Y Combinator Partner: How to Meet with Investors Most Effectively and Raise Funds?

TechFlow Selected TechFlow Selected

Y Combinator Partner: How to Meet with Investors Most Effectively and Raise Funds?

If you don't need to raise funds, don't waste time and energy meeting with investors.

Compiled by: TechFlow

Note: This article is part of the TechFlow series "YC Startup School Chinese Notes" (updated daily), dedicated to collecting and organizing Chinese translations of YC courses. The seventeenth installment features an online course by Y Combinator partner Aaron Harris titled "How to Meet Investors and Raise Funds."

Before holding investor meetings, you need to identify potential investors and understand how to attract them and secure their investment. A successful fundraising meeting requires a clear understanding of what you're doing and how you plan to achieve your goals.

When considering investor meetings, several questions arise: when do you need such meetings, who should participate, how to set up meetings, and how to conduct them effectively.

A meeting isn't just about entering a room, sitting across from someone, and making eye contact. A real meeting involves dialogue, presenting ideas clearly, and knowing exactly what points you want to convey.

To truly get funding from someone, you typically need to go through many steps: finding them, convincing them to meet with you, persuading them to invest, and finally getting the money into your bank account. If you follow these suggestions, no one will reject you. If they do reject you, it's on you.

First, determine when you actually need to raise funds. Not all businesses require external capital. For example, Mailchimp never raised a single dollar in outside funding but is now worth billions. Before approaching investors for funding, ask yourself: Do I really need to raise money?

You can raise money at the idea stage, with a prototype, or once you have users. When you genuinely need capital to grow your business, deciding whether to fundraise becomes a critical decision for your company. Therefore, treat fundraising as an ongoing process.

If you have nothing yet and don’t know how to spend money wisely, don’t attempt to raise funds. Instead, focus on building your product and company. Once you have an idea or prototype, you’ll realize that more capital could help you move faster toward your goals.

Now imagine being an investor—why would you invest in a founder? You’d want the startup to become highly successful and powerful, and you’d expect the founders to use the money wisely.

Why Do You Need Capital to Grow?

- Many believe the first step in fundraising is hiring employees.

This idea is appealing because many companies boast about their headcount. But in reality, when building startups leveraging software, you need far fewer people than you might think.

In fact, hiring may be the fastest way to kill your company, since people cost money. Carefully consider whether you truly need to hire. If you're already hiring, then you likely need funding regardless of whether your idea has growth potential.

Ask yourself: Is hiring more people really the bottleneck preventing your next stage of growth?

- People often claim user acquisition is their main obstacle.

Spending on Google Ads is usually a poor strategy for early-stage growth.

Before spending money, focus on free user acquisition. Let satisfied users refer friends—this gives you organic growth without fundraising.

- The last common issue is customer service.

If you can't meet customer demands, this can be a valid reason to raise funds, because as a founder, you'll handle customer service for a long time. Only when you have enough users and paying customers can you stop doing this personally.

Users of free products generally have lower expectations for support, meaning you can manage more on your own. But if customers are paying, they expect higher-quality service—and you gain more revenue. So before seeking outside capital, you can hire additional staff specifically for customer service.

Finally, here’s a warning: the earlier you raise funds, the more dilution you face. Unless you have tangible progress, no one will give you a $3M, $5M, or $10M valuation. Every dollar raised means giving up more equity in what could eventually be a billion-dollar business.

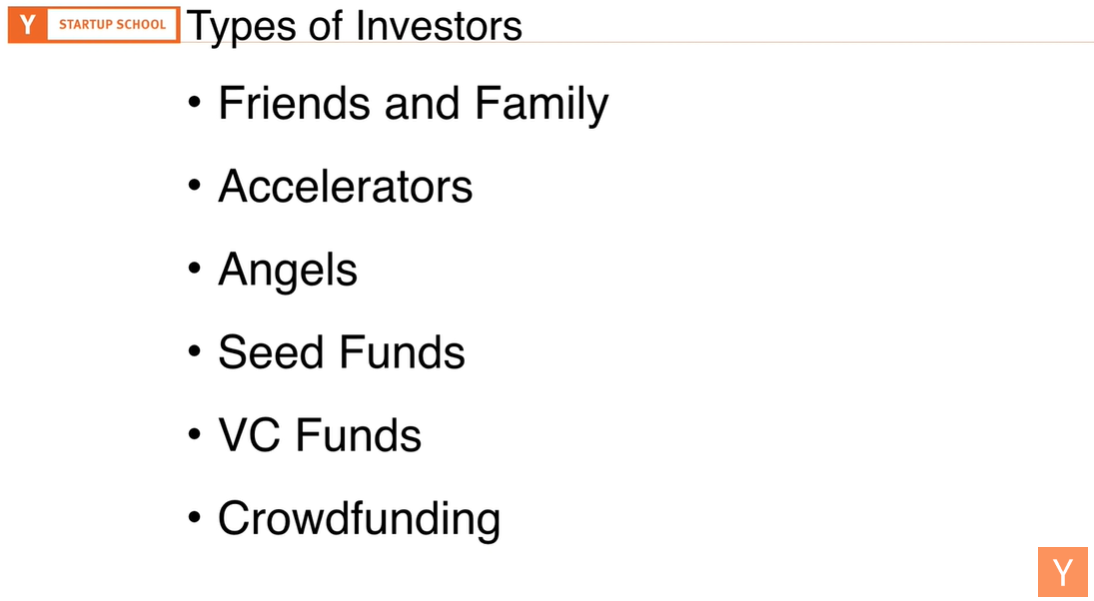

Types of Investors

Before discussing types of investors, we must recognize there are many ways and places to raise capital. To secure funding, you need to understand different investor types, how to approach them, and how to convince them to invest. Investor types include: friends and family, accelerators, angel investors, seed funds, venture capital (VC) firms, and crowdfunding platforms.

Friends and Family

One of the most common sources of startup funding is friends and family. They’re willing to support you financially out of personal loyalty.

However, don’t take advantage of their goodwill. Only accept money from those who can afford to lose it.

Since most startups that raise from VCs fail to return capital, carefully consider whether you need money from loved ones. Keep terms simple. Don’t raise $50K from your grandmother at a $50M valuation—that makes no sense.

Avoid high valuations with family members, as this can complicate future fundraising. Treat any meeting with friends or family as seriously as you would with professional investors—respect their time and treat them like real investors.

Accelerators

Accelerators are typically educational programs run by investors. One famous example is YC.

YC runs a three-month accelerator program that helps startups improve performance and visibility. By sharing experience and helping avoid mistakes, YC aims to make companies stronger. At Demo Day, YC launches these companies and provides community support.

Today, there are thousands of accelerators worldwide. While startups are growing rapidly, the number of accelerators is growing even faster. This is concerning because many accelerator advisors have never worked at a startup, launched one themselves, or invested in startups outside of accelerator programs.

Therefore, consider carefully whether to join an accelerator. Ask yourself: Why listen to advice from people who’ve never done what they’re telling me to do? If most accelerators actually harm companies, we must use them cautiously.

A company doesn’t necessarily need an accelerator to succeed. If it works well, great. But if it fails to accelerate—or even slows us down—using an accelerator could hurt the company.

So before deciding, research thoroughly. An accelerator’s value isn’t just about funding—it also depends on other forms of support.

Angel Investors

Angel investors are typically wealthy individuals with time and money to spare. They often invest for fun—on Twitter, they talk about their “unicorn” companies like it’s a hunting game. While you rarely know how much they actually invest or whether they profit, they enjoy backing new startups for various reasons: seeing new technologies emerge and supporting young entrepreneurs.

Finding angels isn’t hard—just send an email or reach out locally. But beware: some angel groups exist only to show status, not to invest. Research beforehand—check if they’ve made active investments in recent months or years. If they haven’t invested in 1–2 years, pursuing them may not be worthwhile.

Seed Funds

Seed funds are super-professional angel investors who have raised external capital to invest. Typically, they represent limited partners who don’t have enough capital to form large funds. These investors are often new but very focused and skilled. They’re good and usually eager to meet emerging founders and find promising opportunities.

Emailing seed fund investors is effective—they exist to meet new founders and evaluate deals. A warm reply is ideal. Remember, seed investors aim for returns to raise more funds, so they aren’t interested in small outcomes. They usually ignore lifestyle businesses. However, if your business generates cash flow, angel investors might be more inclined to invest.

Venture Capital Funds

Raising from VC funds is a major undertaking—they manage entire industries. These funds write checks ranging from millions to billions of dollars. When seeking investment, understand which capital stage fits your needs.

VC funds typically have multiple limited partners who expect certain return targets. They analyze global VC activity to decide where to allocate capital. As a VC partner, beyond wanting to be a better investor, you must offer higher risk-adjusted returns than peers to win LP commitments.

When VCs consider investing in your company, they care not only about returns but whether the investment could return the entire fund. So during VC meetings, demonstrate your ability to build something big.

VCs usually have strict decision-making structures. In early stages, most top-tier VCs send only one partner to initial meetings.

If you're preparing for your first check, you might not need these investors yet. But when ready for larger raises, this process comes later.

Crowdfunding

Crowdfunding platforms are another option. Like professional investors, these sites vet companies for legitimacy and provide a platform for people to donate without requiring individual meetings. With crowdfunding, managing too many small investors can become a logistical nightmare.

Unlike traditional investors, crowdfunding backers aren’t looking for cold introductions. Sending generic emails won’t work—and spamming is unacceptable. Instead, attract interest through personalized outreach: learn their background and interests, tailor your message, excite them about your vision, and create mutual benefit.

Note: Crowdfunding is rarely suitable for large-scale fundraising, as managing numerous small investors becomes unmanageable. It’s best used when other options fail, you lack local investors, or you want to avoid time-consuming meetings. The goal is to excite investors and secure funding—so weigh this choice carefully.

Cold Emails

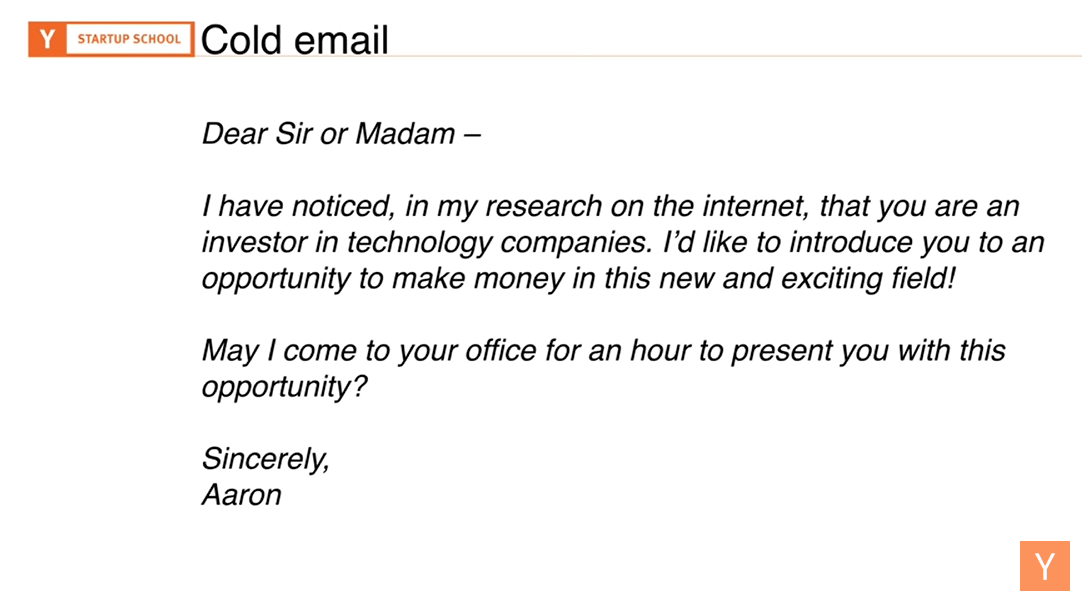

Earlier, I mentioned some investors welcome cold emails. Actually, anyone can receive them—but quality varies. For example, this is a terrible cold email:

“Dear Sir/Madam, I noticed from my online research that you invest in tech companies. I’d like to introduce you to a profitable opportunity in this exciting new field. Can I come to your office for an hour-long presentation?”

This kind of email won’t resonate. It lacks identity, context, and relevance. Professional investors deal with people constantly—their most precious resource is time. A poorly researched cold email that ignores their interests likely gets ignored.

Most investors publicly share their interests—what they’ve invested in, blog posts about ideal companies, past ventures—via social media and blogs.

Research every investor you want to engage with, and find a way to stand out.

For example:

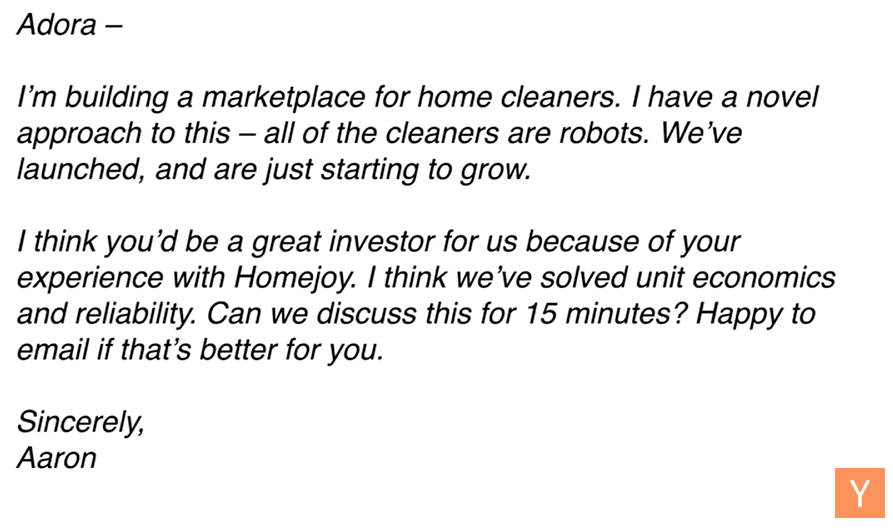

“I’m building a marketplace platform for home cleaning services. My innovation? All cleaners are robots. We’ve launched the platform and are just beginning to scale.

I believe you’d be a great investor because you backed Homejoy. I think we’ve solved unit economics and reliability issues. Could we chat for 15 minutes? Email is fine too if preferred.”

“Home cleaning market” and “robotic cleaners” connect directly to her past investments. Highlighting unit economics and reliability, plus requesting only 15 minutes, increases response likelihood.

When emailing investors, research their background and interests thoroughly—never send spam.

If you conduct deep research, identify relevant connections, and craft tailored messages, you greatly increase your chances of a response—and potentially a successful investment meeting.

Types of Investor Meetings

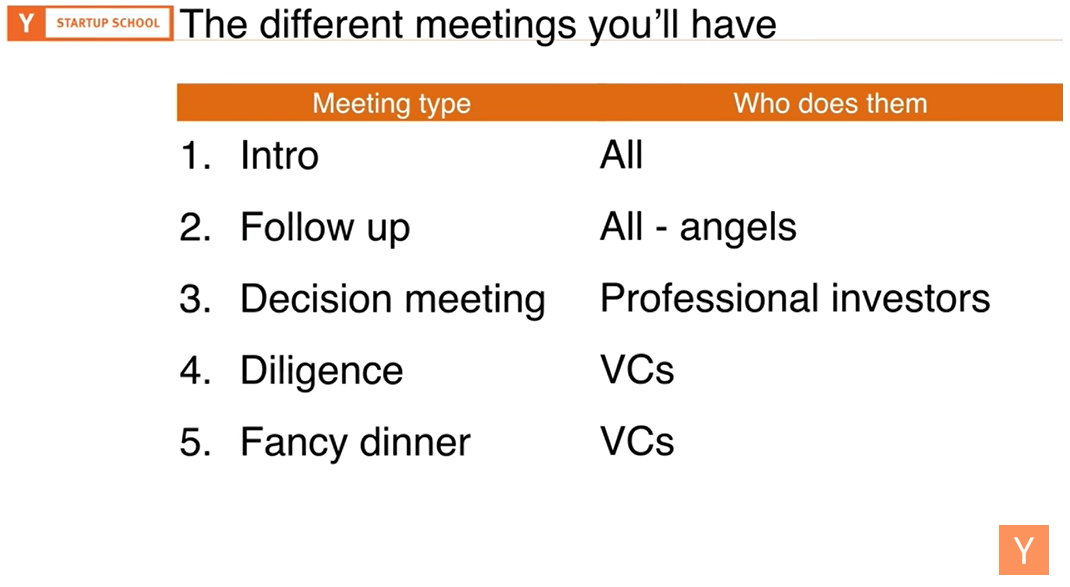

There are several types of investor meetings you’ll encounter, and each investor may attend different kinds.

-

Intro Meeting: Held with all investors except those on crowdfunding platforms. You present your company and business plan.

-

Follow-up Meeting: Attended by nearly all investors, except angels who decided immediately after the first meeting.

-

Decision Meeting: Reserved for professional investors. Involves multiple partners or repeated sessions with one partner to assess fit and finalize terms.

-

Due Diligence Meeting: Typically includes you, your team, and your lawyer. Conducted by the VC firm or sometimes delegated within their team.

-

Fancy Dinner: If things go well, investors may host a celebratory dinner. Note: Even if not raising funds, you might still enjoy free meals—investors use this to impress and showcase themselves. Since investors become part of your company life, ensure they’re not assholes. If you wouldn’t want to spend an hour at dinner with someone, reconsider taking their money. Early on, this matters less with small angel checks, but for large investments, think carefully about whom you bring onto your team.

Intro Meeting

When meeting investors, introductions matter—but clarity matters more. This is foundational, as studies show people decide interest within the first 30 seconds. Ensure you deeply understand your idea and can explain it clearly. Demonstrating a working product helps—even better, let investors interact with it. Investors love real products.

The primary goal is convincing investors your company can become a giant. Progress is key. Dress appropriately—not overly formal, but not sloppy. First impressions count.

If you pass the intro, prepare for follow-ups—except for angels who may invest after the first meeting.

Follow-up Meeting

During follow-ups, dive deeper into your business. Metrics are crucial—whether current or projected. If building consumer products, establish a framework to track monthly, weekly, daily, or even hourly engagement.

Be able to articulate your progress—and understand it’s relative. Know how long you’ve worked and how far you’ve come. Five years with no traction is bad; one month leading to a prototype is excellent.

Go deeper than in the intro meeting, especially since decision meetings demand strong domain expertise. Most angels don’t need a pitch deck—it’s often just flashy slides. Customers buy products, not decks. If you must have a deck, keep it simple—8 to 10 slides max.

If you have metrics, master them. Know your 6- or 12-month retention cold—you shouldn’t need to look it up during the meeting.

Ultimately, any key metric should be explainable at multiple levels—you must fully grasp your business KPIs.

Decision Meeting

The decision meeting is critical with professional investors. Here, you show your current position and forecast the biggest possible future. When I attended Sequoia’s decision meeting, I sat with five partners.

They cared deeply about what my company could become in 10–15 years. They already knew the basics but wanted insight into my long-term vision and ability to execute. Could we become a global leader? You must deeply understand and articulate this to prove you’re not just another company, but one with foresight. This distinction is what convinces investors you can deliver on your vision.

Due Diligence Meeting

If you’ve done your homework, this meeting usually goes smoothly—and happens later anyway. Early in your company’s lifecycle, do everything possible to keep legal and financial records clean to avoid surprises—like discovering your cash balance is 50% lower than expected.

Assuming everything checks out, have a metrics dashboard ready to show investors everything you’ve achieved. If you understand the meeting structure and communicate clearly, you’ll reach the final step: enjoying a lavish dinner.

Fancy Dinner

Ultimately, what you want is the money in your bank. No matter how fancy the restaurant or how cool the investor seems, none of that matters.

As a business, if you need capital to scale, you just need the money. If you can get funded without these dinners, they’re irrelevant.

So if a top-tier investor emails: “Hey, I’m traveling this month, but I really want to invest. Can I wire $250K now and we catch up later?” Don’t reject them just because you haven’t had coffee. Don’t turn down funding due to missing some “perfect” process. Suggest a phone call, do your diligence, check references—and take the money.

Key Considerations

A few key points to remember about meetings and investors.

First, attending meetings ≠ progress. Many founders brag about meeting big names—but that’s not what matters. What matters is building a successful, large company.

If you don’t need funding, don’t waste time meeting investors. Only reach out when you truly need capital.

Once you find an investor willing to fund you, signing documents and receiving the wire completes the deal. Investors hate saying no—it means potentially missing a big return and risking a reputation for poor judgment. Thus, fast-decision investors are highly valued.

If you keep having meetings with no real progress, reevaluate your strategy. When meeting others, delay discussing funding until the end—first understand their needs and expectations. Finally, remember: this is partly a gamble. Someone must make a decision—hesitant investors rarely make the best calls.

Asshole investors come in many forms—trying to impress you with power or connections, or making you feel stupid about your idea. If this happens, walk away—and tell your friends this person is an asshole.

If you face any harassment—including sexual, racial, or discriminatory behavior—speak up. YC takes this seriously. All investor meetings should be safe and comfortable. Follow these guidelines, and I believe everything will go well.

Common Vision Mistakes Founders Make

What are common vision mistakes founders make? Some companies sound too broad and unfocused. For example, introducing your company as: “We’re a search engine—we also build self-driving cars, phones, speakers, balloons that beam internet, plus ads, display advertising, AI, and a whole department exploring wild ideas.”

This sounds messy and scattered. Conversely, focusing only on market share and size feels shallow: “We’ll capture 10% of a $500M market—that’s $50M, and we’ll own 100%.” This lacks ambition and vision.

Instead, balance two extremes: have a grand vision, but also concrete, achievable plans. Only then can you thrive in future competition.

Investor FOMO Mechanism

Investors want to back the biggest possible companies and maximize ownership. But in early-stage startups, there’s little data proving success. So investors seek indirect signals—one of the strongest being: do other smart people believe in this?

Thus, FOMO (fear of missing out) arises: if you see other sharp investors involved, you infer the company is promising and might become huge—and you don’t want to miss out.

Yet the best investors are those who make independent decisions faster, with lightning-fast due diligence—they lead the pack. You can pressure others by showing momentum, forcing them to act quickly. But investors who sit waiting for others to decide are rarely good bets.

How to Get Funding from Friends or Family?

It’s about relationship-building and choosing the right approach. Different people respond to different styles. Some might appreciate you showing up daily with donuts and coffee—but not everyone. Adapt accordingly. Practicing your pitch in elevators or on decks works well.

If your friend or family member is a successful founder or VC, treat them as practice partners—share your plan, seek feedback and support, but keep interactions professional.

Should You Give Up on Fundraising?

Whether to quit fundraising depends on your situation. Generally, if you're torn between building and fundraising, avoid raising unless absolutely necessary.

Fundraising duration varies. Typically, allow at least 18 months. But if fundraising consumes so much time that you’ve gone a year without product development, that’s dangerous—no progress means failure.

So evaluate carefully—don’t rush into fundraising blindly. If you’re a new company that tried fundraising for one or two months with no traction, explore other growth paths first. Return to fundraising once your company gains momentum.

Must All Founders Participate in Fundraising?

Some investors specialize in female founders—a positive trend. Leverage every unfair advantage in fundraising and company-building. If you’re a woman founder, use that as an edge to secure investment.

But not all founders need to fundraise. That’s the CEO’s job. If you have co-founders, let them focus elsewhere to keep operations moving.

In early rounds, you don’t need the whole team at meetings. Professional investors negotiate professionally—you may lack experience. If everyone’s present and an offer comes, you must decide instantly—putting you at a disadvantage.

So only key people—like the CEO—should attend. If you get an offer, discuss it with co-founders afterward. This buys time to properly weigh pros and cons.

Q&A

-

Should you approach a VC who invested in a competitor?: If they invested in a competitor ten years ago and that company went public, they might actually be perfect investors—they understand the space and can help you IPO. Each case differs—assess based on specifics.

-

Check sizes for seed funds, angel funds, and micro VCs: Depends on variables: investor type, market, geography, company needs, etc. Small funds and angels typically write checks from $10K to $100K; larger funds exceed that.

-

Finding credible angel investors: Ask for references and review their portfolio. Active angels often document and discuss their investments—it helps them source deals. In emerging markets, this may be harder, but manageable with effort.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News