield isn't just one of the easiest ways to capture value—it's also one of the worst, as it leaves little economic moat.

Aave is ranked C-tier.

Frequent bad debt incidents and a governance council full of degens don’t help it at all. Especially after the recent launch of GHO, where $GHO is still trading at $0.97.

Aave’s central bank strategy for GHO reminds me of USD/JPY carry trades executed by certain funds just before the Bank of Japan announced rate hikes. I’m curious to see how this plays out when Aave raises rates.

Uniswap is ranked D-tier.

I often write about Uniswap’s shortcomings. Unsurprisingly, v4 fails to address UNI’s obvious lack of value capture—and then there’s impermanent loss...

Rocket Pool gets an F. I was going to give it a D, but it has a particularly poor flywheel design, especially compared to competitors. $RPL is inserted as an arbitrary staking requirement, and worse, its rewards aren’t in $ETH but in its native token.

Optimism is also ranked F by me.

$OP’s price is entirely driven by speculation, and Optimism hasn’t taken meaningful action. Optimism hopes to capture value via sequencer revenue—I bet it won’t happen. In the end, $OP still relies on continuous speculation to maintain its price, much like a meme coin. But unlike $DOGE, OP isn’t even used within a circular economy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News