Historical Development and Model Analysis of Decentralized Reserve Stablecoins

TechFlow Selected TechFlow Selected

Historical Development and Model Analysis of Decentralized Reserve Stablecoins

When centralized services are stable and powerful enough, people might not need decentralization at all.

Author: Lawrence Lee

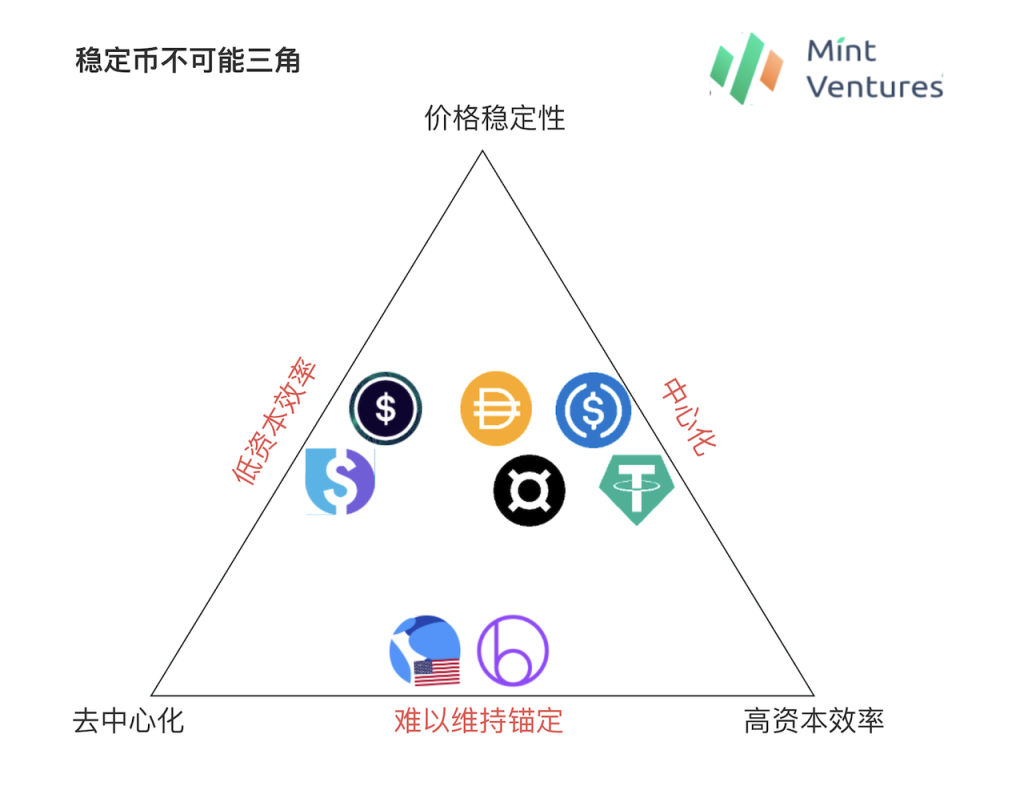

The Impossible Triangle

Chart: Mint Ventures

There has always been an impossible triangle in the crypto stablecoin space: price stability, decentralization, and capital efficiency cannot all be achieved simultaneously.

Centralized stablecoins such as USDT and USDC currently offer the best on-chain price stability and 100% capital efficiency. The only drawback is the risk associated with centralization—BUSD halting new issuance due to regulatory pressure and USDC's depeg during the March SVB collapse clearly illustrate this issue.

Starting in late 2020, a wave of algorithmic stablecoin projects attempted under-collateralization based on decentralization. Projects like Empty Set Dollar and Basis Cash quickly collapsed. Later, Luna used the entire chain’s credit as implicit backing and allowed users to mint UST without over-collateralization. For a significant period (2020–May 2022), it successfully combined decentralization, capital efficiency, and price stability—but eventually succumbed to a death spiral when its credit collapsed. Subsequent under-collateralized attempts, such as Beanstalk, failed to gain substantial market attention. The fundamental flaw for these tokens was their inability to maintain a stable peg.

Another path emerged with MakerDAO, which pursued price stability through over-collateralization of decentralized assets—sacrificing some capital efficiency. Currently, Liquity’s LUSD is the largest stablecoin fully backed by decentralized assets. However, to ensure LUSD’s price stability, Liquity maintains low capital efficiency, with system-wide collateral ratios consistently above 250%. This means each circulating LUSD requires more than $2.50 worth of ETH as collateral. Synthetix’s sUSD is even more extreme; due to higher volatility of its SNX collateral, Synthetix typically requires minimum collateralization exceeding 500%. Low capital efficiency implies lower scalability and reduced appeal to users. Liquity’s planned V2 aims to solve V1’s inefficiency issues, while Synthetix V3 plans to introduce additional collateral types to reduce required collateral ratios.

Early DAI (before or during 2020) also suffered from low capital efficiency. Given the smaller total crypto market cap at the time and high volatility of ETH—the primary DAI collateral—DAI’s price fluctuated significantly. To address this, MakerDAO introduced the PSM (Peg Stability Module) in 2020, allowing centralized stablecoins like USDC to generate DAI. By partially sacrificing decentralization, DAI achieved better price anchoring and higher capital efficiency, enabling rapid scale growth alongside DeFi’s expansion. FRAX, launched at the end of 2020, similarly relies primarily on centralized stablecoins as collateral. Today, DAI and FRAX rank first and second among decentralized stablecoins by circulation—proof of their effective strategies and user demand. But this also indirectly highlights how “maintaining full decentralization” constrains stablecoin scale.

Still, several stablecoins aim to achieve high capital efficiency and strong price stability while preserving decentralization. They attempt to provide users with a stablecoin that:

-

Is generated from decentralized assets (e.g., ETH), avoiding censorship risks;

-

Allows $1 of asset to generate $1 of stablecoin, eliminating the need for over-collateralization and enabling easier scaling;

-

Maintains stable value.

In fact, this represents the most intuitive and theoretically ideal form of a decentralized stablecoin. We adopt Liquity V2’s terminology—Decentralized Reserve Protocol—to describe this type of stablecoin. It should be noted that unlike traditional over-collateralized stablecoins, once a user converts their assets into this type of stablecoin, those assets become owned by the protocol and are no longer linked to the user. In other words, the user effectively performs an ETH → stablecoin swap. These stablecoins resemble centralized ones like USDT—$1 of asset exchanges for $1 of stablecoin, and vice versa—except Decentralized Reserve Protocols accept crypto assets as reserves.

(Some may argue that since collateral no longer belongs to users, such stablecoins lack leverage functionality, losing a key use case. However, I believe real-world stablecoins do not inherently offer leverage. Centralized stablecoins like USDT and USDC never provide leverage. Core monetary functions are medium of exchange, unit of account, and store of value. Leverage is merely a special feature of CDP-type (Collateralized Debt Position) stablecoins, not a general-purpose utility.)

Yet previous stablecoin protocols have failed to sustainably deliver such stablecoins because there’s a seemingly simple but difficult-to-solve problem: How can they guarantee redemption of issued stablecoins at 100% collateral ratio when underlying decentralized assets are highly volatile?

From the stablecoin protocol’s balance sheet perspective, user-deposited collateral is an asset, while issued stablecoins are liabilities. How can we ensure assets always equal or exceed liabilities?

To make it more concrete: If a user deposits 1 ETH valued at $2,000 to mint 2,000 stablecoins, how does the protocol ensure those 2,000 stablecoins can still redeem $2,000 worth of assets when ETH drops to $1,000?

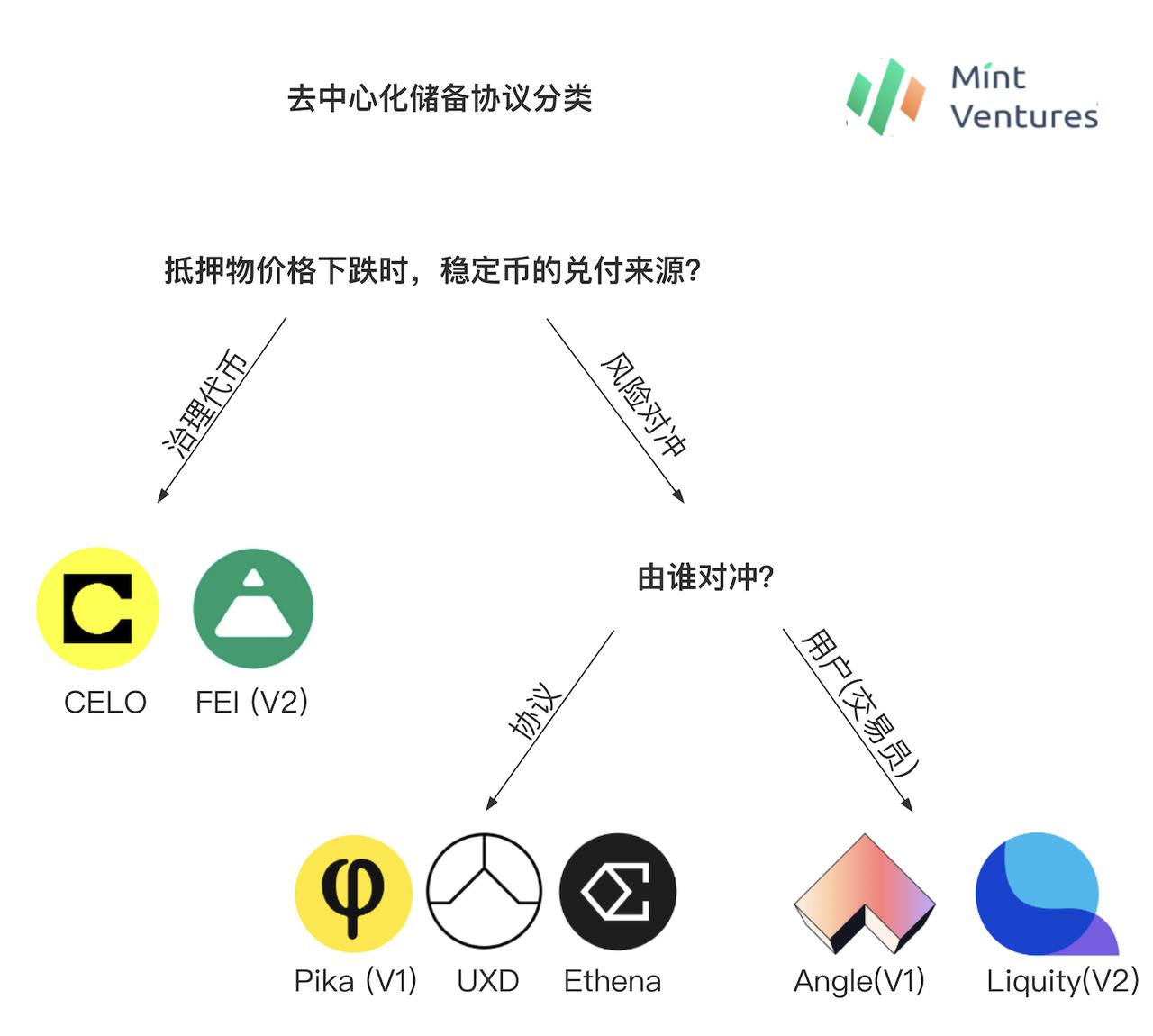

Looking at the development history of Decentralized Reserve Protocols, two main approaches have emerged to solve this: using governance tokens as reserves and risk hedging of reserve assets. Based on hedging methods, the latter further splits into protocol-hedged and user-hedged Decentralized Reserve Protocols. Let’s explore them one by one.

Chart: Mint Ventures

Governance-Token-Backed Decentralized Reserve Protocols

The first category uses the protocol’s own governance token as a “new form of collateral.” When collateral asset prices drop sharply, the protocol mints additional governance tokens to redeem stablecoins held by users. We refer to these as Governance-Token-Backed Decentralized Reserve Protocols. In our earlier example: When ETH falls from $2,000 to $1,000, such a protocol redeems 2,000 stablecoins using $1,000 worth of ETH plus $1,000 worth of governance tokens.

Protocols following this approach include Celo and Fei Protocol.

Celo

Launched in 2020, Celo began as an independent Layer 1 blockchain. In July this year, the core team proposed transitioning Celo to the Ethereum ecosystem via OP Stack. Celo’s stablecoin mechanism works as follows:

Celo’s stablecoins are backed by a diversified reserve pool whose reserve ratio (value of reserves divided by value of circulating stablecoins) far exceeds 1, providing intrinsic value support.

Celo stablecoins aren’t minted through over-collateralization. Instead, users receive stablecoins like cUSD by sending Celo tokens to the official Mento module. Sending $1 worth of Celo yields $1 worth of cUSD, and vice versa. Under this mechanism, if cUSD trades below $1, arbitrageurs buy cheap cUSD to redeem $1 of Celo. If cUSD trades above $1, they mint cUSD via Celo and sell it. Arbitrage keeps cUSD close to its peg.

Three mechanisms ensure reserve adequacy: 1. When reserve ratio falls below threshold, newly minted Celo from block rewards go into the reserve pool, replenishing capital; 2. Transaction fees may be charged (currently inactive); 3. Stability fees collected from Mento trades fund reserve capital.

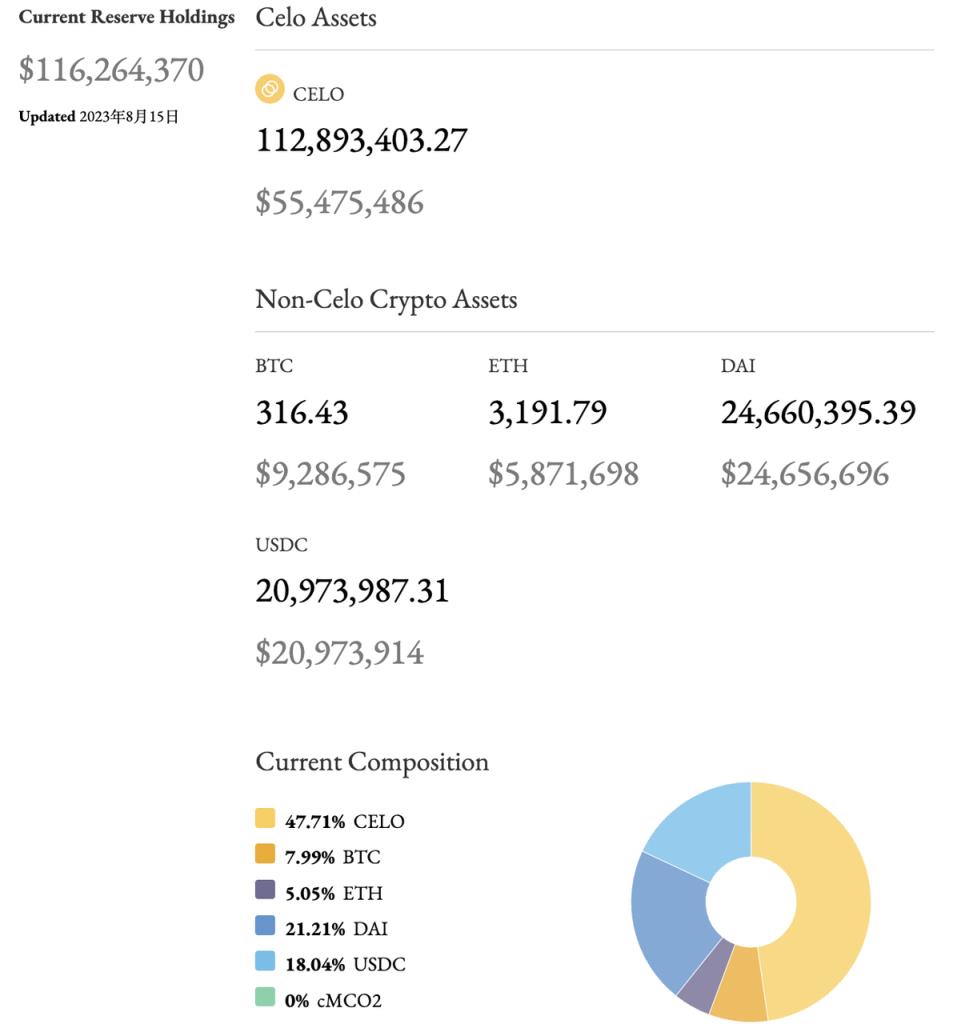

For enhanced security, the reserve portfolio is diverse, including Celo, BTC, ETH, Dai, and carbon credit token cMCO2—safer than relying solely on project-native tokens (similar to Terra’s model, where Luna served as implicit backing).

Source: Mint Ventures Celo Report

As seen, Celo resembles Luna—a Layer 1 centered around a stablecoin—with similar minting/redeeming mechanics. The key difference lies in what happens when the system risks under-collateralization: Celo uses newly minted $CELO from block rewards as protocol collateral to back cUSD redemptions.

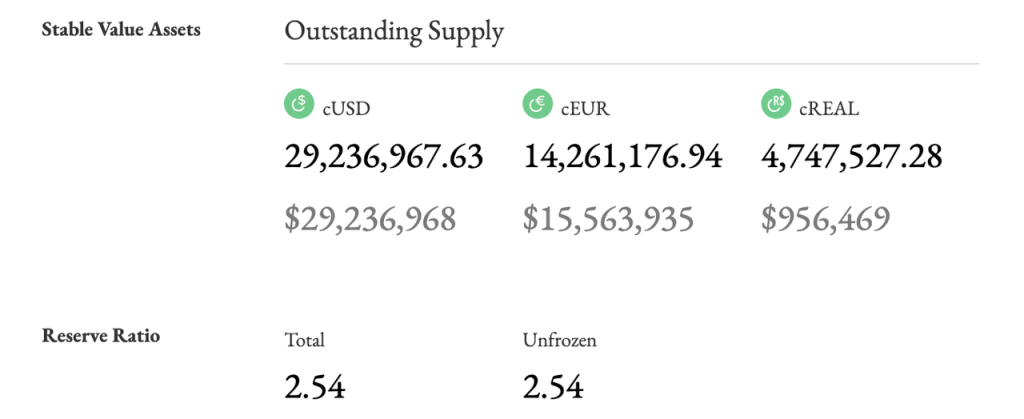

Source: https://reserve.mento.org/

Currently, Celo holds $116 million in total collateral and has issued $46 million in stablecoins, with an overall over-collateralization rate of 254%. While the system remains over-collateralized, users can still exchange $1 worth of CELO for 1 cUSD, achieving excellent capital utilization. That said, half of Celo’s collateral comes from centralized USDC and semi-centralized DAI, so Celo cannot be considered fully decentralized.

Celo ranks 16th in decentralized stablecoin size (14th excluding non-pegged UST and flexUSD).

Fei

In early 2021, Fei Protocol raised $19 million from top-tier investors including a16z and Coinbase, capturing significant market attention due to its alignment with the then-popular algorithmic stablecoin trend. At launch (end of March), it attracted 639,000 ETH to mint 1.3 billion FEI, briefly making FEI the second-largest decentralized stablecoin after DAI (then valued at $3 billion).

However, demand for FEI was largely saturated during genesis minting (mainly driven by users seeking TRIBE governance tokens). With no immediate use cases, FEI remained below $1 for an extended period. Then came May’s market downturn: panic-driven sell-offs led users to redeem FEI en masse, crippling the protocol shortly after launch.

Fei Protocol’s V2, launched late 2021, introduced measures to revive the protocol, including revising its price stabilization mechanism. In V2, FEI could be minted 1:1 against ETH, DAI, LUSD, etc., with deposited collateral going into Protocol Controlled Value (PCV). When PCV / circulating FEI > 100%, indicating healthy asset appreciation and no redemption risk, the protocol would mint extra FEI to buy back TRIBE, lowering collateral ratio. Conversely, if the ratio fell below 100%, signaling potential shortfall, the protocol would mint TRIBE to buy FEI, increasing collateral ratio.

Under this design, governance token TRIBE acts as a backup redemption source during risk events and captures upside during growth (a mechanism similar to Float Protocol, launched alongside Fei V1). Unfortunately, Fei V2 launched near the bull market peak. ETH prices then entered a prolonged decline. Worse, in April 2022, Fei suffered a hack resulting in the loss of 80 million FEI. Ultimately, in August 2022, the team decided to halt protocol development.

Governance-token-backed Decentralized Reserve Protocols essentially dilute governance token holders’ equity to ensure stablecoin redemption. During bull markets, rising stablecoin scale drives up governance token prices, creating a positive feedback loop. But in bear markets, falling asset values drag down governance token valuations. If further minting is needed, token prices may spiral downward, accelerating loss of confidence. Once governance token value falls below a critical threshold relative to stablecoin supply, the protocol’s redemption promise loses credibility, triggering mass exits and a fatal death spiral. Surviving bear markets is key to survival. Celo’s current resilience owes much to its “over-collateralized” state, enabled by allocating significant reserves to USDC/DAI and BTC/ETH during high market valuations—allowing it to remain secure despite CELO dropping from $10 to $0.5.

Risk-Hedged Decentralized Reserve Protocols (Risk-Neutral Stablecoin Protocols)

The second category involves hedging the protocol’s crypto asset holdings. When collateral prices plummet, hedging generates offsetting gains, ensuring assets can cover liabilities. We call these Risk-Hedged Decentralized Reserve Protocols, or Risk-Neutral Stablecoin Protocols. In our earlier example: After receiving 1 ETH worth $2,000, such a protocol hedges the position (e.g., opening a short on an exchange). When ETH drops to $1,000, the protocol redeems 2,000 stablecoins using $1,000 worth of ETH plus $1,000 in hedging gains.

Specifically, depending on who performs the hedge, we distinguish between protocol-hedged and user-hedged models.

Protocol-Hedged Decentralized Reserve Protocols

Protocols taking this approach include Pika Protocol V1, UXD Protocol, and recently funded Ethena.

Pika V1

Pika Protocol is currently an Optimism-based derivatives protocol. However, in its original V1 version, Pika planned to launch a stablecoin, using BitMEX’s inverse perpetual contracts for hedging. Inverse Perpetual Contracts (or coin-margined perps), a BitMEX innovation, differ from today’s popular linear (USD-margined) perps. Instead of tracking price in USD terms, inverse contracts track USD-denominated price in coin terms. Example:

A trader goes long 50,000 contracts of XBTUSD at a price of 10,000. A few days later the price of the contract increases to 11,000.

交易者以 10,000 的价格做多 50,000 份 XBTUSD 合约。几天后,合约价格涨至11,000。

The trader’s profit will be: 50,000 * 1 * (1/10,000 - 1/11,000) = 0.4545 XBT

交易者的利润将是: 50,000 * 1 * (1/10,000 - 1/11,000) = 0.4545 XBT

If the price had in fact dropped to 9,000, the trader’s loss would have been: 50,000 * 1 * (1/10,000 - 1/9,000) = -0.5556 XBT. The loss is greater because of the inverse and non-linear nature of the contract. Conversely, if the trader was short then the trader’s profit would be greater if the price moved down than the loss if it moved up.

如果价格实际上跌至9,000,交易者的损失将是: 50,000 * 1 * (1/10,000 - 1/9,000) = -0.5556 XBT 由于合同的反向和非线性性质,损失更大。相反,如果交易者做空,那么如果价格下跌,交易者的利润将大于价格上涨时的损失。

Source: https://www.bitmex.com/app/inversePerpetualsGuide

Upon analysis, inverse perpetuals appear tailor-made for Risk-Hedged Decentralized Reserve Protocols. Using our earlier example: suppose at ETH = $2,000, Pika Protocol receives 1 ETH and shorts 2,000 ETH inverse perps on BitMEX using 1 ETH as margin. When ETH drops to $1,000, Pika’s gain = 2,000 × 1 × (1/1,000 − 1/2,000) = 1 ETH = $1,000. Thus, when ETH drops from $2,000 to $1,000, Pika’s reserves grow from 1 ETH to 2 ETH—still sufficient to redeem 2,000 stablecoins (ignoring fees and funding costs). Pika V1’s design perfectly mirrors NUSD, a concept described by BitMEX founder Arthur Hayes, capable of perfectly hedging coin-denominated long positions.

Unfortunately, inverse perps—with their counterintuitive, non-linear payoff structure (where local price moves don’t translate linearly to P&L)—are hard for most USDT-based crypto investors to grasp. Over time, inverse perps (coin-margined) gained far less traction than linear perps (USD-margined). On major exchanges, inverse perp volume is only about 20–25% of linear perp volume. Regulatory pressures caused BitMEX to decline from a top-tier exchange to one with less than 0.5% market share. Pika concluded linear perps couldn’t meet their hedging needs, and the inverse perp market was too small. Hence, in its V2, Pika dropped the stablecoin and pivoted to a pure derivatives exchange.

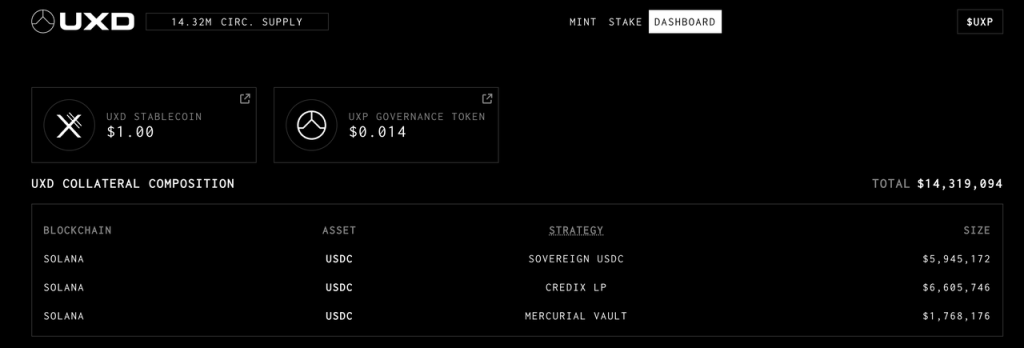

UXD

UXD Protocol is a Solana-based stablecoin launched in January 2022. It previously raised $3 million from Multicoin and $57 million in an IDO. In January this year, UXD announced expansion into Ethereum, launching on Arbitrum in April and planning future deployment on Optimism.

At launch, UXD allowed users to deposit SOL, BTC, and ETH 1:1 to mint UXD. Deposits were hedged via short positions on Mango Markets, Solana’s lending and perpetuals platform. Funding fees earned went to the protocol; paid fees were covered by fundraising capital. For a long time, UXD operated smoothly—so well that it had to cap UXD issuance. Mango Markets’ total open interest was under $100 million; if UXD’s short position reached tens of millions, redemption risk arose. Also, excessive shorts pushed funding rates negative, increasing hedging costs.

Tragically, Mango Markets suffered a governance attack in October 2022, costing UXD nearly $20 million. At the time, UXD’s insurance fund had over $55 million, so redemptions continued normally. Although Mango later returned funds, it never recovered. Coupled with FTX’s collapse draining capital from Solana, UXD could not find suitable venues to hedge its long exposure. Since then, UXD only accepts USDC as collateral—which doesn’t require hedging—and invests USDC into various on-chain treasuries and RWA yield products. UXD’s cross-chain move to Ethereum reflects ongoing efforts to find viable on-chain hedging solutions.

Currently, UXD has $14.3 million in circulation and $53.2 million in insurance fund reserves.

Source: https://dashboard.uxd.fi/

Additionally, the recently announced Ethena Finance stablecoin will also use risk hedging. Ethena raised $6 million from Dragonfly (lead), with participation from centralized exchanges like Bybit, OKX, Deribit, Gemini, and Huobi. Having multiple tier-2 derivatives exchanges as backers could aid hedging execution. Ethena also plans to partner with decentralized derivatives protocol Synthetix, acting as a liquidity provider to open short positions and expanding USDe use cases (e.g., accepting USDe as collateral in pools).

For protocol-hedged Decentralized Reserve Protocols, the advantages are clear: By hedging crypto collateral, the protocol achieves delta-neutral exposure, ensuring stablecoin redemption and ultimately enabling 100% capital efficiency on a decentralized foundation (depending on hedging venue decentralization). If efficient hedging is achieved, excess collateral can earn yield in various ways. Additionally, funding fee income provides flexibility: it can be distributed to stablecoin holders (creating yield-bearing stablecoins with expanded utility) or to governance token holders.

In fact, every stablecoin protocol’s governance token implicitly serves as a “lender of last resort.” Risk-hedged stablecoin protocols can also use their governance token as a final redemption source in extreme scenarios. For stablecoin holders, this offers stronger protection than purely governance-token-backed models. Mechanistically, risk hedging is more coherent and theoretically immune to market cycles—no need to test governance token resilience during bear markets.

But challenges remain:

-

Centralization risk of hedging venues. Centralized exchanges still dominate perpetual contract liquidity. Most decentralized derivatives platforms aren’t designed for stablecoin hedging, forcing unavoidable centralization. This risk manifests in two forms: 1) inherent risks of centralized exchanges; 2) concentration risk—if a single venue handles a large portion of the protocol’s hedge, any incident there severely impacts the protocol. UXD’s suspension after Mango Markets’ attack exemplifies this extreme centralization risk.

-

Limited choice of hedging instruments. Mainstream linear perpetuals cannot perfectly hedge multi-asset long positions. Take ETH: stablecoin protocols need ETH-denominated short positions. But dominant linear perps require USDT margin and settle in USD terms, failing to perfectly offset ETH-based exposures. Even if borrowing ETH to get USDT enables hedging, it raises operational costs, complicates risk management, and reduces capital efficiency. As shown in Pika’s case, inverse perps are ideal for such protocols—but their market share remains too small.

-

Self-limiting growth at scale. Stablecoin growth requires sustained, large-scale perpetual short positions. Beyond the complexity of acquiring sufficient shorts, larger short positions increase demands on counterparty liquidity during unwinding and push funding rates more negative—raising potential hedging costs and operational difficulty. This may not matter for $10–50M scale, but becomes a clear ceiling at $100M+.

-

Operational risk. Regardless of method, hedging involves frequent operations—opening, rebalancing, collateral management—that often require human intervention, introducing operational and moral hazards.

User-Hedged Decentralized Reserve Protocols

Protocols adopting this model include Angle Protocol V1 and Liquity V2.

Angle V1

Angle Protocol launched on Ethereum in November 2021, having previously raised $5 million from a16z-led funding.

Readers can refer to Mint Ventures’ earlier report for full details. Here’s a summary:

Like other Decentralized Reserve Protocols, Angle ideally allows users to generate 1 agUSD stablecoin per $1 worth of ETH (though Angle’s first stablecoin was euro-pegged agEUR, logic remains identical—we’ll use USD for consistency). The difference is Angle targets not just typical stablecoin users but also perpetual traders, whom it calls HA (Hedging Agency).

Using our earlier example: when ETH = $2,000, a user deposits 1 ETH to mint 2,000 stablecoins. Angle then opens a leveraged position worth 1 ETH for traders. Suppose HA posts 0.2 ETH ($400) as margin to open a 5x leveraged short. Now, protocol collateral totals 1.2 ETH ($2,400), liabilities $2,000 in stablecoins.

If ETH rises to $2,200, the protocol retains only enough ETH to cover 2,000 stablecoins—0.909 ETH. The remaining 0.291 ETH ($640) can be withdrawn by HA.

If ETH drops to $1,800, the protocol must retain 1.111 ETH to cover liabilities. HA’s margin drops to 0.089 ETH ($160).

Essentially, traders are long ETH in coin terms. When ETH rises, they gain both ETH appreciation and surplus ETH from the protocol (in the example, +10% price → +60% return). When ETH falls, they lose ETH value plus part of the protocol’s collateral (−10% price → −60% loss). From Angle’s view, traders hedge the protocol’s collateral risk—hence the term "Hedging Agency." Leverage depends on the ratio between hedgeable exposure (0.2 ETH) and stablecoin liability (1 ETH).

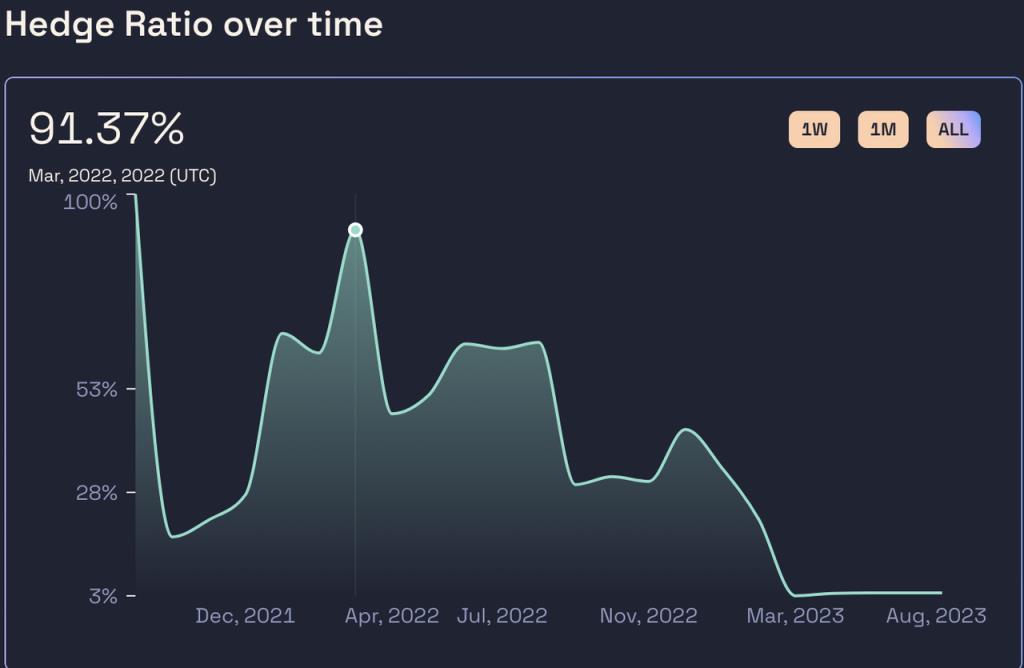

For perpetual traders, trading via Angle offers advantages: 1) no funding fees (unlike CEXs where longs pay shorts), 2) executions at oracle price with zero slippage. Angle aims for win-win: stablecoin users get high capital efficiency and decentralization; traders enjoy superior experience. But this is idealistic. Often, no traders open longs. Angle introduced Standard Liquidity Providers (SLPs) to add extra collateral (stablecoins), maintaining safety while earning interest, fees, and $ANGLE rewards.

Angle’s actual performance was poor. Despite generous $ANGLE incentives, collateral was rarely fully hedged. The core issue, in my view, is that Angle failed to offer traders a sufficiently attractive product. As $ANGLE’s price fell, TVL declined from $250 million at launch to ~$50 million.

Hedging rate of USDC pool—the main collateral source for Angle stablecoins

Source: https://analytics.angle.money/core/EUR/USDC

Source: https://defillama.com/protocol/angle

In March 2023, Angle’s yield-generating reserves were caught in Euler’s hack. Though hackers eventually returned funds, the damage was done. In May, Angle discontinued V1 and announced V2 plans. Angle Protocol V2 reverted to a traditional over-collateralized model, launching in early August.

Liquity V2

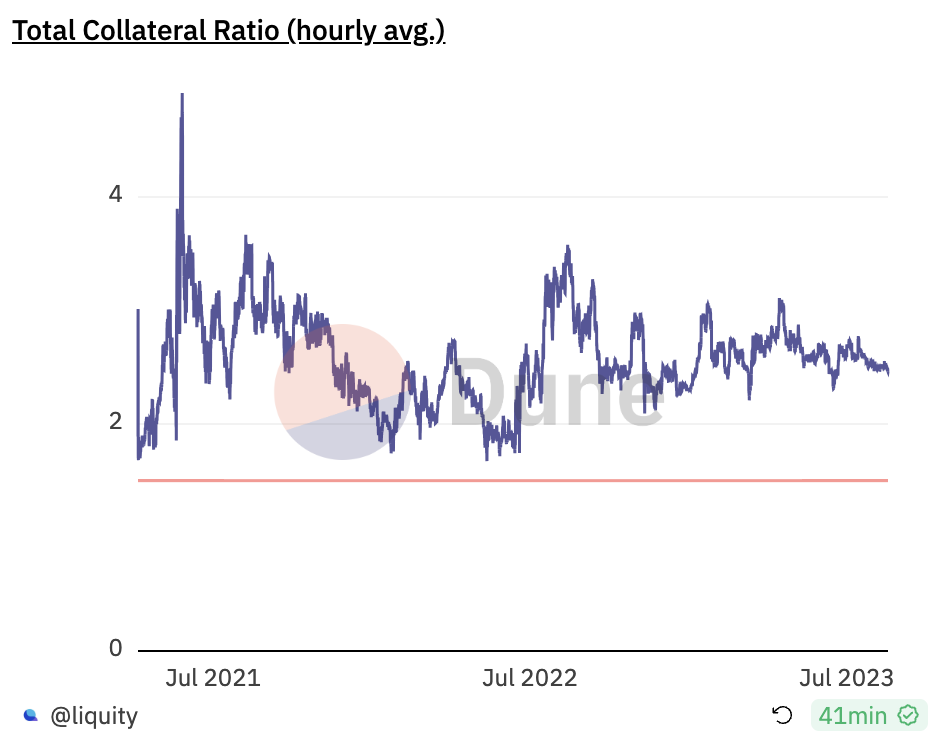

Since launching in March 2021, Liquity’s LUSD has become the third-largest decentralized stablecoin by market size (after DAI and FRAX) and the largest fully decentralized one. We previously published reports in July 2021 and April 2023, analyzing V1 mechanics and subsequent updates. Interested readers may refer there.

The Liquity team believes LUSD already excels in decentralization and price stability. However, capital efficiency remains subpar. Since launch, system collateralization has hovered around 250%, meaning each LUSD requires $2.50 worth of ETH as collateral.

Source: https://dune.com/liquity/liquity

On July 28, Liquity officially unveiled V2 features. Beyond supporting LSDs as collateral, the key announcement was achieving high capital efficiency via protocol-level delta-neutral hedging.

Liquity hasn’t released detailed product docs yet. Public information mainly comes from founder Robert Lauko’s ETHCC talk, prior blog posts, and Discord discussions. Our summary draws from these sources.

Product-wise, Liquity V2 resembles Angle V1: it aims to bring traders onto Liquity for leveraged trading, using their margin as supplementary protocol collateral to hedge risk—while offering traders compelling products.

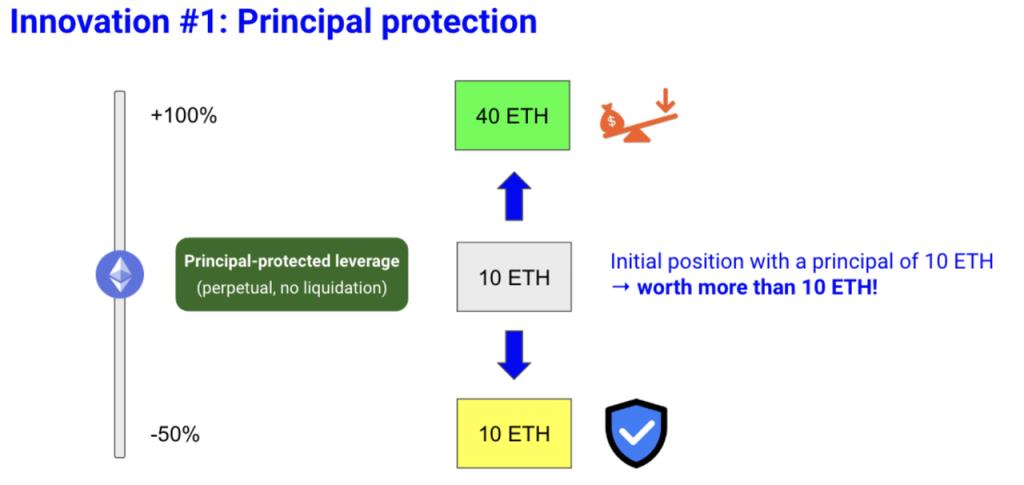

Specifically, Liquity proposes two innovations: 1) “Principal-Protected Leveraged Trading”—offering leveraged positions with downside protection. Users pay a premium to access this feature. For example, at ETH = $1,000, paying 12 ETH (10 ETH principal + 2 ETH premium) buys a 2x long with downside protection. If ETH doubles, the 2x long yields 40 ETH. If ETH falls, the put option ensures users can reclaim $10,000 (10×1,000) anytime.

Source: https://www.liquity.org/blog/introducing-liquity-v2

Clearly, Liquity’s innovation over Angle is this “principal protection.” Though implementation isn’t specified, based on product shape and Discord talks, it closely resembles a call option.

Liquity argues this hybrid product—protecting principal while offering leverage—is highly appealing to traders. Call options allow leveraged upside and downside protection—likely more attractive than Angle’s plain leverage (pricing dependent). From the protocol’s view, the premium becomes a safety buffer: during ETH declines, it supplements collateral for stablecoin redemptions; during rallies, appreciation profits can be shared with traders.

However, a clear issue exists: when traders want to close positions and withdraw ETH, Liquity faces a dilemma. Traders have every right to exit, but closing reduces hedged exposure, weakening protocol security as this “collateral” leaves. This exact issue plagued Angle’s operation—its hedging ratio remained chronically low, with traders inadequately hedging overall exposure.

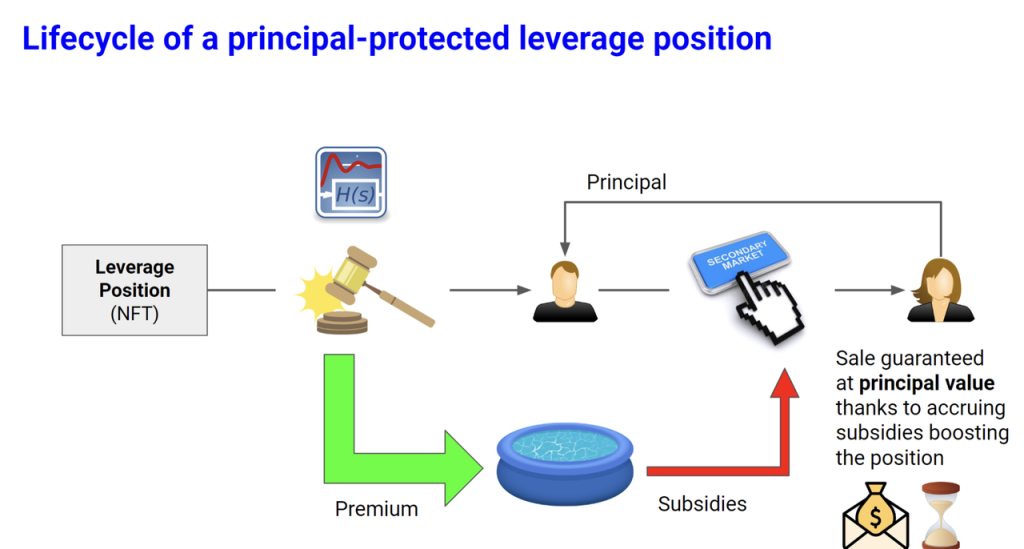

To address this, Liquity introduces a second innovation: a subsidized secondary market.

That is, leveraged positions (NFTs) within Liquity V2 can not only be opened/closed like normal trades but also sold on a secondary market. Liquity worries traders closing positions, reducing hedge ratios. If a trader wants to exit, and another trader buys the position on secondary market at a price above intrinsic value, both benefit—and Liquity preserves hedge ratio. Though Liquity subsidizes the “intrinsic value,” a small subsidy maintains system-wide hedging, enhancing security at low cost.

Source: https://www.liquity.org/blog/introducing-liquity-v2

For example, Alice opens a 10 ETH position at ETH = $1,000, paying 2 ETH premium—effectively buying 10 ETH long + principal protection. If ETH drops to $800, Alice’s 12,000U ETH is now worth only 10 ETH (8,000U). She can either close and get 10 ETH (8,000U), or sell her position on secondary market for 8,000–12,000U. For Bob, buying Alice’s position is like buying (8,000U + a call option with $1,000 strike) at $800—this option has value, so Alice’s position must trade above 8,000U. For Liquity, if Bob buys, the hedge ratio stays intact—premium remains in the pool. If no buyer appears, Liquity gradually increases the position’s value over time (mechanism unspecified—e.g., lowering strike, adding options), funded by the premium pool (slightly reducing overall over-collateralization). Liquity believes not all positions need subsidies, and subsidies won’t consume most of the value—thus a subsidized secondary market can effectively maintain hedge ratios.

Finally, even with these two innovations, extreme liquidity shortages may still occur. Liquity may fall back on mechanisms like Angle’s SLP—as a final backstop (e.g., allowing users to deposit V1 LUSD into a stability pool to support V2 LUSD redemptions in crises).

Liquity V2 is scheduled to launch in Q2 2024.

Overall, Liquity V2 shares many similarities with Angle V1 but offers targeted improvements: “principal protection” makes the product more attractive to traders; a “subsidized secondary market” protects overall hedge ratios.

However, Liquity V2, like Angle, essentially represents a stablecoin team venturing into innovative derivatives to feed back into its core business. Liquity’s expertise in stablecoins is proven, but whether it can design compelling derivatives, achieve PMF (Product-Market Fit), and execute successfully remains uncertain.

Conclusion

Decentralized Reserve Protocols that achieve decentralization, high capital efficiency, and price stability are exciting. But elegant mechanism design is only step one. More importantly, stablecoin use case expansion determines long-term success. Currently, decentralized stablecoins progress slowly in use case development. Most have only one real use case: “yield farming tool”—and farming incentives aren’t infinite.

In a way, PayPal’s PYUSD launch serves as a wake-up call for all crypto stablecoin projects—signaling big Web2 players entering the space. The window of opportunity may not last long. Indeed, when we discuss centralization risks of custodial stablecoins, we usually worry about unreliable custodians or issuers (Silicon Valley Bank was only the 16th largest U.S. bank; Tether and Circle are just “crypto-native” financial firms). But if a traditional finance “too-big-to-fail” institution (e.g., JP Morgan) launches a stablecoin, the implied national backing would instantly undermine Tether and Circle—and severely weaken the value proposition of decentralization: when centralized services are sufficiently stable and powerful, people might simply not need decentralization.

Until then, let’s hope some decentralized stablecoin gains enough use cases to reach a Schelling point—though it won’t be easy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News