DeFi in the Real World: Unlocking Global Financial Potential

TechFlow Selected TechFlow Selected

DeFi in the Real World: Unlocking Global Financial Potential

The real-world DeFi has matured and is now迎来ing an opportunity for disruption.

Authors: tzedonn, Michiel Lescrauwaet, Nicolas Priem, Tioga Capital

Translation: Block unicorn

If software is eating the world, then crypto is eating capital markets.

Tokenization is not a new concept—startups, banks, and stock exchanges have been exploring it since before 2017. However, the current moment presents an unprecedented opportunity for mass adoption. With stablecoins having proven their effectiveness as a medium of exchange and DeFi infrastructure demonstrating its reliability after DeFi Summer in 2020, we are on the verge of a massive on-chain inflow of real-world assets.

In Web3, RWA refers to tokenized real-world assets such as equity, debt, and real estate. Do not confuse this with "RWA" in traditional finance, which stands for "risk-weighted assets."

Currently, stablecoins account for 0.7% of the U.S. M1 money supply (approximately $130 billion), compared to a total M1 supply of $18.6 trillion, peaking at around 1.0%. For comparison, Tesla currently holds a 0.63% market share in the U.S. automotive market.

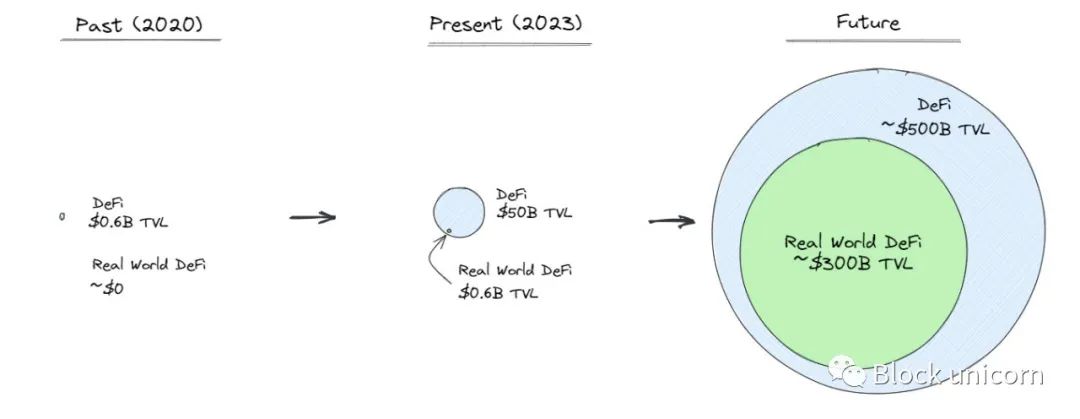

Meanwhile, DeFi’s total value locked (TVL) has surged from just $6 billion in 2020 to approximately $50 billion today—an astonishing 80-fold increase. This remarkable growth outpaces even Ethereum’s 8x price appreciation over the same period.

During the 2022 market turmoil, centralized finance (CeFi) platforms such as FTX, Celsius, BlockFi, and Voyager Digital collapsed, while DeFi demonstrated strong resilience. DeFi protocols—including Aave, Compound, Uniswap, and MakerDAO—operated seamlessly around the clock, proving that DeFi worked exceptionally well.

Therefore, we are now poised for an era of bringing traditional financial assets on-chain. As DeFi evolves, we expect “real-world DeFi” to capture an increasing share of the DeFi ecosystem.

Three Arguments for Real-World DeFi

1. Real-world DeFi enables you to unlock all financial assets and use them as collateral across any DeFi application

In traditional finance (TradFi), obtaining a loan secured by equity is a lengthy and cumbersome process involving multiple parties. It starts with your equity custodian sending a PDF file to a bank to verify that you own the asset in their siloed database. Then, the bank secures your loan, the custodian transfers your equity to the bank, and you receive a cash transfer. Finally, loan terms are manually reviewed to check for violations—all taking several days.

These high operational requirements and costs mean such services are typically only available from banks to high-net-worth clients.

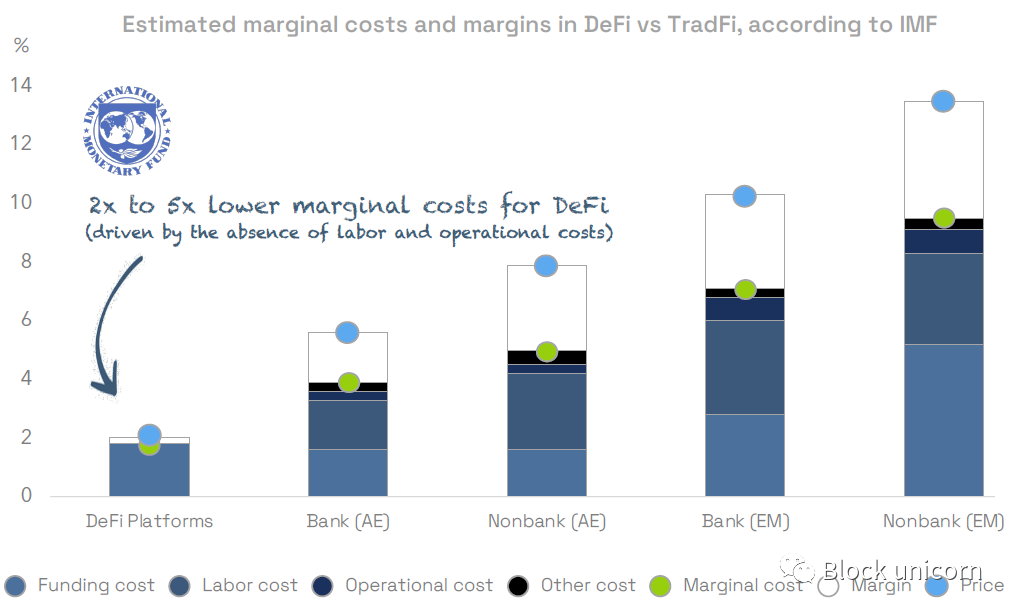

More broadly, the IMF estimates that DeFi platforms reduce marginal costs by about 2x compared to banks and non-bank institutions in advanced economies, and by about 4–5x compared to emerging markets.

In real-world DeFi, this process takes only seconds. You press a few buttons, your equity tokens are cryptographically verified on a public blockchain, pledged via smart contracts, and the transaction settles instantly. You immediately receive digital cash (stablecoins), and loan terms are enforced through code.

It goes further: in a world where individuals can control all their tokenized assets (fiat, equities, real estate, art, etc.) through a wallet, this unlocks diverse potential collateral, improves liquidity through global and 24/7 trading, enables automated portfolio management, and more.

Take PV01 (a Tioga portfolio company) as an example—they are developing bearer bonds issued on-chain. These bearer bonds will be natively composable on the blockchain, allowing users to easily use them as collateral.

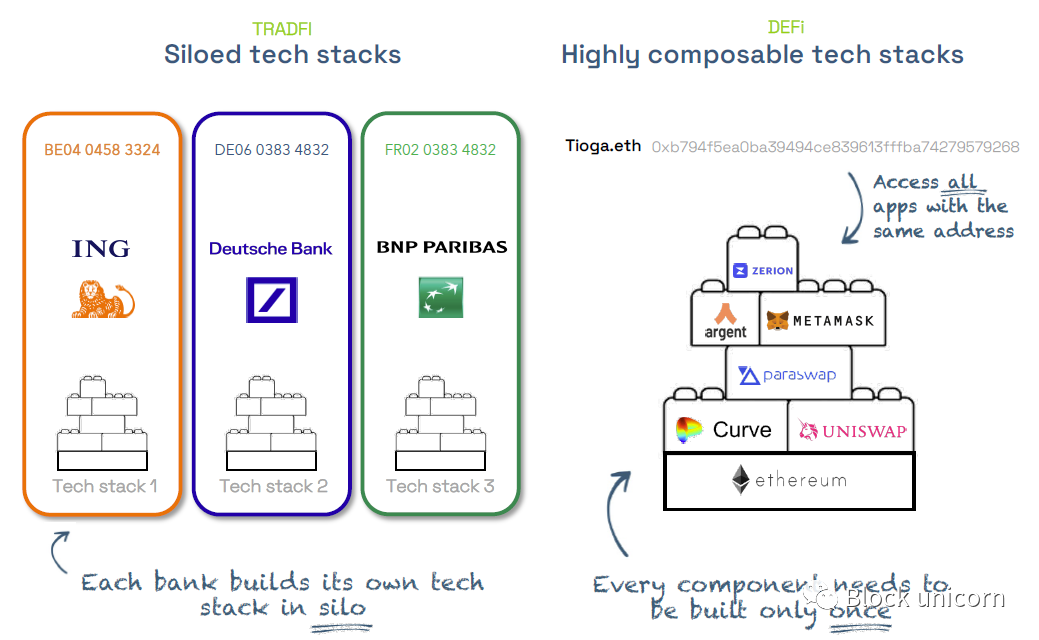

From an entrepreneur's perspective, DeFi allows developers to access a global customer base from day one. Founders can also leverage existing DeFi infrastructure, which is essentially a native open API. For users, low switching costs drive competition among entrepreneurs, accelerating the development of the best possible products.

Consider this: as interest rates rose, ING Bank’s profits nearly quadrupled, yet they continue paying depositors only 0.75%, while euro government bonds yield 3.4%. This remains highly profitable for ING due to high switching costs. Banks are sticky and tend to offer the best rates only to their wealthiest clients.

DeFi offers an alternative: you can switch between services with a single click, without restrictions. Moreover, DeFi clearly distinguishes between cash (no credit risk) and savings accounts, ensuring private losses caused by excessive bank risk-taking do not get socialized afterward.

Despite TradFi’s siloed tech stacks, entrepreneurs can build atop DeFi’s natively interoperable infrastructure.

2. Real-world DeFi provides universal access to financial products

Today, anyone can launch their own private credit fund by leveraging efficiency gains from DeFi applications like Maple or Atlendis (both Tioga portfolio companies) running on blockchain.

For established players like Blackstone (with ~35% operating margins) that already benefit from economies of scale, these back-end cost savings may seem small. But emerging private credit funds can leverage DeFi infrastructure to boost operating margins from ~20% to 35–40%.

In Jeff Bezos’ words: “The profit margin of traditional finance is the opportunity for DeFi.”

If you’re in Argentina, you no longer need to wait for banks to “support USD” or allow purchases at the “official exchange rate” amid rapid peso depreciation. You can simply deposit any tokenized currency (e.g., USDC) directly into your wallet.

Banks and brokers can no longer act as gatekeepers to financial products because consumers are no longer confined within their systems. Instead, they can access a broad range of tokenized financial products and make independent decisions.

Real-world DeFi allows you to find the best yields across DeFi thanks to native composability and universal asset verifiability. Unlike the past, where you had to open accounts at each bank and use separate systems to apply for loans or buy financial products, now anyone with internet access can obtain any financial product.

3. Self-custody reduces counterparty risk; transparency enhances risk management

Self-custody acts as a safeguard against counterparty risk. Although self-custody may still seem daunting today, account abstraction, social recovery, and hybrid recovery methods will soon make the experience no different from logging into a traditional bank.

When Silicon Valley Bank faced a banking crisis (similar to Lehman Brothers in 2008), there was almost zero transparency. No one truly knew whether they were solvent—the risks could not be monitored, let alone externally verified.

Today, if Silicon Valley Bank operated on a blockchain, we would have full transparency into its assets and liabilities. We could create Dune dashboards to “watch the chain.” We could also monitor liquidity using risk management suites like Chaos Labs (a Tioga portfolio company).

The collapse of Terra is a perfect example. When Luna’s price dropped, Anchor Protocol experienced a bank run. In 2008 during Lehman’s collapse, we were kept in the dark—but today, we have minute-by-minute on-chain transparency, accessible equally to retail and institutional users alike, enabling optimal decision-making. But where exactly are we on the adoption curve today?

The Trojan Horse of RWA DeFi—Private Credit and Government Bonds

In early 2020, DeFi’s TVL was around $600 million before surging past $150 billion. Today, DeFi TVL hovers around $50 billion.

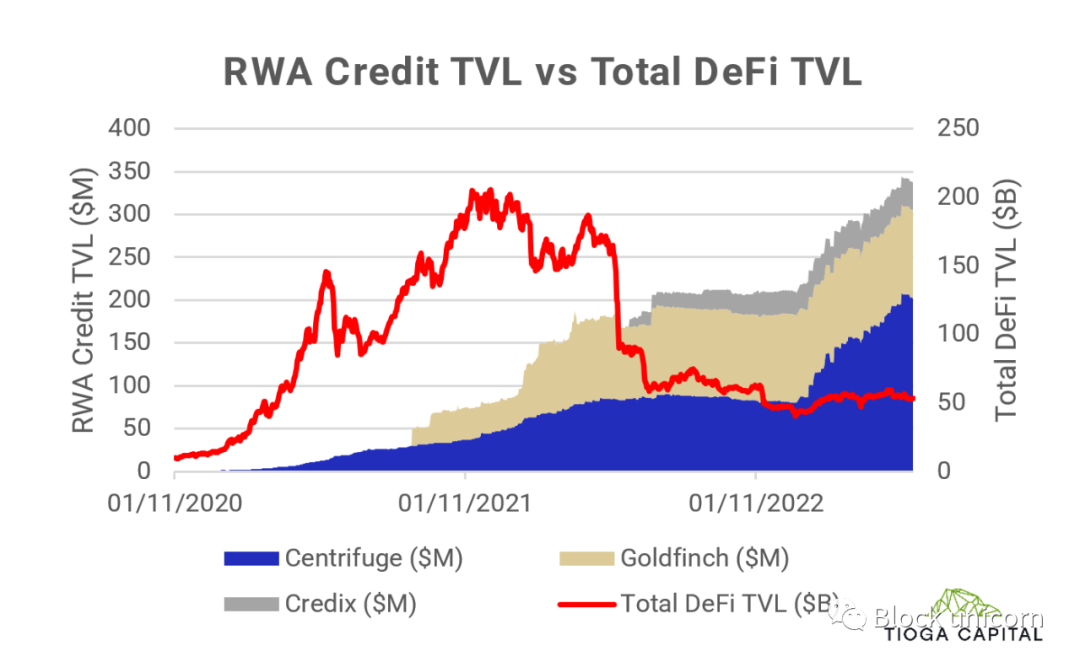

DeFi in 2020 is what on-chain real-world assets (RWA DeFi) are today. Currently, RWA DeFi has reached an all-time high TVL of $600 million—$340 million from private credit and $260 million from on-chain government bonds.

DeFi took off thanks to a unique confluence: liquidity fueled by COVID stimulus checks, time for experimentation during lockdowns, and new cryptographic primitives (like AMMs and liquidity mining) ready for alpha testing.

We believe today’s $50 billion DeFi TVL provides strong evidence that DeFi can serve as the blueprint for the next paradigm shift in finance.

The steady growth of RWA credit, decoupled from crypto price volatility, shows that blockchain technology does not need to be used solely for speculation—it can simply function as a technology for value transfer. Hence the term “internet money”: for the first time, we can transmit self-sovereign value over the internet.

Centrifuge is a pioneer in RWAs, having closely collaborated with MakerDAO since 2020 to fund RWAs in areas such as trade finance, structured credit products, revenue-based financing, and emerging market credit. Goldfinch and Credix focus primarily on emerging market credit in Latin America, Africa, and Southeast Asia.

Meanwhile, many other credit protocols have launched, targeting credit in Africa and Southeast Asia—such as Atlendis (a Tioga portfolio company), Bluejay Finance, and Jia.

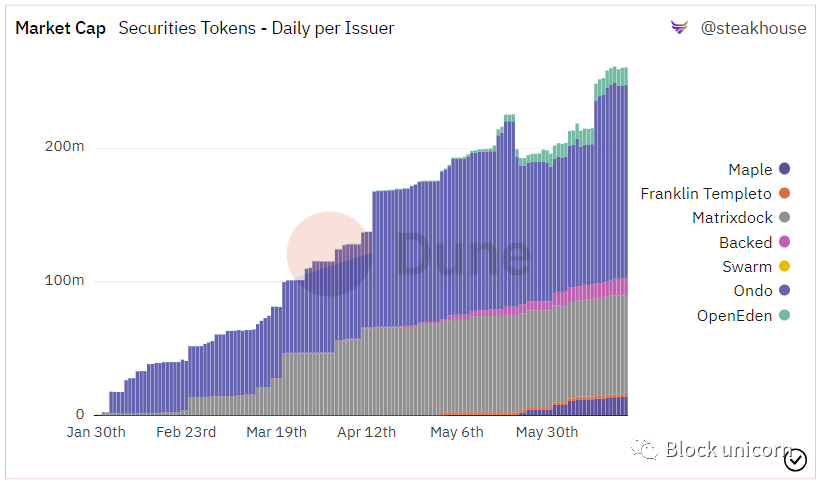

Recently, tokenized government bonds have emerged as another rapidly growing asset class. In the first half of 2023, several new protocols entered the space, including Ondo Finance, Matrixdock, Backed Finance, Swarm Markets, Franklin Templeton’s Benji app, OpenEden, and Maple’s cash management pools.

This momentum is driven by a powerful force: approximately $135 billion in on-chain stablecoin capital may be seeking a more efficient way to access risk-free yields from traditional finance—without enduring complex off-ramping processes—fueling explosive growth in the government bond sector.

Tokenized government bonds grew from zero to a $260 million asset class in just five months (Source: Steakhouse Finance on Dune)

One might question the rationale for using tokenized government bonds—if I’m a high-net-worth individual, can’t I already buy them through traditional brokers? The answer lies in two subtle distinctions.

First, tokenized government bonds are not designed for average users (though they allow anyone to purchase bonds from any country), but rather serve high-net-worth individuals (HNWIs), traders, or hedge funds who prefer to avoid the frictional costs of moving between on-chain and off-chain worlds.

Tokenized government bonds are also beneficial for DAOs and startup treasuries—especially those outside the U.S.—and for DeFi protocols requiring permissionless composability with RWAs.

For instance, Ribbon Finance recently placed a $2 million order for Backed’s tokenized government bonds to use generated yields for purchasing ETH options. Meanwhile, Angle Protocol is working on a proposal to use Backed tokens as collateral for their euro stablecoin.

Second, for many legacy institutions, government bonds serve as a strategic entry point. Due to current interest rate arbitrage between DeFi and CeFi, they demonstrate the technical and legal feasibility of tokenized assets.

In essence, tokenized government bonds may serve as the “Trojan horse” to bring traditional bonds and other financial assets on-chain.

Conclusion

Real-world DeFi has matured and is ripe for disruption.

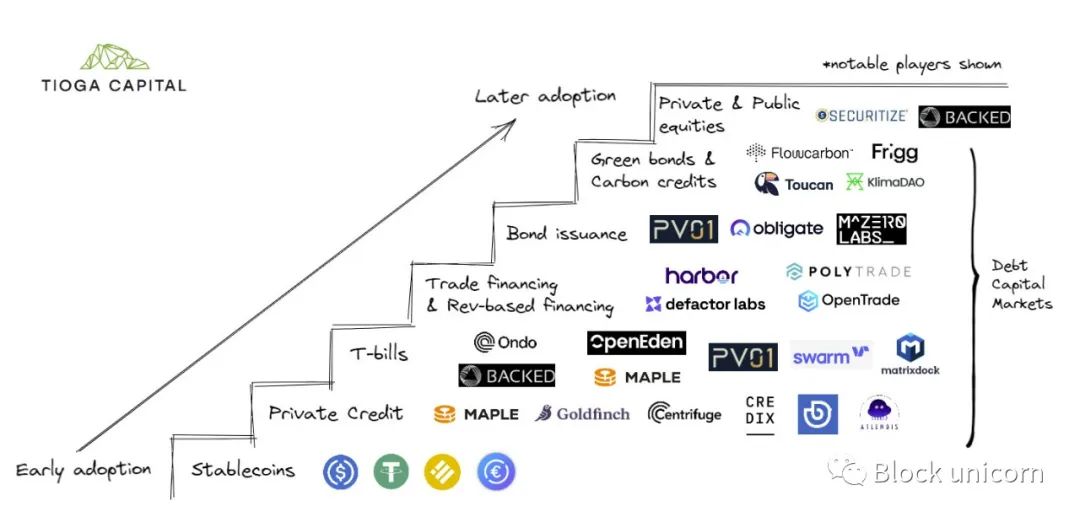

The real-world DeFi space is still in its infancy, but early signs of product-market fit are emerging. We observe adopters beginning with low-risk yield opportunities (government bonds) using on-chain capital (crypto-native users, non-U.S. crypto firms, unbanked populations), then gradually progressing toward higher-risk assets (trade finance, bonds, private credit).

Next, we expect capital from traditional finance to be drawn in by the unique capabilities of blockchain technology—such as collateralizing fully tokenized assets, improved liquidity and capital management, and access to novel investment products (e.g., bond issuance). Finally, institutions will join as efficiency gains and demand grow for blockchain-based services offered to customers.

Gradient overview of real-world DeFi adoption trends

Real-world DeFi remains in its early stages. Beyond tokenizing real-world assets, significant improvements in blockchain scalability, privacy, and security are still needed before reaching a tipping point in DeFi adoption.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News