friend.tech: A flowing feast in a dull bear market—what insights can this old wine in a new bottle offer?

TechFlow Selected TechFlow Selected

friend.tech: A flowing feast in a dull bear market—what insights can this old wine in a new bottle offer?

Did friend.tech change anything?

“If you are lucky enough to have lived in Paris as a young man, then wherever you go for the rest of your life it stays with you, for Paris is a moveable feast.” --- A Moveable Feast

In the world of crypto, Hemingway’s memoir might be rephrased as:

“If you are lucky enough to have lived in crypto as a young man, then wherever you go for the rest of your life speculation will follow you, for speculation is a moveable feast.”

Recently, this feast has arrived at friend.tech.

During a dull and grueling bear market, an innovative project that triggers FOMO-driven speculation easily captures all available attention.

Ponzi schemes, token airdrop expectations, fundraising rumors, and share trading—friend.tech may appear to focus on social, but at its core, it's still finance. Be honest: when people download this app, are they really doing it for socializing? Obviously not.

After all, in crypto, any social behavior not driven by economic incentives is just nonsense.

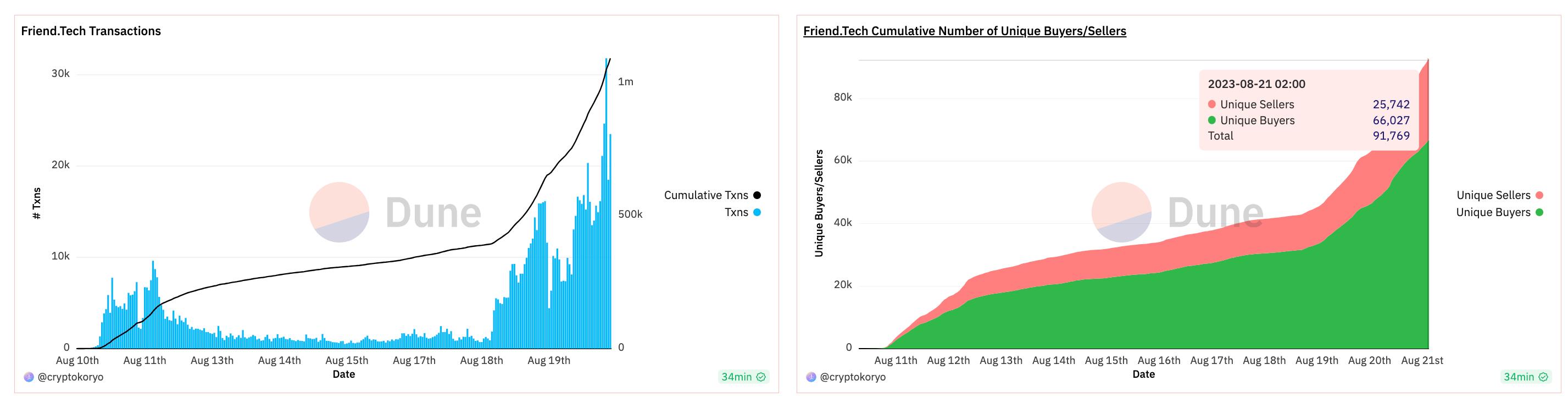

But amid this grand speculative feast, will you be one of those getting a bite? At the time of writing, total trading volume on friend.tech has surpassed 1 million, with over 66,000 unique buyers and 25,000 unique sellers...

Is it too late for me to jump in? Before asking that, it's more important to understand what it "is" and where it's headed.

The Seven Sins and Repackaged Old Tricks

Was friend.tech’s sudden rise unexpected? Yes and no.

Externally, yes—the bear market has been starved for new narratives. But more importantly, the product’s design itself plays a crucial role.

From psychological and sociological perspectives, any social (or socially disguised) product that goes viral owes much to its deep understanding of human nature. The Catholic Church’s classic seven deadly sins—pride, envy, wrath, sloth, greed, gluttony, and lust—are often exploited.

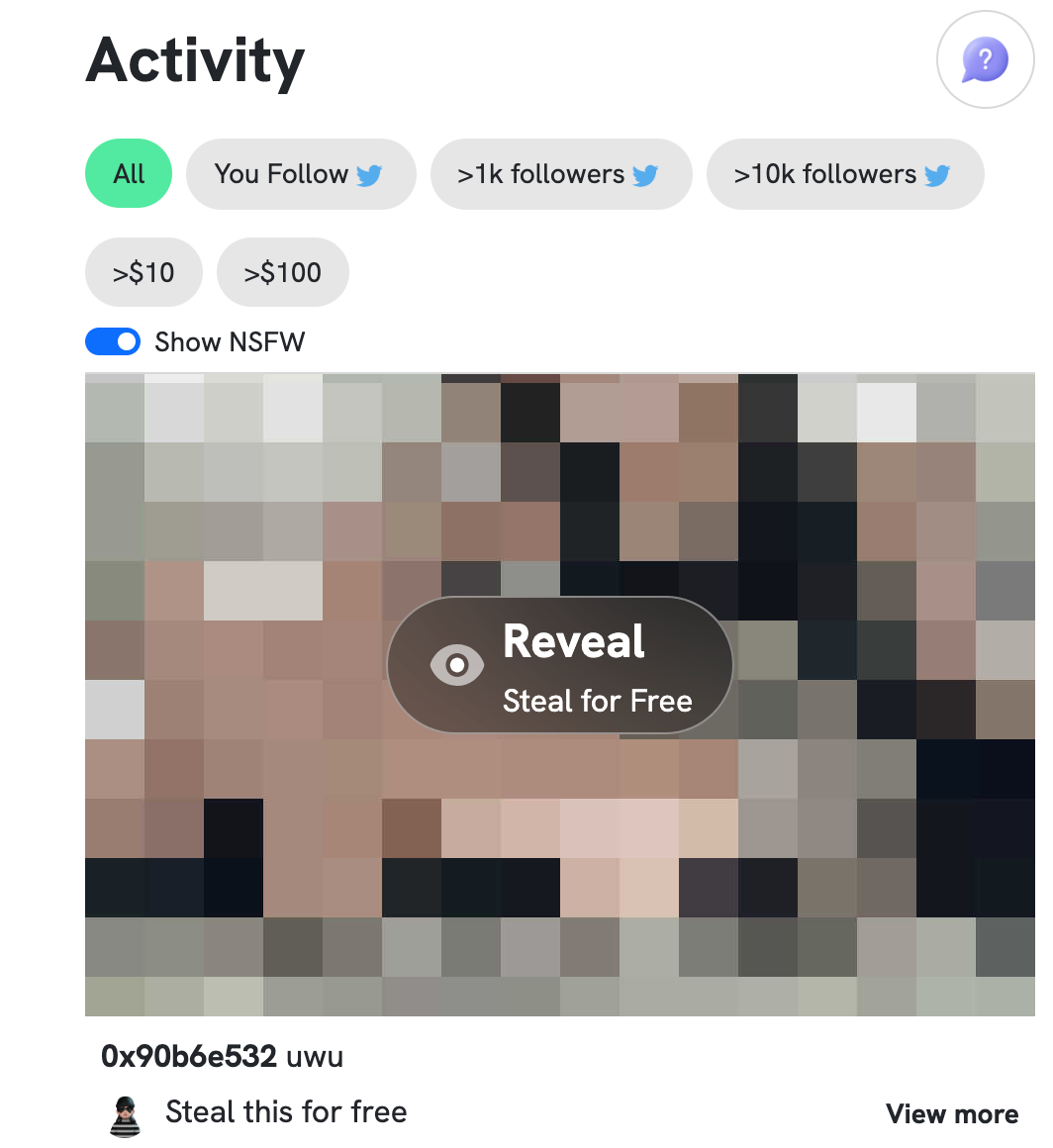

Before friend.tech, Stealcam—an image-sharing dApp on Arbitrum launched in March—already demonstrated how “lust,” or rather “voyeurism,” could be leveraged:

Users can upload an image, but it’s blurred. Others must pay ETH to “steal” and view the original. Each image can be stolen infinitely, with every subsequent steal increasing the price by 10% plus 0.001 ETH.

This “price rises with each purchase” and “payment grants access” mechanism sounds familiar—isn’t it reminiscent of buying shares on friend.tech?

Be honest—given such a design and interface, what kind of images do you think would spread most easily?

Yet Web3’s censorship resistance and fast-moving assets fueled Stealcam’s popularity. In under two weeks, without any token or airdrop, it naturally accumulated over 313 ETH in trading volume.

Human weaknesses should never be underestimated.

But is “pay-to-unblur images” really new? Of course not. Web2 social apps mastered this long ago.

Domestic QQ had “flash photos”—images visible only for seconds before deletion. Other stranger-based social apps featured similar functions like tipping to unblur images or self-destructing messages.

Similarly, friend.tech is essentially a rehash of Stealcam, tapping into “greed” instead of “lust.” But its design around launch, virality, and trading is far more refined:

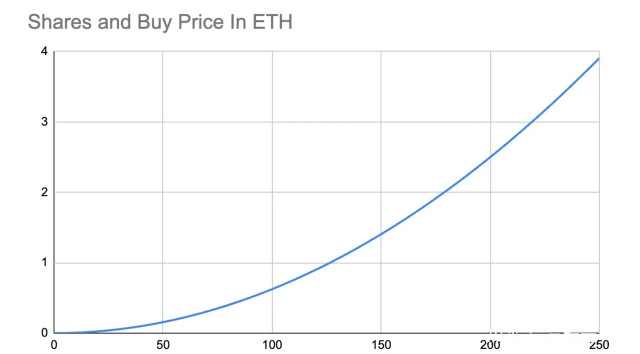

First, the trading model.

Like buying blurred images, you can directly buy shares in a user. Buying an image grants viewing rights; buying shares grants private messaging rights. Just as popular images become pricier with demand, so do shares in influential users (KOLs, gurus, alpha hunters).

But unlike Stealcam, where you need another buyer to offload your image, friend.tech has no counterparty requirement—you can sell a user’s shares anytime, regardless of liquidity. You can enter and exit freely.

Why does this exploit greed? Because:

-

Everyone agrees on who holds social influence, but not on timing. Since accounts are linked to Twitter, it's easy to spot the big players. The earlier you buy their shares, the cheaper they are—and later buyers pay more, letting early investors cash out profitably. This fuels FOMO.

-

Using the app earns free points with airdrop potential. There’s even an “Airdrop” tab explicitly telling users activity is rewarded—though currently in points, not tokens. The future utility is vague, but it plants hope—making users feel they’re “getting something for nothing.”

-

This isn’t just about farming. Social products benefit from network effects: the more people join to farm, the better the experience becomes (more KOLs, more connections), attracting even more users.

Additionally, in terms of product launch:

friend.tech directly taps into Twitter’s social graph, traffic, and influencer clout—no need to build a network from scratch. Using shares as bait, it parasitizes Twitter for distribution and user virality.

This makes users eager to share the app within their existing circles, bringing in more people whose purchases inflate their own share prices—giving them direct benefits.

Wait—doesn’t this user acquisition strategy sound familiar?

In its early days, Pinduoduo leveraged WeChat’s massive user base and pre-existing social networks, urging friends and family to “slash” prices. The more people invited, the bigger the discount—closer to getting desired items cheaply.

Did Pinduoduo succeed? Yes. Why? Because nobody dislikes a bargain—especially in lower-tier markets. Does anyone in Web3 dislike freebies? Otherwise, why would “pig feet rice” (a slang for easy gains) even exist?

Beyond viral loops, friend.tech’s business model resembles “paid subscriptions” or “knowledge monetization.” Domestic Web2 platforms like Zhihu Live and private community groups have long perfected such models.

Thus, across marketing tactics, business mechanics, and psychological insight, friend.tech is clearly repackaging old tricks—every component echoes established Web2 models and prior Web3 experiments.

Yet, Web3’s economic incentives, crypto’s speculative culture, and the buzz around Paradigm’s seed investment turned friend.tech into a rare breakout hit amid a stagnant bear market.

As the gears of fate begin to turn—can you benefit?

Risks Abound, Yet Enthusiasm Remains

The greater the FOMO, the easier it is to ignore risks.

Yu Xian, security expert at SlowMist, analyzed friend.tech’s smart contract code and found the contract owner is an EOA address. Assets in the contract have reached 2,100 ETH and continue growing (this address also receives protocol fees). If ownership is compromised, the fee could be altered, causing user losses.

Moreover, centralized private key custody is a ticking time bomb. In theory, we can only hope for proper management. But for a mature social application, leaving such vulnerabilities in place—especially involving user funds—means wider damage if things go wrong as network effects grow.

Additionally, some KOLs argue this model poses moral hazards. For example, someone might maliciously buy large shares in a KOL at peak prices, then blame or report them when prices crash.

While this may seem far-fetched, it reflects the ethical dilemma influencers face joining friend.tech: not joining means missing profits and opportunities; joining means their reputation hinges on consistently delivering valuable content—or risk being seen as a fraud when share prices fall. After all, falling share value easily correlates with personal downfall and broken trust.

But as they say, watch what people do, not what they say. From many English-speaking crypto Twitter influencers, we see that even after rationally analyzing friend.tech’s pros and cons, they still include their referral codes.

“I’ve warned about the risks, but you can still give it a try.”

After all, everyone wants profits and to try new projects. There’s no shame in that. In crypto, there are no truly risk-free ventures—many are willing to take the leap anyway.

Going all-in for outsized returns is the creed of most in the crypto world.

Ponzi Is the Passport of the Ponzi Players

Has friend.tech changed anything?

On the surface, it changes how Twitter DMs work—but in reality, perhaps nothing has changed at all.

First, current data shows that top shareholders remain established crypto figures like Cobie and Zhu Su. Existing influence and话语权 seem merely replicated onto friend.tech.

You bought shares in Cobie and Zhu Su—do you really think they’ll reply to your messages?

Moreover, the product’s structure remains Ponzi-like. Early entrants enjoy disproportionate gains, relying on newcomers agreeing on user value and buying shares—further inflating the value of shares held by early investors.

For those savvy individuals who entered over ten days ago, many likely used technical skills—writing bots, building databases of influencers, monitoring who joins friend.tech—to buy shares in high-profile users at minimal cost.

The model hasn’t changed—but enthusiasm remains undimmed.

As hype grows, more join: today, the Y Combinator president signed up; Multicoin’s co-founder publicly praised friend.tech…

Therefore, perhaps we shouldn’t seriously compare a Web3 social product like this to mature Web2 counterparts and dismiss its Ponzi nature.

Their audiences, goals, stages, and scopes differ. Rather than criticizing, selective participation may be wiser. Questioning the model, understanding it, then participating—this is likely the shared journey of every crypto native.

In the wild, first-come-first-served world of crypto, Ponzi is the passport of the Ponzi players, and caution may be the epitaph of the cautious.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News