LD Capital: MakerDAO, where all things grow, the spark has been lit

TechFlow Selected TechFlow Selected

LD Capital: MakerDAO, where all things grow, the spark has been lit

The veteran crypto project MakerDAO has entered the "endgame" phase, aiming to become an ecosystem akin to a Layer 1 by establishing several SubDAOs, enabling "everything to grow."

Legacy crypto project MakerDAO has entered the "Endgame Plan" phase, aiming to become an ecosystem akin to a Layer 1 by establishing several SubDAOs, enabling "all things to grow."

Author: LD Capital

Executive Summary

MakerDAO, one of the most successful legacy crypto projects in decentralized governance, development, and operations, has now entered its "Endgame Plan" phase. By creating multiple SubDAOs that spin out new functions and products based on the Maker system—enabling self-governance, financial independence, and potential issuance of new tokens—it aims to reduce operational costs and isolate risks, enhancing the sustainability of its increasingly complex system. This move could transform Maker into an ecosystem similar to a Layer 1, fostering an environment where “all things can grow.”

A new SubDAO formed by core developers and the Chief Growth Officer of MakerDAO will launch Spark, a lending protocol built on Aave V3 code, this April. It is expected to unlock greater value from over $8 billion worth of collateral held in Maker’s treasury. Theoretically, Spark will synergize strongly with Maker’s low-cost D3M lending module and PSM minting pool, offering $DAI the most competitive and relatively stable interest rates available.

“Matrixification” of DeFi has become a trend, as established DeFi applications leverage user assets or liquidity advantages to develop more native nested applications. For example, Curve launched crvUSD, Aave introduced GHO, and Frax released Lend. However, compared to the difficulty for Aave/Curve to scale up their stablecoins (GHO/crvUSD), it is significantly easier for Maker to scale its lending business.

The launch of Spark marks the beginning of a major transformation within the Maker ecosystem. The marginal improvement for the $MKR token is most pronounced, requiring a revaluation from a single-project token to an ecosystem-level token akin to those of public blockchains. For the first time, $MKR gains utility through staking and yield farming, potentially offering stakers 12–37% APY. Additionally, ecosystem applications are projected to expand Maker’s balance sheet effectively, generating an additional $2.75–12 million in annual revenue under conservative to neutral scenarios, thereby increasing $MKR burn volume by 1–3x.

The Spark That Lights the Fire: Spark Protocol

When MakerDAO founder Rune Christensen proposed the "Endgame Plan" in June last year, he emphasized that MakerDAO must continue expanding while maintaining maximum flexibility. On February 9, 2023, a group of key team members❶founded Phoenix Labs, dedicated to developing new decentralized financial products to expand the Maker protocol ecosystem.

Spark Protocol is the first protocol developed by Phoenix Labs—a general-purpose lending protocol using DAI and other mainstream crypto assets as collateral for over-collateralized borrowing. As the first protocol illuminating Maker’s new DeFi matrix, the name “Spark” fittingly echoes the Chinese idiom “a spark can start a prairie fire.”

Built on Aave V3 code, whose lending mechanism has been battle-tested in the market, users deposit highly liquid assets such as ETH, WBTC, stETH, etc., and borrow desired assets according to interest rate models. Theoretically, this will create powerful synergies with Maker’s low-cost D3M lending module and the near-100% capital-efficient PSM minting pool for stablecoins, providing $DAI with the most competitive and relatively stable interest rates across the entire market.

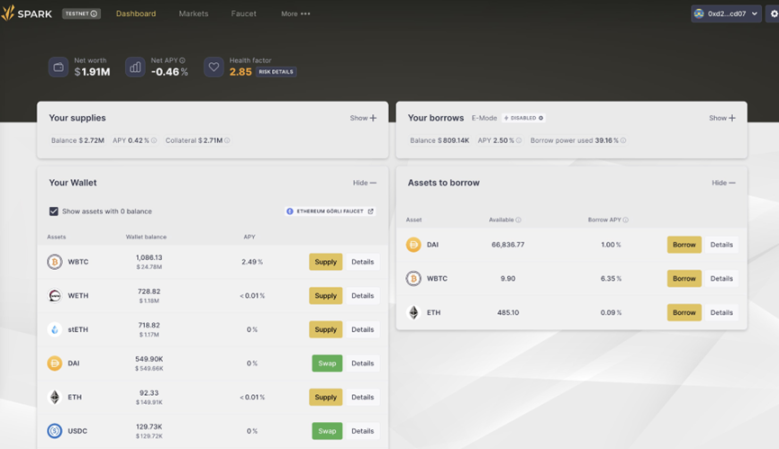

Figure 1: Spark Application Testnet Interface, Source:Spark, Trend Research

Of course, the Spark team has already stated that once DAI borrowing reaches $100 million over the next two years, 10% of profits earned in the DAI market will be allocated to Aave, and a proposal has already been submitted on the Aave forum.

Spark Protocol Product Advantages

Proven Codebase

Modified from Aave’s mature and historically tested code, ensuring high security. Similar to aTokens, depositors receive tokenized versions of their positions (spTokens), which can be transferred and traded like any other crypto asset on Ethereum, further improving capital efficiency.

Low-Fixed Interest Rate Borrowing

Spark Lend can directly access Maker’s credit line—the Dai Direct Deposit Module (D3M❷)—theoretically allowing users to borrow any amount of Dai at a rate slightly above❸ the Dai Savings Rate (DSR, currently at 1%). However, there is an initial cap of $200 million.

High Capital Efficiency for ETH-Class Assets

Spark Lend also incorporates Aave V3’s e-Mode feature, enabling ETH-class assets to borrow against each other at up to 98% LTV. For instance, wstETH can be used to borrow up to 98% of its ETH value, maximizing capital utilization.

Dual Oracle Feeds Increase Resistance to Price Manipulation

Spark may use dual data sources—ChronicleLabs (formerly Maker Oracles) and Chainlink double oracle setup—to provide on-chain pricing. These feeds undergo three layers of validation via TWAPs (time-weighted average prices), signed price sources, and circuit breakers to prevent price manipulation.

Fair Launch

The protocol token will be distributed entirely through liquidity mining with no pre-allocation❹, ensuring fairness and broad community participation. According to project statements, Spark Protocol must compete fairly to earn support from SubDAOs and be accepted as a product.

Full Backing by MakerDAO

Spark is not a typical “independent third-party” protocol. Although developed by Phoenix Labs, it is fully owned by Maker Governance, including all smart contracts, trademarks, and IP rights. This implies that if the protocol ever faces insurmountable challenges, Maker is highly likely to step in as a backstop.

Three Key Initiatives to Make $DAI a Better “World Currency”

Maker’s mission is to create a “fair world currency,” but compared to $USDT’s market cap exceeding $70 billion, $DAI’s $5+ billion valuation falls short. How can it scale and eventually surpass centralized stablecoins?

The launch of Spark Protocol signals three strategic directions for Maker’s future product development—all aimed at increasing DAI issuance and reducing usage costs:

Integration of Internal D3M and PSM Functions

Spark Lend integrates existing internal modules D3M❺ and PSM❻ to provide liquidity for the stablecoin DAI.

The most significant advantage of D3M is enabling direct DAI minting in secondary markets, eliminating the need for primary minter intermediaries who first mint DAI within Maker before depositing it into secondary applications. This consolidates two layers of over-collateralization into one, improving DAI’s real-world capital efficiency.

The initial plan allocates $300 million in D3M liquidity to Spark Lend, with $200 million as the first-phase hard cap and $100 million as buffer funds. This limit may be adjusted dynamically based on actual market borrowing rates.

Additionally, Spark Lend’s frontend will integrate MakerDAO’s PSM and DSR features, allowing USDC holders to directly convert USDC in PSM to DAI via the Spark Protocol website and earn deposit yields through DSR, thus stimulating DAI demand from the user side.

For example, when $1 of $DAI flows out from a lending market like Aave, there are typically two layers of collateral behind it: approximately $1.5 worth of Aave collateral + $1.5 worth of collateral locked in Maker’s treasury❼. Without considering recursive borrowing, this common scenario consumes $3 worth of total crypto collateral. But with D3M and PSM integrated, borrowing $1 of DAI on Spark requires only $1.5 of collateral (or $1 of whitelisted stablecoins like $USDC), greatly improving capital efficiency.

Entering the LSD Market via EtherDAI

Spark Protocol will promote the use of EtherDAI—an ETH-based liquid staking derivative. For example, Lido’s stETH can be wrapped into ETHD and used as collateral to borrow DAI.

Maker governance will retain backdoor access to ETHD collateral, possibly incentivizing liquidity by launching short-term liquidity mining for the ETHD/DAI pair on Uniswap. Alternatively, setting zero stability fees for the EtherDAI Vault could stimulate demand.

Secondly, after Ethereum’s Shanghai upgrade, official staking rewards of over 4% are expected, triggering massive migration of ETH assets. By supporting liquid staking (LSD) wrapped tokens, Spark prevents TVL contraction and may even attract more capital through yield stacking, thereby reducing reliance on USDC.

More importantly, TVL represents the value of locked funds in a protocol. As TVL increases, so does liquidity and usability, leading to higher potential revenues. For Spark, a significant revenue stream comes from the interest spread between lenders and borrowers.

Maker + Spark = Lowest and Predictably Stable Market Rates

The emergence of Spark will also allow Maker to actively control DAI supply based on market demand, enabling direct interaction with secondary markets—aiming to offer better interest rates and increase DAI supply.

Specifically, during periods of DeFi market frenzy, borrowing rates often surge, forcing users to pay unexpectedly high loan costs, negatively impacting $DAI’s supply-demand dynamics. D3M will stabilize $DAI rates and influence major $DAI lending markets (like Spark). When demand for $DAI is high, Maker can expand Spark’s minting and supply caps to lower interest rates. Conversely, if demand weakens, $DAI liquidity will be withdrawn from Spark to raise rates.

In sum, maintaining the cheapest and predictably stable borrowing rates for $DAI in the “battle royale” of stablecoins is a critical competitive advantage for increasing adoption. Through the D3M pool, $DAI can achieve relative rate stability and remain the most competitively priced across all markets.

Current Revenue and Expense Analysis of MakerDAO Protocol

MakerDAO currently incurs over $40 million in annual costs. Without aggressive investments in RWA (real-world assets), the project would face a net loss of $30–40 million. Hence, the founder proposed the cost-saving and revenue-expanding “Endgame Plan.”

Revenue

MakerDAO’s current income stems from four main sources:

Stability fees from over-collateralized Vaults (i.e., interest from minting/borrowing DAI);

Penalty fees from liquidation of undercollateralized positions;

Transaction fees generated through PSM;

Returns from RWA (real-world assets) Vaults.

Stability fees from crypto asset Vaults were once the protocol’s primary revenue source, but RWA investment returns have now become the largest contributor.

Expenses

Protocol expenses mainly consist of employee salaries, marketing, and growth initiatives, with core engineering personnel constituting the largest share.

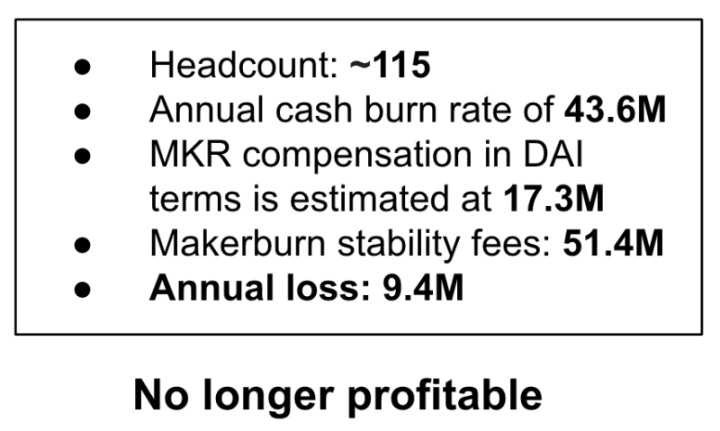

In June 2022, MakerDAO co-founder Rune Christensen revealed: annual stability fee revenue was about $51.4 million, while protocol maintenance cost $60.9 million, including $43.6 million in cash flow and $1.73 million in $MKR-denominated expenses, resulting in a deficit of ~$9.4 million.

Figure 2: MakerDAO Protocol Revenue Disclosure, Source:MakerDAO Forum, Trend Research

Major reasons for the deficit include: 1) sharp decline in protocol revenue during bear markets; 2) generous team compensation; 3) governance redundancy. Current governance processes are complex, require large teams, and result in long cycles, slowing down new product development.

Therefore, Rune Christensen introduced the Endgame Plan, which we’ll detail below. It includes strategies to address the current revenue shortfall, primarily through accelerating RWA growth.

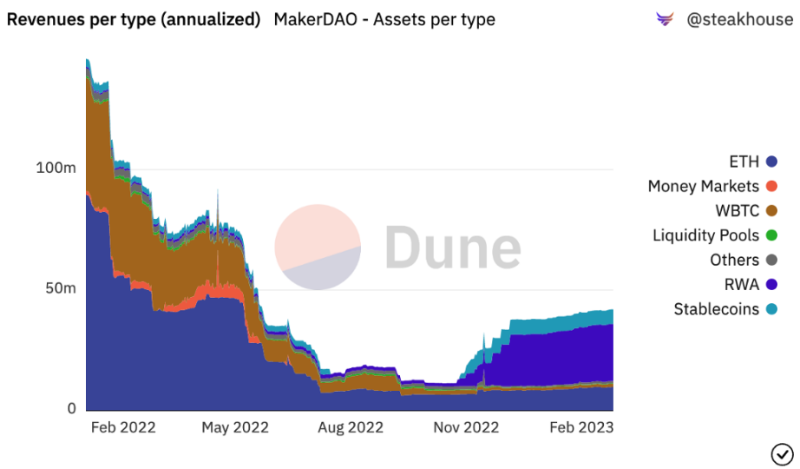

Figure 3: MakerDAO Revenue Structure, Source:Dune Analytics, Trend Research

From the chart above: 1) ETH Vaults were a major profit source until November 2022; 2) since then, RWA Vaults have become the top revenue generator.

RWA Vaults involve investing in off-chain financial markets, primarily bonds and mortgage loans. Since RWA collateral generates higher stability fees, they’ve delivered stronger returns as expected. Based on current $696 million in investments, over $26 million in interest income is projected annually, accounting for more than 40% of Maker’s total revenue.

However, RWA carries higher regulatory seizure risks. Thus, the Endgame Plan outlines strategies to mitigate these risks: under mild regulation, Maker prioritizes maintaining a strict 1:1 USD peg without limiting RWA exposure to maximize income. Assuming tightening regulations ahead, Maker may cap RWA exposure at 25%, and possibly depeg from USD when necessary. In extreme cases, the ultimate goal is preserving DAI’s resilience and survival—no longer accepting easily seizable RWA as collateral and possibly abandoning any reference fiat currency altogether.

Thus, relying solely on RWA income isn’t sustainable. Expanding revenue streams and optimizing organizational structure toward “cost reduction and revenue expansion” are essential for ensuring Maker’s long-term viability.

Endgame Plan: Letting All Things Grow

To better understand the upcoming transformation in the Maker ecosystem and the improved supply-demand dynamics of the $MKR token, one must first grasp the “Endgame Plan.” While much of the discussion revolves around regulatory and political contingencies, the essence of this plan is transforming Maker into an ecosystem akin to a Layer 1, enabling “all things to grow.”

First proposed by Rune in June 2022, the Endgame Plan has undergone at least three iterations of community-wide discussion on the governance forum. It is a structural reorganization initiative aiming to make MakerDAO a fully decentralized, autonomously operated DAO (decentralized autonomous organization), better serving the needs of Dai users. The plan consists of four core components:

Achieving full decentralization of MakerDAO;

Improving Dai’s liquidity and stabilizing its interest rates;

Enhancing protocol sustainability and reducing systemic risk;

Improving decentralized governance and DAO operations.

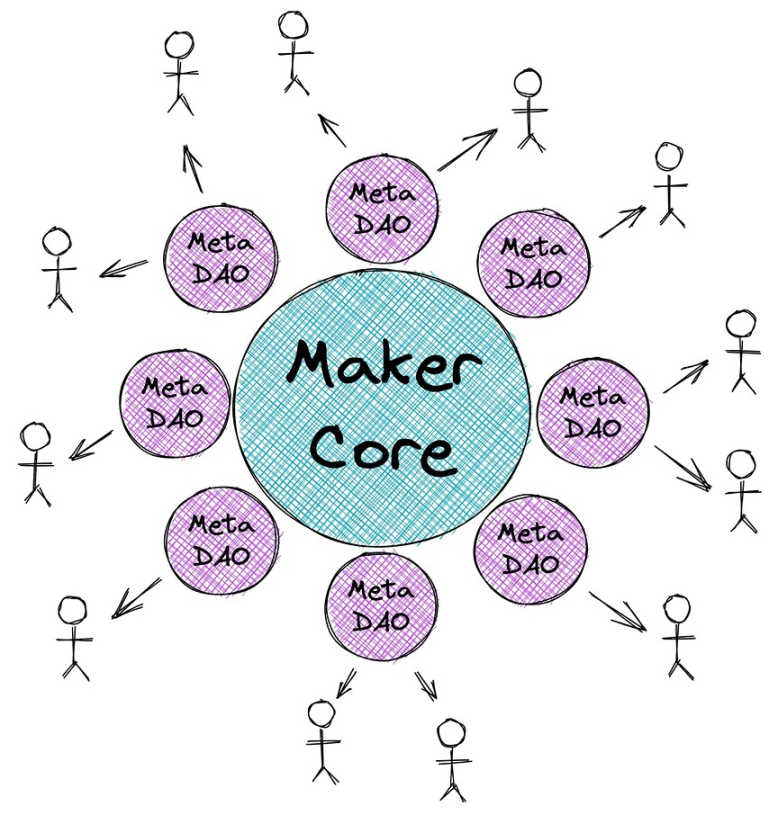

To simplify complex governance, Maker will create a series of self-sustaining DAOs called MetaDAOs❽. Rune likens Maker Core to Ethereum L1—secure but slow and costly to operate—while MetaDAO acts as an L2 solution, fast and flexible yet deriving security from L1. Through MetaDAOs, MakerDAO can focus on its core mission: issuing and stabilizing the Dai stablecoin. Meanwhile, MetaDAOs can provide governance support for other projects within the Maker ecosystem.

MetaDAO refers to the modularization of the Maker protocol. Each MetaDAO is a small community with its own token and treasury. The core value proposition of MetaDAOs is risk isolation, risk reduction, and parallelization of Maker’s highly complex governance process.

Figure 4: Visual Representation of MakerDAO Architecture, Source:MakerDAO Forum, Trend Research

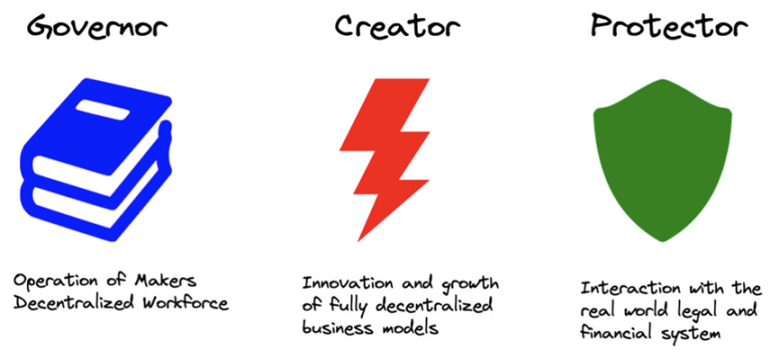

There will be three types of MetaDAOs:

Figure 5: Types of MetaDAO, Source:MakerDAO Forum, Trend Research

Maker Core retains all indispensable and non-removable components of the Maker protocol, essential for generating and maintaining Dai. Each type of MetaDAO surrounding the Core has specific functions determining how it interacts with Maker Core:

Governor (also known as Facilitator): manages decentralized staffing, on-chain governance, engineering, protocol management, and brand oversight for Maker Core;

Creator: focuses on growing the Maker ecosystem and developing new features—Spark’s team falls into this category;

Protector: responsible for managing RWA Vaults, focusing on real-world assets and protecting Maker from physical and legal threats to its off-chain collateral.

Internally, each MetaDAO maintains a governance process similar to Maker Core, deploying new ERC-20 tokens for governance, overcoming the current single-threaded bottleneck and enabling parallel execution to accelerate decision-making.

However, MetaDAOs operate their governance atop Maker Core’s infrastructure: governance signals are voted on by MetaDAO participants and then bundled into Maker’s executive votes for execution. This means MKR holders serve as an “appeals court,” with actual protocol control of MetaDAOs ultimately resting in the hands of MKR voters.

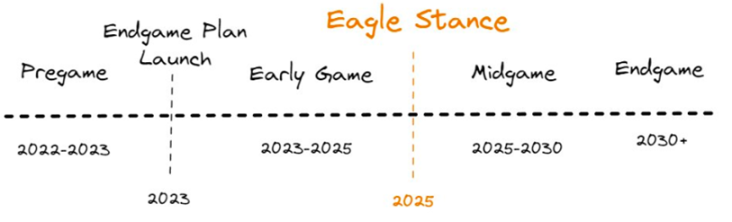

The Endgame Plan consists of four phases, with the Pregame phase expected to go live in 2023, including building ETHD, launching MetaDAOs, and initiating liquidity mining.

Figure 6: Endgame Plan Roadmap, Source:MakerDAO Forum, Trend Research

Spark Protocol will be the first MetaDAO, expected to launch in April 2023, currently undergoing mainnet deployment and branding initiatives. In the second half of the year, Spark plans to integrate with Element Finance and Sense Finance to offer fixed-rate borrowing and diversified yield strategies.

Initially, Maker plans to launch six MetaDAOs, each issuing a Sub Token. While Spark Protocol hasn’t explicitly detailed its tokenomics, based on the Endgame Plan and founder statements, Spark is expected to have its own token.

Moreover, each Sub Token will form a core liquidity pool with $MKR. The Maker team plans to annually distribute 45,000 MKR to incentivize liquidity provision across these pools—meaning each MetaDAO will accumulate 7,500 MKR during the Endgame period. Additionally, smaller rewards will go to ETHD, DAI, and MKR-related liquidity pools.

Figure 7: Spark Roadmap, Source:MakerDAO Forum, Trend Research

As the first application of the Endgame Plan, Spark is expected to generate over $10 million in annual revenue for Maker and introduce the first-ever liquidity mining opportunity for $MKR tokens—we’ll analyze this further below.

Industry Trend: DeFi App Matrixification

The lending platform created by Spark will directly compete with legacy protocols like Aave and Compound. Although Aave and Compound previously integrated D3M❾, Maker’s limited D3M capacity❿ will inevitably prioritize Spark going forward. Ethereum’s leading DeFi protocols appear to be entering a “matrixification race.”

DeFi apps are leveraging their user asset or liquidity advantages to build more native nested applications—making “matrixification” a clear trend. Examples include:

Curve, originally a DEX, has actively pushed its stablecoin $3CRV, directing incentives toward $3CRV pairs rather than individual stablecoins, and announced a new over-collateralized stablecoin crvUSD last year;

Aave, the top TVL general lending protocol, announced plans in summer 2022 to launch its own over-collateralized stablecoin $GHO;

FRAX, known for its agility, launched Frax Lend in September 2022, allowing users to borrow/mint FRAX from the official contract at market rates instead of the standard minting mechanism—a model similar to MakerDAO’s D3M.

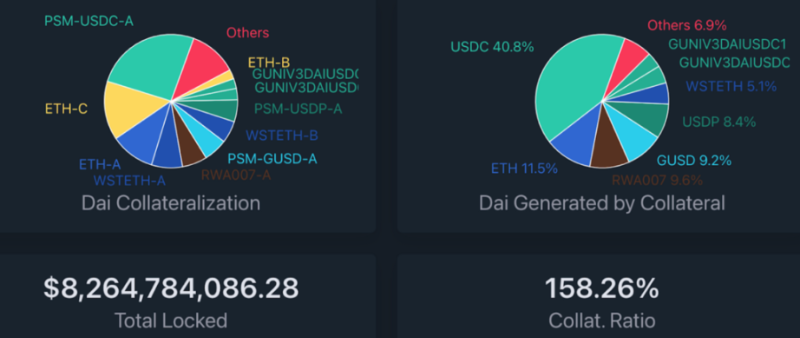

Among these, MakerDAO has long led in TVL. As of February 25, 2023, its vaults hold $8.2 billion in collateral, theoretically convertible into new lending capital. If realized, this could instantly surpass Aave and turn Maker into the largest lending protocol, opening vast new possibilities for its ecosystem expansion.

Currently, GHO and crvUSD are not yet live. We believe that compared to Aave/Curve scaling up their stablecoins (GHO/crvUSD), it is far easier for Maker to scale its lending business because:

1. A new stablecoin faces certain selling pressure (primary minters can only sell or stake), while buying demand is uncertain, heavily dependent on whether Aave/Curve can create sufficient use cases within and beyond their ecosystems. Consider Frax—the second-largest decentralized stablecoin—which despite controlling significant voting power in Curve Wars, has seen its market cap barely exceed a quarter of DAI’s after two years. Even with subsidies artificially driving adoption, growth ceilings remain evident.

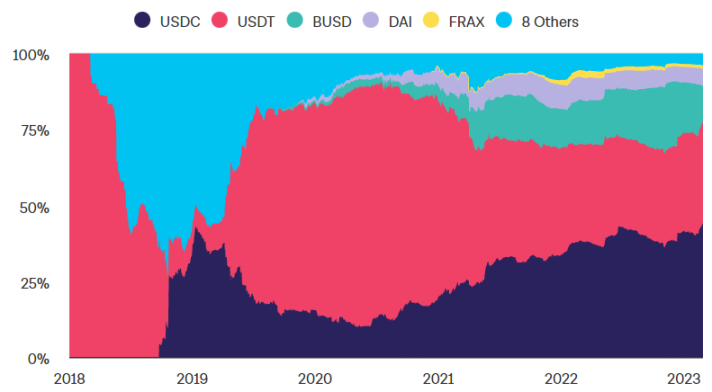

Figure 8: Stablecoin Share on Ethereum, Source:The Block, Trend Research

2. Stablecoin governance is highly complex, requiring specialized expertise. MakerDAO, founded in 2015, is among the earliest and most mature DAOs, gathering expert researchers in DeFi and monetary economics who have successfully navigated DAI through multiple leverage/deleveraging spirals. While Aave/Curve forums are active, unlike lending, stablecoin governance failure can quickly trigger a “death spiral,” crippling the protocol. In this regard, Aave/Curve still have a long way to go.

3. High barriers and narrow windows for liquidity bootstrapping. Beyond offering high staking yields, a new stablecoin must ensure deep liquidity and low slippage when fulfilling its core function as a medium of exchange. This often requires massive early-stage subsidies to incentivize LPs to provide liquidity against other tokens. Before incentives drop below attractive thresholds, sufficient user stickiness must be cultivated—otherwise, LPs exit when yields fall, trading experience deteriorates, and depegs occur frequently, marking the onset of a death spiral.

$MKR Utility Revolution: Liquidity Mining + Burn Volume Doubling

The launch of Spark is not just a product update—it marks the beginning of a major shift in the Maker ecosystem, with the most noticeable marginal improvement for the $MKR token. Its valuation framework must evolve from a single-project token to an ecosystem-level token akin to public chains. For the first time, $MKR gains utility through liquidity mining, potentially offering stakers 12–37% APY. Simultaneously, ecosystem applications will meaningfully expand Maker’s balance sheet, generating an additional $10–20 million in annual revenue under base case assumptions, leading to a 1–3x increase in $MKR burn volume.

General Collateral Lending Expands Asset Inter-Borrowing, Increasing Protocol Revenue Streams

As the flagship DeFi project with strong network effects, Spark’s achievable TVL could rival Aave’s. In Aave V2, ETH and stablecoins dominate asset composition. With a total market size of $5.44 billion and annual revenue of $16.3 million, the combined markets for $USDC, $DAI, $ETH, $WBTC, and $stETH (~$1 billion) represent about one-fifth of total market size.

MakerDAO currently holds $8.2 billion in locked collateral, with $6.6 billion in single-asset (non-LP, non-RWA) value. Total DAI supply stands at 5.2 billion, with 4 billion backed by $USDC. Even releasing just 1/4 of PSM’s $USDC could match Aave’s current TVL.

Figure 9: Distribution of MakerDAO Collateral Vaults, Source:daistats.com, Trend Research

Using Aave’s annual revenue as a benchmark, assuming liquidity mining stimulates migration of 20%/35%/60% of Maker’s existing liquidity (non-LP, non-RWA, $6.6B), Spark’s projected revenue would be:

The official Spark team has also modeled revenue under pessimistic, neutral, and optimistic scenarios. Readers can compare: their bull case exceeds our projections, implying optimism around $5B+ TVL, while their neutral/pessimistic cases seem reasonably aligned:

Data Source:forum.makerdao.com, Trend Research

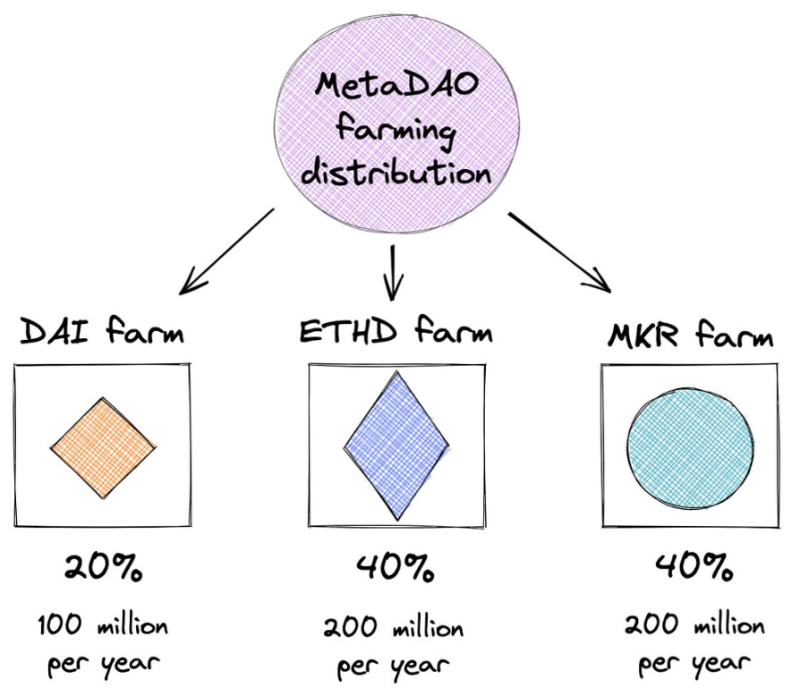

MakerDAO will transition from its current dual-token (MKR/DAI) system to a multi-token architecture, opening liquidity mining for MKR.

It is expected that new MetaDAOs will deploy 2.6 billion MetaDAO (MDAO) tokens upon launch, with 2 billion distributed via liquidity mining—1 billion released in the first two years, halving every two years thereafter. 400 million allocated to contributors, 200 million to the MetaDAO treasury.

Figure 10: Liquidity Mining Reward Allocation, Source:MakerDAO Forum, Trend Research

Liquidity mining distribution: 20% to incentivize DAI demand, 40% to ETHD Vault holders, 40% to $MKR stakers.

Liquidity mining represents a transformative shift in $MKR’s economic model, fundamentally rebalancing its supply-demand dynamics. Prior to this, $MKR served solely as a governance token with limited value capture, resulting in weak demand. Moreover, during debt crises, MKR could be inflated to cover shortfalls, introducing inflationary risks⓫.

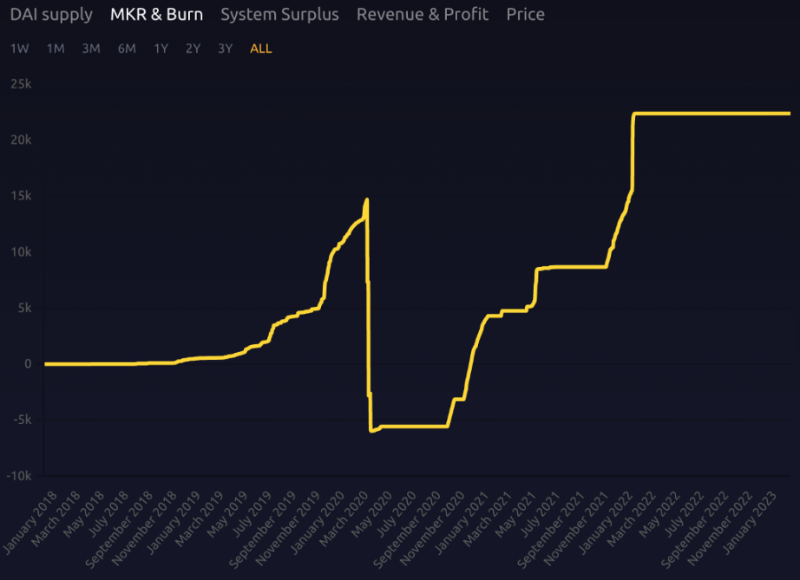

Although surplus revenues can be used to buy back and burn MKR, the effect has historically been modest. Over five years, only 22,000 of 1 million total MKR tokens have been burned—an average annual deflation rate of just 0.4%.

Figure 11: $MKR Issuance & Burn History, Source:Makerburn, Trend Research

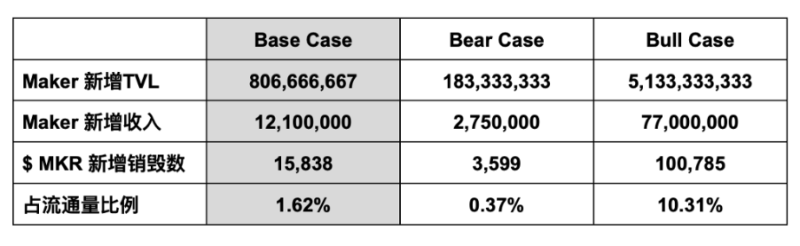

Spark’s lending expansion will bring additional TVL and fee income to MakerDAO. Spark provides simulated revenue figures for reference:

Assuming an average 1.5% stability fee (annualized minting interest) and current $MKR price of $764⓬, the following estimates apply: under base case assumptions, Spark could bring $800 million in new TVL, $12 million in annual revenue, and a 1.6% annual deflation rate—four times the current rate. Even under pessimistic conditions, it might add less than $200 million in TVL and $2.75 million in revenue, still yielding a 0.37% annual $MKR burn rate:

These are linear burn assumptions. In reality, MakerDAO triggers buybacks only when protocol surplus reaches $250 million—currently at $74 million, below the threshold⓭.

With improved revenue structure, MKR’s deflation rate should accelerate. Combined with surging demand driven by newly opened staking opportunities, circulating $MKR is poised to become significantly more valuable.

Building a DeFi Ecosystem Matrix Around a Stablecoin: MakerDAO Evolves from a Single Monetary Protocol Toward a DeFi App Chain.

The goal of a stablecoin is to expand its acceptance and usage. MakerDAO has long pursued partnerships with top-tier DeFi protocols like Aave and Compound. With the MetaDAO model, Maker will build its own DeFi ecosystem matrix centered on the stablecoin, recycling stablecoin value internally and boosting overall $MKR valuation.

For example, simulating $MKR staking to farm Spark tokens at current $764 price, assuming Spark token achieves 35%/20%/60% of A

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News