Can Lido still dominate the Ethereum staking market?

TechFlow Selected TechFlow Selected

Can Lido still dominate the Ethereum staking market?

If centralized exchanges dominate the ETH staking market, it would undermine Ethereum's goal of building a decentralized network.

Author: Momir, IOSG Ventures

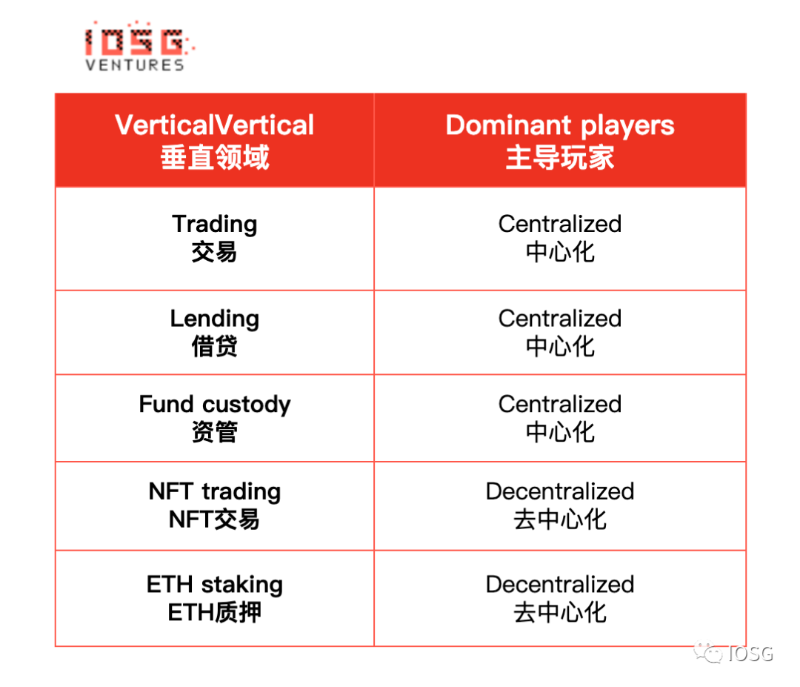

Market Opportunity

Is Liquid Staking a Winner-Takes-All Market?

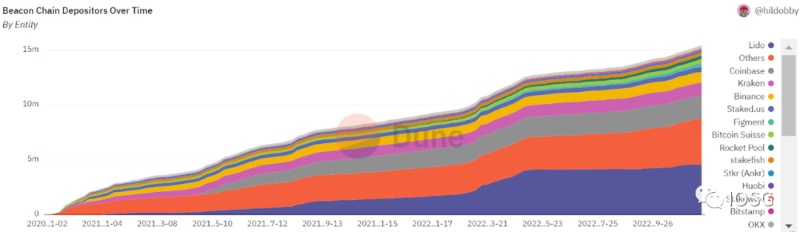

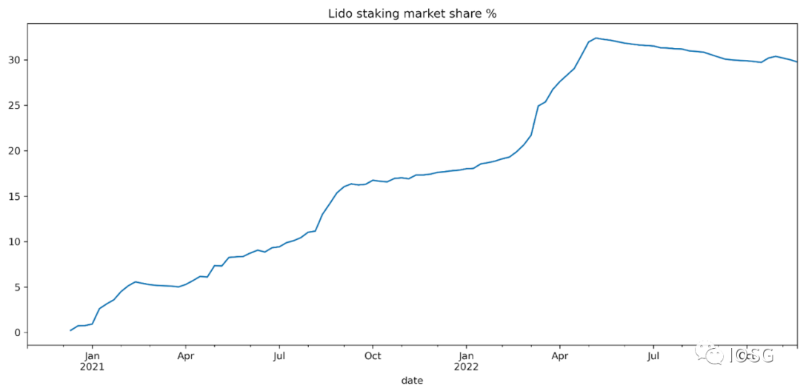

If centralized exchanges dominate the ETH staking market, it would contradict Ethereum's goal of building a decentralized network. As shown in the chart below, Lido is the leading project in the ETH staking space, holding approximately 30% of the market share.

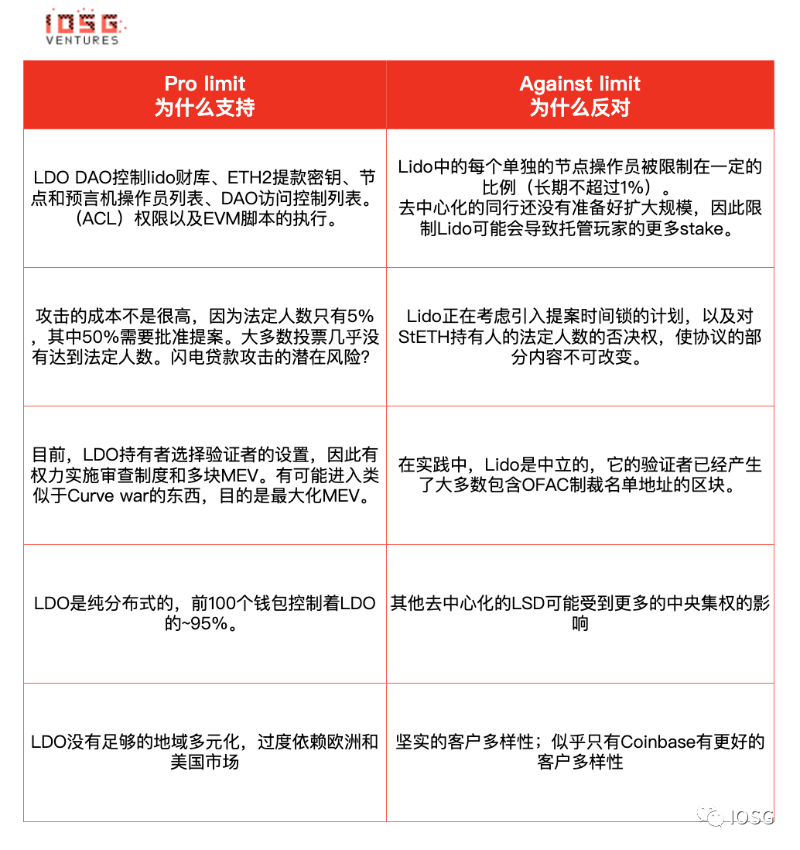

Nonetheless, there are voices within the community calling for limits on Lido’s market share. For instance, Vitalik has suggested that staking providers—both centralized and decentralized—should self-impose caps on the amount of stake they control, proposing 15% as an upper threshold.

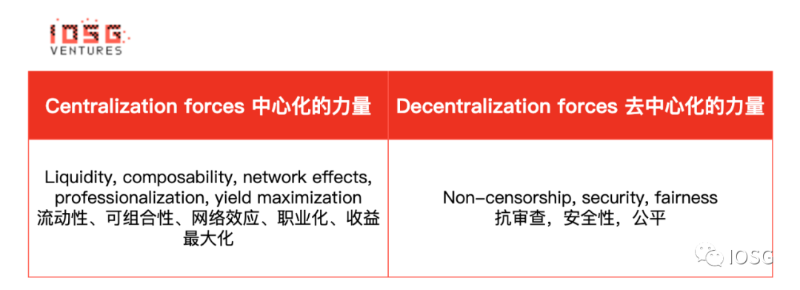

Absent ideological concerns (i.e., decentralization), due to liquidity, composability, network effects, specialization, and yield maximization, this could very well become a winner-takes-all type of market.

How Much Market Share Can Lido Capture?

The main arguments for and against limiting a single project's market share are summarized below:

Summary:

1: Lido will not impose any self-limiting measures.

2: In my opinion, a Lido fork is inevitable, but how much market such a fork can capture is hard to predict—it depends on many factors such as LDO governance actions, timing, governance innovations from the fork, etc.

3: Given competition from both decentralized and centralized players, as well as community pressure, Lido is expected to capture up to 50% of the staking market under the best-case scenario.

4: The most realistic outcome is that Lido maintains its current position with around 30% market share. A significant portion of Lido depositors may have joined primarily for farming rewards, and a non-trivial amount of ETH might be leveraged; these users are likely to withdraw first once withdrawal functionality is enabled.

5: At the same time, we also expect inflows from new depositors when withdrawals are enabled. This is because LSDs (liquid staking derivatives) would trade closer to their peg, reducing concerns about LSD liquidity, as users can convert back to ETH within 27 hours.

Therefore, enabling withdrawals will:

- Allow speculators (yield farmers, leveraged users) to withdraw their deposits, yet increase overall market confidence and make staking more attractive.

- Reduce the dominant LSD’s advantages relative to other solutions, due to lower opportunity costs of staking.

- Enable CEXs to potentially offer products allowing instant withdrawals (without waiting 27 hours), winning users on convenience.

Using the following formula, we can roughly calculate the market’s implied expectation:

*(1/aave_earn * stETH_discount)*365

The current pricing of stETH suggests that withdrawals will be enabled in approximately 460 days.

A Rapidly Growing Market

Among all PoS chains, Ethereum currently has the lowest staking ratio. This is likely due to the following reasons:

Direct staking at the protocol level is not available, forcing users to accept additional risks from smart contracts or custodial solutions

Staked ETH cannot be redeemed

Ethereum is a more mainstream asset with a more decentralized community than any other PoS token, but also attracts greater attention from speculators such as hedge funds

Over time, as new smart contracts are battle-tested and withdrawal certainty increases, we can expect a larger portion of ETH to be staked. However, I would be surprised if more than 50% of ETH becomes staked.

ETH holders’ decision-making process looks like this: Should I invest? If so, should I use a validator pool? If so, should I choose a decentralized option? If so, should I pick Lido?

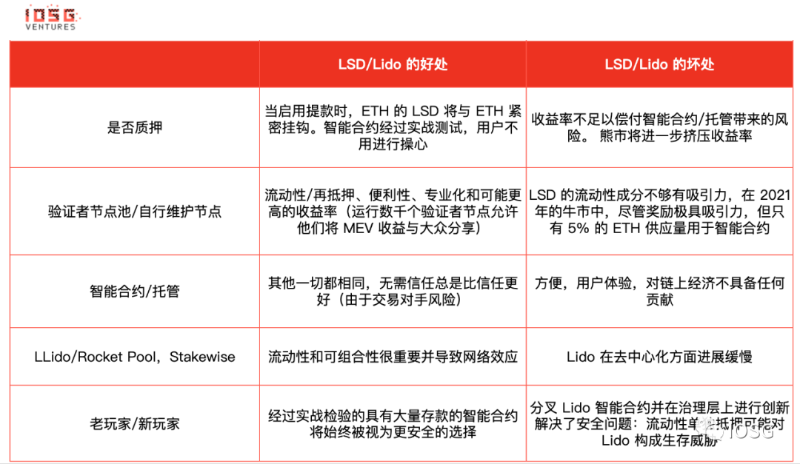

Importance of Liquidity in LSDs

Some argue that the network effect created by the most liquid staking derivative—stETH—and its integration with major DeFi protocols may allow Lido to win the entire market.

For example, if you want a liquid staking derivative, you might prefer:

One with the best market liquidity and ease of exit.

Deep liquidity makes the LSD viable as collateral in many DeFi protocols, offering more use cases for holders.

More use cases enhance the token’s liquidity.

As previously noted, liquidity is even more critical now when withdrawals are not possible, due to high opportunity costs.

But overall, how interested are users in re-staking? Or more simply, are users interested in using ETH in on-chain applications?

We’ve experienced bull markets driven by DeFi, NFTs, and gaming projects distributing massive incentives to attract new users. Yet, despite all these use cases and incentives, only a small fraction of ETH is used in smart contracts.

According to Nansen, in October 2021, usage was about 4.5 million wETH (users must wrap their ETH to participate in the on-chain economy), less than 4% of total ETH supply.

Another point, while not overly concerning but worth noting: not all DeFi protocols support rebase tokens, which is why Lido effectively has two standards: stETH and wrapped stETH (the latter typically trades at a premium since it accrues rewards that unlock upon unwrapping).

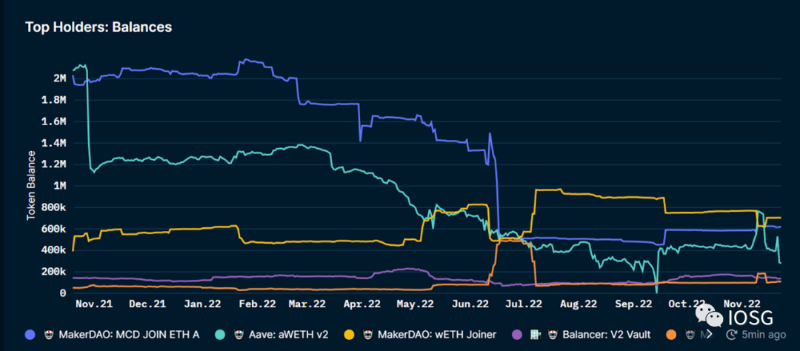

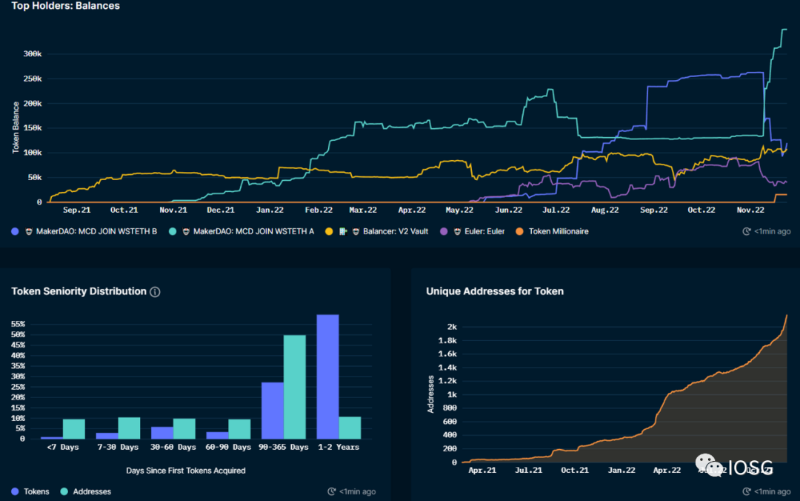

The chart below shows that some of the largest DeFi protocols do not support the stETH standard, which is why we see wrapped stETH being used in MakerDAO, Balancer, Euler, etc. While wrapping and unwrapping isn’t a major barrier, it does impact user experience.

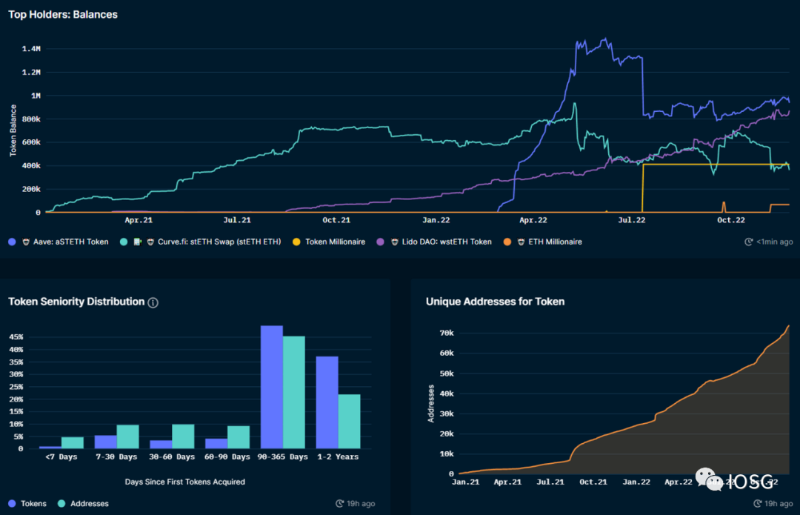

On the other hand, most stETH tokens are held on AAVE and Curve.fi.

Adoption of stETH

LDO vs ETH

To a large extent, LDO price is influenced by Ethereum activity and ETH price.

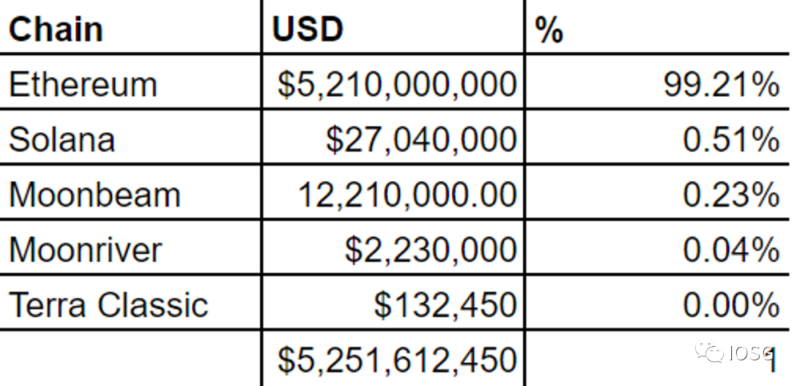

Ethereum is Lido’s target market. Over 99% of Lido’s TVL is locked on Ethereum.

Lido fees come from Ethereum inflation rewards and transaction priority fees.

Lido’s revenue equals 5% of total staking rewards collected on Lido (90% distributed to stETH providers, 5% to node operators).

Ethereum distributes approximately 1,700 ETH per day as staking rewards (about 0.5% of ETH supply), with roughly 30% going to Lido (based on its market share, assuming ceteris paribus).

While Lido is highly dependent on Ethereum fundamentals, we observe that even backed by ETH value, Lido has experienced significant volatility. This may reflect market repricing of Lido’s positioning within the Ethereum ecosystem and estimated market size of the LSD vertical.

Ethereum Inflation Rewards

Since ETH inflation constitutes a large portion of Lido’s income, understanding its dynamics is important.

Using data points from https://ultrasound.money/, we estimate that a 1% increase in TVL reduces base reward APY by 0.41%.

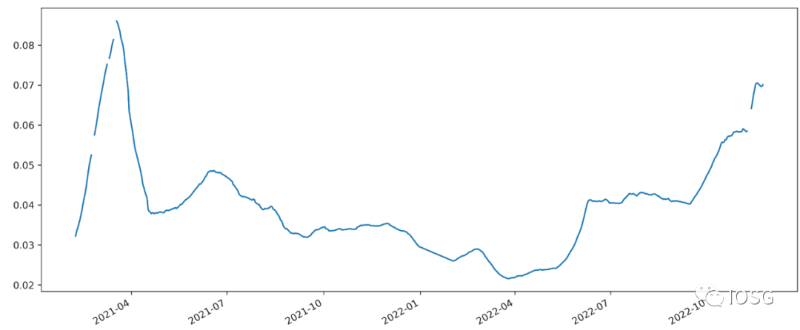

Lido 30-Day Staking Reward APY %

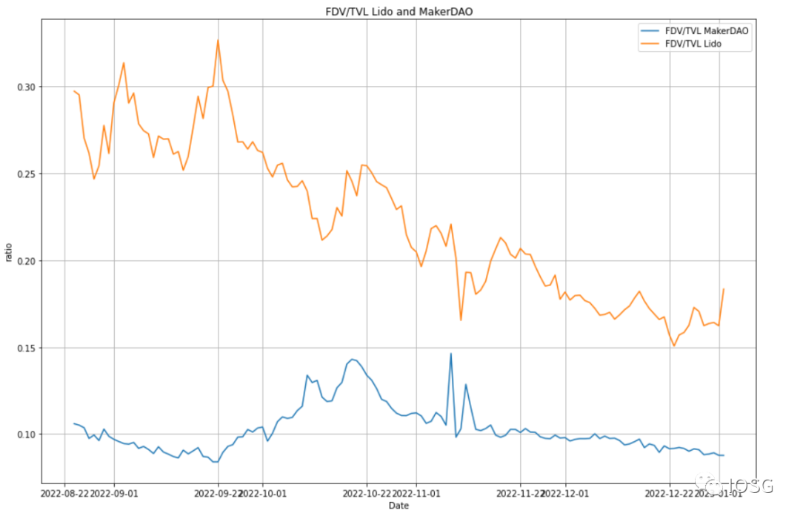

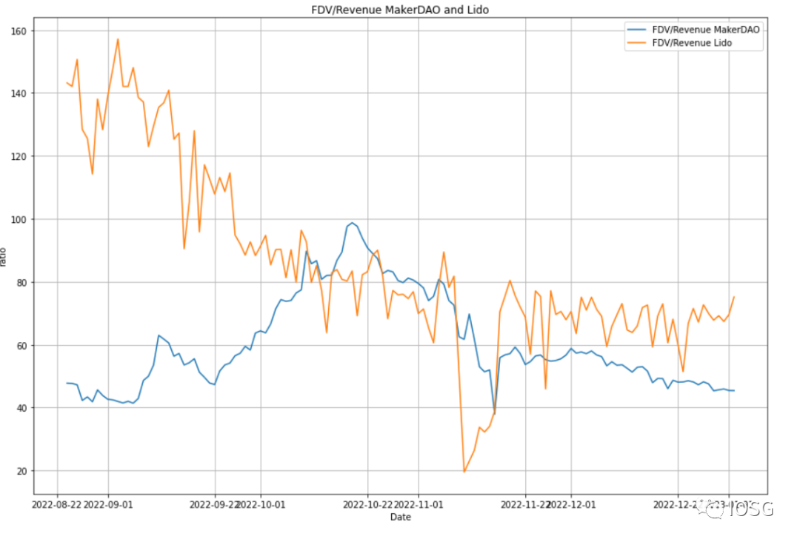

Competitor Benchmarking

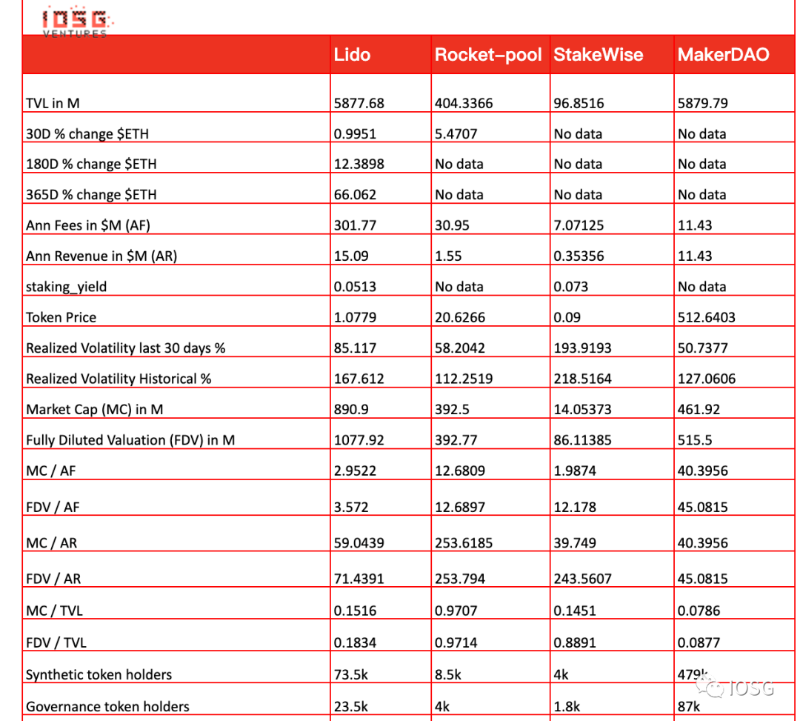

Quantitative Comparison: To establish a mature benchmark competitor, we include MakerDAO in the table, as LSDs are conceptually closest to synthetic assets, with stETH being a form of synthetic asset. I wouldn’t be surprised if Lido one day decides to support minting a synthetic stablecoin backed by staked ETH.

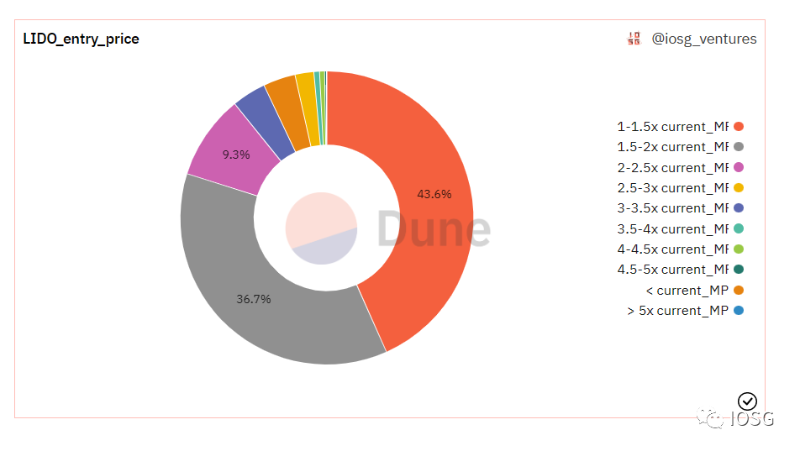

Token Health (Behavioral Finance / Market Psychology)

Note: This data lacks insights into LDO token usage on centralized exchanges

How to interpret this data?

Honest answer: Unclear.

Possible intuition – Disposition effect, where investors tend to sell winning positions too early and hold losing ones too long.

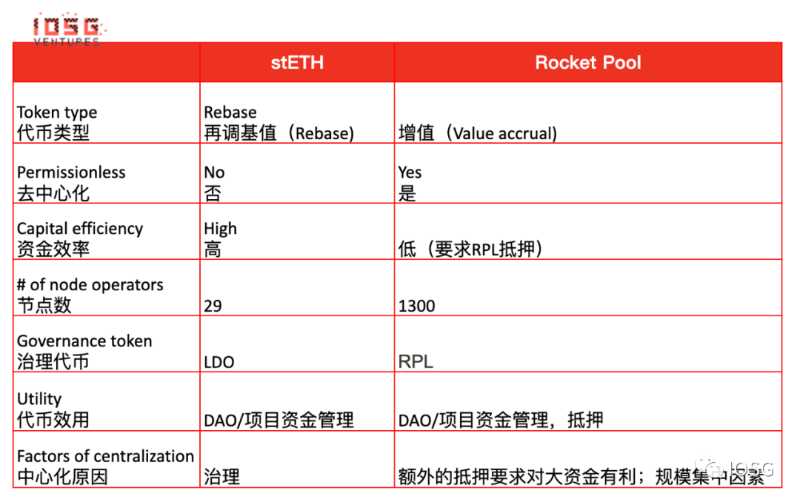

Qualitative Comparison

Conclusion

We estimate that staked ETH will account for at most 50% of total ETH supply.

Due to community challenges and emerging competitors, we reasonably estimate Lido’s liquid staking market share to settle around 35%.

After Lido enables fluid withdrawals, we expect leveraged traders and yield farmers to withdraw ETH, although withdrawals overall should create a more favorable environment for staking interest. Smooth withdrawals will also diminish the value proposition of LSDs.

Withdrawals are likely to go live about a year from now.

Lido Advantages

Leading liquid ETH staking project with first-mover advantage and strong moat.

Superior security, liquidity, composability, network effects, and specialization/efficiency compared to competitors. Lido is likely to remain the primary decentralized liquid staking platform.

Historically censorship-resistant.

Transparent roadmap with a track record of execution and development.

Lido Disadvantages

If Lido does not introduce certain limits, the cost of governance attacks would not be high.

Risk of validators participating in LDO token wars to manipulate reward-sharing mechanisms.

LDO token is not sufficiently decentralized.

Prolonged bear markets will lead to low staking yields and a smaller proportion of staked ETH.

The importance of liquidity may be overestimated: Many ETH holders simply aren’t interested in re-staking or using on-chain assets; once withdrawals are enabled, LSDs will lose part of their value proposition.

A Lido fork is inevitable; its threat level remains uncertain.

Lido’s addressable market size is largely determined by ETH’s market cap. Lido is essentially a leveraged bet on ETH, but on a risk-adjusted basis, ETH may be a better investment than Lido.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News