A New Chapter for DeFi: Unlocking Value through Staking Yields and Real-World Assets

TechFlow Selected TechFlow Selected

A New Chapter for DeFi: Unlocking Value through Staking Yields and Real-World Assets

Do you think LSD and RWA could be the future of DeFi?

Author | Day

Produced by|Baicai Blockchain (ID: hellobtc)

Since the DeFi Summer of 2020, despite significant progress and the emergence of various infrastructure components over the years, traditional DeFi blue-chip tokens such as UNI, LINK, AAVE, and SNX have performed extremely poorly since peaking in May 2021. They seem to be gradually fading from market attention—an awkward fate that once again confirms the crypto industry’s tendency toward “loving the new and discarding the old.”

Recently, the term "outdated DeFi blue chips" has even surfaced within the community. Readers have become numb to DeFi topics; any article with “DeFi” in the headline is unlikely to attract high readership, and some people don’t even bother reading them anymore—after all, without short-term investment potential, how many will truly care about technical discussions?

On the other hand, it's undeniable that DeFi (decentralized finance)—which builds financial systems using blockchain technology instead of relying on outdated, inefficient traditional infrastructures to provide services like trading and lending of crypto assets—has long become an indispensable part of the blockchain industry. Recently, established DeFi blue chips like UNI and MKR have been increasingly active. This article aims to briefly trace the evolution from DeFi 1.0 to DeFi 3.0 and highlight innovations at each stage.

01 DeFi 1.0: Building the Foundational Framework

DeFi 1.0 marks the early phase of decentralized finance, primarily focused on establishing the foundational framework for financial services on blockchains, introducing several key concepts, including stablecoins, AMM-based DEXs, lending/borrowing platforms, liquidity incentives, and incentive-driven staking.

-

Key developments and innovations during the DeFi 1.0 era:

The rise of stablecoins such as Tether (USDT), USD Coin (USDC), and DAI provided a reliable medium of value exchange, forming the foundation for trading and lending activities within the DeFi ecosystem.

The emergence of Automated Market Makers (AMMs) and liquidity incentives powered decentralized exchanges (DEXs) like Uniswap and Curve, enabling peer-to-peer transactions without intermediaries.

The appearance of lending platforms such as Aave and Compound allowed users to earn interest on their crypto holdings or borrow against their digital assets as collateral.

The introduction of incentive-based staking rewarded users with governance tokens for providing liquidity to DeFi protocols, acting as a major catalyst for growth and driving Total Value Locked (TVL) from hundreds of millions to tens of billions of dollars.

While DeFi 1.0 laid the essential groundwork for the future development of decentralized finance, it also came with its share of challenges.

Most DeFi 1.0 activity was concentrated on Ethereum, where scalability issues led to high user participation costs. Moreover, although incentive-based liquidity proved highly effective initially, liquidity providers were primarily motivated by rewards rather than loyalty. Once incentives were removed, users would leave, leading to price drops and potentially sending projects into a death spiral.

Additionally, liquidity providers faced impermanent loss risks when token prices fluctuated significantly. Liquidity was fragmented across different platforms, and locking capital to provide liquidity reduced overall capital efficiency.

Despite these shortcomings, DeFi 1.0 projects laid the foundation for today’s DeFi landscape and pointed the way forward, inspiring teams to overcome these obstacles and push the ecosystem further.

02 DeFi 2.0: Product Diversification and Improved Capital Efficiency

DeFi 2.0 emerged to address the limitations of DeFi 1.0 while expanding functionality.

-

Notable developments and innovations in DeFi 2.0 include:

A surge in DeFi protocol forks on alternative blockchains like BSC, Solana, and Fantom, alongside the rise of cross-chain bridges, reflected efforts to circumvent Ethereum’s scalability constraints.

Established DeFi protocols such as AAVE, Uniswap, and Synthetix began expanding to other chains;

Increased adoption of Layer 2 solutions improved Ethereum’s scalability and reduced transaction fees;

Innovative financial products built atop DeFi 1.0 foundations, such as derivatives, yield aggregators (“gunpool”), and DEX aggregators;

Growing prominence of Decentralized Autonomous Organizations (DAOs), enabling collective community governance of DeFi protocols;

Introduction of ve-token governance models, (3,3) dynamics, and ve(3,3) frameworks helped align user and protocol incentives over longer time horizons, encouraging sustained contributions. The core idea behind ve-tokens is that users lock their tokens to receive non-transferable voting rights (veTokens); the longer the lock-up period, the greater the voting power earned. Notable examples include Curve and OlympusDAO’s (3,3) model, later adopted by GMX;

Uniswap launched its V3 version, introducing concentrated liquidity that allows LPs to provide liquidity within custom price ranges, enhancing capital efficiency and flexibility.

Compared to DeFi 1.0, DeFi 2.0 brought substantial expansion in product offerings and functionality, marking a major transformation in the entire DeFi ecosystem. As DeFi matured, opportunities diminished, and attention gradually shifted toward newer narratives such as NFTs, metaverse, Layer 2, and AI.

03 DeFi 3.0: Fixed-Income Products

As DeFi continues evolving, foundational infrastructure is now largely in place. TVL has grown from zero to over $43 billion, while the total crypto market cap stands around $1.2 trillion. The crypto industry is maturing, with increasing capital retention. Many users have grown accustomed to investing in the space and are optimistic about its long-term prospects, no longer rushing to cash out profits immediately. Consequently, demand for stable returns has steadily increased as idle assets accumulate within the ecosystem.

Market offerings such as ETH staking yields exceeding 4% and U.S. Treasury bonds yielding around 5% annually now meet this growing demand. This shift has steered DeFi development along two main paths: inward—LSDFi, and outward—RWA.

-

Inward: LSD → LSDFi

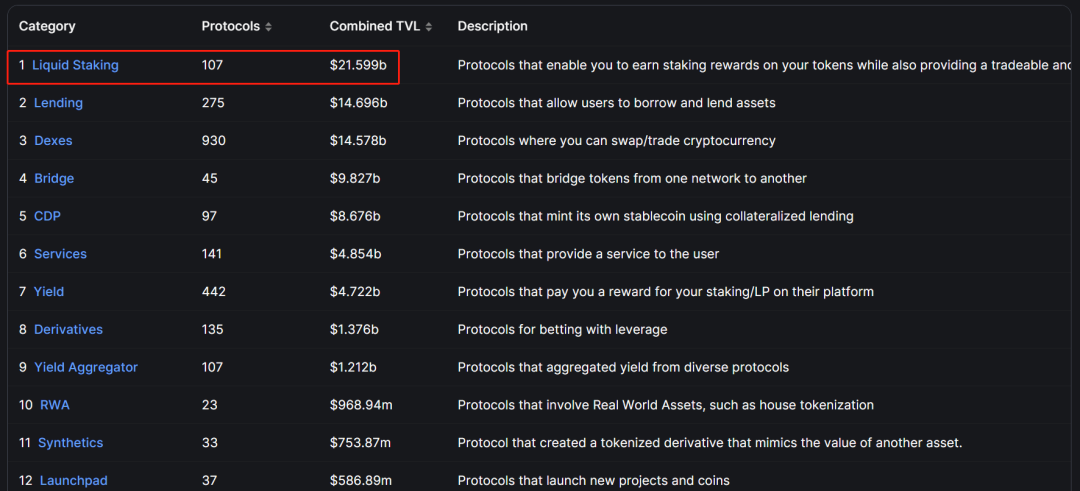

As of July 28, total DeFi TVL reached approximately $43.2 billion. Ethereum staking has surged from nearly zero in 2020 to over $40 billion today, with Liquid Staking Derivatives (LSD) accounting for more than $21 billion—about 50% of total DeFi TVL. LSD has clearly become an essential pillar of DeFi, and its share is expected to grow further as Ethereum’s market cap and staking ratio increase.

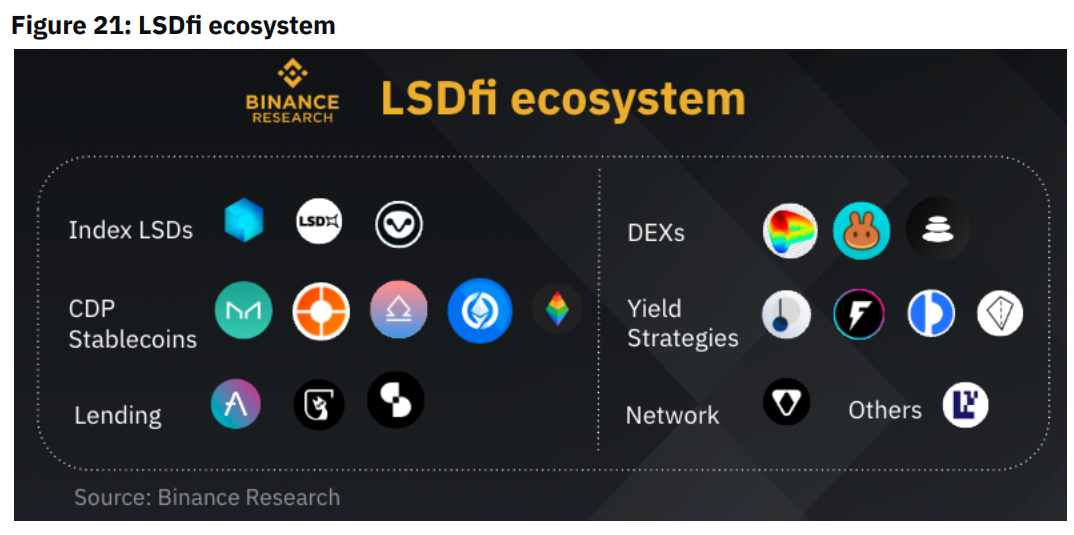

Solutions like Lido, Frax, and Rocket Pool offer liquid staking derivatives, greatly improving liquidity for staked assets. As the LSD sector matures and the scale of Ethereum staking expands, LSD is evolving vertically into LSDFi—layering protocols upon one another to generate higher yields. For more details on LSDFi, see Baicai’s earlier article: After Shanghai Upgrade, Ethereum Staking Volume Rises Instead of Falling, Boosting Hype Around LSDFi.

Binance Research classification of LSDFi

-

Outward: RWA

RWA, or Real World Assets, refers to the tokenization of real-world assets. The concept was first introduced around 2017, with attempts to tokenize real estate and luxury goods, but failed to gain traction. However, recent advancements in DeFi have created fertile ground for RWA to finally take root.

In the first half of this year, the concept resurfaced as traditional institutions began experimenting: Goldman Sachs launched its GS DAP platform to help the European Investment Bank (EIB) issue a €100 million digital bond; private equity firm Hamilton Lane tokenized part of its equity fund for investor sales; Siemens issued a €60 million digital bond on a blockchain; and BOC International (BOCI) announced a collaboration with UBS Group to issue a tokenized note worth 200 million RMB.

Meanwhile, in the crypto space, legacy DeFi protocols like MakerDAO, Aave, and Compound have started targeting the RWA sector, fueling rising interest. According to CoinMarketCap, the total market cap of RWA-related tokens exceeds $2.5 billion.

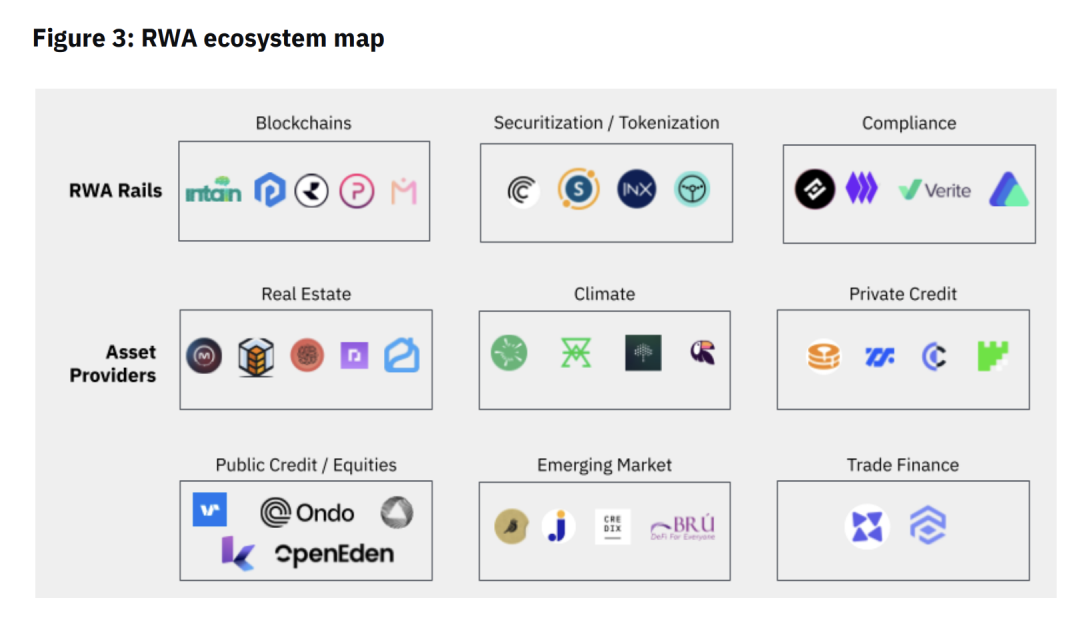

RWA initiatives currently fall into two main categories: one involves investing on-chain assets off-chain to generate returns; the other involves bringing off-chain assets on-chain to create economic value. These approaches bridge on-chain and off-chain ecosystems, enhancing liquidity while generating yield. Currently, the most popular form of RWA involves digital dollar stablecoins like USDT, USDC, and DAI—essentially mapping U.S. Treasuries onto the blockchain through tokenization.

Binance Research classification of RWA

What Are Some Key Projects in the RWA Space?

MakerDAO: In 2022, co-founder of MakerDAO proposed the “Endgame Plan,” incorporating certain RWA assets as collateral for the DAI stablecoin. Data from MakerBurn shows that 11 RWA projects have been integrated, contributing $2.48 billion in assets—accounting for 53% of MakerDAO’s total collateral and generating 53.9% of its revenue;

AAVE: Aave launched its RWA market in 2021, enabling borrowing against real-world assets. Current RWA market size stands at only $76.65 million, but with the launch of its native stablecoin GHO, Aave is expected to follow DAI’s path and integrate RWA-backed assets;

Superstate: A new venture founded by the creator of Compound, aiming to tokenize U.S. Treasury bonds on Ethereum;

Centrifuge: One of the earliest DeFi protocols in the RWA space, serving as the underlying tech provider for MakerDAO and Aave. Centrifuge currently hosts 17 RWA pools totaling $230 million in value;

Ondo Finance: A decentralized investment bank that invests in U.S.-listed money market funds off-chain and partners with Flux Finance on-chain for stablecoin lending. Launched tokenized funds early this year, allowing stablecoin holders to invest in bonds and U.S. Treasuries;

Maple Finance: Primarily focused on institutional lending, Maple Finance announced plans in April to launch a lending pool backed by U.S. Treasury bonds, expanding its real-asset-collateralized lending model;

RealT: A compliant real estate tokenization platform founded in 2019, having facilitated over $52 million in real estate tokenizations, with more than 970 homes tokenized on its platform;

Toucan: Transforms carbon credits into tokens, leveraging DeFi to facilitate trading of carbon offsets.

04 Summary

The above outlines the evolutionary path of DeFi. It’s clear that the blockchain industry tends to innovate and improve upon existing technologies when they encounter bottlenecks or limitations.

Is DeFi really dead? Not at all. LSDFi already experienced a surge earlier this year, and RWA has gained increasing attention over recent months.

Do you think LSDFi and RWA represent the future of DeFi—or is there another possibility?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News