GMX V2 Upgrade and Optimization: Focusing on Building the Underlying Architecture to Ensure Protocol Security

TechFlow Selected TechFlow Selected

GMX V2 Upgrade and Optimization: Focusing on Building the Underlying Architecture to Ensure Protocol Security

At its core, GMX V2 places greater emphasis on protocol architecture, security, and balance.

Author: duoduo, LD Capital

GMX V2 officially launched on August 4, 2023. This article reviews the development and issues of GMX V1, compares the changes in V2, and analyzes their potential impacts.

I. GMX V1: An Effective Model for Derivatives DEX Protocols

Launched at the end of 2021, GMX V1 adopted the GLP model, providing a simple and effective trading mechanism that pioneered the concept of "real yield" and established a significant position among derivatives DEX protocols. Numerous projects have forked the GMX V1 model.

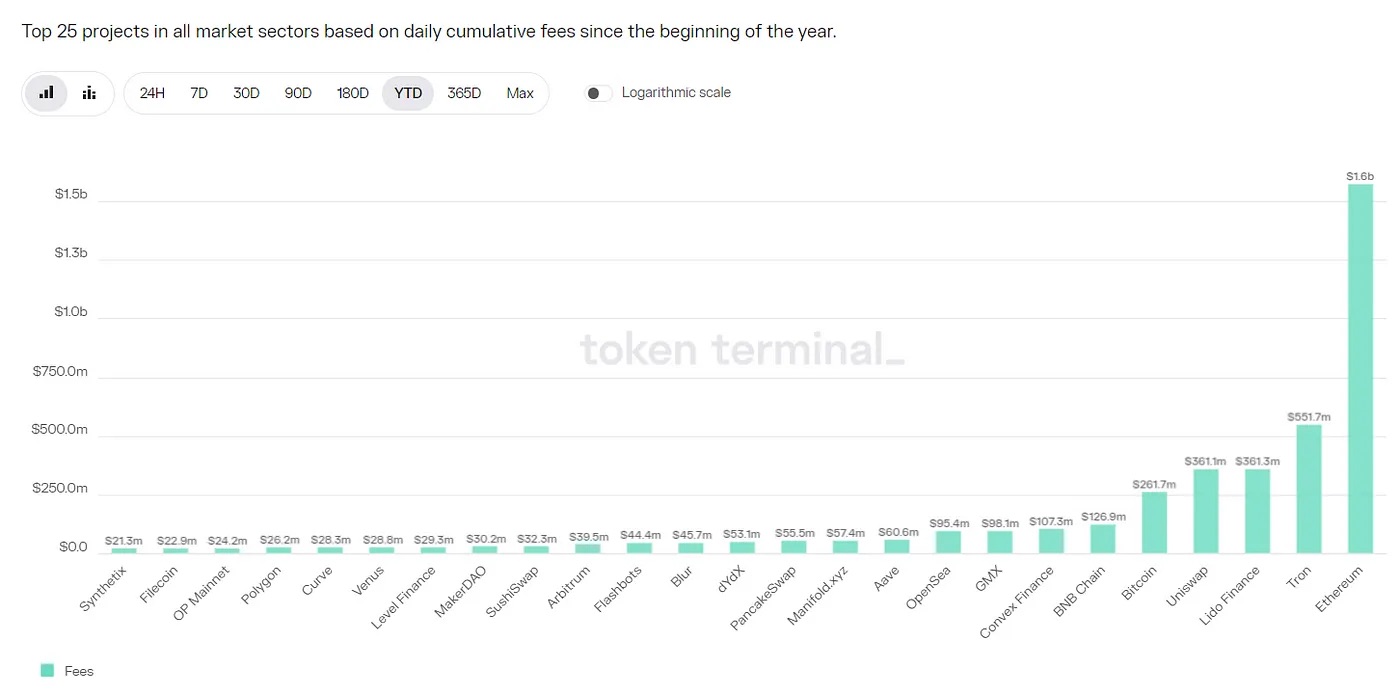

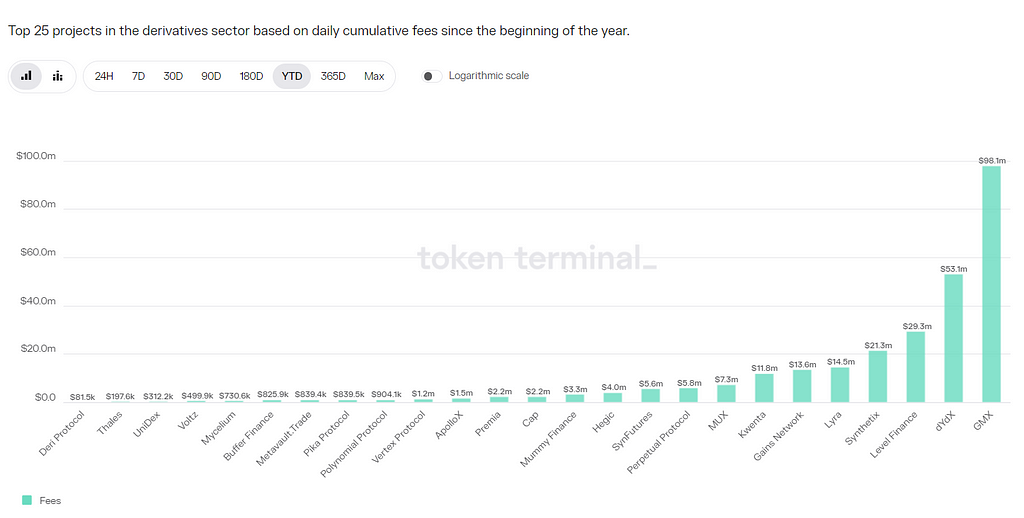

GMX V1 has captured substantial fees. Since 2023, GMX V1's protocol revenue has reached $98.1 million, ranking eighth overall and first among derivatives DEX protocols.

Source:token terminal

However, GMX V1 also has limitations, including:

1. Imbalanced open interest (OI) exposes liquidity providers (LPs) to significant risk

GMX V1 charges opening/closing fees and borrowing fees but does not include funding rates. Borrowing costs create holding expenses, preventing infinite liquidity consumption. Additionally, the dominant side pays higher fees. However, since both long and short positions incur fees without arbitrage opportunities, imbalanced open interest cannot be quickly corrected through arbitrage.

If left unaddressed, extreme imbalances could lead to massive losses for the GLP pool, resulting in losses for LPs and potentially causing protocol collapse.

2. Limited tradable assets

GMX V1 supports only five tradable assets: BTC, ETH, UNI, LINK, and AVAX. In contrast, DYDX and Synthetix offer dozens of trading pairs. Gains provides forex instruments, while newer platforms like HMX offer commodities and U.S. stock derivatives.

3. High fees for small and medium-sized traders

GMX V1 charges 0.1% for both opening and closing positions, which is relatively high. Amid increasing competition in the derivatives DEX space, many protocols now charge below 0.05%.

II. GMX V2: Enhancing Protocol Security and Balance

1. Core objectives

The core goal of GMX V2 is to enhance protocol security and balance by modifying fee mechanisms to maintain equilibrium between long and short positions, thereby reducing systemic risks during volatile market conditions. Through isolated pools, it enables the addition of high-risk trading assets while controlling overall risk exposure. By partnering with Chainlink, GMX V2 delivers more timely and reliable oracle services, minimizing price manipulation risks. The team has also considered relationships among traders, liquidity providers, GMX token holders, and sustainable project development, adjusting and balancing protocol revenue distribution accordingly.

2. Fee structure adjustments: Introduction of funding rates and price impact fees

GMX V2 significantly revised its fee model, focusing on promoting balanced long/short positions and improving capital efficiency. Key changes include:

Reduced opening and closing fees—from the previous 0.1% to either 0.05% or 0.07%, depending on whether the trade contributes to balance. Trades that improve balance are charged lower fees.

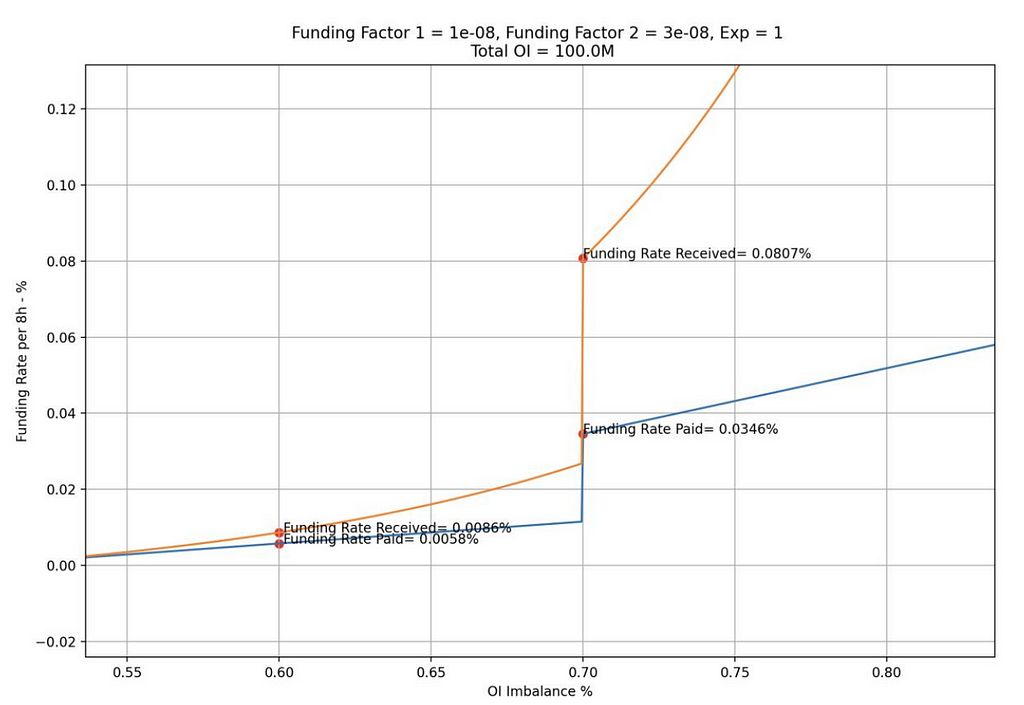

Introduced funding rates—charged from the stronger side to the weaker side.

Funding rates are tiered: when the dominant side’s position ranges between 0.5–0.7 of total open interest, rates remain low; once exceeding 0.7, rates increase significantly, creating larger arbitrage incentives to restore balance.

Source:chaos labs

Retained borrowing fees to prevent infinite liquidity usage.

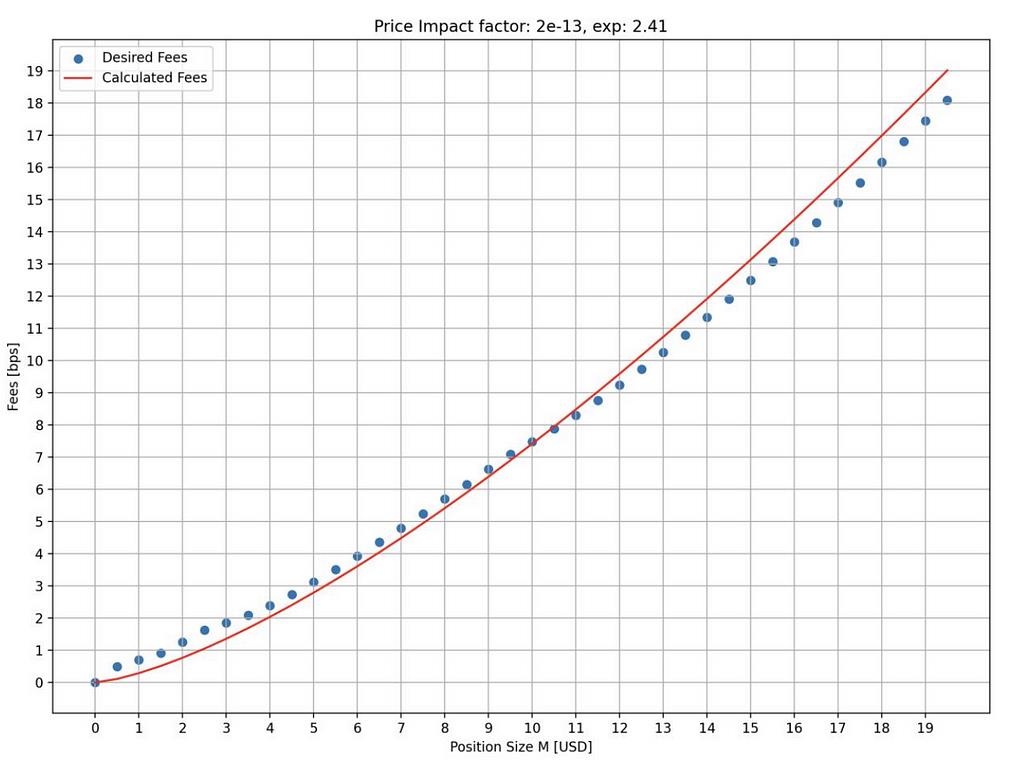

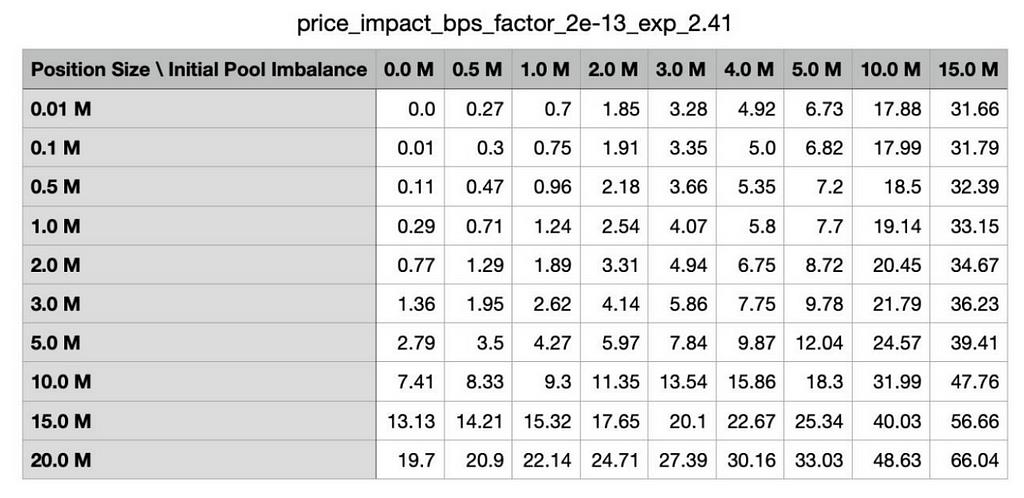

Introduced price impact fees—larger positions and those worsening imbalance incur higher fees.

Price impact fees simulate dynamic price movements in order-book markets—larger positions cause greater price impact. This design increases the cost of price manipulation, reduces attack risks, prevents flash crashes or spikes, maintains balanced long/short exposure, and sustains healthy liquidity.

The chart below shows simulated price impact fees under different position sizes—clearly demonstrating that larger positions face higher fees. The x-axis represents position size (in millions USD), and the y-axis represents fee rate (in bps).

Source:chaos labs

Additionally, fees increase if a new position worsens existing imbalance. The table below illustrates fee levels under various simulated scenarios. The first column indicates position size, and the first row shows initial pool imbalance.

Source:chaos labs

A brief comparison of fees across major derivatives DEX protocols:

-

DYDX: maker 0.02%, taker 0.05%; larger volumes receive bigger discounts;

-

Kwenta: maker 0.02%, taker 0.06%-0.1%;

-

Gains Network: 0.08% opening/closing fee + 0.04% spread + price impact fee.

Overall, GMX V2 fees remain relatively high but have decreased from previously high levels to moderate. Opening/closing fees have dropped nearly 50%, making V2 more favorable for small and medium-sized traders.

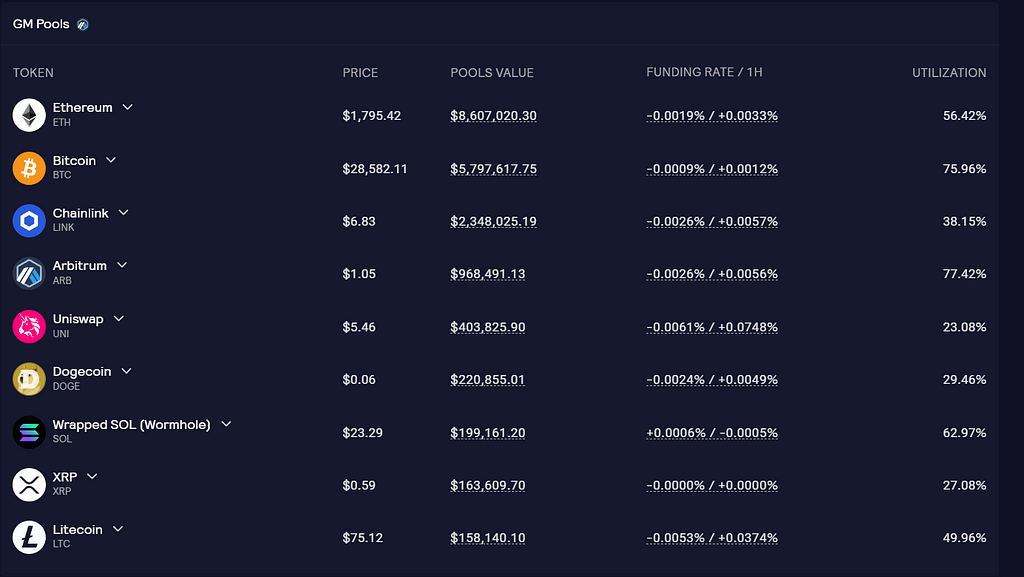

3. Liquidity provision: Introduction of isolated pools and synthetic assets

GMX V2 uses isolated liquidity pools called GM Pools, each operating independently. Users can view each pool’s funds, funding rates, and utilization rates on the official website.

Source:GMX

The advantage of isolated pools is that different token markets can have distinct underlying assets and parameter settings, enabling independent risk control with greater flexibility—expanding tradable assets while managing risk. LPs can choose exposure based on their risk tolerance and return expectations. A downside is fragmented liquidity—some pools may struggle to attract sufficient capital.

Currently, GMX V2 divides markets into three categories:

-

Blue-chip: BTC and ETH. These tokens are less prone to price manipulation, allowing lower price impact fees—making them more competitive than CEXs. Both use native tokens as backing.

-

Mid-cap assets: Tokens with market caps between $1B and $10B, having strong liquidity and volume on CEXs but susceptible to external shocks (e.g., regulatory news). For these, price impact fees are set higher, liquidity capped below external markets to raise attack costs. LINK, UNI, AVAX, ARB, and SOL fall into this category. Native tokens serve as backing.

-

Mid-cap synthetic assets: Not backed by native tokens but using ETH as underlying liquidity. DOGE and LTC belong here.

A key issue with these assets is that if the underlying token surges sharply, the ETH in the pool might not cover all payouts.

For example, suppose a pool holds 1,000 ETH and 1 million USDC, with a maximum DOGE long position capped at 300 ETH. If DOGE’s price increases tenfold while ETH only doubles, profits could exceed the value of ETH in the pool.

To mitigate this, GMX V2 introduces ADL (Auto-Deleveraging). When unrealized profits exceed predefined thresholds, profitable positions may be partially or fully closed. This ensures market solvency and full profit settlement upon closure. However, for traders, ADL may result in losing winning positions prematurely, missing out on future gains.

According to Chaos Labs’ report, suggested OI caps during initial V2 operation are $256 million each for BTC and ETH, $4 million each for AVAX and LINK, and $1 million for other tokens. These can be adjusted based on performance. Currently, total GM Pool TVL is around $20 million—still far below limits.

4. Enhanced user experience: Introduction of coin-margined contracts, faster execution, and lower slippage

In GMX V1, traders could only open USD-margined contracts. Regardless of collateral used, position values were calculated in USD at entry, with profit defined as exit USD value minus entry USD value.

GMX V2 adds coin-margined contracts. Traders can now deposit the relevant trading asset as collateral without USD conversion, meeting diverse needs and enabling richer portfolio strategies.

Additionally, GMX V2’s oracle system prices every block, executing orders as close as possible to the latest price—resulting in faster execution and lower slippage.

5. Revenue distribution model

To support long-term sustainability, GMX V2 adjusts its revenue distribution, allocating 8.2% to the protocol treasury for operations and development.

-

GMX V1: 30% to GMX stakers, 70% to GLP providers.

-

GMX V2: 27% to GMX stakers, 63% to GLP providers, 8.2% to the protocol treasury, and 1.2% to Chainlink. This allocation has been approved via community vote.

III. GMX V2 Operational Status

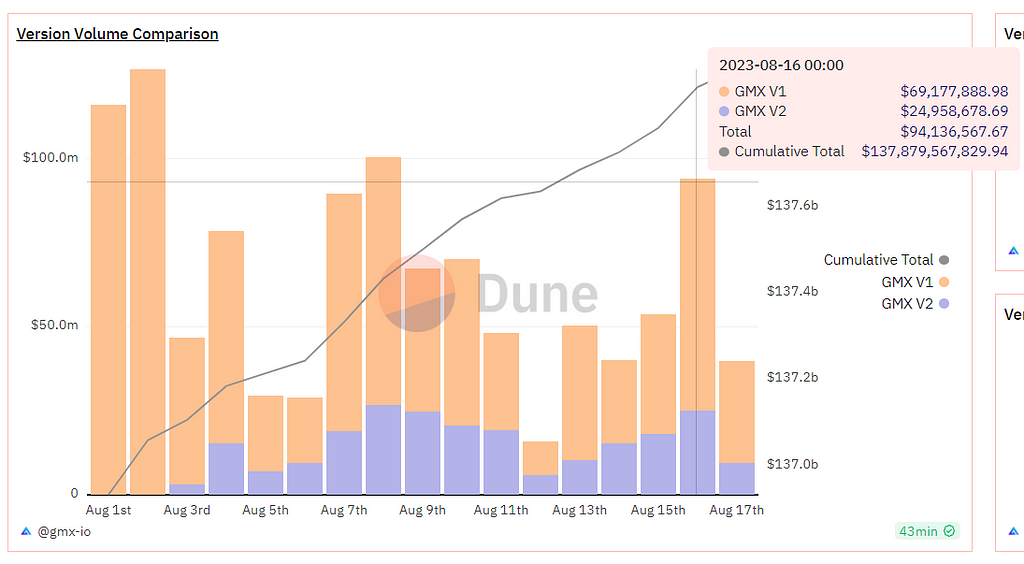

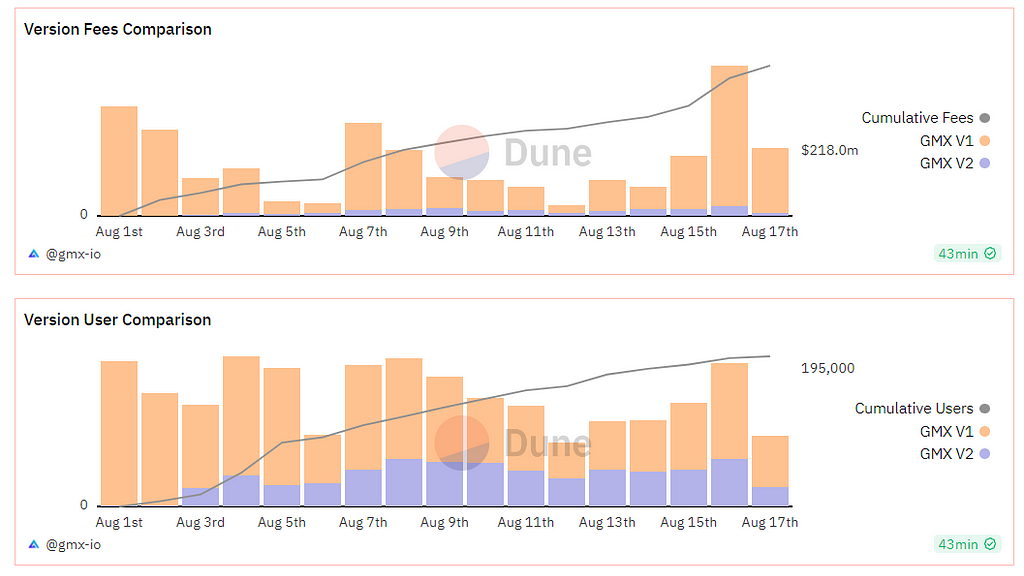

After approximately two weeks of operation, GMX V2 has achieved ~$20 million TVL, ~$23 million average daily trading volume, ~$15,000 daily protocol revenue, $10.38 million open interest, and 300–500 daily active users. Given no trading incentives have been deployed, this is a reasonable start.

Some V1 users have migrated to V2. V2’s trading volume and daily active users represent roughly 40%-50% of V1’s levels. Below charts compare V1 and V2 metrics:

Source:dune

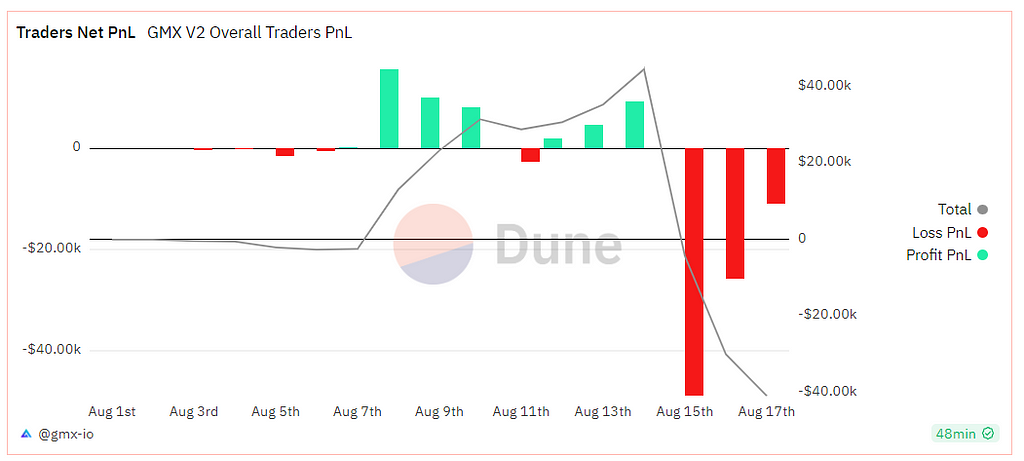

GMX V2 traders are currently net losers, with cumulative net losses reaching $40,000.

Source:dune

In terms of returns, GMX V1 yields have remained low recently: weekly staking yield for GMX is 1.44%, GLP (Arbitrum) is 3.18%, and GLP (Avalanche) is 8.09%. In contrast, GMX V2 offers higher returns, as shown below:

Source:GMX

Since launch, market enthusiasm for GMX V2 has been muted, with limited capital response. Primary reasons include historically low market volatility, shrinking overall trading volume, intense competition within the sector, and stagnant protocol revenue growth.

IV. Conclusion

GMX V1 is a successful model in the derivatives DEX space, widely emulated. GMX V2 largely meets market expectations, reflecting the team’s strong protocol design capabilities. Mechanically, V2 improves liquidity pool balance, expands tradable asset types, and offers multiple collateral options. For LPs and traders alike, investment methods are more diversified, risk management is improved, and fees are reduced.

However, in its early stage, the use of isolated pools leads to liquidity fragmentation, potentially leaving some assets undercapitalized. Moreover, the GMX team has undertaken minimal marketing or incentive campaigns, resulting in no significant boost to new users or trading volume in the short term.

At its core, GMX V2 prioritizes protocol architecture, security, and balance. In the current bear market, focusing on foundational infrastructure, ensuring safety, and leveraging accumulated data for better risk parameter design may better position the project for success in the next bull cycle. Then, it can support higher open interest capacity, broader markets, and launch aggressive marketing initiatives to attract more users.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News